|

市场调查报告书

商品编码

1440228

游戏 GPU - 市占率分析、产业趋势与统计、成长预测(2024 - 2029 年)Gaming GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

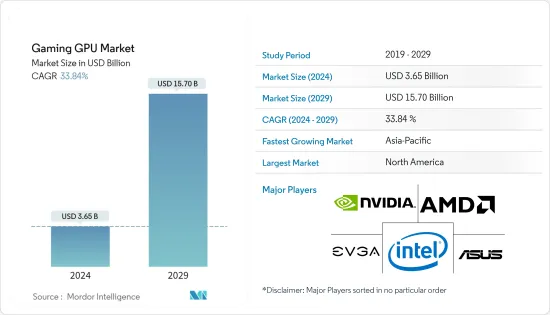

游戏 GPU 市场规模预计 2024 年为 36.5 亿美元,预计到 2029 年将达到 157 亿美元,在预测期内(2024-2029 年)CAGR为 33.84%。

千禧世代游戏化趋势的兴起导致电玩玩家越来越多地采用虚拟世界。游戏机也从餐厅、游乐场和酒吧中强大的基于位置的设备发展到游戏机和个人电脑形式的家用游戏机。随着摩尔定律降低了晶片价格并提高了性能,人们购买了更多的家用游戏机,这会产生积极的价格弹性效应,但会牺牲基于位置的游戏机。随着过去几年游戏机销量的成长,对游戏 GPU 的需求也显着成长。

主要亮点

- 随着智慧型手机、平板电脑、个人电脑和游戏机越来越多地用于游戏目的,对图形密集型游戏应用程式的高阶运算系统的需求也在增加。对能够处理与游戏所需的 2D 和 3D 图形相关的复杂数学计算的专用处理器的需求不断增长,推动了 GPU 市场需求。

- 高效能运算领域的技术进步也可能为 GPU 供应商带来机会。例如,今年 4 月,Nvidia 表示,研究人员使用配备 NVIDIA GPU 的超级电脑发现了 4 月 25 日哈伯资料的趋势。此外,高效能运算与 NVIDIA GPU 结合使用,可加深对所有行星的了解并分析其炎热的大气层。

- 市场的其他驱动力包括汽车、製造、房地产和医疗保健等垂直行业,以及支援图形应用和 3D 内容的处理器的使用不断增加。例如,在汽车行业的製造和设计应用中,CAD 和模拟软体使用 GPU 为关键应用创建逼真的图像和动画。

- 游戏 GPU 使用先进的技术和材料。造成当前 GPU 高价格的主要因素之一是较高的製造费用。只有生产者能够负担得起的材料才能生产。由于製造成本上升导致 GPU 售价上涨,生产商正在考虑在不牺牲产品品质或数量的情况下实现利润最大化。由于庞大的初始投资,消费者更愿意在他们的设备中使用最新游戏 GPU 以外的其他东西,这对市场成长来说是一个挑战。

- 现代电玩控制台和伺服器使用许多组件,包括游戏 GPU 电路。由于供应链问题,COVID-19 威胁了许多此类组件的平均生产。然而,半导体代工厂开始恢復生产,这刺激了市场上的製造商。云端运算、游戏、资料中心伺服器、自动化和人工智慧技术的需求可以帮助 GPU 製造商在疫情后期恢復成长。

游戏 GPU 市场趋势

产业对游戏机、扩增实境 (AR) 和虚拟实境 (VR) 的需求不断增长正在推动市场发展

随着电子竞技和其他类型线上游戏的日益普及,游戏机上的视频游戏正在兴起,并将在未来几年呈现出更多的成长机会。由于这一趋势,连接和娱乐提供者可以透过提供与游戏机相关的视讯服务产品(例如快速宽频和体育直播)来瞄准游戏机游戏玩家,并透过 OTT 服务以最佳方式透过观众获利。电玩游戏开发商可以为游戏订阅服务提供高价,包括存取电子竞技赛事和原创内容。

- 随着云端游戏的兴起,GPU市场近年来呈现上升趋势。 Blade 是 Shadow 背后的法国新创公司,是一项面向游戏玩家的云端运算服务,允许玩家按月付费访问资料中心的游戏 PC。与其他云端游戏服务相比,该公司提供完整的 Windows 11 功能。该公司目前提供每月 35 美元的单一配置,配备 Intel Xeon 2620 处理器、Nvidia Quadro P5000 GPU 和 Nvidia GeForce GTX 1080、8 个执行绪、12GB RAM 和 256GB 储存。

- 此外,主要游戏开发商也专注于开发具有高图形品质的基于主机的游戏,为游戏领域的成长做出了贡献。索尼和微软优先考虑高达 120 fps 的刷新率,而不是试图将游戏机推销为支援 8K,从而实现无缝的游戏体验。 Nvidia 正试图透过其强大的 RTX 3090 显示卡超越 4K,该显示卡可为 PC 提供 8K 游戏。

- 游戏机开发商也专注于新产品开发,以提高市场竞争的门槛。索尼的目标是10.28 teraflops 的性能,这比Xbox Series X 低了近15%。散热和架构方面也存在一些根本差异,这使得索尼能够提供可变的GPU 和CPU 速度,而微软则坚持更传统的在固定速度速度方面,4K 性能与索尼非常接近。

- AR 和 VR 在各种应用中的日益普及预计将推动 GPU 的采用。由于图形技术的改进,现在可以实现真正的 AR 或 VR 并创造引人注目的用户体验。许多公司正在开发 VR 解决方案,主要是为了重新定义人们体验运算和游戏的方式,这些公司也在开发用于 AR 和 VR 应用程式的 GPU 系统。

北美预计将占据重要份额

过去几年,北美地区千禧世代的游戏需求急剧增长。据 Limelight Networks 称,在美国,超过 30% 的电玩玩家为游戏订阅服务付费,超过 35% 的人每周至少玩一次线上电玩游戏。

- 主要技术开发商正在投资北美游戏市场的线上游戏,进一步推动该地区的市场成长。今年1月,美国跨国企业微软宣布计画收购游戏开发与互动娱乐内容发行领域的知名企业动视暴雪公司。此次收购可能会加速微软游戏业务在行动、PC、游戏机和云端领域的成长,预计将推动对该公司 Xbox 产品的需求。

- 此外,今年3月,英特尔推出了适用于笔记型电脑和桌上型电脑的Arc系列图形处理单元(GPU)。配备Arc 3 GPU 的笔记型电脑专为增强游戏和内容製作而设计,现已接受预订,而配备Arc 5 和Arc 7 GPU 的笔记型电脑专为高级和高效能游戏而设计,将于今年稍后上市。

- 云端游戏公司受益于与电信公司的合作,开发更好的端到端网路并鼓励该地区采用 5G。电信公司增加上游容量以满足电竞玩家需求的需求是进一步的驱动力,各个供应商正在合作以满足他们的游戏需求。

该地区的游戏 GPU 厂商也专注于开发 GPU 产品,进一步推动该地区的成长。例如,去年 7 月,AMD 推出了 AMD Radeon RX 6600XT 系列显示卡产品,利用 AMD RDNA 架构的强大功能,同时凭藉 9.6 teraflops 的 RDNA 2 技术和 8 GB GDDR6 RAM 提供更好的效能。

游戏 GPU 产业概览

游戏 GPU 市场显着整合,全球和区域参与者较少。这些参与者占据了重要的市场份额,并专注于扩大全球客户群。这些供应商专注于研发投资,引入新的解决方案、策略联盟以及其他有机和无机成长策略,以在预测期内获得竞争优势。

2022 年 11 月,华硕更新了 TUF Gaming GeForce RTX 3060 Ti 和 Dual GeForce RTX 3060 Ti 显示卡,加入 GDDR6X 内存,以获得更好的性能。 3060 Ti 的功能透过添加 GDDR6X RAM 得到了改进,这为挑剔的 PC DIY 建造者提供了更多的选择。华硕生产了一款配备 8 GB GDDR6 VRAM 的全新 GeForce RTX 3060,以提高 GPU 的客製化和组装能力。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争激烈程度

- 产业价值链分析

- COVID-19 对产业影响的评估

- 市场驱动因素

- 产业对游戏机、扩增实境 (AR) 和虚拟实境 (VR) 的需求不断增长

- 对具有更高刷新率的高级显示器的需求不断增加

- 市场限制

- 初始投资高

第 5 章:市场细分

- 类型

- 专用显示卡

- 整合显示卡解决方案

- 其他市场类型

- 装置

- 行动装置

- 个人电脑和工作站

- 游戏机

- 汽车

- 其他设备

- 地理

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第 6 章:竞争格局

- 公司简介

- Intel Corporation

- Advanced Micro Devices Inc.

- Nvidia Corporation

- ASUSTEK Computer Inc

- GIGA-BYTE Technology Co., Ltd.

- Arm Limited

- Qualcomm Technologies Inc.

- Imagination Technologies Group

- EVGA Corporation

- SAPPHIRE Technology Limited

第 7 章:投资分析

第 8 章:市场的未来

The Gaming GPU Market size is estimated at USD 3.65 billion in 2024, and is expected to reach USD 15.70 billion by 2029, growing at a CAGR of 33.84% during the forecast period (2024-2029).

The rising gamification trend among millennials has led to the increasing adoption of a virtual world for video gamers. Gaming machines have also evolved from powerful location-based devices found in restaurants, arcades, and bars to in-home machines in the form of gaming consoles and then PCs. As Moore's Law drove down chip prices and increased performance, people bought more gaming machines for the home, which has a positive price elasticity effect at the expense of location-based gaming machines. As gaming machine sales have increased in the last few years, the demand for gaming GPUs has grown significantly.

Key Highlights

- The demand for high-end computing systems for graphics-intensive gaming applications has increased with the rising adoption of smartphones, tablets, PCs, and consoles for gaming purposes. The growing demand for specialized processors that can handle complex mathematical calculations related to the 2D and 3D graphics required for gaming drives the GPU market demand.

- Technological advancement in high-performing computing may also develop an opportunity for GPU vendors. For instance, in April this year, Nvidia stated that researchers discovered trends in Hubble data on April 25 using a supercomputer with NVIDIA GPUs. Also, high-performance computing is used with NVIDIA GPUs to increase the understanding of all planets and analyze their torrid atmospheres.

- Other drivers for the market include industry verticals such as automotive, manufacturing, real estate, and healthcare, with the rising usage of processors to support graphics applications and 3D content. For instance, in manufacturing and design applications in the automotive sector, CAD and simulation software uses GPUs to create realistic images and animations for critical applications.

- Gaming GPUs use advanced technologies and materials. One of the primary factors contributing to the high price of current GPUs is higher manufacturing expenses. Only the materials that producers can afford can be produced. Producers are thinking of maximizing their profits without sacrificing a product's quality or quantity due to rising manufacturing costs, which cause a rise in the selling price of the GPU. Due to this huge initial investment, consumers prefer to use something other than the latest gaming GPU in their devices, which is a challenge for market growth.

- Modern-day video game consoles and servers utilize many components, including gaming GPU circuits. COVID-19 threatened the average production of many of these components due to supply chain problems. However, semiconductor foundries started resuming production, which motivated manufacturers in the market. Demand in cloud computing, gaming, data center servers, automation, and AI technologies could help GPU manufacturers revive growth in the later part of the pandemic.

Gaming GPU Market Trends

Rising Demand for Gaming Consoles, Augmented Reality (AR), and Virtual Reality (VR) in the industry are Driving the Market

With the increasing adoption of esports and other types of online gaming, video games on consoles are rising and will show more growth opportunities in the coming years. As a result of this trend, connectivity and entertainment providers could target console gamers by offering console-related video services offerings, like fast broadband and live sports, and optimally monetizing the audience through OTT services. Video game developers could provide premium pricing for gaming subscription services, including access to esports events and original content.

- With the rising trend of cloud gaming, the GPU market has seen an upward trend in recent years. Blade, the French startup behind Shadow, is a cloud computing service for gamers that allows a player to access a gaming PC in a data centre for a monthly subscription fee. The company provides full Windows 11 features compared to other cloud gaming services. The company currently offers a single configuration for USD 35 per month with eight threads on an Intel Xeon 2620 processor, an Nvidia Quadro P5000 GPU, and an Nvidia GeForce GTX 1080, 12GB of RAM, and 256GB of storage.

- Further, major game developers are also focusing on developing console-based games with high graphic quality, contributing to the gaming segment's growth. Sony and Microsoft prioritize refresh rates up to 120 fps instead of trying to market the consoles as 8K capable, making the gaming experience seamless. Nvidia is trying to move beyond 4K with its monster RTX 3090 graphics card, which delivers 8K gaming for PCs.

- Console developers are also focusing on new product development to raise the bar for the competition in the market. Sony is aiming for 10.28 teraflops of performance, which is almost 15% less than the Xbox Series X. There are also some fundamental differences in cooling and architecture that allow Sony to offer variable GPU and CPU speeds, while Microsoft sticks to the more traditional fixed speeds and is very close to Sony in terms of 4K performance.

- The increasing incorporation of AR and VR in various applications is expected to drive the adoption of GPUs. Due to improvements in graphics technology, it is now possible to achieve true AR or VR and create a compelling user experience. Many companies are developing VR solutions primarily to redefine the way people experience computing and gaming, and the companies are also developing GPU systems for AR and VR applications.

North America is Expected to Hold a Significant Share

The rise in gaming among millennials in the North American region has been dramatic and swift in the past few years. In the United States, over 30% of video gamers pay for gaming subscription services, and more than 35% play online video games at least once a week, according to Limelight Networks.

- Major technology developers are investing in online gaming in the North American gaming market, further bolstering the region's market growth. In January of this year, Microsoft, an American MNC, announced plans to acquire Activision Blizzard Inc., a prominent player in game development and interactive entertainment content publishing. This acquisition may accelerate the growth of Microsoft's gaming business across mobile, PC, console, and cloud and is expected to drive demand for the company's Xbox offerings.

- Additionally, in March of this year, Intel launched the Arc series of Graphics Processing Units (GPU) for laptops and desktop PCs. Laptops with the Arc 3 GPU, designed for enhanced gaming and content production, are available for pre-order, while laptops with the Arc 5 and Arc 7 GPUs, designed for advanced and high-performance gaming, will come later in the current year.

- Cloud gaming companies benefit from collaborating with telecoms to develop better end-to-end networks and encourage 5G adoption in the region. The need for telecoms to increase their upstream capacity to meet the demands of esports players is a further driving force, and various vendors are collaborating to meet their gaming needs.

Gaming GPU players in the region also focus on developing GPU products, further driving the region's growth. For instance, in July last year, AMD introduced the AMD Radeon RX 6600XT series graphics products, harnessing the power of the AMD RDNA architecture while providing better performance with its 9.6 teraflops of RDNA 2 technology and 8 GB of GDDR6 RAM.

Gaming GPU Industry Overview

The gaming GPU market is significantly consolidated and consists of fewer global and regional players. These players account for a significant market share and focus on expanding their customer base globally. These vendors focus on research and development investment in introducing new solutions, strategic alliances, and other organic & inorganic growth strategies to earn a competitive edge over the forecast period.

In November 2022, ASUS updated its TUF Gaming GeForce RTX 3060 Ti and Dual GeForce RTX 3060 Ti graphics cards to include GDDR6X memory for better performance. The 3060 Ti's capabilities have been improved by the addition of GDDR6X RAM, which expands the options available to discerning PC DIY builders. ASUS has produced a new GeForce RTX 3060 with 8 GB of GDDR6 VRAM to increase the GPU's capacity for customization and assembly.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Industry

- 4.5 Market Drivers

- 4.5.1 Rising Demand for Gaming Consoles, Augmented Reality (AR), and Virtual Reality (VR) in the industry

- 4.5.2 Increasing Demand for Advanced Displays with Higher Refresh Rates

- 4.6 Market Restraints

- 4.6.1 High Initial Investment

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Dedicated Graphic Cards

- 5.1.2 Integrated Graphics Solutions

- 5.1.3 Other Market Types

- 5.2 Device

- 5.2.1 Mobile Devices

- 5.2.2 PCs and Workstations

- 5.2.3 Gaming Consoles

- 5.2.4 Automotive

- 5.2.5 Other Devices

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Intel Corporation

- 6.1.2 Advanced Micro Devices Inc.

- 6.1.3 Nvidia Corporation

- 6.1.4 ASUSTEK Computer Inc

- 6.1.5 GIGA-BYTE Technology Co., Ltd.

- 6.1.6 Arm Limited

- 6.1.7 Qualcomm Technologies Inc.

- 6.1.8 Imagination Technologies Group

- 6.1.9 EVGA Corporation

- 6.1.10 SAPPHIRE Technology Limited