|

市场调查报告书

商品编码

1441677

建筑化学品:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

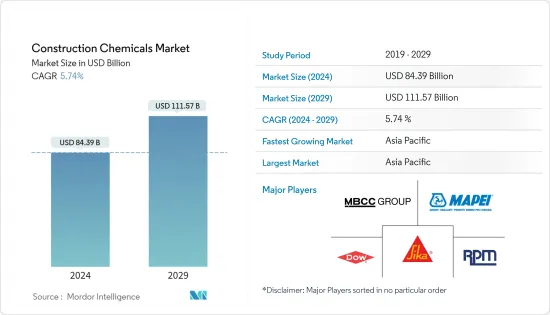

建筑化学品市场规模预计2024年为843.9亿美元,预计到2029年将达到1115.7亿美元,在预测期内(2024-2029年)增加57.4亿美元,复合年增长率为%。

主要亮点

- COVID-19的爆发对2020年的市场产生了负面影响。当 COVID-19 大流行开始时,世界各地的建筑工作都停止了,特别是在中国、美国、美国和欧洲国家等主要建筑中心。由于全球建筑业的成长,预计市场在预测期内将稳定成长。

- 短期来看,亚太地区(尤其是亚洲国家)建设活动的成长以及对水性产品需求的增强是推动研究市场成长的一些因素。

- 有关挥发性有机化合物排放的环境法规不断加强,仍是所研究市场成长的限制因素。

- 此外,美国对永续材料和即将开展的建设计划的日益关注可能会提供市场成长机会。

- 亚太地区主导市场,预计在整个预测期内将继续主导市场。

建筑化学品市场趋势

住宅领域的需求增加

- 精英阶层是奢华的代名词,精英住宅指的是豪华住宅。对具有世界一流设计和设施的封闭式社区的公寓、顶层公寓、别墅和平房的需求正在迅速增加,开发商正在推出计划来满足这种需求。

- 许多居民对在世界各地购买豪华住宅表现出极大的兴趣,以寻求舒适、声望和隐私。因此,这导致了全球精英住宅计划数量的增加。

- 由于中国和印度住宅建筑市场的扩张,亚太地区预计将录得最高成长率。亚太地区拥有最大的低成本住宅建筑市场,以中国、印度和东南亚各国为首。

- 不断增长的经济实力和高所得群体的大量投资预计将增加美国、加拿大、德国、英国、印度和日本等地区对豪华住宅的需求。因此,这可能有利于建筑化学品市场。

- 2021 年 10 月,圣保罗州住宅协会 (Secovi-SP) 记录圣保罗住宅销售量为 5,555 套。由于消费者在住宅方面的支出,这一数字可能会进一步增加。此外,巴西单户住宅的成长趋势预计将在未来支持住宅建设产业。

- 因此,基于上述因素,住宅领域预计将在预测期内主导市场。

亚太地区主导市场

- 亚太地区的建筑业是世界上最大的,并且由于人口增长、中阶收入增加和都市化稳步增长。

- 基础设施建设活动的增加以及欧盟主要公司进入盈利的中国市场进一步加速了该行业的扩张。

- 另外,中国在过去的50年里经历了多次维修,建造了许多建筑物,目前都面临严重的损坏,因此现有旧建筑的维修计划非常重要,不仅在都市区和乡村都很受欢迎。 。显示建筑化学品的主要标记区域。

- 台湾建设公司闪亮建筑商业有限公司计划于 2022 年 2 月在台湾和中国推出价值 300 亿新台币(10.8 亿美元)的新住宅计划。该计画包括台湾价值108亿新台币的计划和中国成都价值1900万新台币的项目。

- 此外,印度政府正在积极推动住宅建设,目标是为约13亿人提供住宅。未来七年,该国的住宅投资可能约为 1.3 兆美元。预计该国将新建6,000万套住宅。

- 新石化设施的开发刺激了私营部门的需求,而榜鹅数位区的工业和建筑计划则促进了新加坡公共部门的需求。基础设施产业预计也将经历相对健康的成长,主要受到改善公路、铁路和其他大众交通工具基础设施以及能源和公共建设计划投资的推动。政府计划在 2022 年投资 280 亿新元(209 亿美元)来扩大和改善交通系统。

- 因此,所有这些市场趋势预计将在预测期内推动该地区建筑化学品的需求。

建筑化学品产业概况

建筑化学品市场本质上是分散的。市场主要企业包括西卡股份公司、MBCC集团、RPM国际公司、MAPEI SpA、陶氏化学等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 亚太地区住宅和商业建设活动呈上升趋势

- 水性产品需求增加

- 抑制因素

- VOC排放法规和熟练劳动力短缺

- 由于 COVID-19 的影响,情况不利

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章市场区隔(收益,百万美元)

- 产品类别

- 混凝土外加剂

- 表面处理

- 维修/维修

- 保护涂层

- 工业地板材料

- 防水的

- 黏剂/密封剂

- 水泥浆锚

- 水泥助磨剂

- 最终用户产业

- 商业的

- 工业

- 基础设施/公共场所

- 住宅

- 地区

- 亚太地区

- 北美洲

- 欧洲

- 南美洲

- 中东

- 非洲

第六章 竞争形势

- 併购、合资、合作与协议

- 市场占有率分析

- 主要企业采取的策略

- 公司简介(公司简介、财务状况、产品/服务、近期状况)

- 3M

- Arkema Group

- Ashland

- MBCC Group(BASF SE)

- Bolton Group

- Cementaid International Ltd

- CHRYSO GROUP

- CICO Group

- Conmix Ltd

- Dow

- Fosroc Inc.

- Franklin International

- GCP Applied Technologies Inc.

- Henkel AG &Co. KGaA

- LafargeHolcim

- MAPEI SpA

- MUHU(China)Construction Materials Co. Ltd

- Nouryon

- Pidilite Industries Ltd

- RPM International Inc.

- Selena Group

- Sika AG

- Thermax Limited

第七章市场机会与未来趋势

简介目录

Product Code: 47467

The Construction Chemicals Market size is estimated at USD 84.39 billion in 2024, and is expected to reach USD 111.57 billion by 2029, growing at a CAGR of 5.74% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 outbreak negatively impacted the market in 2020. With the COVID-19 pandemic's beginning, construction work stopped worldwide, especially in major construction hubs, like China, India, the United States, and European nations. The market is projected to grow steadily in the forecast period owing to global growth in the construction sector.

- Over the short term, growing construction activities in the Asia-Pacific region, especially in Asian countries, and strengthening demand for water-based products are some of the factors driving the growth of the market studied.

- Increasing environmental regulations regarding VOC emissions remains a constraint for the growth of the market studied.

- Moreover, increasing focus on sustainable materials and upcoming construction projects in the United States will likely provide market growth opportunities.

- Asia-Pacific has dominated the market and is expected to continue dominating it through the forecast period.

Construction Chemicals Market Trends

Increasing Demand from Residential segment

- Elite class is synonymous with luxury, and elite housing refers to luxurious residences. The demand for apartments, penthouses, villas, and bungalows in gated communities with world-class designs and amenities is increasing rapidly, and developers are launching projects to cater to such demands.

- Many residents have been showing huge interest in buying luxury homes globally for comfort, prestige, and privacy. Therefore, this has been increasing the number of elite housing projects worldwide.

- The highest growth rate in this regard was expected to be registered in the Asia-Pacific region, owing to China's and India's expanding housing construction market. Asia-Pacific has the largest low-cost housing construction segment, which China, India, and various Southeast Asian countries lead.

- The growing economic strength and high investments by the high-income category are expected to increase the demand for luxury homes in geographies of the United States, Canada, Germany, the United Kingdom, India, and Japan. Thus, it is likely to benefit the construction chemicals market.

- In October 2021, Sao Paulo State Housing Union (Secovi-SP) recorded 5,555 new residential units sold in Sao Paulo. The number is more likely to rise owing to consumer spending on residential housing units. Moreover, the growing trend for single-family housing in Brazil is expected to support the residential construction industry in the upcoming period.

- Therefore, based on the abovementioned factors, the residential segment is expected to dominate the market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific construction sector is the largest in the world and is growing at a healthy rate, owing to the rising population, increase in middle-class incomes, and urbanization.

- Increasing infrastructure construction activities and the entry of major players from the European Union into the lucrative market of China have further fueled the industry's expansion.

- In addition, many renovations have been taking place in China over the past 50 years, many buildings have been built, and they are facing severe damage now, and hence renovation of existing old building projects is very popular in the city and countryside as well as depicting a major marker area for construction chemicals.

- In February 2022, Shining Building Business Co., a building construction company in Taiwan, planned to launch new housing projects worth NTD 30 billion (USD 1.08 billion) in Taiwan and China. The plan included projects valued at NTD 10.8 billion in Taiwan and NTD 19 million in Chengdu, China.

- Moreover, the Indian Government has been actively boosting housing construction, aiming to provide homes to about 1.3 billion people. The country will likely witness around USD 1.3 trillion of investment in housing over the next seven years. It is also expected to see the construction of 60 million new homes in the country.

- New petrochemical facilities development boosted the private sector demand, while industrial and building projects in the Punggol Digital District contributed to the public sector demand in Singapore. The infrastructure sector is also expected to post relatively healthy growth, mainly driven by the efforts to upgrade the country's road, rail, and other public transport infrastructure and investment in energy and utilities construction projects. The Government had been planning to invest SGD 28 billion (USD 20.9 billion) in the expansion and upgrading of the transport system by 2022.

- Hence, all such market trends are expected to drive the demand for construction chemicals in the region during the forecast period.

Construction Chemicals Industry Overview

The construction chemicals market is fragmented in nature. Some of the major players in the market include Sika AG, MBCC Group, RPM International Inc., MAPEI SpA, and Dow, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Residential and Commercial Construction Activities in the Asia-Pacific Region

- 4.1.2 Strengthening Demand for Water-based Products

- 4.2 Restraints

- 4.2.1 Regulations for VOC Emissions and Inadequacy of Skilled Labor

- 4.2.2 Unfavorable Conditions Arising Due to the COVID-19 Impact

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Revenue in USD Million)

- 5.1 Product Type

- 5.1.1 Concrete Admixture

- 5.1.2 Surface Treatment

- 5.1.3 Repair and Rehabilitation

- 5.1.4 Protective Coatings

- 5.1.5 Industrial Flooring

- 5.1.6 Waterproofing

- 5.1.7 Adhesive and Sealants

- 5.1.8 Grout and Anchor

- 5.1.9 Cement Grinding Aids

- 5.2 End-user Industry

- 5.2.1 Commercial

- 5.2.1.1 Office Space

- 5.2.1.2 Retails

- 5.2.1.3 Education Institutes

- 5.2.1.4 Hospitals

- 5.2.1.5 Hotels

- 5.2.1.6 Other Commercials

- 5.2.2 Industrial

- 5.2.2.1 Cement

- 5.2.2.2 Iron and Steel

- 5.2.2.3 Capital Goods

- 5.2.2.4 Automobile

- 5.2.2.5 Pharmaceutical

- 5.2.2.6 Paper

- 5.2.2.7 Petrochemical (Including Fertilizers)

- 5.2.2.8 Food and Beverage

- 5.2.2.9 Other Industrials

- 5.2.3 Infrastructure and Public Places

- 5.2.3.1 Roads and Bridges

- 5.2.3.2 Railways

- 5.2.3.3 Metros

- 5.2.3.4 Airports

- 5.2.3.5 Water

- 5.2.3.6 Energy

- 5.2.3.7 Government Buildings

- 5.2.3.8 Statues and Monuments

- 5.2.4 Residential

- 5.2.4.1 Elite Housing

- 5.2.4.2 Middle-class Housing

- 5.2.4.3 Low-cost Housing

- 5.2.1 Commercial

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China (Including Taiwan)

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 Indonesia

- 5.3.1.5 Australia and New Zealand

- 5.3.1.6 South Korea

- 5.3.1.7 Thailand

- 5.3.1.8 Malaysia

- 5.3.1.9 Philippines

- 5.3.1.10 Bangladesh

- 5.3.1.11 Vietnam

- 5.3.1.12 Singapore

- 5.3.1.13 Sri Lanka

- 5.3.1.14 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Benelux

- 5.3.3.7 Turkey

- 5.3.3.8 Switzerland

- 5.3.3.9 Scandinavian Countries

- 5.3.3.10 Poland

- 5.3.3.11 Portugal

- 5.3.3.12 Spain

- 5.3.3.13 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Chile

- 5.3.4.5 Rest of South America

- 5.3.5 Middle-East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Kuwait

- 5.3.5.5 Egypt

- 5.3.5.6 Rest of Middle-East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Nigeria

- 5.3.6.3 Algeria

- 5.3.6.4 Morocco

- 5.3.6.5 Rest of Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Ashland

- 6.4.4 MBCC Group (BASF SE)

- 6.4.5 Bolton Group

- 6.4.6 Cementaid International Ltd

- 6.4.7 CHRYSO GROUP

- 6.4.8 CICO Group

- 6.4.9 Conmix Ltd

- 6.4.10 Dow

- 6.4.11 Fosroc Inc.

- 6.4.12 Franklin International

- 6.4.13 GCP Applied Technologies Inc.

- 6.4.14 Henkel AG & Co. KGaA

- 6.4.15 LafargeHolcim

- 6.4.16 MAPEI S.p.A

- 6.4.17 MUHU (China) Construction Materials Co. Ltd

- 6.4.18 Nouryon

- 6.4.19 Pidilite Industries Ltd

- 6.4.20 RPM International Inc.

- 6.4.21 Selena Group

- 6.4.22 Sika AG

- 6.4.23 Thermax Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Upcoming Construction Projects in the United States

- 7.2 Increasing Focus on Sustainable Materials

02-2729-4219

+886-2-2729-4219

全球建筑化学品市场规模:按类型、应用、地区、范围和预测

全球建筑化学品市场规模:按类型、应用、地区、范围和预测 建筑化学品市场:按类型、应用分类 - 2025-2030 年全球预测

建筑化学品市场:按类型、应用分类 - 2025-2030 年全球预测 建筑化学品市场规模、份额、趋势分析报告:按产品、按应用、按地区、细分市场预测,2024-2030

建筑化学品市场规模、份额、趋势分析报告:按产品、按应用、按地区、细分市场预测,2024-2030 建筑化学品市场报告:2030 年趋势、预测与竞争分析

建筑化学品市场报告:2030 年趋势、预测与竞争分析 2024-2032 年建筑化学品市场报告(按类型(混凝土外加剂、防水和屋顶、修补、地板、密封剂和黏合剂等)、应用(住宅、非住宅)和地区)

2024-2032 年建筑化学品市场报告(按类型(混凝土外加剂、防水和屋顶、修补、地板、密封剂和黏合剂等)、应用(住宅、非住宅)和地区) 全球混凝土裂缝填充剂市场规模、份额、成长分析,按类型(塑性收缩混凝土裂缝填充剂和硬化混凝土裂缝填充剂),按应用(公路、桥樑)-行业预测 2024-2031

全球混凝土裂缝填充剂市场规模、份额、成长分析,按类型(塑性收缩混凝土裂缝填充剂和硬化混凝土裂缝填充剂),按应用(公路、桥樑)-行业预测 2024-2031 2024 年建筑化学品全球市场报告

2024 年建筑化学品全球市场报告 2024-2028年全球建筑化学品市场

2024-2028年全球建筑化学品市场 建筑化学品市场,按产品类型、按应用、最终用户、国家和地区 - 2023-2030 年行业分析、市场规模、市场份额和预测

建筑化学品市场,按产品类型、按应用、最终用户、国家和地区 - 2023-2030 年行业分析、市场规模、市场份额和预测 全球建筑化学品市场:按材料、产品类型、最终用户和地区划分的评估、机会和预测(2016-2030)

全球建筑化学品市场:按材料、产品类型、最终用户和地区划分的评估、机会和预测(2016-2030)

▼