|

市场调查报告书

商品编码

1438298

汽车点火线圈 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Automotive Ignition Coil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

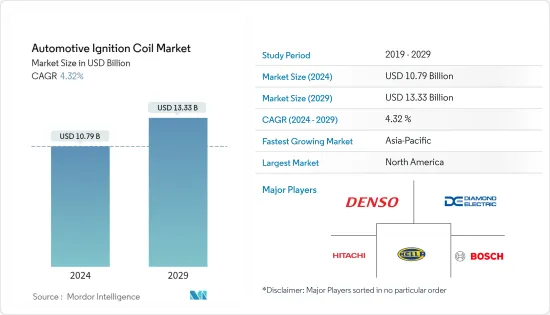

2024年汽车点火线圈市场规模预计为107.9亿美元,预计到2029年将达到133.3亿美元,在预测期内(2024-2029年)CAGR为4.32%。

主要亮点

- COVID-19 的爆发导致多家车辆和零件製造工厂暂时关闭。然而,随着一些国家逐步解除封锁,对车辆的需求也略有增加。汽车产业受到的影响尤其明显,许多企业的生产活动和供应链都面临干扰。

- 然而,随着疫情在 2021 年下半年和 2022 年初消退,在汽车产业电气化指数级成长的进一步推动下,该产业已恢復到疫情前的状况。儘管成长,但电气化是点火线圈潜在市场需求放缓的明显迹象,并可能降低未来几年的市场价值。

- 全球汽车销售的成长和汽车产量的增加对汽车点火线圈的销售产生了积极影响。儘管近期经济状况仍不稳定,但全球汽车产业仍取得了令人满意的成长。在新兴经济体尤其如此,与已开发经济体相比,新兴经济体的汽车产量预计将很高。这些新兴经济体的城市化进程不断加快、人均收入成长以及生活水准的提高也在市场成长中发挥着至关重要的作用。

- 全球不断增长的汽车需求预计将增加对点火系统的需求。但目前,由于多种原因,汽车需求正以缓慢的速度成长。影响各国汽车销售和产量的首要因素是中美贸易战,点火系统在不久的将来可能会出现缓慢的成长。

- 车辆平均寿命的延长加速了维护和修理活动,包括更换点火线圈。随着行驶里程的增加,点火线圈的更换量增加,进一步拉动了售后市场对汽车点火线圈市场的需求。

- 另一个因素是人均收入,不同国家的人均收入不同,可能会影响车辆的平均车龄。儘管美国、中国、印度以及法国、德国等一些欧洲国家的人均收入较高,但汽车的平均车龄却在不断增加,乘用车接近10年,商用车接近11-14年。汽车。

汽车点火线圈市场趋势

电动车需求的成长阻碍了汽车齿轮市场的成长

- 实现永续交通的需求在推动电动车需求方面发挥着重要作用。电动车 (EV) 市场正在成为汽车产业不可或缺的一部分,代表着实现能源效率和减少污染物及其他温室气体排放的途径。

- 越来越多的环境问题和有利的政府措施是推动电动车市场成长的一些主要因素。不断增加的能源成本和新兴节能技术之间的竞争预计也将推动市场成长。

- 电动车的崛起主要还是受到政策环境的推动。电动车普及率领先的 10 个国家(中国、美国、挪威、德国、日本、英国、法国、瑞典、加拿大和荷兰)均制定了一系列促进电动车普及的政策。

- 全球每年註册的新电动车数量显着增加。需求激增的原因包括新的、有吸引力的车型、政府绿色復苏基金的激励措施、95克二氧化碳排放指令、可用性的提高以及电动车的广泛推广。

- 根据 EV Volumes 的数据,插电式混合动力车的同比增长率一直呈上升趋势,其中中国在 2021 年至 2022 年期间增长了 82%。同样,北美也出现了增长同比增长率为48%,其中欧洲2021 年至2022 年间的年成长率为15%。

- 全球和地区的电动车製造商正在利用新技术进行创新,将其服务扩展到世界各地。例如:

- 中国比亚迪在欧洲拥有庞大的生产网络,但自 2021 年以来,该网络在乘用车领域基本上没有引起人们的注意。造成这种情况的一些主要原因是该公司计划于 2023 年下半年开始建造的匈牙利新工厂、计划在法国的工厂以及在英国生产电动巴士的合资企业。

- 2021年12月,戴姆勒与中国政府合作,在中国推广电动车。电动车是戴姆勒未来出行策略的主要支柱之一。该公司正在全球推广这项策略,特别是在中国这个全球最大的新能源汽车市场。

- 由于点火线圈不用于电动车,上述因素预计将对预测期内全球汽车点火线圈市场的成长构成重大挑战。

亚太地区引领点火线圈市场

- 由于印度、中国和东协国家等国家的汽车需求不断增长,以及建筑、电子商务和采矿业的成长,商用车的需求不断增加,预计亚太地区将主导汽车点火线圈市场活动(导致物流业的兴起) 。欧洲和北美分别紧接着亚太地区之后。

- 中国、日本、印度等主要汽车市场的汽车销售量下降,进一步影响了汽车点火线圈市场的成长。发展中经济体的政府正在采取各种措施来增加各自国家的汽车销售量。

- 例如,2020年中国插电式电动车销量总计130万辆,其次是韩国,插电式混合动力车销量总计52万辆。儘管电动车市场规模很大,但巨大的机会在于插电式混合动力车的巨大销量,这仍然需要车辆使用点火线圈,从而推动整个亚太地区的市场主要成长。

- 大多数豪华车辆都配备了多个车辆点火线圈,因为它们的功率高且性能优异。发展中地区豪华车销售大幅成长。例如,中国已发展成为豪华车销售的主要目的地。

- 以价值计算,近三分之一的豪华车在中国销售。从销售来看,印度是全球最大的汽车点火线圈市场之一,豪华汽车对汽车点火线圈产生了很高的需求。然而,豪华和非豪华汽车製造商都预见到该国销售成长的巨大潜力,并寻求进一步投资这个快速成长的市场。

汽车点火线圈产业概况

汽车点火线圈市场由日立汽车系统公司、大陆集团、钻石电气製造公司、电装公司、三菱电机公司和博格华纳等少数几家公司主导。这些公司正在推出技术更先进的点火线圈,并扩大其地理分布,以在竞争中保持领先地位。例如:

2021年9月,日立Astemo宣布将总计投资5,600万美元,用于提高其生产点火线圈等各种汽车零件的生产工厂的工业安全和生产能力。

2021年3月,Diamond Electric Mfg.宣布将在美国西维吉尼亚州兴建新厂,生产汽车点火线圈。美国点火线圈产能将提高20%。美国新工厂建筑面积12,263平方公尺。除了福特现有的北美生产基地外,主要供货目的地是日本汽车製造商的北美生产基地。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 市场驱动因素

- 乘用车和商用车的需求不断增加

- 其他的

- 市场限制

- 电动车需求的成长阻碍了汽车齿轮市场的成长

- 其他的

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争激烈程度

第 5 章:市场细分

- 类型

- 块点火线圈

- 插头上的线圈

- 点火线圈导轨

- 依工作原理分类

- 单火花技术

- 双火花技术

- 按配销通路

- OEM

- 售后市场

- 按车型分类

- 搭乘用车

- 商务车辆

- 地理

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 欧洲其他地区

- 亚太

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 世界其他地区

- 巴西

- 阿根廷

- 南非

- 其他国家

- 北美洲

第 6 章:竞争格局

- 供应商市占率

- 公司简介

- NGK SPARK PLUG Co. Ltd

- Denso Corporation

- Robert Bosch GmbH

- Hitachi Ltd

- HELLA GmbH & Co. KGaA

- Diamond Electric Holdings Co. Ltd

- Taiwan Ignition System Co. Ltd

- BorgWarner Inc.

- Eldor Corporation

- Furuhashi Auto Electric Parts Co. Ltd

第 7 章:市场机会与未来趋势

The Automotive Ignition Coil Market size is estimated at USD 10.79 billion in 2024, and is expected to reach USD 13.33 billion by 2029, growing at a CAGR of 4.32% during the forecast period (2024-2029).

Key Highlights

- The outbreak of COVID-19 caused several vehicle and component manufacturing facilities to shut down temporarily. However, with the gradual removal of lockdowns in several countries, the demand for vehicles slightly increased. The impact was evident in the auto industry as many companies faced disturbances with their production activities and supply chain.

- However, with the pandemic subsiding in the latter half of 2021 and early 2022, the industry has been crawling back up to pre-pandemic conditions, further aided by the exponentially growing electrification of the automotive industry. Despite the growth, electrification is a clear sign of a potential market demand slowdown for the ignition coils and can reduce market value in the coming years.

- The rise in the sales of automobiles globally and an increase in vehicle production positively affect the sales of automotive ignition coils. Even though the recent economic conditions have remained unstable, the global automotive industry has witnessed satisfactory growth. This is especially true in emerging economies, where automotive production is expected to be significant compared to developed economies. Rising urbanization, per capita income growth, and a rise in the living standards in these emerging economies also play a crucial role in market growth.

- The growing automotive demand worldwide is expected to increase the demand for ignition systems. However, at present, vehicle demand is increasing at a slow growth rate due to various reasons. The prime factor affecting vehicle sales and production in every country is the US-China trade war, owing to which the ignition system is likely to witness a slow growth rate in the near future.

- The increase in the average life of vehicles has accelerated maintenance and repair activities, including replacing their ignition coils. As the number of miles traveled increases, the replacement of ignition coils increases, which further boosts the demand for the automotive ignition coil market in the aftermarket segment.

- Another factor is the per capita income, which varies from country to country, and may influence the average age of vehicles. Despite the United States, China, India, and some European countries, like France, and Germany, observing high per capita incomes, the average age of vehicles has been increasing and was approximated to 10 years for passenger cars and 11-14 years for commercial vehicles.

Automotive Ignition Coil Market Trends

Growing Demand for Electric Vehicles Hindering the Automotive Gear Market Growth

- The need to attain sustainable transportation plays a significant role in driving the demand for electric vehicles. The electric vehicle (EV) market is becoming an integral part of the automotive industry and represents a pathway toward achieving energy efficiency and reduced emissions of pollutants and other greenhouse gasses.

- The rising number of environmental concerns and favorable government initiatives are some of the major factors driving the growth of the electric vehicle market. The increasing energy costs and competition among emerging energy-efficient technologies are also expected to fuel market growth.

- The rise in electric vehicles is still majorly driven by the policy environment. The 10 leading countries in electric vehicle adoption (China, the United States, Norway, Germany, Japan, the United Kingdom, France, Sweden, Canada, and the Netherlands) all have a range of policies to promote the uptake of electric vehicles.

- There has been a significant increase in the number of new electric vehicles registered every year around the world. The upsurge in demand was due to the combination of new and attractive models, incentive boosts by governments' green recovery funds, the 95g CO2 mandate, improved availability, and the extensive promotion of EVs.

- According to EV Volumes, the year-on-year growth rate of Plug-In-Hybrid Electric Vehicles has been on an increasing trend, with China witnessing a huge 82% growth between the years 2021 and 2022. Similarly, North America witnessed a growth rate of 48% (Y-o-Y), with Europe registering a 15% Y-o-Y growth rate between 2021 and 2022.

- The global and regional manufacturers of electric vehicles are innovating with new technologies, expanding their services across the world. For instance:

- China's BYD has a large production network in Europe that has largely gone unnoticed since 2021 in the passenger car world. Some of the primary reasons for this are the firm's new plant in Hungary, which is scheduled to begin construction in the latter half of 2023, its planned plant in France, and its joint venture operations in the United Kingdom, manufacturing electric buses.

- In December 2021, Daimler teamed up with the Chinese government to promote e-mobility in China. Electric mobility is one of the major pillars of Daimler's future mobility strategy. The company is bringing this strategy forward globally, especially in China, the world's largest NEV market.

- As ignition coils are not used in electric cars, the factors mentioned above are expected to put a significant challenge to the growth of the global automotive ignition coil market over the forecast period.

Asia-Pacific Leading the Ignition Coil Market

- Asia-Pacific is expected to dominate the automotive ignition coil market, owing to the growing vehicle demand in countries such as India, China, and ASEAN countries and increasing demand for commercial vehicles, due to the rise in construction, e-commerce, and mining activities (resulting in a rise in the logistics industry). Europe and North America, respectively, follow the Asia-Pacific region.

- The sales of vehicles are declining in major automotive markets such as China, Japan, and India, further impacting the growth of the automotive ignition coil market. The governments of growing economies are taking various steps to increase vehicle sales in their respective countries.

- For instance, China registered a total of 1.3 million units of plug-in electric vehicle sales in 2020, followed by South Korea, witnessing a total sales of 520,000 units of plug-in hybrid electric vehicle sales. Despite the high market for electric vehicles, the significant opportunity lies in the huge plug-in hybrid electric vehicle sales, which still require the vehicles to use ignition coils, thereby driving a major market growth across the Asia-Pacific region.

- Most luxurious vehicles are equipped with multiple vehicle ignition coils due to their high power and excellent performance. A significant increase has been witnessed in the sales of luxury vehicles in developing regions. For example, China has grown to become a major destination for the sales of luxury vehicles.

- Almost one-third of luxury vehicles are sold in China in terms of value. India is one of the world's largest vehicle ignition coil markets in terms of volume, with luxury cars generating high demand for vehicle ignition coils. However, vehicle manufacturers, both luxury and non-luxury segments, foresee a high potential for sales growth in the country and seek to invest further in this fast-growing market.

Automotive Ignition Coil Industry Overview

The automotive ignition coil market is dominated by a few players, such as Hitachi Automotive Systems, Continental AG, and Diamond Electric Mfg. Co. Ltd, Denso Corp., Mitsubishi Electric Corp., and BorgWarner. The companies are launching more technologically advanced ignition coils and expanding their geographical presence to be ahead of the competition. For instance:

In September 2021, Hitachi Astemo announced that it would invest a total of USD 56 million to improve the industrial safety and production capacities of its production plants that manufacture various automotive parts, including ignition coils.

In March 2021, Diamond Electric Mfg. Co. Ltd announced that it would build a new plant in West Virginia, USA, to manufacture ignition coils for automobiles. The production capacity of ignition coils in the United States will be increased by 20%. The new US plant has a building area of 12,263 square meters. In addition to Ford's existing North American production bases, the main supply destinations are the North American production bases of Japanese automobile manufacturers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand for Passenger Cars and Commercial Vehicles

- 4.1.2 Others

- 4.2 Market Restraints

- 4.2.1 Growing Demand for Electric Vehicles Hindering the Automotive Gear Market Growth

- 4.2.2 Others

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Block Ignition Coils

- 5.1.2 Coil on Plug

- 5.1.3 Ignition Coil Rail

- 5.2 By Operating Principle

- 5.2.1 Single Spark Technology

- 5.2.2 Dual Spark Technology

- 5.3 By Distribution Channel

- 5.3.1 OEM

- 5.3.2 Aftermarket

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Commercial Vehicles

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 South Africa

- 5.5.4.4 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 NGK SPARK PLUG Co. Ltd

- 6.2.2 Denso Corporation

- 6.2.3 Robert Bosch GmbH

- 6.2.4 Hitachi Ltd

- 6.2.5 HELLA GmbH & Co. KGaA

- 6.2.6 Diamond Electric Holdings Co. Ltd

- 6.2.7 Taiwan Ignition System Co. Ltd

- 6.2.8 BorgWarner Inc.

- 6.2.9 Eldor Corporation

- 6.2.10 Furuhashi Auto Electric Parts Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球汽车点火器线圈市场预测(至2032年):按类型、车型、销售管道、引擎类型、运行原理、应用和地区划分点火器线圈市场(依产品类型和地区)

全球汽车点火器线圈市场预测(至2032年):按类型、车型、销售管道、引擎类型、运行原理、应用和地区划分点火器线圈市场(依产品类型和地区) 全球点火器线圈市场:市场规模、份额、趋势分析(按产品类型、最终用途和地区)、细分市场预测(2025-2030 年)

全球点火器线圈市场:市场规模、份额、趋势分析(按产品类型、最终用途和地区)、细分市场预测(2025-2030 年) 2025年全球汽车点火器线圈市场报告

2025年全球汽车点火器线圈市场报告 汽车点火线圈市场报告(按类型、产品类型、车辆类型、配销通路和地区)2025 年至 2033 年

汽车点火线圈市场报告(按类型、产品类型、车辆类型、配销通路和地区)2025 年至 2033 年 汽车点火线圈售后市场 - 2019-2029 年全球产业规模、份额、趋势、机会与预测,按车型、产品、工作原理、地区和竞争细分点火线圈市场 - 全球产业规模、份额、趋势、机会和预测,按类型、组件、车辆类型、地区和竞争细分,2019-2029F

汽车点火线圈售后市场 - 2019-2029 年全球产业规模、份额、趋势、机会与预测,按车型、产品、工作原理、地区和竞争细分点火线圈市场 - 全球产业规模、份额、趋势、机会和预测,按类型、组件、车辆类型、地区和竞争细分,2019-2029F 汽油车点火器线圈市场报告:趋势、预测、竞争分析(至 2030 年)

汽油车点火器线圈市场报告:趋势、预测、竞争分析(至 2030 年) 全球汽车点火器线圈市场:按类型、电压、销售管道、车型和应用分类 - 2025-2030 年预测

全球汽车点火器线圈市场:按类型、电压、销售管道、车型和应用分类 - 2025-2030 年预测 汽车点火器线圈市场规模、份额、成长分析、按产品类型、车辆类型、分销管道、地区 - 产业预测,2024-2031

汽车点火器线圈市场规模、份额、成长分析、按产品类型、车辆类型、分销管道、地区 - 产业预测,2024-2031