|

市场调查报告书

商品编码

1439873

生物活性材料:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Bioactive Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

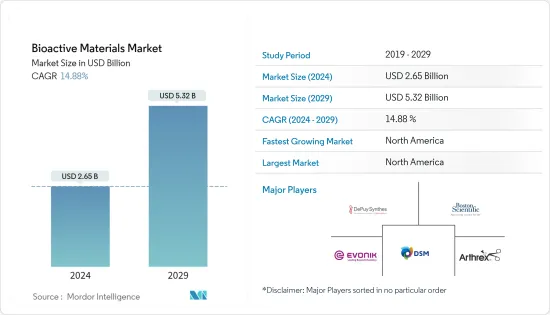

生物活性材料市场规模预计到2024年为26.5亿美元,预计到2029年将达到53.2亿美元,在预测期内(2024-2029年)增长14.88%,复合年增长率为

由于这种材料广泛应用于医疗保健行业,COVID-19 对市场产生了积极影响,对医疗保健设备的需求大幅增加。

从长远来看,牙科治疗和根管治疗需求的不断增长预计将推动市场。

主要亮点

- 另一方面,高成本、监管和潜在的毒性极大地阻碍了市场的成长。

- 整形外科不断增长的需求和新发展预计将为所研究的市场创造机会。

- 预计北美将在预测期内主导市场。

生物活性材料的市场趋势

整形外科需求增加

- 生物活性物质刺激身体的生物反应,例如与组织的结合。生物活性材料在奈米医学、生物感测器、机械联锁、骨组织癒合和牙科等领域具有应用。

- 在整形外科,羟磷石灰是最常用的生物活性陶瓷材料。生物活性材料在植入表面形成生理活性层,从而在自然组织和材料之间形成连接。透过改变生物活性材料的成分,可以实现不同的结合速率和界面结合层厚度。

- 儘管生物活性玻璃在体内具有很高的生物活性,但与金属植入相比,生物活性玻璃在整形外科手术中发挥的作用较小。生物活性玻璃是一种具有用于骨科整形外科潜力的新材料。

- 根据欧盟统计局的数据,2021 年,五分之一(20.8%)的欧盟人口年龄超过 65 岁。 2021年至2100年间,欧盟人口中80岁及以上人口的比例预计将增加一倍以上,从6.0%增加至14.6%。

- 根据国家统计局(NSO)的《2021年印度老年人口》调查,2031年印度老年人口(60岁以上)将达到1.94亿,比2021年的1.38亿增长41%,预计还会增加。

- 所有这些因素预计将在预测期内推动整形外科领域对生物活性材料的需求。

北美地区占据市场主导地位

- 随着美国高度发展的医疗保健和医疗技术领域的持续投资,北美有望主导全球市场。

- 美国医疗保健产业是该地区最先进的产业之一。根据医疗保险和医疗补助服务中心的数据,2021年至2028年,国家医疗保健支出预计将平均成长5.5%以上,到2028年将达到约61,920亿美元。

- 生物活性材料用于根管和骨缺损治疗、牙齿再生、硬组织修復和干细胞移植。生物活性玻璃和玻璃陶瓷是骨组织工程中使用的主要生物活性材料。

- 根据世界银行资料,美国65岁以上人口约占总人口的16.6%。蛀牙和牙龈问题需要更多医生的关注,并且患关节炎的风险更高。

- 根据美国整形外科医师学会 (AAOS) 的数据,肌肉骨骼疾病和关节重建(膝关节和髋关节)是美国最常见的手术。这些应用越来越多地使用生物活性材料。

- 加拿大2022年的医疗支出总额为2,457.2亿美元,预计年终将达到2,645亿美元。医疗保健产业的医疗设备产业是一个高度多元化、出口导向的产业,生产设备和消耗品。该行业由产品创新驱动。该行业可以利用加拿大大学、研究机构和医院正在进行的世界一流的创新研究,其中一些研究正在分拆为加拿大医疗设备公司。

- 进行手术需要先进的医疗设备和含有生物活性材料的零件。加上这些材料在药品中的使用,预计将在未来几年推动北美生物活性材料市场的发展。

生物活性材料产业概况

全球生物活性材料产业较为分散,主要企业占了很大的市场。主要企业包括(排名不分先后)Boston Scientific、Depuy Synthes、Evonik Industries、DSM 和 Arthrex。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 牙科治疗和根管治疗的需求不断增长

- 医疗产业应用不断增加

- 抑制因素

- 高成本、法规和潜在毒性

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争程度

第五章市场区隔(收益市场规模)

- 材料类型

- 生物活性玻璃

- 生物活性陶瓷

- 生物活性复合材料

- 其他材料类型

- 目的

- 整形外科

- 牙齿保健

- 奈米医学和生物技术

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业采取的策略

- 公司简介

- Arthrex Inc.

- Bioactive Bone Substitutes OyJ

- Biomatlante

- BTG(Boston Scientific)

- Cam Bioceramics

- Ceraver

- Collagen Matrix Inc.

- DePuy Synthes(Johnson and Johnson)

- DSM

- Evonik Industries

- Medtronic Inc.

- Noraker

- OSARTIS GmbH

- Pulpdent Corporation

- Septodont Holding

- Stryker Corporation

- Zimmer Holdings Inc.

第七章市场机会与未来趋势

- 整形外科需求不断增长和新发展

The Bioactive Materials Market size is estimated at USD 2.65 billion in 2024, and is expected to reach USD 5.32 billion by 2029, growing at a CAGR of 14.88% during the forecast period (2024-2029).

As the material is widely used in the healthcare industry, COVID-19 had a positive impact on the market, as the demand for healthcare equipment grew significantly.

Over the long term, the growing demand for dental care and root canal treatment will drive the market.

Key Highlights

- On the flip side, high costs, regulations, and probable toxicity hinder market growth significantly.

- The rising demand for orthopedics and new developments are expected to create opportunities for the market studied.

- North America is expected to dominate the market during the forecast period.

Bioactive Materials Market Trends

Growing Demand from Orthopedics

- Bioactive materials stimulate a biological response from the body, such as bonding to the tissue. Bioactive materials find their application in nanomedicine and biosensors, mechanical interlocks, bone tissue healings, and dental, amongst others.

- In orthopedic surgery, hydroxyapatite is the most commonly utilized bioactive ceramic material. Bioactive materials create a physiologically active layer on the implant's surface, resulting in a link between the native tissues and the substance. Changing the composition of the bioactive material allows a wide variety of bonding rates and interfacial bonding layer thickness.

- Bioactive glasses, despite their higher bioactivity within the body, serve a minor role in orthopedic surgery compared to metallic implants. Bioactive glass is a new material that has the potential to be employed in surgical orthopedics.

- According to Eurostat, in 2021, a fifth of the EU population (20.8%) was 65 or older. Between 2021 and 2100, the proportion of people aged 80 and up in the EU's population is expected to more than double, from 6.0% to 14.6%.

- According to the National Statistical Office's (NSO) Old in India 2021 study, India's elderly population (aged 60 and more) is expected to reach 194 million in 2031, up by 41% from 138 million in 2021.

- All such factors are expected to drive the demand for bioactive materials in the orthopedics sector during the forecast period.

North America Region to Dominate the Market

- North America is expected to dominate the global market due to the highly developed healthcare sector in the United States and the continuous investments to advance the medical technology sector.

- The healthcare sector in the United States is one of the most advanced in the region. According to the Centers for Medicare and Medicaid Services, during 2021-2028, national healthcare spending is projected to grow at an average of more than 5.5% and reach approximately USD 6.192 trillion by 2028.

- Bioactive materials are used in root canal and bone defect treatment, tooth regeneration, hard tissue repairs, and stem cell transplantation. Bioactive glasses and glass ceramics are major bioactive materials used in bone tissue engineering.

- According to World Bank data, the population above 65 years of age in the United States stood at around 16.6% of the total population. They require more medical attention for tooth decay and gum problems and pose a higher risk of arthritis.

- According to the American Academy of Orthopedic Surgeons (AAOS), musculo skeletal diseases and replacement of joints (knee and hip) are the most common surgeries among the American population. These applications increasingly use bioactive materials.

- In 2022, total health expenditure in Canada was valued at USD 245.72 billion and is expected to reach USD 264.5 billion by end of this year. In the healthcare industry, the medical device sector is a highly diversified and export-oriented industry that manufactures equipment and supplies. The sector is driven by product innovations. The industry can draw on world-class innovative research conducted in Canadian universities, research institutes, and hospitals, some of which are spun off into Canadian medical device companies.

- Performing surgeries requires advanced medical devices and components, including bioactive materials.This, along with the use of these materials in pharmaceutical, is expected to drive the market for bioactive materials through the years to come in North America.

Bioactive Materials Industry Overview

The global bioactive materials industry is fragmented, with the top players accounting for a major share of the market. Some major companies are Boston Scientific, Depuy Synthes, Evonik Industries, DSM, and Arthrex, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Dental Care and Root Canal Treatment

- 4.1.2 Increasing Applications in Medical Industry

- 4.2 Restraints

- 4.2.1 High Cost, Regulations, and Probable Toxicity

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

- 5.1 Material Type

- 5.1.1 Bioactive Glass

- 5.1.2 Bioactive Ceramics

- 5.1.3 Bioactive Composites

- 5.1.4 Other Material Types

- 5.2 Application

- 5.2.1 Orthopedics

- 5.2.2 Dental Care

- 5.2.3 Nanomedicines and Biotechnology

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arthrex Inc.

- 6.4.2 Bioactive Bone Substitutes OyJ

- 6.4.3 Biomatlante

- 6.4.4 BTG (Boston Scientific)

- 6.4.5 Cam Bioceramics

- 6.4.6 Ceraver

- 6.4.7 Collagen Matrix Inc.

- 6.4.8 DePuy Synthes (Johnson and Johnson)

- 6.4.9 DSM

- 6.4.10 Evonik Industries

- 6.4.11 Medtronic Inc.

- 6.4.12 Noraker

- 6.4.13 OSARTIS GmbH

- 6.4.14 Pulpdent Corporation

- 6.4.15 Septodont Holding

- 6.4.16 Stryker Corporation

- 6.4.17 Zimmer Holdings Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand from Orthopedics and New Developments

生物活性材料市场:按材料、按应用划分 - 2025-2030 年全球预测

生物活性材料市场:按材料、按应用划分 - 2025-2030 年全球预测 生物活性薄膜市场(材料:天然聚合物和合成聚合物;应用:医疗保健、食品包装、工业等)- 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测

生物活性薄膜市场(材料:天然聚合物和合成聚合物;应用:医疗保健、食品包装、工业等)- 2024-2034 年全球产业分析、规模、份额、成长、趋势和预测 2024-2032年按材料(玻璃、玻璃陶瓷、复合材料等)、类型(粉末、可模塑、颗粒等)、应用(牙科、外科、生物工程等)和地区分類的生物活性材料市场

2024-2032年按材料(玻璃、玻璃陶瓷、复合材料等)、类型(粉末、可模塑、颗粒等)、应用(牙科、外科、生物工程等)和地区分類的生物活性材料市场 全球生物活性材料市场规模、份额、成长分析(按类型、按应用) - 产业预测,2023-2030 年

全球生物活性材料市场规模、份额、成长分析(按类型、按应用) - 产业预测,2023-2030 年 全球生物活性材料市场按材料类型、应用和地区——规模、份额、前景和机会分析,2023-2030 年

全球生物活性材料市场按材料类型、应用和地区——规模、份额、前景和机会分析,2023-2030 年