|

市场调查报告书

商品编码

1437938

浮体式海上风电:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Floating Offshore Wind Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

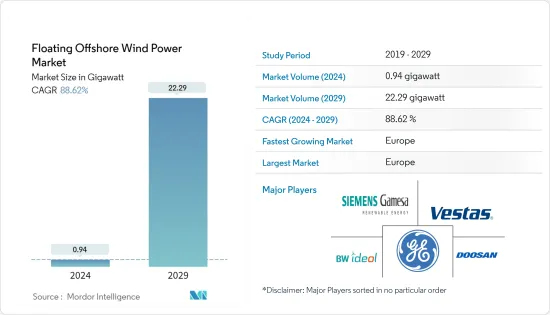

2024年浮体式海上风电市场规模预计为0.94吉瓦,预计到2029年将达到22.29吉瓦,在预测期(2024-2029年)复合年增长率为88.62%。

儘管 COVID-19感染疾病对 2020 年市场产生了负面影响,但已达到疫情前的水平。

主要亮点

- 从长远来看,随着越来越多的人希望利用离岸风力发电,浮体式海上风电市场可能会成长。此外,深化离岸风力发电计划被视为一项创新技术,可以利用更深水域的强风来推动市场成长。

- 另一方面,天然气和太阳能发电等清洁发电方式的使用正在增加。从太阳能或天然气中获取电力是更清洁的能源产出方式之一,因此随着越来越多的人使用这些方法,对风能的需求可能会放缓。

- 海上风力发电在发展中国家和未开发市场也越来越受欢迎。这可能会在预测期内为浮体式海上风电市场创造成长机会。

- 欧洲地区占市场最大份额,预计未来五年复合年增长率最高。这一增长得益于离岸风力发电投资的快速增加,以及挪威、英国和法国等该地区国家製定了支持风电的政策。

浮体式海上风力发电市场趋势

过渡水域(30m至60m深)预计将成长

- 浮体式海上风力发电机(FOWT)技术在过渡水深(30-60 m)更加发达,因为更深的水深使计划经济性更加有利。驳船变体是最具商业性可行性的浮体式风力发电机设计。此型号适用于 30 m 以上高度作业,具有浮体式基础中最浅的吃水深度。驳船式浮体式风力发电机的占地面积为平方公尺,而其他设计则采用月池来减少波浪载荷带来的应力。据GWEC称,典型的6兆瓦浮体式驳风力发电机重量在2,000吨至8,000吨之间。然而,BW Ideol 凭藉其倾卸池浮体浮动下部结构技术,是唯一部署兆瓦级驳船型 FOWT 的公司。

- 由于水深较浅,与固定基地技术相比,FOWT技术从商业角度来看实用性较差。因此,在预测期内,驳船技术预计将占整个 FOWT 市场的一小部分。美国环保署称,截至2021年,全球运作中的驳船FOWT容量仅为5MW。据宣布,该驳船的 FOWT 容量占全球未来计划宣布的所有离岸风基础技术的 2.1%。

- 大多数公司都在尝试销售可在深水中使用的 FOWT 设计。然而,一些半潜式技术也可以在瞬时深度使用。多种基于半潜式设计的商用 FOWT 型号即使在过渡深度也能发挥作用。其中一些模型最初用于实验计划,而其他模型则经过改编用于商业企业。

- EolMed计划是法国第一个位于地中海的浮体式风电场。 2022年5月,TotalEnergies宣布计划开始建设,预计2024年运作。该计划位于水深62公尺处,由三个锚定在海底的10MW浮体式涡轮机组成。涡轮机采用带有阻尼池的驳船设计。该计划将由 Quadran Energies Marines、Ideol、土木工程公司 Bouygues Travaux Publix 和风力发电机製造商 Senvion 管理。

- 在过渡深度区域,固定式和浮体式风力发电机风力发电机都可以工作,但驳船设计在商业性最可行。

- 2010 年至 2021 年间,全球风力发电平均装置成本从每度电 4,876 美元下降到 2,858 美元,下降了 41%。在 2011 年的高峰期,全球加权平均装置成本为每千瓦 5,584 美元,是 2021 年价值的两倍。在欧洲,2020年至2021年间,新委託的海上计划的加权平均LCOE从0.092美元下降了29%。 /kWh 至 0.065 美元/kWh。计划规模效益使总安装成本与前一年同期比较减了25%,新计画的加权平均容量係数从2021年的42%增加到48%。

- 大多数过渡性 FOWT计划可能会在欧洲进行,特别是在英国、斯堪地那维亚和法国,这些国家的大型计划正处于规划阶段。在预测期内,该细分市场的大部分发展可能会发生在这些地区。

欧洲主导市场成长

- 欧洲占全球离岸风力发电电场的最大份额。根据欧盟统计,欧洲占全球离岸风力发电电场的四分之一。这个国家(主要是北海国家)很可能主导离岸风力发电市场。

- 全球约85%的离岸风力发电电场位于欧洲水域。欧洲地区,特别是北海地区各国政府,制定了在其领海安装离岸风力发电的雄心勃勃的目标。

- 预计到 2022 年,欧洲将安装 112 兆瓦的浮体式海上风电,其中英国、法国、挪威、爱尔兰和西班牙是该地区最大的市场。

- 2022 年 8 月,Cerulean Winds 与 PING Petroleum UK 签署了一项主要由离岸风电供电的海上石油和天然气设施协议。根据协议,Cerulean Winds 及其层级工业合作伙伴集团将交付大型浮体式海上石油和天然气设施。风力发电机透过电缆连接到 Ping Petroleum 的浮体式生产和储存船。该计划预计将于 2025 年运作。津贴使该计划能够透过浮体式海上风电示范计划交付给 Cerulean Winds。

- 2022年2月,挪威宣布计画首次竞标离岸风力发电。此次竞标定于今年下半年进行,竞标将寻求开发至少 1.5 吉瓦的离岸风力发电容量,为该国供电,随后竞标将提供更多电力出口到欧洲。经济。

- 在预测期内,这些趋势将使欧洲成为浮体式海上风电场业务的最佳开展业务地点。

浮体式海上风电产业概况

浮体式海上风电市场较为分散。市场主要企业包括(排名不分先后)通用电气公司、斗山能源、西门子歌美飒可再生能源、BW Ideaol SA、维斯塔斯风力系统公司等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查范围

- 市场定义

- 调查先决条件

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2028年浮体式海上风电潜在设置容量预测(兆瓦)

- 主要计划资讯

- 现有主要计划

- 即将进行的计划

- 最新趋势和发展

- 政府政策法规

- 市场动态

- 促进因素

- 抑制因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 按水深(仅限定性分析)

- 浅水(水深小于30m)

- 渐进深度(30 m 至 60 m 深度)

- 深海(深度超过60m)

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 南美洲

- 中东和非洲

第六章 竞争形势

- 合併、收购、合作和合资企业

- 主要企业采取的策略

- 公司简介

- Vestas Wind Systems AS

- General Electric Company

- Siemens Gamesa Renewable Energy SA

- BW Ideol AS

- Equinor ASA

- Marubeni Corporation

- Macquarie Group Limited

- Doosan Enerbility Co. Ltd.

第七章市场机会与未来趋势

The Floating Offshore Wind Power Market size is estimated at 0.94 gigawatt in 2024, and is expected to reach 22.29 gigawatt by 2029, growing at a CAGR of 88.62% during the forecast period (2024-2029).

Though the COVID-19 pandemic negatively impacted the market in 2020, it reached pre-pandemic levels.

Key Highlights

- Long-term, the floating offshore wind power market is likely to grow because more people want to use offshore wind power. Also, increasing the water depth of offshore wind power projects is seen as a game-changing technology that can take advantage of the strong winds in deeper waters and help the market grow.

- On the other hand, more and more gas and solar power, which are both clean ways to make electricity, are being used. Since getting power from solar and gas is one of the cleaner ways to make energy, more people using these methods is likely to slow the demand for wind power.

- Also, offshore wind energy is becoming more popular in developing and untapped markets. This is likely to create growth opportunities for the floating offshore wind power market during the forecast period.

- The European region has the biggest share of the market and is also expected to register the highest CAGR over the next five years. This growth is due to the fast rise in offshore wind power investments and the fact that countries in this area, like Norway, the UK, and France, have policies that support wind power.

Floating Offshore Wind Market Trends

The Transitional Water (30 m to 60 m Depth) Segment is Expected to Grow

- Due to the greater water depth and favorable project economics, floating offshore wind turbine (FOWT) technology is more developed in transitional water depths (30-60 m). The barge variant is the most commercially viable floating wind turbine design at shallow depths. This model is appropriate for activities higher than 30 m and has the shallowest draft of any floating foundation. Barge-style floating wind turbines have a square footprint, while other designs incorporate a moonpool to lessen stresses brought on by wave-induced loads. A typical 6-megawatt floating barge wind turbine weighs between 2000 and 8000 tons, according to GWEC. However, BW Ideol, with its Damping Pool Barge Floating Substructure Technology, is the only company that has deployed barge-type FOWT at the MW scale.

- Since the water depth is shallower, FOWT technology is less practical from a business point of view than fixed-base technology. So, during the period of the projection, barge technology is expected to make up a small part of the FOWT market as a whole.The US EPA claims that only 5 MW of barge FOWT capacity was operating globally as of 2021. Just 1932 MW of FOWT capacity on barges, or 2.1% of all announced offshore wind substructure technologies for future projects around the world, were announced.

- Most companies attempt to market FOWT designs that can be used in deeper waters. However, some semi-submersible technologies can also be used at transitional water depths. They can function at transitional depths due to several commercial FOWT models that are built on the semi-submersible design. A few of these models were initially used in experimental projects, while others were modified for use in ventures for profit.

- The EolMed project is France's first floating pilot wind farm in the Mediterranean Sea. In May 2022, TotalEnergies announced the start of the project's construction, which is expected to be operational by 2024. The project will consist of three 10 MW floating turbines on the bathymetry of the 62-meter depth and anchored to the seabed. The turbines will use a barge design with a damping pool. Quadran Energies Marines, Ideol, Bouygues Travaux Publics, a company that specializes in civil engineering, and Senvion, a manufacturer of wind turbines, will run the project.

- In the area of transitional depth, both fixed and floating wind turbines can work, but the barge design is the most commercially viable.

- Between 2010 and 2021, the global average installed cost of wind energy decreased by 41%, from USD 4,876 per kW to USD 2,858/kW. At its peak in 2011, the global weighted average installed cost was USD 5,584 per kW, which was twice its value in 2021. In Europe, the weighted average LCOE of newly commissioned offshore projects decreased by 29% between 2020 and 2021, from USD 0.092/kWh to USD 0.065/kWh. Driven by project economies of scale, there was a 25% reduction in total installed costs year-on-year and an increase in new projects' weighted average capacity factor from 42% to 48% in 2021.

- Most of the FOWT projects in transitional depths are likely to be in Europe, especially in the United Kingdom, Scandinavia, and France, where large projects are in the planning stages. During the forecast period, most of the deployments in this market segment are likely to happen in these regions.

Europe to Dominate the Market Growth

- Europe holds the largest share of offshore wind energy installations globally. According to the European Union, Europe represents a quarter of global offshore wind installations. The country (primarily North Sea countries) is likely to be at the helm of the offshore wind market.

- Around 85% of offshore wind installations are globally in European waters. The governments of the European region, particularly in the North Sea area, have set an ambitious target for installing offshore wind farms in their territorial waters.

- Europe was expected to have 112 MW of floating offshore wind power capacity installed by 2022, with the UK, France, Norway, Ireland, and Spain being the region's biggest markets.

- In August 2022, an agreement was made between Cerulean Winds and Ping Petroleum UK about offshore oil and gas facilities that would be mostly powered by offshore wind.Under the agreement, Cerulean Winds and its group of Tier 1 industrial partners will provide a large floating offshore wind turbine that will be connected by a cable to Ping Petroleum's floating production and storage vessel.The project is expected to go online by 2025. A grant enabled the project to go to Cerulean Winds through the Floating Offshore Wind Demonstration Program.

- In February 2022, Norway announced plans for its first auction for offshore wind. The tender, scheduled for the second half of this year, would first look for bids to develop at least 1.5 GW of offshore wind capacity to supply the country, with subsequent tenders designed to provide an economic boost by providing more electricity for export to Europe.

- During the forecast period, these trends should make Europe a great place to do business for people who are in the business of floating offshore wind farms.

Floating Offshore Wind Industry Overview

The floating offshore wind power market is moderately fragmented. Some major players in the market (in no particular order) include General Electric Company, Doosan Energy, Siemens Gamesa Renewable Energy, BW Ideaol SA, and Vestas Wind Systems AS, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Floating Offshore Wind Power Potential Installed Capacity Forecast in MW, till 2028

- 4.3 Key Projects Information

- 4.3.1 Major Existing Projects

- 4.3.2 Upcoming Projects

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.2 Restraint

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Water Depth (Qualitative Analysis Only)

- 5.1.1 Shallow Water (less than 30 m depth)

- 5.1.2 Transitional Water (30 m to 60 m depth)

- 5.1.3 Deep Water (higher than 60 m depth)

- 5.2 By Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 South America

- 5.2.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies Adopted by Key Players

- 6.3 Company Profiles

- 6.3.1 Vestas Wind Systems AS

- 6.3.2 General Electric Company

- 6.3.3 Siemens Gamesa Renewable Energy SA

- 6.3.4 BW Ideol AS

- 6.3.5 Equinor ASA

- 6.3.6 Marubeni Corporation

- 6.3.7 Macquarie Group Limited

- 6.3.8 Doosan Enerbility Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球离岸风电电缆市场规模、份额、成长分析,按技术(阵列间,11 kV 至 33 kV),按导体(铜、铝)- 2024-2031 年行业预测

全球离岸风电电缆市场规模、份额、成长分析,按技术(阵列间,11 kV 至 33 kV),按导体(铜、铝)- 2024-2031 年行业预测 Orsted改变政策并设定更保守的路线

Orsted改变政策并设定更保守的路线 离岸风电:2023年回顾

离岸风电:2023年回顾 浮体式海上风电市场:按水深和涡轮机容量分類的全球预测 - 2024-2030

浮体式海上风电市场:按水深和涡轮机容量分類的全球预测 - 2024-2030 2024年全球离岸风力发电市场报告

2024年全球离岸风力发电市场报告 全球离岸风电市场:2024-2034

全球离岸风电市场:2024-2034 离岸风力发电市场规模、份额、趋势分析报告:按装机量、容量、水深、地区、细分趋势,2023-2030年

离岸风力发电市场规模、份额、趋势分析报告:按装机量、容量、水深、地区、细分趋势,2023-2030年 离岸风力发电的供应链的限制因素 (2023年)

离岸风力发电的供应链的限制因素 (2023年) 全球离岸风电市场

全球离岸风电市场 离岸风电电缆市场规模 - 按技术(阵列间 {11kV 至 33kV、34kV 至 66kV}、出口 {132 kV 及以下、132 kV 及以上})、按导体材料(铝、铜)和全球预测,2023 年 - 2032

离岸风电电缆市场规模 - 按技术(阵列间 {11kV 至 33kV、34kV 至 66kV}、出口 {132 kV 及以下、132 kV 及以上})、按导体材料(铝、铜)和全球预测,2023 年 - 2032