|

市场调查报告书

商品编码

1440203

分散式能源管理系统:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Distributed Energy Resource Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

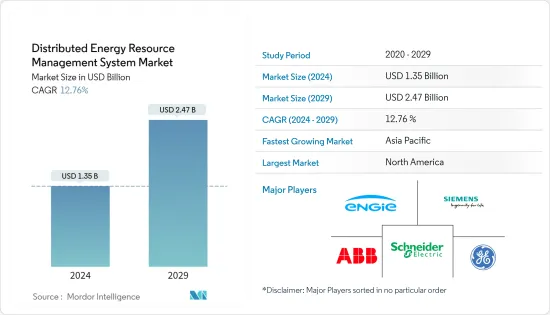

分散式能源管理系统市场规模预计到 2024 年为 13.5 亿美元,预计到 2029 年将达到 24.7 亿美元,在预测期内(2024-2029 年)复合年增长率为 12.76%。

主要亮点

- 从中期来看,对高效能源管理系统的需求不断增加以及再生能源来源的普及不断提高等因素预计将成为预测期内分散式能源管理系统(DERMS)市场的最重要驱动因素。会有一个。

- 另一方面,实施 DERMS 需要初始成本。这对预测期间的分散式能源管理系统(DERMS)市场构成威胁。

- 儘管如此,在亚太和非洲低电气化地区引入分散式发电预计将在不久的将来成为市场机会。

- 由于政府对分散式发电技术的支持政策以及可再生能源在能源结构中所占份额的增加,预计北美将在预测期内成为最大的市场。

分散式能源管理系统 (DERMS) 市场趋势

光伏(PV)领域主导市场

- 太阳能可以安装在屋顶或地面,是世界上最大的分散式电源之一。预计该细分市场的装置容量将在平均装置成本(美元/千瓦)降低的支持下增加,从而推动分散式能源管理系统的发展。分散式能源管理系统限制即时光伏(PV)输出,以防止回流和局部高电压。

- 分散式发电在经济上是可行的,并且比同类传统设施所需的资本要少得多。针对太阳能发电厂和分散式太阳能发电的税收优惠正在推动全球分散式太阳能发电。

- 根据国际可再生能源机构的数据,2022年全球装置容量为1,046.61吉瓦。随着22.4%的与前一年同期比较成长率以及政府对太阳能发电的支持目标,太阳能发电容量预计将增加。未来,很可能带动分散式能源管理系统市场。

- 成本的降低预计将大大促进中国太阳能发电的扩张,其中大部分将是公用事业规模的计划。随着新的商业和工业竞标以及住宅系统补贴,分散式太阳能发电容量预计也将迅速增加。

- 印度太阳能发电装置容量从2021年的49.34吉瓦增加到2022年的62.8吉瓦。总合包括企业规模、屋顶太阳能和分散式太阳能发电容量。因此,随着越来越多地采用太阳能作为分散式电源,对分散式能源管理系统的需求预计将会增加。

- 印度製定了到 2030 年太阳能发电量约 280 吉瓦的雄心勃勃的计划,并概述了额外支出 1950 亿印度卢比以促进当地太阳能组件製造的计划。在美国,在企业采购的支持下,太阳能投资大幅增加。

- 因此,太阳能投资的增加、政府法规的变化以及即将推出的计划预计将使太阳能发电领域成为预测期内最大的市场。

北美市场占据主导地位

- 2022 年,北美引领 DERMS 市场。此外,由于美国和加拿大支持超过100万台分散式发电机组,预计在预测期内将成为最大的市场。

- 儘管发电量充足且输配电网路可用,但洪水和风暴等自然灾害仍导致该地区部分地区停电。使用 DERMS 等远端电力系统来协调分散式能源系统可能会缓解这个问题。

- 由于初始成本相对较低且服务成本降低,分散式太阳能发电预计将显着成长,导致投资收益较短。加州和德克萨斯等许多州推出了多项整合可再生能源的法律,例如安装屋顶太阳能,预计将推动市场成长。

- 截至 2022 年,加拿大有 300 多个偏远社区依赖发电基础设施,限制了能源安全、环境健康和经济成长。与传统的中央发电机相比,分散式发电系统的核准和开发过程更快,更容易快速开发电力系统,以补充和扩大老化基础设施的使用,特别是在偏远地区,安装变得更容易。

- 许多北美电力公司需要一种更好的方法来管理和控制其配电系统内的资产。分散式能源(DER)的高普及将在实现排放目标和满足更高的能源需求方面发挥关键作用。

- 根据国际可再生能源机构的数据,美国到 2022 年安装了 111.53 吉瓦 (GW) 的太阳能装置容量,高于 2021 年的 93.91 吉瓦。预计这将创造对分散式能源管理系统的需求。

- 因此,基于这些因素,北美很可能在预测期内成为分散式能源管理系统的最大市场。

分散式能源管理系统 (DERMS) 产业概述

分散式能源管理系统市场分为两个部分:该市场的主要企业包括(排名不分先后)通用电气公司、西门子公司、ABB 有限公司、施耐德电气公司和 Engie SA。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查范围

- 市场定义

- 调查先决条件

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2028 年之前的市场规模与需求预测(美元)

- 最新趋势和发展

- 政府政策法规

- 市场动态

- 促进因素

- 对高效率能源管理系统的需求不断增长

- 普及再生能源来源

- 抑制因素

- 设定 DERMS 的初始成本较高

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 科技

- 光伏(PV)

- 试车

- 微型电网

- 其他技术

- 最终用户

- 工业的

- 住宅

- 商业的

- 区域(区域市场分析{2028年之前的市场规模与需求预测(仅限区域)})

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 俄罗斯

- 法国

- 英国

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 新加坡

- 其他亚太地区

- 南美洲

- 巴西

- 智利

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 以色列

- 约旦

- 其他中东和非洲

- 北美洲

第六章 竞争形势

- 併购、合资、合作与协议

- 主要企业采取的策略

- 公司简介

- General Electric Company

- Siemens AG

- ABB Ltd

- Schneider Electric SE

- Engie SA

- AutoGrid Systems Inc.

- Doosan Corporation

- Open Access Technology International Inc.

- Mitsubishi Electric Corporation

- Emerson Electric Co.

第七章市场机会与未来趋势

- 低电气化地区引进分散式发电

简介目录

Product Code: 71080

The Distributed Energy Resource Management System Market size is estimated at USD 1.35 billion in 2024, and is expected to reach USD 2.47 billion by 2029, growing at a CAGR of 12.76% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, factors such as increasing demand for efficient energy management systems, and increased penetration of renewable energy sources are expected to be one of the most significant drivers for the distributed energy resource management system (DERMS) market during the forecast period.

- On the other hand, high initial cost of setting up DERMS. This poses a threat to the distributed energy resource management system (DERMS) market during the forecast period.

- Nevertheless, the adoption of distributed power generation in the low-electrified areas of the Asia-Pacific and African regions is expected to act as an opportunity for the market soon.

- North America is expected to be the largest market during the forecast period, owing to supportive government policies for distributed power generation technology and the increasing share of renewables in the energy mix.

Distributed Energy Resource Management System (DERMS) Market Trends

Solar Photovoltaic (PV) Segment to Dominate the Market

- Solar PV can be located on rooftops or ground-mounted and is one of the largest distributed power sources globally. This segment is expected to drive the distributed energy resources management system with increased installed capacity supported by decreasing average installed cost (USD/kilowatt). Distributed energy resource management systems limit real-time photovoltaic (PV) output to prevent reverse flows and high local voltages.

- Distributed generation is economically viable, requiring significantly less capital than an equivalent traditional facility. Tax incentives for both solar stations and distributed solar generation are driving distributed solar PV globally.

- According to the International Renewable Energy Agency, the global solar PV installed capacity accounted for 1,046.61 GW in 2022. With an annual growth rate of 22.4% compared to the previous year and supportive solar PV targets of the government, solar PV capacity is expected to increase in the future, which, in turn, may drive the distributed energy resource management system market.

- Cost reductions are expected to strongly boost PV expansion in China, the majority being utility-scale projects. Distributed solar PV capacity is also expected to increase rapidly, driven by new auctions for commercial and industrial applications and subsidies for residential systems.

- India's solar PV installations in 2022 reached 62.8 GW, up from 49.34 GW in 2021. The total includes utility-scale, rooftop, and distributed-generation solar capacity. Hence, with the increased adoption of solar as distributed power, the demand for distributed energy resource management systems is expected to grow.

- India has an ambitious plan of generating about 280 GW of sun-fired electricity by 2030 and outlined plans to spend an additional INR 19,500 crore to boost local manufacturing of solar modules. In the United States, solar PV investments rose significantly, supported by corporate procurement.

- Therefore, with increased investment in solar PV and changing government regulations, coupled with upcoming projects, the solar PV segment is expected to be the largest market during the forecast period.

North America to Dominate the Market

- North America led the DERMS market in 2022. It is further expected to be the largest market during the forecast period, supported by the United States and Canada, which have more than a million distributed generation units.

- Despite enough power generation and accessibility of transmission and distribution networks, power outages are caused in some areas of the region due to natural disasters, such as flooding and storms. The use of remote power systems, such as DERMS, to regulate distributed energy systems is likely to mitigate the issue.

- Distributed solar PV generation is expected to witness significant growth due to relatively low initial costs and a reduction in service costs, leading to a short return on investment. Many states, such as California and Texas, have introduced several laws for integrating renewables, such as installing rooftop solar PV, which is expected to boost the growth of the market.

- As of 2022, more than 300 remote Canadian communities relied on power-generating infrastructure that limits energy security, environmental health, and economic growth. Compared to a traditional central power generator, the faster process of approving and developing a distributed generation system facilitates a quick-off-the-ground electrical system to supplement and extend the use of aging infrastructure, especially in remote areas.

- Many North American utilities need better ways to manage and control assets in their distribution system. The high penetration of distributed energy resources (DER) is set to play a vital role in achieving emission targets and meeting higher energy demand.

- As per the International Renewable Energy Agency, the United States installed 111.53 gigawatts (GW) of solar PV capacity in 2022, greater than 93.91 GW in 2021. This is expected to create demand for distributed energy resource management systems.

- Therefore, based on these factors, North America is likely to be the largest market for distributed energy resource management systems during the forecast period.

Distributed Energy Resource Management System (DERMS) Industry Overview

The distributed energy resource management system market is semi fragmented. Some of the major players in the market (in no particular order) include General Electric Company, Siemens AG, ABB Ltd, Schneider Electric SE, and Engie SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Efficient Energy Management Systems

- 4.5.1.2 Increased Penetration of Renewable Energy Sources

- 4.5.2 Restraints

- 4.5.2.1 High Initial Cost of Setting Up DERMS

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.2 Electric Vehicles

- 5.1.3 Microgrids

- 5.1.4 Other Technologies

- 5.2 End User

- 5.2.1 Industrial

- 5.2.2 Residential

- 5.2.3 Commercial

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 Russia

- 5.3.2.3 France

- 5.3.2.4 United Kingdom

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Singapore

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Chile

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.6 United Arab Emirates

- 5.3.7 Israel

- 5.3.8 Jordon

- 5.3.9 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 General Electric Company

- 6.3.2 Siemens AG

- 6.3.3 ABB Ltd

- 6.3.4 Schneider Electric SE

- 6.3.5 Engie SA

- 6.3.6 AutoGrid Systems Inc.

- 6.3.7 Doosan Corporation

- 6.3.8 Open Access Technology International Inc.

- 6.3.9 Mitsubishi Electric Corporation

- 6.3.10 Emerson Electric Co.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Adoption of Distributed Power Generation in Low-electrified Areas

02-2729-4219

+886-2-2729-4219

分散式能源管理系统 (DERMS) 的全球市场:按产品、按应用、按最终用户、按地区 - 预测至 2029 年

分散式能源管理系统 (DERMS) 的全球市场:按产品、按应用、按最终用户、按地区 - 预测至 2029 年 分散式能源管理系统的全球市场(按组件、按应用、按最终用户、按地区):趋势分析、竞争格局、未来预测(2019-2030)

分散式能源管理系统的全球市场(按组件、按应用、按最终用户、按地区):趋势分析、竞争格局、未来预测(2019-2030) 2024 年分散式能源管理系统 (DERMS) 全球市场报告

2024 年分散式能源管理系统 (DERMS) 全球市场报告 分散式能源管理系统市场规模、份额和成长分析:按组件、最终用途、应用、地区 - 产业预测,2024-2031 年

分散式能源管理系统市场规模、份额和成长分析:按组件、最终用途、应用、地区 - 产业预测,2024-2031 年 到 2030 年分散式能源管理系统市场预测 - 按组件、应用、最终用户和地理位置进行的全球分析

到 2030 年分散式能源管理系统市场预测 - 按组件、应用、最终用户和地理位置进行的全球分析 Guidehouse Insights Leaderboard Report-DERMS提供者:评估 10家Grid DERMS供应商和15家Grid Edge DERMS平台供应商策略.执行情况

Guidehouse Insights Leaderboard Report-DERMS提供者:评估 10家Grid DERMS供应商和15家Grid Edge DERMS平台供应商策略.执行情况 2023年至2028年分散式能源管理系统市场预测

2023年至2028年分散式能源管理系统市场预测 分散式能源管理系统市场 - 全球产业规模、份额、趋势、机会和预测。 2018-2028F 按软体、按应用、最终用户、地区细分

分散式能源管理系统市场 - 全球产业规模、份额、趋势、机会和预测。 2018-2028F 按软体、按应用、最终用户、地区细分 全球分布式能源资源管理系统 (DERMS) 市场 - 2023-2030 年

全球分布式能源资源管理系统 (DERMS) 市场 - 2023-2030 年 全球分布式能源管理系统市场2023-2030

全球分布式能源管理系统市场2023-2030

▼