|

市场调查报告书

商品编码

1438288

测试、检验和认证(TIC):市场占有率分析、行业趋势和统计、成长预测(2024-2029)Testing, Inspection, and Certification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

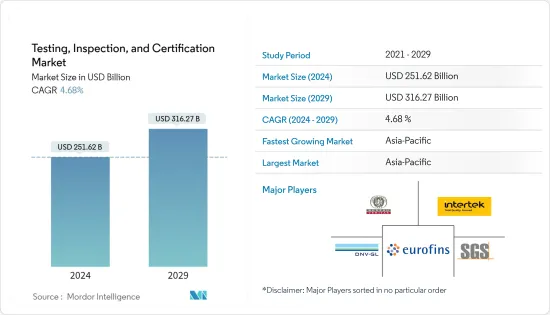

测试、检验和认证(TIC)市场规模预计到 2024 年为 2516.2 亿美元,预计到 2029 年将达到 3162.7 亿美元,预测期间(2024-2029 年)将以 4.68% 的复合年增长率增长。

主要亮点

- 测试、检验和认证 (TIC) 行业帮助提高行业内各种最终用户使用的产品质量,为全球经济做出了重大贡献。 TIC 服务也有助于减少产量召回并维持对监管机构和各个领域标准的遵守。

- 对 TIC 服务的需求不断增加,以促进各行业先进技术的采用以及技术的安全开发和部署,同时保持合规性。 TIC Services 还提供必要的认证,因为医疗保健和製药、食品和饮料、汽车和工业製造等某些行业需要国际认证的产品和技术。

- 测试、检验和认证 (TIC) 在确保基础设施、服务和产品符合安全和品质标准和法规方面发挥关键作用。由于石油和天然气等多个行业对定期检查和测试的需求很高,无论行业季节性如何,TIC 市场预计都会成长。

- 政府和监管机构的严格规定,特别是有关食品认证和建筑能源效率的规定,迫使组织使用测试、检验和认证 (TIC) 服务。

- 为了标准化质量,印度食品业的测试和检验服务预计将大幅成长。食品监管机构印度食品安全和标准局 (FSSAI) 可以透过引入全国性线上平台来提高食品安全检查和抽样的透明度。

- 贸易全球化使供应链变得复杂,并可能影响产品品质。因此,为了保持相同的状态,供应链的每个阶段都需要TIC服务。由于全球化的快速发展、国有实验室的私有化以及最终用户效率标准的提高,复杂的供应链给 TIC 市场带来了重大挑战。

- 代表独立第三方测试、检验和认证 (TIC) 行业的全球贸易协会 TIC 理事会表示,COVID-19 大流行迫使企业减少差旅和现场测试、评估和认证活动。表示实施受到阻碍。这项活动主要归因于为遏制疫情进一步蔓延而实施的旅行限制。此外,出于对员工的谨慎考虑,公司避免亲自拜访。这导致该部门的收益总体下降。

测试、检验和认证 (TIC) 市场趋势

食品和农业预计将占据很大的市场占有率

- 在包括食品业在内的各个行业中,品管最重要的要素是测试、检验和认证 (TIC)。维持食品安全和品质标准取决于 TIC。创建新颖且富有创意的解决方案来解决 COVID-19 的挑战(例如虚拟检查和远端审核)并利用食品行业的尖端技术将有助于 TIC 行业的扩张。 TIC 服务使公司能够提高生产力、降低风险并提高产品和服务的品质、合规性和安全性,同时遵守全球标准。

- 近年来,消费者对食品品质安全议题的意识不断增强。这主要是由于最近的食品召回讨论以及由于大流行而更加关注清洁和安全的结果。这促进了公共和商业食品部门食品安全和品质的多项标准的製定。

- 油和牛奶等食品中掺假和物质混合的发生率不断增加,需要可靠的 TIC 系统。此外,消费者对风险和诈骗的了解也越来越多。产品测试、认证和检验程序确保产品品质、安全性和可靠性。

- 食品检验、测试和认证市场正在不断增长,并且在未来几年具有巨大的成长潜力。食物中毒的日益普及、检测技术的进步、食品供应的全球化以及严格的食品安全国际标准是推动食品检测、检测和认证市场成长的主要因素。

- 污染物和化学物质可能会污染价值链中每个环节的食品,从收穫到製造再到消费。因此,食品品管是必要的,因为食品污染可能是食物中毒的严重原因。美国和加拿大执行食品安全标准的严格法律增加了该地区对食品安全检验服务的需求。美国食品安全现代化法案(FSMA)的通过显示全球食品安全检查的需求日益增长。

- 此外,世界卫生组织(WHO)于2022年10月17日发布了核准的《2022-2030年全球食品安全战略》。该战略透过加强食品安全系统和鼓励国际合作来指导和支持世卫组织会员国。努力确定优先顺序、计划、实施、监测和定期审查措施,以尽量减少食源性疾病。

- 根据韩国MFDS统计,截至2021年,韩国政府核准的国外食品检测设施中约有一半位于中国。资讯来源称,此类国际检测设施总合60个。

亚太地区占最大市场占有率

- 随着中国、印度、日本和韩国等新兴市场随着本土产业的发展和随后的出口引入而变得更具吸引力,预计亚太地区将占据较大的市场占有率。严格标准,快速都市化。

- 中国等新兴市场透过本土产业的发展和随后的出口加速、严格标准的引入和快速都市化而成为有吸引力的市场。

- 中国的「中国製造2025」倡议将5G视为新兴产业。这为中国企业提供了在全球市场上更具竞争力和创新性的机会,并防止低品质的仿冒品进入市场,而这可以透过获得特定行业的认证来实现。

- 与其他亚太主要国家一样,日本在下游石油和天然气领域也很活跃。福岛核电事故,该国的几座核能发电厂因安全原因被关闭,导致日本严重依赖石化燃料来满足所有能源需求。

- 由于国内产量较低,日本政府鼓励能源公司在世界各地增加探勘开发计划,以确保石油和天然气的稳定供应。这些努力使日本成为能源产业资本设备的主要出口国之一,而该产业已成为该国 TIC 服务的主要采用者之一。

- 在製造业方面,韩国政府计划重点将国内机器人发展成为价值2,500万美元的产业,并在年终前成为第四大公司。这正在推动机器人公司的出现。然而,要将工业机器人引入製造和服务业,企业必须获得基于国际和地区标准的产品安全认证。

测试、检验和认证 (TIC) 行业概览

测试、检验和认证(TIC)市场将面临竞争对手之间的激烈竞争。由于预计未来几年将出现高度整合,市场上竞争公司之间的敌对行动预计将进一步加剧。公司透过开发新产品、合作和收购来保持竞争力。市面上营运的主要企业有 Intertek Group PLC、SGS SA、Bureau Veritas SA、Underwriters Laboratories (UL) 和 DNV GL。

- 2023 年 5 月 - Thunderbolt 3 和 4 主机和设备的产品资格测试现已在应用安全科学领域的全球先驱 UL Solutions 位于台湾台北的工厂进行。 Thunderbolt 3 和 4 主机产品,包括笔记型电脑、桌上型电脑、显示器和扩充坞,均在 UL Solutions 台北实验室进行电气和功能测试。

- 2023 年 4 月 - UL 解决方案和韩国测试认证委员会 (KTC) 在华盛顿特区签署谅解备忘录 (MoU),合作评估电动车 (EV) 充电器的安全性和性能并进入全球市场。随着美国电动车使用量的增加,这种合作关係将为韩国製造商满足日益增长的电动车充电器需求铺平道路。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 竞争公司之间的敌意强度

- 替代品的威胁

- 评估 COVID-19 对 TIC 产业的影响

第五章市场动态

- 市场驱动因素

- 食物中毒发生率增加

- 假冒和有缺陷药品的贸易增加

- 市场挑战

- 创新技术采用率低

第六章无损检测服务业分析

- 目前市场需求

- 市场区隔 - 石油和天然气、建筑、汽车、航太、国防等。

第七章市场区隔

- 按服务类型

- 测试和检验服务

- 认证服务

- 依采购类型

- 外包

- 公司内部

- 最终用户产业

- 消费品/零售

- 食品/农业

- 油和气

- 建设工程

- 能源/化学

- 工业产品製造

- 交通运输(铁路/航太)

- 工业/汽车

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 挪威

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 其他亚太地区

- 拉丁美洲

- 巴西

- 墨西哥

- 其他拉丁美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 土耳其

- 奈及利亚

- 其他中东和非洲

- 北美洲

第八章 竞争形势

- 公司简介

- Intertek Group PLC

- SGS SA

- Bureau Veritas SA

- UL Group

- DNV GL

- Eurofins Scientific SE

- Dekra Certification GmbH

- ALS Limited

- BSI Group

- SAI Global Limited

- MISTRAS Group Inc.

- Element Metech(Exova Group PLC)

- TUV SUD Ltd

- Applus Services SA

- Kiwa NV

第九章投资分析及市场展望

The Testing, Inspection, and Certification Market size is estimated at USD 251.62 billion in 2024, and is expected to reach USD 316.27 billion by 2029, growing at a CAGR of 4.68% during the forecast period (2024-2029).

Key Highlights

- The testing, inspection, and certification industry significantly contributes to the global economy as it helps improve the quality of products used across industries by various end users. Also, TIC services help reduce yield recalls and maintain compliance with regulatory authorities and standards governing different sectors.

- The introduction of advanced technologies across various sectors has further intensified the need for TIC services as they foster the safe development and adoption of technologies while maintaining compliance. TIC services also provide the required certifications as specific industries, including healthcare and pharmaceuticals, food and beverage, automotive, and industrial manufacturing, require internationally certified products and technologies.

- Testing, inspection, and certification (TIC) play a significant role in ensuring that the infrastructure, services, and products meet the standards and regulations of safety and quality. Due to the high demand for inspection and testing at regular intervals across a few industries, such as oil and gas, the TIC market is expected to witness growth, irrespective of industrial seasonality.

- Stringent regulations from government and regulatory bodies, especially in food certification and energy efficiency in construction, are compelling organizations to leverage testing, inspection, and certification (TIC) services.

- To standardize quality, testing and inspection services in India's food industry are expected to grow significantly. The Food Regulator Food Safety and Standards Authority of India (FSSAI) can bring transparency to food safety inspection and sampling by implementing a nationwide online platform.

- Globalization of trade leads to a complex supply chain that can impact product quality. Therefore, TIC services are required at every stage of the supply chain to maintain the same. Due to rapid globalization, privatization of state-owned laboratories, and increasing standards of end-user efficiency, complex supply chains have posed significant challenges to the TIC market.

- According to TIC Council, the global trade federation representing the independent third-party testing, inspection, and certification (TIC) industry, the COVID-19 pandemic hindered companies from performing testing, assessment, and certification activities by traveling and carrying out on-site activities, which was primarily attributed to the travel restrictions imposed to curb the pandemic from spreading further. Furthermore, companies discouraged in-person visits out of caution for their workers. This led to an overall decline in the revenue generated from the sector.

Testing, Inspection, and Certification Market Trends

Food and Agriculture Expected to Hold a Significant Market Share

- The most important components of quality control across a range of industries, including the food industry, are testing, inspection, and certification (TIC). Maintaining the standards for food safety and quality depends on TIC. Creating novel, inventive solutions (such as virtual inspections and remote audits) to solve the COVID-19 conundrum and utilizing cutting-edge technology in the food industry contribute to the expansion of the TIC sector. Utilizing TIC services, businesses may boost productivity, lower risk, and improve the quality, compliance, and safety of their products and services while still conforming to global standards.

- In recent years, consumer awareness of food quality and safety problems has increased, mostly as a result of debates around recent food recalls and the pandemic's increasing concern for cleanliness and safety. In the public and commercial food sectors, this has made creating several standards for food safety and quality easier.

- Due to the increased incidences of adulteration and substance mixing in food products, such as oils and milk, a reliable TIC system is needed. Additionally, consumers are becoming more informed about hazards and frauds. Procedures for testing, certifying, and inspecting products guarantee their quality, safety, and confidence.

- The food testing, inspection, and certification market is growing and has a sizable growth potential in the coming years. The rise in the prevalence of foodborne diseases, technological advancements in testing, the globalization of the food supply, and stringent international standards for food safety are the main factors driving the growth of the market for food testing, inspection, and certification.

- At every point along the value chain, from harvest to manufacture to consumption, contaminants and chemicals have the potential to contaminate food. Therefore, food quality management is necessary since contamination can be a serious cause of food poisoning. The need for food safety testing services in the area has risen due to strict laws enforcing food safety standards in the United States and Canada. The adoption of the U.S. Food Safety Modernization Act (FSMA) signals a rise in the need for food safety testing on a global scale.

- In addition to that, the World Health Organization (WHO) introduced its accepted Global Strategy for Food Safety 2022-2030 on October 17, 2022. By bolstering food safety systems and encouraging international collaboration, the strategy will direct and support WHO Member States in their efforts to prioritize, plan, execute, monitor, and routinely review measures towards minimizing foodborne diseases.

- According to the MFDS, South Korea, about half of all foreign food testing facilities authorized by the South Korean government were located in China as of 2021. The source states that there were a total of 60 such international laboratories.

Asia-Pacific Holds the Largest Market Share

- The Asia-Pacific region is anticipated to hold a significant market share due to emerging markets in countries such as China, India, Japan, and South Korea, which have become attractive through the development of indigenous industries and subsequent acceleration in exports, the introduction of stringent standards, and rapid urbanization.

- Emerging markets, such as China, have become attractive spots through developing indigenous industries and subsequent acceleration in exports, the introduction of stringent standards, and rapid urbanization.

- China's "Made in China 2025" initiative has identified 5G as an emerging industry. It offers opportunities for Chinese companies to become more competitive and innovative in the global market and prevent low-quality and counterfeit goods from entering the market, which the attainment of domain-specific certifications can achieve.

- Like other key Asia-Pacific countries, Japan is active in the downstream oil and gas sector. After the Fukushima plant accident, the shutdown of multiple nuclear power plants for safety purposes in the country made Japan largely dependent upon fossil fuels for all its energy needs.

- Owing to low domestic production in the country, the Japanese government has encouraged its energy companies to increase exploration and development projects globally to secure a stable oil and natural gas supply. These initiatives make Japan one of the major exporters of capital equipment for the energy sector and make the industry one of the country's significant adopters of TIC services.

- On the manufacturing front, the South Korean government plans to turn the nation's robotics technology into a USD 25 million industry, focusing on becoming the fourth-largest player by the end of 2023. This is fostering the emergence of robotic companies. However, companies must acquire industrial robot product safety certification based on international and local standards to bring such robots into the manufacturing and service sector.

Testing, Inspection, and Certification Industry Overview

The testing, inspection, and certification market will witness intense competitive rivalry. With high consolidation expected over the next few years, the competitive rivalry in the market is expected to increase further. The companies develop new products, collaborations, and acquisitions to remain competitive. Key players operating in the market are Intertek Group PLC, SGS SA, Bureau Veritas SA, Underwriters Laboratories (UL), and DNV GL.

- May 2023 - The Thunderbolt 3 and 4 host and device product certification testing can now be done at UL Solutions' facility in Taipei, Taiwan, a worldwide pioneer in applied safety science. The Thunderbolt 3 and 4 host goods, including laptops, desktops, monitors, and docking stations, tested electrically and functionally at the UL Solutions Taipei lab.

- April 2023 - To work together on the safety and performance assessment and worldwide market access of electric vehicle (EV) chargers, UL Solutions and the Korea Testing Certification Institute (KTC) signed a memorandum of understanding (MoU) in Washington, DC. As EV usage increases in the U.S., the alliance paves the way for Korean manufacturers to satisfy the rising need for EV chargers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitues

- 4.3 Assessment of Impact of COVID-19 on the TIC Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing incidence of foodborne diseases

- 5.1.2 Increasing trade in counterfeit and defective pharmaceutical products

- 5.2 Market Challenges

- 5.2.1 Low adoption rate of Innovative Technologies

6 ANALYSIS OF THE NDT SERVICE INDUSTRY

- 6.1 Current Market Demand

- 6.2 Market Breakdown - Oil and Gas, Construction, Automotive, Aerospace and Defense, etc.

7 MARKET SEGMENTATION

- 7.1 By Service Type

- 7.1.1 Testing and Inspection Service

- 7.1.2 Certification Service

- 7.2 By Sourcing Type

- 7.2.1 Outsourced

- 7.2.2 In-house

- 7.3 By End-user Vertical

- 7.3.1 Consumer Goods and Retail

- 7.3.2 Food and Agriculture

- 7.3.3 Oil and Gas

- 7.3.4 Construction and Engineering

- 7.3.5 Energy and Chemicals

- 7.3.6 Manufacturing of Industrial Goods

- 7.3.7 Transportation (Rail and Aerospace)

- 7.3.8 Industrial and Automotive

- 7.3.9 Other End-user Verticals

- 7.4 By Geography

- 7.4.1 North America

- 7.4.1.1 United States

- 7.4.1.2 Canada

- 7.4.2 Europe

- 7.4.2.1 United Kingdom

- 7.4.2.2 Germany

- 7.4.2.3 France

- 7.4.2.4 Spain

- 7.4.2.5 Norway

- 7.4.2.6 Rest of Europe

- 7.4.3 Asia-Pacific

- 7.4.3.1 China

- 7.4.3.2 Japan

- 7.4.3.3 South Korea

- 7.4.3.4 India

- 7.4.3.5 Rest of Asia-Pacific

- 7.4.4 Latin America

- 7.4.4.1 Brazil

- 7.4.4.2 Mexico

- 7.4.4.3 Rest of Latin America

- 7.4.5 Middle-East and Africa

- 7.4.5.1 Saudi Arabia

- 7.4.5.2 United Arab Emirates

- 7.4.5.3 Qatar

- 7.4.5.4 Turkey

- 7.4.5.5 Nigeria

- 7.4.5.6 Rest of Middle-East and Africa

- 7.4.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Intertek Group PLC

- 8.1.2 SGS SA

- 8.1.3 Bureau Veritas SA

- 8.1.4 UL Group

- 8.1.5 DNV GL

- 8.1.6 Eurofins Scientific SE

- 8.1.7 Dekra Certification GmbH

- 8.1.8 ALS Limited

- 8.1.9 BSI Group

- 8.1.10 SAI Global Limited

- 8.1.11 MISTRAS Group Inc.

- 8.1.12 Element Metech (Exova Group PLC)

- 8.1.13 TUV SUD Ltd

- 8.1.14 Applus Services SA

- 8.1.15 Kiwa NV

9 INVESTMENT ANALYSIS AND MARKET OUTLOOK

2024-2032 年按服务类型、调试类型、采购类型、最终用途行业和地区分類的测试和调试市场报告

2024-2032 年按服务类型、调试类型、采购类型、最终用途行业和地区分類的测试和调试市场报告 日本测试、检验和认证 (TIC) 市场 2024-2028

日本测试、检验和认证 (TIC) 市场 2024-2028 2024 年测试、检验和认证 (TIC) 全球市场报告

2024 年测试、检验和认证 (TIC) 全球市场报告 测试、检验和认证市场:按服务类型、采购类型、应用、产业分类:2023-2032年全球机会分析与产业预测

测试、检验和认证市场:按服务类型、采购类型、应用、产业分类:2023-2032年全球机会分析与产业预测 TIC(测试、检验和认证)市场报告:到 2030 年的趋势、预测和竞争分析

TIC(测试、检验和认证)市场报告:到 2030 年的趋势、预测和竞争分析 北美测试、检验和认证市场规模和预测、区域份额、趋势和成长机会分析报告范围:按采购类型、服务类型、最终用户

北美测试、检验和认证市场规模和预测、区域份额、趋势和成长机会分析报告范围:按采购类型、服务类型、最终用户 全球测试、检验和认证市场 (TIC)

全球测试、检验和认证市场 (TIC) 航太与生命科学实验,检验,认证的全球市场

航太与生命科学实验,检验,认证的全球市场 测试、检验和认证 (TIC) 全球市场规模、份额和行业趋势分析报告:用途、按采购类型、按服务类型(测试、检验、认证)、按地区、展望和预测,2023-2030 年

测试、检验和认证 (TIC) 全球市场规模、份额和行业趋势分析报告:用途、按采购类型、按服务类型(测试、检验、认证)、按地区、展望和预测,2023-2030 年 到2030年测试、检验和认证(TIC)市场预测-按服务类型、采购类型、应用、最终用户和地区进行的全球分析

到2030年测试、检验和认证(TIC)市场预测-按服务类型、采购类型、应用、最终用户和地区进行的全球分析