|

市场调查报告书

商品编码

1440130

浮体式液化天然气发电厂:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Floating LNG Power Plant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

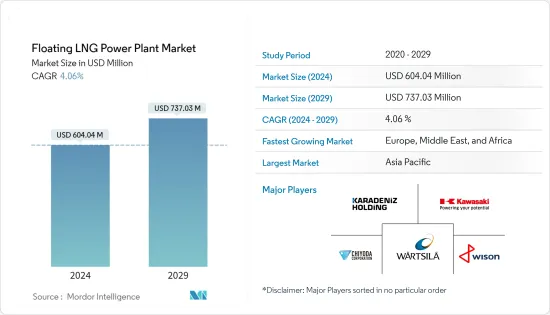

浮体式液化天然气发电厂市场规模预计到2024年为6.0404亿美元,预计到2029年将达到7.3703亿美元,在预测期内(2024-2029年)持续成长,复合年增长率为4.06%。

冠状病毒感染疾病(COVID-19)对 2020 年市场产生了负面影响。现在,市场可能达到大流行前的水平。

主要亮点

- 从长远来看,人口成长导致的电力需求增加以及新兴国家缺乏足够的电力基础设施等因素预计将推动浮体式液化天然气发电厂市场的发展。

- 另一方面,液化天然气价格的高波动性和不均匀性预计将抑制浮体式液化天然气电厂市场。

- 儘管如此,由于全球排放标准,预计未来液化天然气的采用将会增加。液化天然气是一种相对清洁的燃料,符合排放气体法规。 IMO 降低船用燃料硫含量的规定将于 2020 年生效,这可能会导致液化天然气作为船用燃料。西非沿海的石油和天然气活动也在增加,这也将为 FLNG 发电厂市场创造机会。

- 亚太地区最近占据了重要的市场占有率,预计将在预测期内成为最大和最快的市场。

浮体式液化天然气发电厂的市场趋势

电力驳船领域预计将主导市场

- 电力驳船是安装在扁平浮体结构上的发电厂设备。与动力船不同,驳船没有自航系统从一个地方移动到另一个地方,这降低了驳船的生产成本。

- 这些动力驳船没有自航式移动系统,由其他小船或船隻移动。驳船推进引擎节省的空间可用于更有效的船内空间。

- 由于发电资本投资低或基础设施可用性低的国家越来越多地安装基于浮体式天然气的浮动发电厂,电力驳船市场预计在未来几年将显着增长。

- 动力驳船具有多项优势,将推动其在 FLNG 发电领域的采用。这些用于降低运输成本和大批量运输,并且有多种尺寸可供选择。这些驳船即使在低潮时也能航行,产生能量并在漂浮时成功运输各种类型的货物。

- 驳船设计用于在特定水域中运行,并且驳船在其整个生命週期中只能在该水域中运行。如果驳船要在其他水域使用,则必须由拖船适当拖曳或协助。

- 2021年12月,惠生海工与MAN Energy Solutions签署了开发电力解决方案的谅解备忘录。双方计划在动力驳船和浮体式液化天然气发电工程上合作,这将很好地体现双方在技术和应用方面的优势。

- 因此,由于上述几点,电力驳船预计将在预测期内主导浮体式液化天然气发电厂市场。

预计亚太地区将主导市场

- 在亚太地区,能源供需缺口往往透过煤炭、水力、天然气、核能和可再生能源技术等资源来缓解。大多数国家已经实现了显着的电力供应水准。另一方面,再生能源来源已最大程度地克服了电力可靠性问题,这表明浮体式液化天然气发电厂市场不太可能在该地区发展。

- 然而,东南亚很少国家引进浮动电厂来保障能源供应。据马来西亚能源局称,2039年电力需求预计将达到约24GW。为了满足不断增长的需求,各国政府正在采取措施扩大能源系统,包括浮体式液化天然气发电厂来满足这项需求。

- 2023年,马来西亚国家石油公司与Kejurtelan Asastela (KAB)签订合同,开发和营运一座52MW浮体式液化天然气发电厂,价值5,220万美元。浮体式液化天然气发电厂将位于沙巴。开发工作预计将于 2023 年第二季开始。斯里兰卡政府也同意与亚洲开发银行合作,于 2022 年对一座浮体式液化天然气发电厂进行可行性研究,有助于实现该国能源结构的多元化。

- 此外,2022年,印尼将接受设计用于液化天然气运作的浮体式发电驳船,这很可能满足该国的发电需求。 BMPP Nusantara 1 有潜力满足该国偏远地区的电力需求,帮助企业和居民最大限度地减少对发电驳船租赁的依赖。

- 因此,由于上述几点,亚太地区预计将在预测期内主导浮体式液化天然气发电厂市场。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 调查先决条件

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2028 年之前的市场规模与需求预测(十亿美元)

- 最新趋势和发展

- 政府政策法规

- 市场动态

- 促进因素

- 抑制因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 元件类型

- 燃气引擎或燃气涡轮机

- 内燃机

- 蒸气涡轮和发电机

- 船型

- 动力船

- 动力驳船

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 南美洲

- 中东和非洲

第六章 竞争形势

- 合併、收购、合作和合资企业

- 主要企业采取的策略

- 公司简介

- Kawasaki Heavy Industries Ltd

- Wartsila Oyj Abp

- Siemens Energy AG

- Waller Marine Inc.

- Wison Group

- Chiyoda Corporation

- Karadeniz Holding

第七章市场机会与未来趋势

简介目录

Product Code: 70155

The Floating LNG Power Plant Market size is estimated at USD 604.04 million in 2024, and is expected to reach USD 737.03 million by 2029, growing at a CAGR of 4.06% during the forecast period (2024-2029).

COVID-19 negatively impacted the market in 2020. Presently the market is likely to reach pre-pandemic levels.

Key Highlights

- Over the long term, factors such as increasing demand for power due to increasing population and the lack of proper power infrastructures in developing countries are expected to drive the floating LNG power plant market.

- On the other hand, high volatility and uneven LNG prices are expected to restrain the floating LNG power plant market.

- Nevertheless, LNG adoption is expected to increase in the future owing to global emission norms. LNG being a comparatively cleaner fuel fulfills emission regulations. In 2020, IMO's reduced sulfur content in maritime fuel came into force, which is likely to result in the adoption of LNG as a bunker fuel. Offshore West Africa is also seeing increased oil and gas activity that, in turn, will present opportunities in the FLNG power plant market as well.

- Asia-Pacific held a significant market share recently, and it is expected to be the largest and the fastest market during the forecast period.

Floating LNG Power Plant Market Trends

Power Barge Segment Expected to Dominate the Market

- A power barge is a power plant facility installed on flat floating structures. Unlike power ships, a barge doesn't have a self-propelled system for moving from one location to the other, which cuts the cost of production for barges.

- As these power barges do not have any self-propelled moving systems, they are moved by other small boats or ships. The space saved from the propulsion engines in barges is used for more usable space in the vessel.

- The market for power barge is estimated to grow significantly in upcoming years due to the increasing installation of floating LNG-based power plants in countries with lower CAPEX for power generation or by countries having lower infrastructure availability.

- Power barges have several advantages that fuel their adoption across the FLNG power generation segment. These are used to transport bulk with lower transportation costs, and they are available in different sizes. These barges can travel in low-tide water, and they can facilitate successful transportation of any sort of cargo while producing energy and floating.

- The barge is designed to carry out for a specific water body and that barge can only run in that water body throughout its life. If that barge is used in some different water body, then it needs to be properly tugged or assisted by a tugboat.

- In December 2021, Wison Offshore and Marine signed an MoU with MAN Energy Solutions for power solutions development. The two parties will establish cooperation for power barge and floating LNG-to-power projects, which will become a good demonstration of each party's advantage in technology and application.

- Hence, owing to the above points, the power barge segment is expected to dominate the floating LNG power plant market during the forecast period.

Asia-Pacific Expected to Dominate the Market

- In the Asia-Pacific region, the supply-demand energy gap is often mitigated by sources such as coal, hydro, natural gas, nuclear, and renewable energy technologies. A significant rate of electricity access has been achieved in most of the economies. On the other hand, renewable energy sources have eradicated power reliability issues to the maximum extent, which indicates low chances for the development of a floating LNG power plants market in the region.

- However, few countries in Southeast Asia have adopted floating power plants to secure energy supplies. According to Malaysia's energy authority, the electricity demand is expected to reach about 24 GW in 2039. To cater to the growing demand, the government has taken measures to scale up energy systems, such as floating LNG power plants to fulfill the same.

- In 2023, Petronas contracted Kejuruteraan Asastera(KAB) to develop and commission a 52MW floating LNG power plant worth USD 52.2 million. The floating LNG power plant would be located at Sabah. The development work is expected to start in the second quarter of 2023. Also, the Sri Lankan government, in association with Asian Development Bank, agreed to conduct a feasibility study in 2022 on a floating LNG power plant, which could help the country to diversify its energy mix.

- Further, in 2022, Indonesia received a floating power barge designed to run on LNG, which is likely to bridge the power generation requirements in the country. BMPP Nusantara-1 holds the potential to fulfill the electricity demand of far-flung areas of the country, which would help businesses and residents minimize their dependence on rented power generation barges.

- Hence, owing to the above points, Asia-Pacific is expected to dominate the floating LNG power plant market during the forecast period.

Floating LNG Power Plant Industry Overview

The floating LNG power plant market is moderately consolidated. Some of the key players in the market (in no particular order) include Wison Group, Kawasaki Heavy Industries Ltd, Wartsila Oyj Abp, Chiyoda Corp, and Karadeniz Holding.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Component Type

- 5.1.1 Gas Engines or Gas Turbines

- 5.1.2 IC Engines

- 5.1.3 Steam Turbines & Generators

- 5.2 Vessel Type

- 5.2.1 Power Ship

- 5.2.2 Power Barge

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies Adopted by Key Players

- 6.3 Company Profiles

- 6.3.1 Kawasaki Heavy Industries Ltd

- 6.3.2 Wartsila Oyj Abp

- 6.3.3 Siemens Energy AG

- 6.3.4 Waller Marine Inc.

- 6.3.5 Wison Group

- 6.3.6 Chiyoda Corporation

- 6.3.7 Karadeniz Holding

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

02-2729-4219

+886-2-2729-4219

浮体式储存与再气化装置 (FSRU) 市场,全球 2025-2029 年

浮体式储存与再气化装置 (FSRU) 市场,全球 2025-2029 年 浮体式液化天然气 (FLNG) 市场:现状分析与未来预测 (2024年~2032年)

浮体式液化天然气 (FLNG) 市场:现状分析与未来预测 (2024年~2032年) 浮式液化天然气 (FLNG) 市场 - 按技术(LNG FPSO、FSRU 等)按最终用户(小型/中型、大型、其他)、按地区分類的全球行业规模、份额、趋势、机会和预测& 竞赛, 2019 -2029F

浮式液化天然气 (FLNG) 市场 - 按技术(LNG FPSO、FSRU 等)按最终用户(小型/中型、大型、其他)、按地区分類的全球行业规模、份额、趋势、机会和预测& 竞赛, 2019 -2029F 浮体式液化天然气市场:按容量、按技术划分 - 2025-2030 年全球预测

浮体式液化天然气市场:按容量、按技术划分 - 2025-2030 年全球预测 全球浮体式储存再气化装置市场:按组件、按容器类型、按容量、按设计类型、按运营、按最终用户行业、按应用 - 预测 2025-2030

全球浮体式储存再气化装置市场:按组件、按容器类型、按容量、按设计类型、按运营、按最终用户行业、按应用 - 预测 2025-2030 浮动储存再气化装置市场,按建筑类型、储存类型、应用、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

浮动储存再气化装置市场,按建筑类型、储存类型、应用、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 全球 FSRU(浮式储存和再气化装置)市场规模研究,按建筑(新建、改造)、储存(小型、中型、大型)、应用(工业、发电、其他)和区域预测 2022-2032

全球 FSRU(浮式储存和再气化装置)市场规模研究,按建筑(新建、改造)、储存(小型、中型、大型)、应用(工业、发电、其他)和区域预测 2022-2032 浮式液化天然气 (FLNG) 终端市场(技术:LNG FPSO、FSRU 等;产品:小型/中型、大型等)- 全球产业分析、规模、份额、成长、趋势和预测, 2024-2034

浮式液化天然气 (FLNG) 终端市场(技术:LNG FPSO、FSRU 等;产品:小型/中型、大型等)- 全球产业分析、规模、份额、成长、趋势和预测, 2024-2034 浮体式液化天然气 (FLNG) 市场:按技术、按容量划分:2023-2032 年全球机会分析与产业预测

浮体式液化天然气 (FLNG) 市场:按技术、按容量划分:2023-2032 年全球机会分析与产业预测 浮式液化天然气 (FLNG) 市场:2024-2034

浮式液化天然气 (FLNG) 市场:2024-2034