|

市场调查报告书

商品编码

1441581

汽车悬吊系统:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Automotive Suspension System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

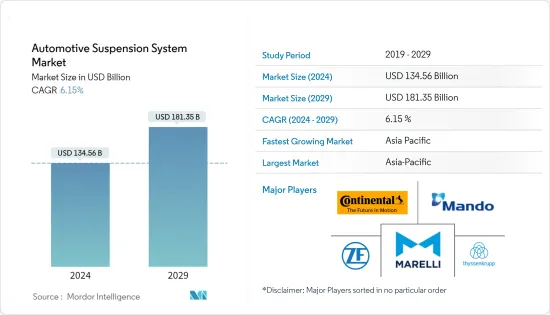

汽车悬吊系统市场规模预计到2024年为1345.6亿美元,预计到2029年将达到1813.5亿美元,在预测期内(2024-2029年)增长61.5亿美元,复合年增长率为%。

2022 年,全球汽车产量约 8,500 万辆。 2022年,中国小客车产量跃居世界第一,小客车产量约2,384万辆,商用车产量约319万辆,巩固全球第一大小客车生产国地位。

从中期来看,对豪华车的普及和主动悬吊系统的普及预计将在预测期内推动市场需求。车辆自主性的提高预计将推动感测器和电子悬吊系统市场的成长。汽车空气悬吊的发展是业界最重要的变革之一。

不断变化的汽车製造模式和不断提高的消费者期望要求汽车製造商将有效的性能元素融入他们的车辆中。OEM正在投资研发,将新技术整合到悬吊系统中,以提高操纵稳定性并提供更舒适的乘坐体验。这些发展将推动车辆悬吊市场的发展。例如,2023 年 4 月,EXT 开发了 Era 前叉开创性双正气室设计的现代改造,专为满足 Aria 应用的独特需求而量身定制。在此基础上,我们创造了一种减震器,它拥有显着增强的空气弹簧,将灵敏度和支撑力的极限推向了前所未有的水平,而以前只有螺旋弹簧减震器才能达到这一水平。

亚太地区和欧洲等地区预计将成为汽车悬吊系统市场成长最快的地区。在亚太地区,预计中国将在预测期内继续成为市场成长的驱动力。

汽车悬吊系统市场趋势

扩大商用车销售拉动市场需求

由于物流业的成长以及货车(用于叫车服务)等轻型商用车的使用增加,对商用车的需求不断增加。轻型商用车的主要驱动因素之一是,出于物流目的,人们越来越偏爱皮卡车和轻型货车,而不是重型卡车和铁路。物流需求的增加归因于全球电子商务产业的成长。随着电商市场的扩大,皮卡车、轻卡等轻型商用车的需求预计将增加。

2021年德国轻型商用车新车销售总计265,732辆,2022年销售312,400辆。 2021年法国新型轻型商用车销量总计431,385辆。 2022年,登记车辆为347,069辆。

政府和汽车製造商为采用商用电动车所做的努力预计将在研究期间推动汽车悬吊市场的发展。过去几年,电动商用车市场的主要汽车製造商纷纷制定电动出行策略,为全球悬吊市场的振兴做出了贡献。例如:

2022 年 5 月,蒂森克虏伯在巴西圣保罗开设了一个用于重型车辆悬吊产品全球开发的新技术中心,由该公司的弹簧和稳定器业务部门负责营运。蒂森克虏伯在圣保罗和伊比利特设有弹簧和稳定器工厂,为各种尺寸的车辆(包括小客车、巴士和卡车)生产弹簧和稳定器。

技术进步以及新车的推出和全球商用电动车的日益普及,预计将在预测期内推动汽车悬吊系统市场的成长。由于环境问题日益严重,电动商用车市场正处于成长阶段,预计在预测期内市场将大幅成长。

预计亚太地区在预测期内将实现最高成长

预计亚太地区汽车悬吊系统市场的收益在预测期内将显着增长。由于全部区域新车(包括小客车和商用车)销量的增加,该市场正在经历显着增长。例如,

2022年,中国小客车销量将超过2,300万辆,成为亚太地区最大的市场。印度是该地区第二大市场,2022 年销量约 380 万辆。

随着大公司在全部区域扩大生产设施,市场上可能会出现机会。例如,

2022 年 5 月,天纳克宣布 2022 年 Mercedes-AMG SL 级豪华跑车将配备 Monroe 智慧悬吊产品组合中的两项最新智慧悬吊技术。新车型将配备天纳克的CVSA2半主动悬吊或整合式CVSA2/Kinetic悬吊。

这些倡议预计将在未来几年提高汽车产量,进而提高全部区域对汽车悬吊系统的需求。

汽车悬吊系统产业概况

汽车悬吊系统市场适度整合,大陆集团、万都公司、采埃孚、马瑞利、蒂森克虏伯公司和万都公司等主要企业占据了主要市场占有率。产品创新和新市场的地理扩张对于汽车悬吊市场的任何参与者的成功都发挥着重要作用。

2022 年 1 月,采埃孚股份公司推出了商用车部门,名为商用车解决方案。这使得该公司成为汽车行业最大的商用车供应商。

2022年5月,捷豹路虎(JLR)宣布推出新款路虎卫士130。 Defender 130标配路虎智慧全轮驱动(iAWD)系统与八速ZF自动排檔变速箱。它配备了「自我调整电子空气悬吊」和路虎先进的地形反应系统。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 扩大全球汽车销售

- 市场限制因素

- 先进悬吊系统高成本

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌意强度

第五章市场区隔(金额、市场规模)

- 元件类型

- 螺旋弹簧

- 钢板弹簧

- 空气弹簧

- 避震器

- 其他组件类型

- 类型

- 被动悬吊

- 半主动悬吊

- 主动悬吊

- 车辆类型

- 小客车

- 商用车

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东和非洲

- 北美洲

第六章 竞争形势

- 供应商市场占有率

- 公司简介

- Continental AG

- Mando Corporation

- ZF Friedrichshafen AG

- Thyssenkrupp AG

- Tenneco Inc.

- Marelli Corporation

- Hyundai Mobis Co. Ltd

- Hitachi Astemo Ltd

- BWI Group

- Sogefi SpA

- KYB Corporation

- LORD Corporation

第七章市场机会与未来趋势

- 感测器和电子集成

The Automotive Suspension System Market size is estimated at USD 134.56 billion in 2024, and is expected to reach USD 181.35 billion by 2029, growing at a CAGR of 6.15% during the forecast period (2024-2029).

In 2022, some 85 million motor vehicles were produced worldwide. In 2022, China emerged as the global leader in passenger car production, manufacturing approximately 23.84 million such vehicles alongside 3.19 million commercial vehicles, solidifying its position as the foremost producer of passenger cars worldwide.

Over the medium term, demand for luxury cars and penetration of active suspension systems are expected to drive the market demand over the forecast period. The rise in vehicle autonomy is expected to drive the market growth for sensor- and electronic-based suspension systems. The development of air suspension in automobiles was one of the most significant changes in the industry.

The shifting paradigm of automobile manufacturing and rising consumer expectations will necessitate the incorporation of effective performance elements into vehicles by automakers. OEMs are investing in R&D to integrate novel technologies into suspension systems to improve steering stability and provide a comfortable ride. Such developments will drive the vehicle suspension market forward. For Instance, In April 2023, EXT developed an updated adaptation of the Era fork's pioneering dual-positive air chamber design, specifically tailored to meet the unique demands of the Aria application. Building upon this foundation, they have crafted a shock absorber that boasts a significantly enhanced air spring, pushing the boundaries of sensitivity and support to unprecedented levels previously attainable solely by coil-sprung shocks.

Regions like Asia-Pacific and Europe are forecasted to be the fastest-growing automotive suspension system market. In Asia-Pacific, China is expected to continue to be the driver of market growth during the forecast period.

Automotive Suspension Systems Market Trends

Growing Sales of Commercial Vehicles to Drive Demand in the Market

The demand for commercial vehicles is rising owing to the growing logistics industry and increasing usage of light commercial vehicles, such as vans (for ride-hailing services). One of the key driving factors for light commercial vehicles is the increased preference for pickup trucks and small vans over heavy-duty trucks and railways for logistics. The growing demand for logistics stems from the growing e-commerce industry globally. As the e-commerce market continues to expand, demand for pickup vans, small trucks, and other LCVs is also likely to increase.

The new vehicle sales of Light commercial vehicles in Germany stood at 265732 units in 2021 and 312400 units in 2022. The new vehicle sales of Light commercial vehicles in France stood at 431385 units in 2021. In 2022, the same was 347069 units registered.

The government and car manufacturers' initiatives to introduce commercial electric vehicles are expected to drive the automotive suspension market in the study period. In the past few years, the electric commercial vehicle market witnessed major automakers rolling out their strategies toward electric mobility, helping to boost the global suspension market. For instance:

In May 2022, Thyssenkrupp opened a new technology center for the global development of suspension products for heavy vehicles in Sao Paulo, Brazil, operated by its Springs & Stabilizers business unit. ThyssenKrupp has Springs & Stabilizers factories in Sao Paulo and Ibirite, which produce springs and stabilizer bars for vehicles of various sizes, such as cars, buses, and trucks.

Technological advancements, along with new vehicle launches and increasing adoption of commercial electric vehicles across the world, are expected to help the automotive suspension system market grow during the forecasted period. Due to the rising environmental concerns, the electric commercial vehicle market is in its growth phase, and the market is expected to rise exponentially during the forecast period.

Asia-Pacific is Anticipated to Register the Highest Growth During the Forecast Period

The Asia-Pacific automotive suspension system market is expected to grow at a significant rate in terms of revenue during the forecast period. The rise in new vehicle sales, including passenger cars and commercial vehicles across the region, is witnessing major growth in the market. For instance,

In 2022, over 23 million passenger cars were sold in China, making it the largest market in the Asia-Pacific region. India was the second biggest market in the region, with nearly 3.8 million unit sales in 2022.

Major companies expanding their production facilities across the region is likely to create an opportunity for the market. For instance,

In May 2022, Tenneco Inc. announced that the 2022 Mercedes-AMG SL-Class of luxury roadsters would feature two of the latest intelligent suspension technologies from its Monroe Intelligent Suspension portfolio. The new models will be offered with Tenneco's CVSA2 semi-active suspension or integrated CVSA2/Kinetic suspension.

Such initiatives are expected to drive automotive production in the upcoming years, which, in turn, would drive the demand for automotive suspension systems across the region.

Automotive Suspension Systems Industry Overview

The automotive suspension system market is moderately consolidated with leading players such as Continental AG, Mando Corporation, ZF, Magneti Marelli, Thyssenkrupp AG, Mando Corporation, etc., accounting for major market share. Product innovation and geographic expansion to new markets will play a major role in the success of any player in the automotive suspension market.

In January 2022, ZF Friedrichshafen AG launched a commercial vehicle division named Commercial Vehicle Solutions. This makes the company the largest commercial vehicle supplier in the automotive industry.

In May 2022, Jaguar Land Rover (JLR) announced the launch of the new Land Rover Defender 130. Defender 130 is fitted with Land Rover's Intelligent All-Wheel Drive (iAWD) system and eight-speed ZF automatic transmission as standard. It is fitted with 'Electronic Air Suspension with Adaptive Dynamics' and Land Rover's advanced Terrain Response system.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Automotive Sales Across the Globe

- 4.2 Market Restraints

- 4.2.1 High Cost of Advanced Suspension Systems

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value (USD))

- 5.1 Component Type

- 5.1.1 Coil Spring

- 5.1.2 Leaf Spring

- 5.1.3 Air Spring

- 5.1.4 Shock Absorber

- 5.1.5 Other Component Types

- 5.2 Type

- 5.2.1 Passive Suspension

- 5.2.2 Semi-active Suspension

- 5.2.3 Active Suspension

- 5.3 Vehicle Type

- 5.3.1 Passenger Car

- 5.3.2 Commercial Vehicle

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Continental AG

- 6.2.2 Mando Corporation

- 6.2.3 ZF Friedrichshafen AG

- 6.2.4 Thyssenkrupp AG

- 6.2.5 Tenneco Inc.

- 6.2.6 Marelli Corporation

- 6.2.7 Hyundai Mobis Co. Ltd

- 6.2.8 Hitachi Astemo Ltd

- 6.2.9 BWI Group

- 6.2.10 Sogefi SpA

- 6.2.11 KYB Corporation

- 6.2.12 LORD Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration of Sensors and Electronics

汽车悬吊市场,按产品类型、零件、几何形状、悬吊类型、车辆类型、国家和地区 - 2024-2032 年产业分析、市场规模、市场份额和预测

汽车悬吊市场,按产品类型、零件、几何形状、悬吊类型、车辆类型、国家和地区 - 2024-2032 年产业分析、市场规模、市场份额和预测 全球汽车悬吊市场:市场规模、份额、成长分析 - 按系统类型、悬吊类型、产业预测(2024-2031)

全球汽车悬吊市场:市场规模、份额、成长分析 - 按系统类型、悬吊类型、产业预测(2024-2031) 汽车悬吊系统的全球市场规模、份额和成长分析:按原材料和最终用户划分 - 产业预测(2024-2031)

汽车悬吊系统的全球市场规模、份额和成长分析:按原材料和最终用户划分 - 产业预测(2024-2031) 火车悬吊系统的全球市场:份额、规模、趋势、产业分析 - 按元件类型、悬吊类型、火车类型、地区、细分市场预测,2024-2032 年

火车悬吊系统的全球市场:份额、规模、趋势、产业分析 - 按元件类型、悬吊类型、火车类型、地区、细分市场预测,2024-2032 年 2024-2028年重型卡车悬吊系统全球市场

2024-2028年重型卡车悬吊系统全球市场 全球汽车悬吊系统市场 2023-2030

全球汽车悬吊系统市场 2023-2030 2024 年汽车悬吊系统全球市场报告

2024 年汽车悬吊系统全球市场报告 卡车悬吊系统市场:按类别、销售管道、类型:2023-2032 年全球机会分析和产业预测

卡车悬吊系统市场:按类别、销售管道、类型:2023-2032 年全球机会分析和产业预测 2024-2028年全球汽车悬架构件市场

2024-2028年全球汽车悬架构件市场 乘用车悬吊系统市场 - 全球产业规模、份额、趋势机会和预测,按车辆类型、零件类型、类型、地区、竞争细分,2018-2028 年

乘用车悬吊系统市场 - 全球产业规模、份额、趋势机会和预测,按车辆类型、零件类型、类型、地区、竞争细分,2018-2028 年