|

市场调查报告书

商品编码

1438392

生物基 1,4-丁二醇:市场占有率分析、产业趋势与统计、成长预测(2024-2029 年)Bio-based 1,4-Butanediol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

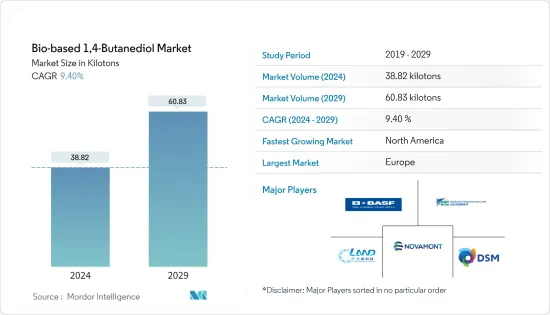

生物基1,4-丁二醇市场规模预计到2024年为38,820吨,在预测期内(2024-2029年)预计到2029年将达到60,830吨,复合年增长率为9.40%。

由于员工隔离、一般企业关闭和供应链中断,冠状病毒感染疾病(COVID-19) 大流行对生物基 1,4-丁二醇市场产生了影响。疫情期间,许多负责生产生物基1,4-丁二醇的工厂关闭。这些製造厂的关闭导致生物基 1,4-丁二醇的销量下降。汽车、电气/电子和纺织等行业已暂时搁置。然而,在目前的情况下,市场成长已经恢復。

主要亮点

- 推动市场成长的主要因素是各行业对聚对聚丁烯对苯二甲酸酯(PBT)的需求不断增加以及严格的政府法规。

- 另一方面,来自石化燃料产品的大规模竞争仍然是所研究市场的一个担忧。

- 在预测期内,重点转向环保产品可能会为受调查的市场提供机会。

- 欧洲主导了全球市场。汽车、电子和电器产品等行业越来越多地使用生物基 1,4-丁二醇,推动了该地区的需求。

生物基1,4-丁二醇市场趋势

纺织品市场需求增加

- 1,4 BDO 用作皮革、塑胶、聚酯层压板和聚氨酯鞋类的黏剂。 1,4-丁二醇是一种用于生产热塑性聚氨酯(TPU)的即时化学品,也用于生产合成革鞋底材料。

- 然而,1-4 BDO 会产生四氢呋喃 (THF)。四氢呋喃 (THF) 用于生产服饰工业中捕获的氨纶纤维。氨纶是一种轻质、柔软、滑爽的合成纤维,具有独特的弹性。由于其弹性,用于生产可拉伸的服装类。

- 由 80% 聚四亚甲基醚二醇(PTMEG 或 PolyTHF)组成的氨纶纤维可拉伸至其原始长度的 500% 至 700%,并持久保持其形状。

- 氨纶纤维的成长率预计在10%左右,远高于化纤的成长率。舒适服装类的趋势正在推动该行业的需求。

- 2022 年 9 月,莱卡公司宣布全球首次大规模商业化生产生物基氨纶,使用 QIRA 生物基 1,4-BDO 作为其关键成分之一。该公司与 Qore 合作生产下一代生物基莱卡。该产品中 70% 的莱卡纤维成分来自可再生原料,有助于将莱卡纤维的碳排放减少约 44%。预计到 2024 年,第一批使用 QIRA 生物基 1,4-BDO 製成的可再生莱卡纤维将在莱卡公司位于新加坡大士的生产工厂生产。莱卡公司正在寻求与准备追求生物纤维的各种品牌和零售客户签订合约。我们开发了服装解决方案。

- 此外,根据日本财务省的数据,2021 年日本纺织製造业的外商直接投资 (FDI) 达 5,600 万美元,而 2020 年为 3,900 万美元。

- 这些因素显示市场在预测期内将观察到纺织业成长停滞。

预计欧洲将主导市场

- 欧洲地区主导了全球市场占有率。所研究市场的需求是由汽车、电子和电器产品等行业不断增长的需求所推动的。

- 德国拥有欧洲最重要的电子和汽车工业。德国的电气和电子市场是欧洲最大、世界第五大。

- 根据ZVEI统计,2021年德国电子和数位产业销售额达2,004亿欧元(2,181.9亿美元),较2020年的1,819亿欧元(1,980.5亿美元)成长10.2%,创下了成长率。 2021年电子数位产业销售额为1,629亿欧元(1,773.6亿美元),而2020年为1,496亿欧元(1,628.8亿美元),成长率为8.8%。国内电子和半导体应用1,4-丁二醇产业的这些趋势正在增加对生物基产品的需求。

- 德国也引领欧洲汽车市场,拥有41家组装和引擎生产厂,占欧洲汽车总产量的三分之一。 2021年全年,全国生产汽车3,096,165辆,比2020年同期的3,742,454辆下降12%。汽车产业的衰退可能会影响所研究的市场。然而,汽车产业预计将在预测期下半年復苏和成长。

- 英国是欧洲最大的高端消费性电子产品市场,拥有约 18,000 家英国电子公司。由于对技术先进的电子设备的需求,国内电器产品市场录得显着增长。这种需求的增加预计将推动国内电子产品生产,并导致电子应用中对生物基 1,4-丁二醇的需求。

- 过去几年,法国汽车工业的表现比其他欧洲主要经济体好得多。 2021年全年,该国生产了约917,907辆汽车,比2020年成长了3%。

- 而且,随着人口收入的增加,对空调、冰箱、洗衣机、微波炉等家电电器产品的需求大幅增加,进一步推动电器产品市场的成长。

- 因此,所有这些有利的市场趋势预计将在预测期内推动该地区原料应用中生物基 1,4-丁二醇的需求。

生物基1,4-丁二醇产业概况

全球生物基1,4-丁二醇市场由寡占主导,Novamont SpA 占据压倒性的产能份额。市场知名企业包括Novamont SpA、山东蓝电生物科技、帝斯曼、BASF、环球生化科技集团有限公司(排名不分先后)等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 聚对聚丁烯对苯二甲酸酯(PBT) 需求增加

- 严格的政府法规

- 抑制因素

- 来自石化燃料产品的巨大竞争

- 其他限制

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

- 专利分析

第五章市场区隔(市场规模(数量))

- 目的

- 四氢呋喃 (THF)

- 聚丁烯对苯二甲酸酯(PBT)

- γ-丁内酯 (GBL)

- 聚氨酯(PU)

- 其他用途

- 最终用户产业

- 车

- 电气和电子

- 纤维

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 世界其他地区

- 南美洲

- 中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、合作与协议

- 市场占有率(%)分析

- 主要企业采取的策略

- 公司简介

- BASF SE

- DSM

- Genomatica Inc.

- Global Bio-chem Technology Group Company Limited

- Novamont SpA

- Qira

- Shandong LanDian Biological Technology Co. Ltd

- Yuanli Science and Technology

第七章市场机会与未来趋势

- 将重点转向环保产品

- 其他机会

The Bio-based 1,4-Butanediol Market size is estimated at 38.82 kilotons in 2024, and is expected to reach 60.83 kilotons by 2029, growing at a CAGR of 9.40% during the forecast period (2024-2029).

The COVID-19 pandemic affected the bio-based 1,4-butanediol market because of quarantined workforces, general businesses shut down, and disrupted supply chains. During the pandemic, many factories responsible for bio-based 1,4-butanediol production were shut down. The closure of these manufacturing plants dampened bio-based 1,4-butanediol sales. Sections like automobile, electrical and electronics, and textile were temporarily held. However, in the present scenario, the market growth recovered.

Key Highlights

- The major factors driving the market's growth are the increasing polybutylene terephthalate (PBT) demand from various industries and stringent government regulations.

- On the flip side, massive competition from fossil fuel-based products remains a concern for the market studied.

- The shift in focus toward eco-friendly products will likely provide opportunities for the market studied during the forecast period.

- Europe dominated the market across the world. The demand in the region is driven by the growing usage of bio-based 1,4-butanediol in industries such as automotive, electronics, and consumer appliances.

Bio-based 1,4-Butanediol Market Trends

Increasing Demand in the Textile Market

- 1,4 BDO is used as an adhesive in leather, plastics, polyester laminates, and polyurethane footwear. 1,4-butanediol is an immediate chemical used in thermoplastic polyurethane (TPU) production, further used in making synthetic leather sole material.

- However, 1-4 BDO produces tetrahydrofuran (THF), used to make spandex fiber captured in the garment industry. Spandex is a lightweight, soft, smooth synthetic fiber with a unique elasticity. Due to its elastic property, it is used in making stretchable clothing.

- Spandex fibers, consisting of 80% polytetramethyleneether glycol (PTMEG or PolyTHF), can be stretched to between 500% and 700% of their original length and durably retain their shape.

- The growth rates for spandex fiber are estimated to be around 10%, much higher than those for textiles. The trend toward comfortable clothing with high wearing comfort is driving demand in this area.

- In September 2022, Lycra Company announced the world's first large-scale commercial manufacturing of bio-derived spandex using QIRA bio-based 1,4-BDO as one of its key ingredients. The company collaborated with Qore to manufacture next-generation bio-derived LYCRA. This manufacturing involves 70% of the LYCRA fiber content sourced from renewable feedstock, helping to reduce the carbon footprint of LYCRA fiber by nearly 44%. The first renewable LYCRA fiber made using QIRA bio-based 1,4-BDO will be produced at the LYCRA Company's production facility in Tuas, Singapore, by 2024. The LYCRA Company is seeking commitments with various brands and retail customers ready to pursue bio-derived solutions for their apparel.

- Moreover, according to the Ministry of Finance Japan, the inward foreign direct investment (FDI) in the Japanese textile manufacturing industry accounted for USD 56 million in 2021, compared to USD 39 million in 2020.

- Such factors depict that the market will observe stagnant growth from the textile industry during the forecast period.

Europe is Expected to Dominate the Market

- The European region dominated the global market share. The demand in the market studied is driven by the growing demand from industries such as automotive, electronics, and consumer appliances.

- Germany includes the most significant electronic and automobile industry in Europe. The German electrical and electronics market is Europe's largest and the 5th largest worldwide.

- According to the ZVEI, Germany's electro and digital industry turnover accounted for EUR 200.4 billion (USD 218.19 billion) in 2021, witnessing a growth rate of 10.2% compared to EUR 181.9 billion (USD 198.05 billion) in 2020. Furthermore, the production from the electro and digital industry accounted for EUR 162.9 billion (USD 177.36 billion) in 2021, registering a growth rate of 8.8% compared to EUR 149.6 billion (USD 162.88 billion) in 2020. Such trends in the industry have enhanced the demand for bio-based 1,4 butanediol for electronics and semiconductor applications in the country.

- Also, Germany leads the European automotive market, with 41 assembly and engine production plants contributing to one-third of Europe's total automobile production. In the overall 2021, the country produced 3,096,165 vehicles which declined by 12% compared to 3,742,454 cars in the same period in 2020. The declining automotive industry is likely to affect the market studied. However, the automotive industry is estimated to recover and grow later in the forecast period.

- The United Kingdom is the largest European market for high-end consumer electronics products, with about 18,000 UK-based electronics companies. The demand for technologically-advanced electronic devices registered significant growth in the consumer electronics market in the country. This increase in demand is expected to drive electronics production in the country, leading to the need for bio-based 1,4-Butanediol for electronic applications.

- The France automobile industry fared much better when compared to other major economies in Europe in the past few years. In overall 2021, the country produced about 917,907 units of vehicles, which increased by 3% in comparison to 2020.

- Besides, with the increasing population income, consumer appliance demand, such as air-conditioners, fridges, washing machines, microwaves, etc., noticeably increased, further driving the consumer appliances market growth.

- Hence, all such favourable market trends are expected to drive the demand for bio-based 1,4-butanediol for raw material applications in the region during the forecast period.

Bio-based 1,4-Butanediol Industry Overview

The global bio-based 1,4 butanediol market is an oligopoly, where Novamont SpA holds the dominant production capacity share. Some of the noticeable players in the market include Novamont SpA, Shandong Landian Biological Technology, DSM, BASF SE, and Global Bio-chem Technology Group Company Limited (not in a particular order), among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Polybutylene Terephthalate (PBT)

- 4.1.2 Stringent Government Regulations

- 4.2 Restraints

- 4.2.1 Huge Competition From Fossil Fuel-based Products

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Patent Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Tetrahydrofuran (THF)

- 5.1.2 Polybutylene Terephthalate (PBT)

- 5.1.3 Gamma-Butyrolactone (GBL)

- 5.1.4 Polyurethane (PU)

- 5.1.5 Other Applications

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Electrical and Electronics

- 5.2.3 Textile

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 DSM

- 6.4.3 Genomatica Inc.

- 6.4.4 Global Bio-chem Technology Group Company Limited

- 6.4.5 Novamont S.p.A

- 6.4.6 Qira

- 6.4.7 Shandong LanDian Biological Technology Co. Ltd

- 6.4.8 Yuanli Science and Technology

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shift in Focus toward Eco-friendly Products

- 7.2 Other Opportunities

1,4-丁二醇市场:按技术、衍生物和最终用户划分 - 全球预测 2025-2030

1,4-丁二醇市场:按技术、衍生物和最终用户划分 - 全球预测 2025-2030 1,4丁二醇衍生物市场规模、份额、趋势分析报告:依产品、按应用、按地区、细分市场预测,2025-2030年

1,4丁二醇衍生物市场规模、份额、趋势分析报告:依产品、按应用、按地区、细分市场预测,2025-2030年 1,4丁二醇市场规模、份额和趋势分析报告:按应用、按市场驱动因素、按市场趋势和限制、按地区、细分市场预测,2025-2030年

1,4丁二醇市场规模、份额和趋势分析报告:按应用、按市场驱动因素、按市场趋势和限制、按地区、细分市场预测,2025-2030年 γ-丁内酯的全球市场(2024-2028)

γ-丁内酯的全球市场(2024-2028) 全球 1,4-丁二醇市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球 1,4-丁二醇市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 1,4-丁二醇全球市场规模、份额和趋势分析报告(按类型、技术、应用、区域展望和预测,2024-2031年)

1,4-丁二醇全球市场规模、份额和趋势分析报告(按类型、技术、应用、区域展望和预测,2024-2031年) 1,4 丁二醇市场报告(按类型、衍生物(四氢呋喃、聚对苯二甲酸丁二醇酯、γ-丁内酯、聚氨酯等)、最终用途行业和地区)2024-2032

1,4 丁二醇市场报告(按类型、衍生物(四氢呋喃、聚对苯二甲酸丁二醇酯、γ-丁内酯、聚氨酯等)、最终用途行业和地区)2024-2032 1,4丁二醇市场:依产品类型、应用、最终用途产业:2024-2033年全球机会分析与产业预测

1,4丁二醇市场:依产品类型、应用、最终用途产业:2024-2033年全球机会分析与产业预测 1,4-丁二醇全球市场:按类型、按应用、按技术类型、按地区 - 预测(至 2029 年)

1,4-丁二醇全球市场:按类型、按应用、按技术类型、按地区 - 预测(至 2029 年) 全球 1,3-丁二醇 (BDO) 市场 - 2024-2031

全球 1,3-丁二醇 (BDO) 市场 - 2024-2031