|

市场调查报告书

商品编码

1437500

汽车自动升降门:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Automotive Automatic Liftgate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

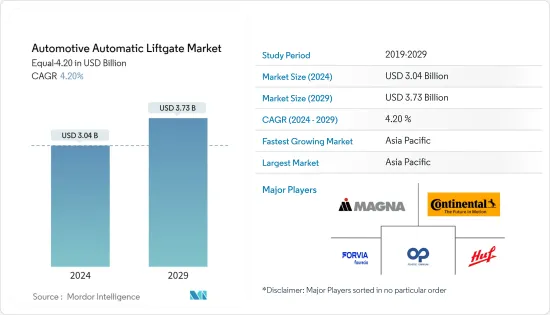

以Equal-4.20 计算的汽车自动提升门市场规模预计将从2024 年的30.4 亿美元增长到2029 年的37.3 亿美元,预测期内(2024-2029 年)复合年增长率为4.20%,预计将增长到2029 年的37.3 亿美元。 。

从中期来看,提高乘客舒适度是小客车外饰市场最重要的考量之一。组件必须需要最少的人力并提供最大的舒适度。因此,这方面得到了持续的发展。

消费者对汽车安全功能的趋势不断上升、技术进步不断进步以及对豪华车的需求激增预计将在预测期内主要推动市场发展。

零件供应商正在加紧研究各种车辆外饰新技术,这些新技术具有多种新功能,可适应乘客和驾驶因素不断变化的要求。这些尾门解决方案透过减轻车辆重量和改善燃油消费量来提高车辆效率。金属化涂料进一步增强了这些特性,金属化涂料可产生类似铬的外观,而不会增加使用金属本身时会产生的额外重量。这种新的涂层技术比电镀铬便宜约 5-20%,总重量减轻了 10-20%。

动态也是尾门的一个重要方面。如今,在主动后扰流板和侧扰流板的帮助下,尾门的空气动力学性能得到了改善,可以更好地将空气传输到车顶。新型尾门将风阻係数提高了3-4%,可减少二氧化碳排放1克/公里。

汽车自动提升门市场趋势

SUV推动市场成长

可能刺激汽车自动尾门产业需求的一个因素是今年SUV在小客车中的份额不断增加。主要汽车OEM和外饰零件製造商正在花费数百万美元用于未来汽车外饰的研发。

SUV细分市场预计将维持较高的复合年增长率。小客车销量的下降速度与 SUV 销量的成长速度大致相同,因为该细分市场的销量增幅高于其他小客车细分市场。

SUV 兴起的原因包括弹性、货物容量、机动性、驾驶座椅视野良好以及易于进入乘客舱。大多数现代 SUV 属于跨界车类别,它们是更大、更圆润的车辆,而不是美国基于皮卡车的运动公共事业车。

SUV 变得越来越受欢迎,因为它们比掀背车或轿车提供更多的空间和舒适度。大多数SUV都有混合版本,电动版本也越来越受欢迎。这是因为SUV对于注重环保驾驶的驾驶者来说也是一个不错的选择。许多最新车型都提供混合和全电动式选项。

消费者现在了解其车辆的剩余价值、品质融资费用、可用性、支付的价格,在某些情况下,也了解交易结束时卖方的报酬率。这种认可改变了动态,并允许客户利用他们的见解,从而增加选择电动运动休旅车的可能性。考虑到 Majo 地区购买二手 SUV 的人群中二手车种类繁多,该市场在预测期内可能会大幅成长。

随着全球范围内的上述发展,未来几年对 SUV 的需求可能会增加,预计市场在预测期内将大幅增长。

亚太地区可望引领市场

亚太地区是世界主要汽车生产国之一。中国、印度和日本是该地区市场的主要经济体,预计也将影响全球市场。儘管受新能源车款影响,整体汽车销售市场情绪疲软,但2022年各地区汽车销售仍呈现稳定成长轨迹。

该地区是许多全球和本地汽车製造商和层级参与者的关键市场,汽车外饰零件製造商与OEM製造商合作,为未来车辆开发下一代举升式车门。

中国在汽车工业吞吐量和汽车产量方面在亚太地区占据主导地位。该地区是主要OEM、汽车供应商和汽车零件製造商的所在地,在全球范围内保持稳定的供应。 2022年中国汽车销售总量为26,863,745辆,与前一年同期比较%。

车辆排放气体水准的上升和对环保车辆的需求增加预计将在预测期内推动市场扩张。该全部区域对电动车不断增长的需求可能会在未来几年为市场创造利润丰厚的机会。

印度公司正在进行研发活动,以开发新产品,这将对预测期内目标市场的成长产生正面影响。例如,

2022年8月,印度最大汽车製造商马鲁蒂铃木宣布将于年终推出首款电动车。

由于汽车安全性和舒适性的提高而导致汽车销量增加,预计未来几年对自动尾门的需求将会增加。

汽车自动尾门产业概况

几家主要企业主导着汽车自动尾门市场,包括麦格纳国际公司、佛吉亚公司、彼欧公司和大陆集团。先进技术、感测器使用的增加、研发计划投资的增加以及电动车市场的成长等因素正在显着推动市场发展。为了给车主提供更便利的体验,领先的汽车自动尾门製造商正在开发新技术,以实现更轻、更方便的尾门。例如,

2023 年 10 月,塔塔汽车有限公司在印度推出了塔塔 Harrier Facelift。新车型配备了电动尾门。透过此次发布,该公司增强了即将推出的车型的安全性和舒适性。

2023 年 10 月,义法半导体宣布推出一款新型汽车电源管理 IC,可简化各种组件的车身控制器设计。

2022年3月,吉普印度推出了专为印度市场开发的全新三排SUV Meridian SUV。新车型配备了电动尾门。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 豪华车销售增加

- 市场限制因素

- 与系统相关的高成本

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代产品的威胁

- 竞争公司之间敌对的强度

第五章市场区隔(以以金额为准的市场规模-美元)

- 按车型

- 掀背车

- SUV

- 轿车

- 其他的

- 依材料类型

- 金属

- 复合材料

- 依销售管道类型

- OEM

- 售后市场

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东和非洲

- 北美洲

第六章 竞争形势

- 供应商市场占有率

- 公司简介

- Faurecia SE

- Magna International Inc.

- Plastic Omnium SE

- Huf Hulsbeck &First GmbH &Co.KG

- Continental AG

- STMicroelectronics NV

- Autoease Technology

- Brose Fahrzeugteile SE &Co. KG

- Aisin Seiki Co., Ltd.

- Stabilus SE

- Johnson Electric Holdings Limited.

第七章市场机会与未来趋势

The Automotive Automatic Liftgate Market size in terms of Equal-4.20 is expected to grow from USD 3.04 billion in 2024 to USD 3.73 billion by 2029, at a CAGR of 4.20% during the forecast period (2024-2029).

Over the medium term, increasing passenger comfort has become one of the most important considerations in the passenger car exterior market. Components should take as little human effort as possible and provide the maximum level of comfort. As a result, consistent development is taking place in this regard.

Growing consumer trends toward safety features in vehicles, rising technological advancements, and a surge in demand for luxurious vehicles are likely to primarily drive the market during the forecast period.

Component suppliers are working intensively on various new technologies for vehicle exteriors with a variety of new functionalities that can be adapted to the continuously changing requirements of passengers and drivers. These liftgate solutions improve vehicle efficiency by reducing the weight of the vehicle and improving fuel consumption. Such properties are further enhanced by metalized paint that creates a chrome-like appearance without the additional weight in case of using the metal itself. This new paint technique is around 5 to 20% less expensive than chrome electroplating and reduces overall weight by 10 to 20%.

Aerodynamics is also a key aspect of the tailgate; nowadays, the tailgate aerodynamics are improved with the help of an active rear spoiler and side spoiler that transfer the air better over the car roof. The new tailgates can improve the drag coefficient by 3-4% and also reduce CO2 emissions by 1 g per km.

Automotive Automatic Liftgate Market Trends

SUV Will Fuel The Growth Of The Market

The factor that is likely to fuel the demand for the automotive automatic liftgate industry is the increasing share of SUVs in passenger cars in the current year. Leading automotive OEMs and exterior component manufacturers are spending of huge amount on research and development of exteriors for future vehicles.

The SUV segment is expected to register a high CAGR; on account of the rising sales of this segment over other passenger cars segment, passenger-vehicle sales declined at roughly the same rate as SUV sales have risen.

Some of the reasons for the rise of SUVs are flexibility, payload-carrying ability, drivability, commanding view from the driver's seat, and ease of cabin access. Most of the latest SUVs come under the crossover category, which are larger, more bulbous cars rather than the pickup truck-based sports utilities in the United States.

The rise in popularity of SUV vehicles as the vehicle offers extra space and provides better comfort as compared to hatchback and sedan vehicles. Most SUVs come in hybrid and electric versions are gaining popularity as SUVs can also be a great choice for drivers who are trying to be more eco-friendly. Many of the latest models are offered in hybrid and all-electric options.

Consumers are now aware of the vehicle's residual value, quality finance charges, availability, the price paid, and, in some cases, the seller's profit margin in a closing transaction. This awareness has changed the dynamics and allowed them to capitalize on customer insight, which in turn is likely to opt for electric sport utility vehicles. Considering the wide range of used cars among people who bought a used SUV in the Majo region, which in turn is likely to witness major growth for the market during the forecast period.

With the development mentioned above across the globe, the demand for sport utility vehicles is likely to grow in the coming years, which in turn is anticipated to witness major growth for the market during the forecast period.

Asia Pacific is Anticipated to Lead the Market

The Asia-Pacific is among the leading automobile producers in the world. China, India, and Japan are the major economies in the regional market that are anticipated to influence the global market, too. Regional automotive sales reflected a steady growth trajectory in 2022 despite weak market sentiment in overall car sales due to new energy vehicles.

The region is the main market for many global as well as local car manufacturers and tier players, the automotive exterior component manufacturers are a partnership with OEMs to develop next-generation liftgates for their future vehicles.

China holds the dominating hand in the Asia-Pacific region regarding auto industry throughput and vehicle production. Region houses leading OEM, auto suppliers, and automotive component manufacturers maintain steady supply across the globe. In 2022, the total number of vehicles sold in China stood up at 26,863,745 units as compared to 26,274,820 Units in 2021, registering a year-on-year growth of 2.2%.

Rising levels of vehicular emissions and increased demand for environmentally friendly automobiles are likely to drive market expansion over the forecast period. The rise in demand for electric vehicles across the region is likely to create a lucrative opportunity for the market in the coming years.

Indian companies are working on research and development activities to develop new products that would positively impact the target market growth during the forecast period. For instance,

In August 2022, India's largest automaker, Maruti Suzuki, confirmed that it shall soon introduce its first electric vehicle by 2025 end.

An increase in vehicle sales with the rise in safety and comfort features in vehicles is likely to enhance the demand for automatic liftgates in the coming years.

Automotive Automatic Liftgate Industry Overview

Several key players, such as Magna International Inc., Faurecia SE, Plastic Omnium, Continental AG, and others, dominate the automotive automatic liftgate market. Factors like advanced technology, more use of sensors, growing investment in R&D projects, and a growing market of electric vehicles highly drive the market. To provide a more convenient experience for the car owner, major automotive automatic liftgate manufacturers are developing new technology for lighter and more convenient liftgates. For instance,

In October 2023, Tata Motor Ltd introduced the Tata Harrier Facelift in India. The new facelift model consists of the power liftgate. Through this launch, the company enhanced its safety and comfort features in its upcoming models.

In October 2023, STMicroelectronics N.V. introduced new automotive power-management ICs that simplify the design of car-body controllers for various components.

In March 2022, Jeep India introduced the Meridian SUV, an all-new 3-row SUV developed for the Indian market. The new models come with features such as a power liftgate.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rise in Sale of Luxury Vehicles

- 4.2 Market Restraints

- 4.2.1 High Costs Associated With the System

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Vehicle Type

- 5.1.1 Hatchback

- 5.1.2 Sports Utility vehicle

- 5.1.3 Sedan

- 5.1.4 Other Vehicle Types

- 5.2 By Material Type

- 5.2.1 Metal

- 5.2.2 Composite

- 5.3 By Sales Channel Type

- 5.3.1 Original Equipment Manufacturers (OEM)

- 5.3.2 Aftermarket

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Faurecia SE

- 6.2.2 Magna International Inc.

- 6.2.3 Plastic Omnium SE

- 6.2.4 Huf Hulsbeck & First GmbH & Co.KG

- 6.2.5 Continental AG

- 6.2.6 STMicroelectronics N.V.

- 6.2.7 Autoease Technology

- 6.2.8 Brose Fahrzeugteile SE & Co. KG

- 6.2.9 Aisin Seiki Co., Ltd.

- 6.2.10 Stabilus SE

- 6.2.11 Johnson Electric Holdings Limited.