|

市场调查报告书

商品编码

1440270

流量计 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029 年)Flow Meters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

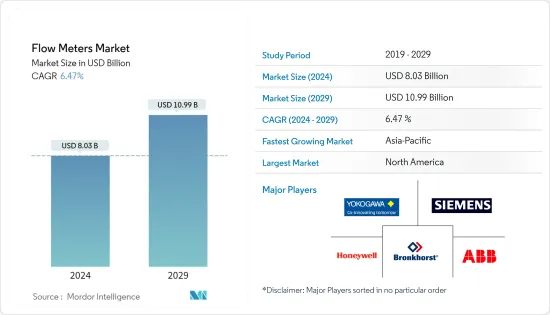

流量计市场规模预计到 2024 年为 80.3 亿美元,预计到 2029 年将达到 109.9 亿美元,在预测期内(2024-2029 年)CAGR为 6.47%。

流量计,称为流量感测器,是主要测量或调节管道内液体和气体流量的电子设备。它们通常用于暖通空调系统、医疗设备、化工厂和化粪池系统。这些仪表主要可以检测洩漏、堵塞、管道爆裂以及由于污染或污染造成的液体浓度变化。

主要亮点

- 流量感测器/设备通常连接到仪表以进行测量;然而,它们也可以连接到电脑和数位介面。流量计可分为两大类:接触式流量计和非接触式流量计。当被监测的液体或气体(通常是食品)会因与运动部件接触而受到污染或物理改变时,使用非接触式流量计。

- 工业物联网、资产管理和高级诊断等多种新兴技术也有助于在用户和供应商之间形成新的合作。此外,最终用户和供应商的策略一直在利用网路和云端平台以及包括资料和分析在内的服务产品的进步。流量计也见证了监测和测量蒸汽、气体、水、化学品和矿物油等流量的需求稳定成长。这些仪表在流量测量过程中提供关于理想和经济数量的基本精度。它们在加工控制方面具有优势。

- 流量计技术的主要趋势包括流量计的数位讯号、多种测量格式、线上诊断和故障排除、远端校准和配置以及具有线上警报的智慧感测器。透过强大的研究和开发实现的技术进步也使该行业能够针对复杂的营运问题开发适当的解决方案。自动清洁也是市场上观察到的革命性趋势之一。这一趋势有利于水和废水管理等产业。

- 然而,预计某些因素会阻碍市场扩张。市场上现有的流量计仅有时与现代机器和基础设施相容。因此,需要用更新、高效且相容的仪器来取代现有的过时版本。用新一代设备更换旧仪器的费用可能是一个昂贵的过程。这肯定会限制流量计的市场。

- 石油和天然气、化学、纸浆和造纸、金属和采矿等工业部门受 Covid-19 大流行影响最大,因此这些行业的产品需求也随之下降。然而,许多服务于製药、能源和公用事业应用的工业领域的需求显着激增。此外,疫情也大大推动了工业自动化的采用,导致疫情期间的产品发布和创新增加。

流量计市场趋势

电磁流量计占据重要市场份额

- 电磁流量计利用法拉第感应定律侦测流量。电磁线圈产生磁场和捕捉电磁流量计内电压(电动势)的电极。电磁流量计由于有线圈和电极,流管内没有任何东西,可以测量流量。

- 根据法拉第感应定律,在磁场内移动的导电液体会产生电压。内管直径、磁场强度和平均流速都成正比。另外,电磁流量计与其他流量计的一个本质差异是,由于电磁流量计是靠电磁感应工作的,所以导电液体是唯一可以侦测流量的液体。

- 电磁流量计在食品工业、化学应用、天然气供应、废水、采矿和电力设施中有着广泛的应用。它们基本上不受液体温度、压力、密度和黏度的影响。

- 据美国地质调查局称,去年全球铜矿产量估计为 2,100 万吨。过去十年,全球铜产量稳定成长,从 2010 年的 1,600 万吨上升。

- 电磁流量计最初是体积流量设备,但可以透过堵塞产品的密度来测量质量流量。密度值必须保持稳定以确保准确性。在少数情况下,密度计也与电磁计一起使用来提供质量流量读数。

- 例如,采矿公司经常使用电磁流量计来测量具有特定衬里的泥浆流量,以减少磨损。密度计向电磁流量计发送资料,以转换为线上质量流量测量。全球采矿活动的成长鼓励了电磁流量计的使用。据EIA称,由于钻井活动增加,导致流量计的采用,今年美国原油产量预计将增加40万桶/日。

北美有望成为最大市场

- 北美地区预计将占据重要的市场份额,这主要是由于石油和天然气、化学品和发电行业的显着发展。北美再生能源发电产业预计也将继续对新项目进行大量投资。据IRENA称,去年全球再生能源装置容量为3.1太瓦,较上年成长9.3%。近几十年来,由于再生技术的价格下降以及对传统能源对环境影响的担忧,再生能源产业经历了扩张。

- 根据《管道与天然气杂誌》去年发表的报告,隔膜容积式流量计在美国广泛用于商业和公用事业燃气流量测量。这些仪表通常在餐厅和其他小型企业外使用来测量燃气消耗量。较大的商业机构也使用隔膜表来测量燃气消耗量,儘管在许多情况下,公用事业公司拥有该仪表。最近,在某些应用中,旋转流量计已经取代了隔膜流量计。

- 因此,为了维持废水系统的建立和组织,许多公司正在进行策略性收购以获得所需的技术专业知识。例如,2021 年 5 月,TASI 集团收购了 Mission Communication 和 Norcross GA,以补充 TASI Flow 现有的资产管理和无线连接策略,从而在水和废水处理市场上占据强大地位。

- 公司也在研究领域推出创新的数位介面和软体解决方案。例如,2021 年 2 月,艾默生推出了新软体,透过在石油和天然气行业应用 Roxar 2600 多相流量计 (MPFM) 来提高製程自动化。其快速自适应测量软体架构可协助 Roxar 2600 以 10Hz 进行平行运算,并自动选择特定时间的最佳配置。

流量计行业概况

流量计市场高度分散,主要参与者包括横河电机公司、ABB 有限公司、西门子股份公司、布琅轩鹿高科技公司和霍尼韦尔国际公司。市场参与者正在采取合作、创新和收购等策略增强他们的产品供应并获得可持续的竞争优势。

2022年9月,横河电机公司宣布推出OpreXTM电磁流量计CA系列。这个新产品系列继承了 ADMAG CA 系列,并作为 OpreX 现场仪表系列的一部分推出。这个新系列中的产品都是电容式电磁流量计,可以测量通过测量管的导电流体的流量,而无需接触设备的电极。除了非润湿电极架构之外,该系列还具有新颖的功能,可提高使用者友善性、可维护性和操作效率。

2022 年 6 月,Sensirion 透过 SFC5500 扩展了其质量流量控制器产品线。高性能质量流量控制器和仪表针对多种气体进行了校准。此功能包括直插式配件,使用者可以从合适的组件清单中轻鬆更换。每个设备可以覆盖传统设备中存在的各种流量范围。 SFC5500 是一款灵活的 SFC5500,可处理多种应用。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力——波特五力

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 替代产品的威胁

- 竞争激烈程度

- 最新技术发展

- COVID-19 对产业影响的评估

第 5 章:市场动态

- 市场驱动因素

- 物联网和自动化在流量测量应用中的渗透

- 安全和效率问题方面的工业需求不断增长

- 市场挑战

- 产品进步导致成本上升

第 6 章:市场细分

- 科技

- Coriolis

- 电磁

- 线上电磁流量计

- 小流量电磁流量计

- 插入

- 不同的压力

- 超音波

- 夹紧式

- 排队

- 其他技术

- 最终用户产业

- 油和气

- 水和废水

- 化学与石化

- 食品与饮料

- 纸浆和造纸

- 其他最终用户产业

- 地理

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 印度

- 亚太地区其他地区

- 拉丁美洲

- 中东和非洲

- 北美洲

第 7 章:竞争格局

- 公司简介

- Yokogawa Electric Corporation

- ABB Ltd

- Siemens AG

- Bronkhorst High-Tech BV

- Honeywell International Inc.

- Emerson Electric Co.

- SICK AG

- OMEGA Engineering

- Christian Burkert GmbH & Co. KG

- TSI incorporated

- Keyence Corporation

- Sensirion AG

- Azbil Corporation

- Endress+Hauser AG

- Krohne Messtechnik GmbH

第 8 章:投资分析

第 9 章:未来展望

The Flow Meters Market size is estimated at USD 8.03 billion in 2024, and is expected to reach USD 10.99 billion by 2029, growing at a CAGR of 6.47% during the forecast period (2024-2029).

Flow meters, called flow sensors, are electronic devices that primarily measure or regulate the flow rate of liquids and gases within pipes and tubes. They are commonly used in HVAC systems, medical devices, chemical factories, and septic systems. These meters can primarily detect leaks, blockages, pipe bursts, and liquid concentration changes owing to contamination or pollution.

Key Highlights

- The flow sensors/devices are generally connected to the gauges to render their measurements; however, they can also be connected to computers and digital interfaces. Flow meters can be divided into two groups, contact, and non-contact flow meters. Non-contact flow meters are used when the liquid or gas (generally, a food product) being monitored would be otherwise contaminated or physically altered by coming in contact with the moving parts.

- Multiple emerging technologies, such as IIoT, asset management, and advanced diagnostics, are also helping in forming new collaborations among users and suppliers. Moreover, the strategies for both end users and suppliers have been leveraging advancements in networking and cloud platforms and service offerings that include data and analytics. Flow meters are also witnessing a steady rise in the demand for monitoring and measuring the flow of steam, gas, water, chemicals, and mineral oil, among others. These meters offer essential precision regarding ideal and economic quantity during flow measurement. They offer advantages when it comes to processing control.

- Major trends in flow meter technology include digital signals for flow meters, multiple measurement formats, online diagnosis and troubleshooting, remote calibration and configuration, and smart sensors with online alerts. The technological advancements via robust research and development have also enabled the industry to develop appropriate solutions to complex operational problems. Automated cleaning is also one of the revolutionary trends observed in the market. This trend is advantageous for industries such as water and wastewater management.

- However, certain factors are projected to hinder market expansion. The existing flowmeters in the market are only sometimes compatible with modern machines and infrastructure. Therefore, there is a need to replace the existing outdated versions with newer, efficient, and compatible instruments. The expense of replacing the old instruments with the new generation of equipment might be a costly procedure. This will most certainly limit the market for Flow Meters.

- Industrial sectors, such as oil and gas, chemicals, pulp and paper, and metals and mining, were most affected due by the Covid-19 pandemic, thus witnessing a subsequent decline in the demand for products offered by these industries. However, demand significantly surged in many industrial sectors serving the pharmaceutical, energy, and utility applications. Furthermore, the pandemic also significantly fueled industrial automation adoption, resulting in increased product launches during the pandemic and innovation.

Flow Meters Market Trends

Electromagnetic Flow Meter Holds Significant Market Share

- Electromagnetic flow meters detect flow using Faraday's law of induction. An electromagnetic coil generates a magnetic field and electrodes that capture voltage (electromotive force) within an electromagnetic flowmeter. Due to the presence of coil and electrodes, there is nothing inside the flow pipes of an electromagnetic flow meter, and flow can be measured.

- According to Faraday's law of induction, moving conductive liquids inside the magnetic field generates voltage. The inner pipe diameter, magnetic field strength, and average flow velocity are all proportional. Also, an essential difference between electromagnetic and other flow meters is that because electromagnetic flowmeters work on electromagnetic induction, conductive liquids are the only liquids for which flow can be detected.

- Electromagnetic flowmeters have a wide range of applications in food industries, chemical applications, natural gas supplies, wastewater, mining, and power utilities. They are largely unaffected by the liquid's temperature, pressure, density, and viscosity.

- According to US Geological Survey, global copper mine production amounted to an estimated 21 million metric tons in the last year. Global copper production has steadily grown over the past decade, rising from 16 million metric tons in 2010.

- Electromagnetic flowmeters start as volumetric flow devices but can measure mass flow by plugging the product's density. The density value must remain stable for accuracy. In a few cases, a density meter is also used with electromagnetic meters to provide mass flow readings.

- For instance, mining companies often use an electromagnetic flow meter to measure slurry flow with specific liners to reduce abrasion. A densimeter sends data for the electromagnetic flowmeter to translate into an online mass flow measurement. The growth in mining activities globally is encouraging the use of electromagnetic flowmeters. According to EIA, crude oil production in the United States is expected to increase in the current year by 0.4 million b/d due to increased drilling activities, leading to flow meter adoption.

North America is Expected to Register the Largest Market

- The North American region is expected to hold a significant market share, primarily owing to the significantly developed oil and gas, chemicals, and power generation industries. The North American renewable power generation industry is also expected to continue to invest significantly in new projects. According to IRENA, In the last year, the global installed renewable energy capacity will be 3.1 terawatts, a 9.3 percent increase over the previous year. The renewable energy sector has undergone an expansion over recent decades due to decreasing pricing in renewable technologies as well as concerns about the environmental impact of more traditional sources.

- Diaphragm-positive displacement meters are widely used in the United States for commercial and utility gas flow measurement, per the Pipeline and Gas Journal report published last year. These meters are often used outside restaurants and other small businesses to measure gas consumption. Larger business establishments also use diaphragm meters to measure gas consumption, although, in many cases, the utility owns the meter. Recently, rotary meters have been replacing diaphragm meters in some applications.

- Thus, to maintain the establishment and organization of the wastewater system, many companies are making strategic acquisitions to gain the technical expertise required. For instance, in May 2021, The TASI Group of Companies acquired Mission Communication and Norcross GA to complement TASI Flow's existing Asset Management and Wireless Connectivity Strategy, enabling a strong presence in the Water and Wastewater market.

- Companies are also introducing innovative digital interfaces and software solutions in the studied segment. For instance, in February 2021, Emerson launched new software that boosts process automation with the application of the Roxar 2600 Multiphase Flow Meter (MPFM) for the oil and gas industry. Its Rapid Adaptive Measurement software architecture helps the Roxar 2600 to do the parallel calculation at 10Hz and automatically select the optimal configuration for a particular time.

Flow Meters Industry Overview

The flow meters market is highly fragmented with the presence of major players like Yokogawa Electric Corporation, ABB Ltd, Siemens AG, Bronkhorst High-Tech BV, and Honeywell International Inc. Players in the market are adopting strategies such as partnerships, innovations, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In September 2022, Yokogawa Electric Corporation announced the launch of the OpreXTM Magnetic Flowmeter CA Series. This new product series succeeded the ADMAG CA Series and was introduced as part of the OpreX Field Instruments family. The items in this new series are all capacitance-type magnetic flowmeters that can measure the flow of conductive fluids through a measurement tube without contacting the device's electrodes. This series has novel functionalities that increase user-friendliness, maintainability, and operational efficiency, in addition to the non-wetted electrode architecture.

In June 2022, Sensirion expanded its mass flow controller line with the SFC5500. The high-performance mass flow controllers and meters are calibrated for numerous gases. The feature includes push-in fittings, which the user from the list of suitable components can readily replace. Each device may cover a variety of flow ranges present in traditional devices. The SFC5500 is a flexible SFC5500 that can handle many applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter Five Forces

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Recent Technological Developments

- 4.5 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Penetration of IoT and Automation in Flow Rate Measurement Applications

- 5.1.2 Growing Industrial Demand regarding Safety and Efficiency Concerns

- 5.2 Market Challenges

- 5.2.1 Rising Cost With Product Advancement

6 MARKET SEGMENTATION

- 6.1 Technology

- 6.1.1 Coriolis

- 6.1.2 Electromagnetic

- 6.1.2.1 In-line Magnetic Flowmeters

- 6.1.2.2 Low Flow Magnetic Flowmeters

- 6.1.2.3 Insertion

- 6.1.3 Differential Pressure

- 6.1.4 Ultrasonic

- 6.1.4.1 Clamp-on

- 6.1.4.2 In-line

- 6.1.5 Other Technologies

- 6.2 End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Water and Wastewater

- 6.2.3 Chemical and Petrochemical

- 6.2.4 Food & Beverage

- 6.2.5 Pulp and Paper

- 6.2.6 Other End-user Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 Rest of Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Yokogawa Electric Corporation

- 7.1.2 ABB Ltd

- 7.1.3 Siemens AG

- 7.1.4 Bronkhorst High-Tech BV

- 7.1.5 Honeywell International Inc.

- 7.1.6 Emerson Electric Co.

- 7.1.7 SICK AG

- 7.1.8 OMEGA Engineering

- 7.1.9 Christian Burkert GmbH & Co. KG

- 7.1.10 TSI incorporated

- 7.1.11 Keyence Corporation

- 7.1.12 Sensirion AG

- 7.1.13 Azbil Corporation

- 7.1.14 Endress+Hauser AG

- 7.1.15 Krohne Messtechnik GmbH

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK

2024-2032 年按产品类型(类比流量计、智慧流量计)、应用(住宅、工业、商业)和地区分類的流量计市场报告

2024-2032 年按产品类型(类比流量计、智慧流量计)、应用(住宅、工业、商业)和地区分類的流量计市场报告 超音波管道流量计市场报告:2030 年趋势、预测和竞争分析

超音波管道流量计市场报告:2030 年趋势、预测和竞争分析 2024 年流量计全球市场报告

2024 年流量计全球市场报告 全球流量计市场规模、份额和趋势分析报告:2023-2030 年按应用、产品类型和地区分類的展望和预测

全球流量计市场规模、份额和趋势分析报告:2023-2030 年按应用、产品类型和地区分類的展望和预测 流量计市场:按类型、驱动类型、最终用途行业划分 - 2024-2030 年全球预测

流量计市场:按类型、驱动类型、最终用途行业划分 - 2024-2030 年全球预测 全球流量计市场 2023-2030

全球流量计市场 2023-2030 涡式流量计全球市场2024-2028

涡式流量计全球市场2024-2028 文丘里管市场:按产品类型、分销管道和最终用户产业:2023-2032 年全球机会分析和产业预测

文丘里管市场:按产品类型、分销管道和最终用户产业:2023-2032 年全球机会分析和产业预测 2024 年整合流量计和计数设备全球市场报告

2024 年整合流量计和计数设备全球市场报告 天然气流量计的全球市场: 2023年

天然气流量计的全球市场: 2023年