|

市场调查报告书

商品编码

1438474

资料中心互连:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Data Center Interconnect - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

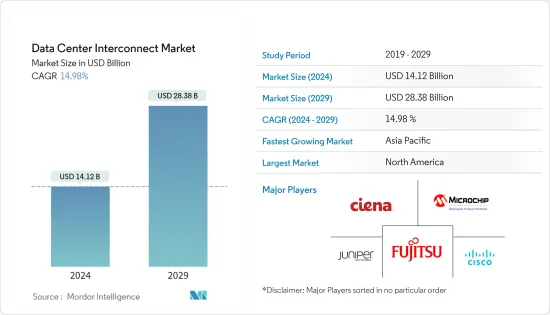

资料中心互连市场规模预计到2024年为141.2亿美元,预计到2029年将达到283.8亿美元,在预测期内(2024-2029年)增长14.98%。复合年增长率为

随着资料的激增以及人工智慧和高效能运算 (HPC) 等技术的扩展,快速、可靠且经济高效地连接资料中心资产的需求大大增加。

主要亮点

- 吞吐量、延迟、简化操作和维护、智慧和安全性等因素正在成为资料中心供应商的关键优先事项。这是推动资料中心互连(DCI)技术采用的主要因素之一。这是因为它可以增加资料中心之间的频宽、减少延迟并防止资料包遗失。

- 随着云端运算产业的发展以及最近由于全国封锁而导致OTT服务使用量的增加,所研究的市场正在日益扩大。此外,5G服务的日益商业化可能会进一步扩大互连资料中心解决方案的范围。自动驾驶汽车、智慧城市、数位双胞胎、虚拟实境、人工智慧虚拟助理、视讯监控和游戏可能会推动市场需求。

- 资料中心互连市场正在不断增长,越来越多的人享受到它的诸多好处,例如易于访问、增加便利性、高度加密的资料以及与其他资料区段的连接,这是因为它已经得到认可。

- 边缘运算的趋势对于 2020 年全国封锁至关重要,进一步扩大了正在研究的市场范围。大约 10-15% 的资料是在集中式资料中心或云端之外创建和处理的,预计到 2025 年将达到 60-70%。 Amazon、Google、Equinix 和 DRT 的超大规模资料中心相互连接并进行串流传输。透过网路将资料和应用程式发送给最终用户。边缘云端可以是开放、互连资料中心的独特生态系统。

- 一个主要挑战是资料中心连接服务的成本,特别是对于中小型企业而言。新资料中心需要在建设和维护方面进行大量投资。此外,资料中心之间的距离也很重要,因为它会降低资料中心的效率并限制资料中心互连产业的成长。

COVID-19 的爆发导致全球对云端运算的需求激增。资料中心市场范围也不断扩大。儘管资料中心建设计划因劳动力短缺而导致供应链中断,但预计某些计划的完工不会出现延迟。这仅在早期阶段可见。视讯串流和会议使用量激增超出预期,尤其是在国家封锁期间,全球对网路频宽的需求不断增加。疫情过后,由于数位化的快速发展和 5G 服务的增加,市场目前正在成长。

资料中心互连市场趋势

增加资料中心数量以推动市场成长

- 据美国市场供应商Ciena公司称,近年来资料中心的数量有所增加,目前全球已有7,500多个资料中心,其中仅全球前20名城市就有2,600个。据华为预计,2025年全球每年产生的资料将达到180ZB。非结构化资料(例如原始音讯、视讯和影像资料)的比例也在增加,很快就会达到 95% 以上,世界各地都有可能推动资料成长。

- 资料通讯网路(DCN)和资料中心互连(DCI)解决方案利用DCN和DCI频宽来保证无损网路的零丢包、低时延和高吞吐量,以满足业务快速发展的要求。迅速地。连接资料中心的DCI网路已演进为10Tbit/s分波多工(WDM)互连网路。

- 此外,资料中心服务供应商正在投资扩展主机代管和云端功能。选择建立自己的资料中心的最终用户公司(例如通讯和金融机构)对使资料中心互连市场成为全球投资热点负有主要责任。由于资料中心的成长和分布、光纤利用率的提高以及低成本的可插拔模组,各行业(主要是 OTT、ISP、金融部门和公共部门)正在开发 DCI 网路的用例。

- 资料中心的成长也推动了DCI的兴起,它允许企业连接自己的资料中心、云端供应商和其他资料中心营运商,以实现更简单的资料和资源共用。据 CloudScene 称,印度每 100 人就有 29 名网路用户,其连接生态系统由 122 个主机代管资料中心、348 个云端服务供应商和 8 个网路结构组成。

虚拟和云端运算的成长、行动资料的扩展、视讯消费和随选服务等许多因素正在推动印度和全球对 DCI 的需求。其他关键驱动因素包括资料和数位智慧型装置(例如亚马逊的 Alexa 和 Google Home)的显着增长以及政府雄心勃勃的数位印度倡议。

欧洲占有很大的市场占有率

- 资料中心数量的增加、云端技术投资的增加以及最终用户市场的扩大是推动欧洲资料中心互连市场投资的一些关键因素。 GDPR和个人资料保护倡议(Gaia-X)等严格的当地法律进一步鼓励该地区的本地资料中心建设和发展。

- 德国、英国、荷兰和法国是所研究市场的主要投资者和采用者。该地区资料中心产业的投资和成长正在增加。这主要是由于云端技术的高采用率。例如,光是微软最近就将其欧洲资料中心的容量增加了一倍。

- 资料流量的增加预计将显着促进市场成长。例如,据 Equinix 称,伦敦预计仍将是欧洲最重要的资料市场。此外,随着欧洲资料法令遵循的不断加强,预计每年将成长48%,占全球互连频宽的23%。

- 此外,诺基亚于今年 11 月宣布,其运行 SR Linux 的 7220 IXR资料中心硬体平台现已可用于 Eurooptical Cloud Infra 的子公司 DCspine,该公司在欧洲资料中心提供数位基础设施和连接服务。该解决方案将使 DCspine 能够提供更多云端和互连服务、促进网路扩展并实现网路营运自动化。

- 该建筑将更名为 Equinix HH1 国际商业交换 (IBX)资料中心。这为该公司的全球互连平台 Platform Equinix 增加了第四个德国市场,使其能够满足整个欧洲连接数位基础设施不断增长的需求。

资料中心互连产业概述

由于全球参与者和中小企业的存在,资料中心互连市场变得碎片化。如今,资料中心供应商也在结合资料中心互连解决方案。市场相关人员正在采取产品创新、併购、收购和合作等策略。

2022 年 11 月,诺基亚宣布将为非洲资料中心(非洲最大的营运商中立和云端中立互连资料中心设施供应商)提供用于其 7250 IXR(互连路由器)系统的 400 个Gigabit。非洲资料中心是泛非科技公司Cassava Technologies旗下业务,将能够为许多非洲国家的客户提供低成本、高容量的互联服务。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌意强度

- 产业价值链分析

第五章市场动态

- 市场驱动因素

- 资料中心数量增加(边缘和超大规模)

- AI、HPC等应用推动DCI网路超宽频、极简化、智慧化

- 市场挑战

- 市场机会

- 5G商业化程度不断提高

- 自动驾驶汽车和智慧城市等市场的成长

第六章 评估 COVID-19 对产业的影响

第7章技术简介

第八章市场区隔

- 按用途

- 灾害復原和业务永续营运

- 共用资料和资源

- 资料(储存)移动性

- 其他用途

- 按最终用户产业

- 通讯服务供应商(CSP)

- 网路内容和营运商中立供应商 (ICP/CNP)

- 政府/研究/教育(Government/R&E)

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第9章 竞争形势

- 公司简介

- Ciena Corp.

- Cisco Systems Inc.

- Juniper Networks Inc.

- Fujitsu Ltd.

- Microsemi Corp.

- Pluribus Networks Inc.

- Huawei Technologies Co. Ltd.

- ADVA Optical Networking SE

- Infinera Corp.

- Nokia Oyj

第十章投资分析

第十一章市场的未来

The Data Center Interconnect Market size is estimated at USD 14.12 billion in 2024, and is expected to reach USD 28.38 billion by 2029, growing at a CAGR of 14.98% during the forecast period (2024-2029).

With the proliferation of data and expansion of technologies like AI and High-Performance Computing (HPC), the need to connect data center assets quickly, reliably, and cost-effectively is growing significantly.

Key Highlights

- Factors such as throughput, latency, simplified operations and maintenance, intelligence, and security are becoming significant priorities for data center vendors. This is one of the major factors driving the adoption of Data Center Interconnect (DCI) technology. This is because they can increase bandwidth between data centers, cut down on latency, and stop packet loss.

- The market being studied is getting bigger because of the growing cloud computing industry and the recent rise in OTT service use due to a nationwide lockdown.Moreover, the increasing commercialization of 5G services may further expand the scope of interconnected data center solutions. Autonomous vehicles, smart cities, digital twins, virtual reality, AI virtual assistants, video surveillance and monitoring, and gaming can drive the market's demand.

- The data center interconnection market is growing because more and more people are becoming aware of its many benefits, such as easy access, more convenience, highly encrypted data, connecting with other data segments, and so on.

- The edge computing trend, essential in the 2020 nationwide lockdown scenario, further expands the studied market scope. About 10-15 percent of data is created and processed outside a centralized data center or cloud, but it is expected to reach 60-70 percent by 2025. The hyperscale data centers of Amazon, Google, Equinix, and DRT, are interconnected and stream data and applications over the network to end users. The edge cloud may be a unique ecosystem of open and interconnected data centers.

- The major challenge, especially for small and medium-sized businesses, is the cost of data center connectivity services. A new data center necessitates a significant investment in both construction and maintenance. Furthermore, the distance between data centers is important since it might reduce a data center's efficiency, limiting the growth of the data center interconnect industry.

The COVID-19 outbreak sparked a surge in demand for cloud computing globally. It also expanded the scope of the data center market. Although the data center construction projects witnessed a supply chain disruption due to the labor shortage, it was not expected to delay the completion of several projects. This was only seen in the initial phases. Video streaming and conferencing usage surged beyond expectations, particularly during the nationwide lockdown period, driving up bandwidth demands for networks globally. After the pandemic, the market is currently growing due to rapid digitization and increased 5G services.

Data Center Interconnect Market Trends

Increasing Number of Data Centers to Drive the Market Growth

- According to the US-based market vendor, Ciena Corporation, the number of data centers has increased in recent years, as there are now more than 7,500 around the globe, with 2,600 packed into the top 20 global cities alone. According to Huawei, global data produced annually may reach 180 ZB in 2025. The proportion of unstructured data (such as raw voice, video, and image data) may also continue to increase, reaching more than 95% shortly, boosting the growth of data centers globally.

- Data Communication Network (DCN) and Data Center Interconnect (DCI) solutions are increasingly concerned with quickly increasing DCN and DCI bandwidth to ensure zero packet loss, low latency, and high throughput of lossless networks, meeting the requirements of rapid service development. The DCI network connecting data centers has evolved into a 10 Tbit/s Wavelength Division Multiplexing (WDM) interconnection network.

- Further, data center service providers are investing in expanding their colocation and cloud capabilities. End-user enterprises (like telecom and financial organizations) opting to build their own data centers are mainly making the interconnected market for data centers a global investment hotspot. Industries, mainly OTT, ISPs, the financial sector, and the public sector, are developing their use cases for DCI networks due to data center growth and distribution, improved fiber utilization, and low-cost pluggable modules.

- The growth of data centers is also driving an increase in DCI, which allows enterprises to connect their data centers, cloud providers, and other data center operators to enable simpler data and resource sharing. According to CloudScene, India has 29 internet users for every 100 people, and its connectivity ecosystem is made up of 122 colocation data centers, 348 cloud service providers, and eight network fabrics.

Numerous factors, including the growth of virtualization and cloud computing, mobile data expansion, video consumption, and on-demand services, are driving a greater need for DCI in India and globally. Other key drivers include a significant increase in data and digital intelligent devices (such as Amazon's Alexa and Google Home) and the government's ambitious Digital India initiative.

Europe to Hold Significant Market Share

- The growing number of data centers, increasing investment in cloud technologies, and the expansion of end-user markets are some of the major factors driving the European data center's investment in the interconnect market. The stringent regional laws, like GDPR and the Personal Data Protection Initiative (Gaia-X), further boost the region's local data center construction and development.

- Germany, the United Kingdom, the Netherlands, and France are some of the major investors and adopters in the market studied. Investment and growth in the data center sector in the region have been increasing. This is mainly due to the high rate of adoption of cloud technologies. For instance, Microsoft alone has doubled its European data center capacity recently.

- Data traffic growth is expected to contribute to the market's growth significantly. For instance, according to Equinix, London is expected to remain the most important European market for data. Furthermore, an increasing number of European data compliance regulations serve as a catalyst, which is expected to grow 48% per year, accounting for 23% of global interconnection bandwidth.

- Furthermore, Nokia announced the availability of its 7220 IXR data center hardware platforms running SR Linux to DCspine, a subsidiary of Eurofiber Cloud Infra that provides digital infrastructure and connectivity services across European data centers, in November of this year.With this solution, DCspine will be able to offer more cloud and interconnection services, make the network easier to scale, and automate network operations.

- The building would be renamed the Equinix HH1 International Business Exchange (IBX) data center. It would add a fourth market in Germany to the company's global interconnection platform, Platform Equinix, and help meet the growing demand for connecting digital infrastructure across Europe.

Data Center Interconnect Industry Overview

The Data Center Interconnect Market is fragmented due to the presence of both global players and small and medium-sized enterprises. Lately, the vendors offering data centers are also combining data center interconnect solutions. Market players are adopting strategies such as product innovation, mergers, acquisitions, and partnerships.

In November 2022, Nokia announced that it will provide 400-gigabit-enabled interfaces for its 7250 IXR (interconnect router) systems to Africa Data Centers, the continent's largest provider of interconnected, carrier- and cloud-neutral data center facilities. Africa Data Centres, a business of Cassava Technologies, a pan-African technology company, would be able to offer its clients in many African countries low-cost, high-capacity interconnection services.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Data Centers (Edge and Hyperscale)

- 5.1.2 Increasing Need for Ultra- broadband, Simplified, and Intelligent DCI Networks due to Applications, like AI and HPC

- 5.2 Market Challenges

- 5.3 Market Opportunities

- 5.3.1 Rising Commercialization of 5G

- 5.3.2 Growth in Markets, Such as Autonomous Vehicle, Smart City

6 ASSESSMENT OF COVID-19 IMPACT ON THE INDUSTRY

7 TECHNOLOGY SNAPSHOT

8 MARKET SEGMENTATION

- 8.1 By Application

- 8.1.1 Disaster Recovery and Business Continuity

- 8.1.2 Shared Data and Resources

- 8.1.3 Data (Storage) Mobility

- 8.1.4 Other Applications

- 8.2 By End-user Industry

- 8.2.1 Communications Service Providers (CSPs)

- 8.2.2 Internet Content and Carrier- neutral Providers (ICPs/CNPs)

- 8.2.3 Government/Research and Education (Government/R&E)

- 8.2.4 Other End-user Verticals

- 8.3 By Geography

- 8.3.1 North America

- 8.3.2 Europe

- 8.3.3 Asia Pacific

- 8.3.4 Rest of the World

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 Ciena Corp.

- 9.1.2 Cisco Systems Inc.

- 9.1.3 Juniper Networks Inc.

- 9.1.4 Fujitsu Ltd.

- 9.1.5 Microsemi Corp.

- 9.1.6 Pluribus Networks Inc.

- 9.1.7 Huawei Technologies Co. Ltd.

- 9.1.8 ADVA Optical Networking SE

- 9.1.9 Infinera Corp.

- 9.1.10 Nokia Oyj

10 INVESTMENT ANALYSIS

11 FUTURE OF THE MARKET

资料中心联轴器市场:按组件、按冷却类型、按资料中心类型、按行业 - 2025-2030 年全球预测

资料中心联轴器市场:按组件、按冷却类型、按资料中心类型、按行业 - 2025-2030 年全球预测 资料中心互连平台市场:按组件、行业、应用程式和公司划分 - 2025-2030 年全球预测

资料中心互连平台市场:按组件、行业、应用程式和公司划分 - 2025-2030 年全球预测 2024 年资料中心互连 (DCI) 全球市场报告

2024 年资料中心互连 (DCI) 全球市场报告 资料中心互连市场 - 2018-2028 年全球产业规模、份额、趋势、机会与预测,按类型、按应用、最终用户、地区细分

资料中心互连市场 - 2018-2028 年全球产业规模、份额、趋势、机会与预测,按类型、按应用、最终用户、地区细分 2023-2030 年全球数据中心互连市场规模研究与预测(按类型、按最终用户和地区分析

2023-2030 年全球数据中心互连市场规模研究与预测(按类型、按最终用户和地区分析 数据中心互连 (DCI) 市场:按类型、按应用(实时灾难恢復和业务连续性、工作负载和数据移动性、共享数据和资源)、按最终用户:2021-2031 年全球机会分析和行业预测

数据中心互连 (DCI) 市场:按类型、按应用(实时灾难恢復和业务连续性、工作负载和数据移动性、共享数据和资源)、按最终用户:2021-2031 年全球机会分析和行业预测 资料中心互相连接(DCI)的全球市场 - 各产品类型,各部署类型,各终端用户,各地区,各国:市场规模,考察,竞争,COVID-19影响,预测(2023年~2028年)

资料中心互相连接(DCI)的全球市场 - 各产品类型,各部署类型,各终端用户,各地区,各国:市场规模,考察,竞争,COVID-19影响,预测(2023年~2028年)