|

市场调查报告书

商品编码

1443912

工业淀粉:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Industrial Starches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

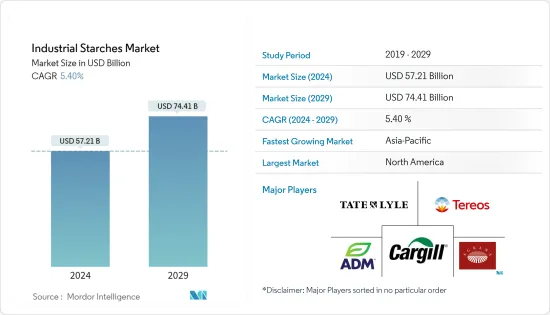

工业淀粉市场规模预计到 2024 年为 572.1 亿美元,预计到 2029 年将达到 744.1 亿美元,预测期内(2024-2029 年)复合年增长率为 5.40%

淀粉是从农业原料中提取的碳水化合物,具有许多日常食品和非食品应用。工业淀粉的来源多种多样,包括玉米、马铃薯、小麦和其他来源。随着全球经济逐渐改善以及加工食品和即食食品食品的消费增加,大量用于这些食品应用的工业淀粉市场的需求增加并带动整体市场。

在食品工业快速发展的同时,变性淀粉的需求也不断增加。改质淀粉为各种食品提供许多功能性益处,例如烘焙产品、点心、饮料和营养食品。目前,市面上有各种各样的淀粉,并且正在研究天然淀粉、改性淀粉、麦芽糊精、淀粉基糖等形式。这些淀粉正在推动市场的扩大应用,主要是在饮料和糖果零食行业、製药和发酵行业。

工业淀粉市场趋势

玉米作为工业淀粉的主要来源之一

由于其质地特性,玉米淀粉作为增稠剂的需求量很大,尤其是在乳製品和饮料等行业。这种成分也为无麸质产品的开发提供了优势,这对小麦淀粉来说是一个挑战,因为在萃取过程中可能会留下痕迹。洁净标示成分和产品趋势正在对全球食品和饮料产业产生重大影响。此外,食品加工业的快速扩张为原料製造商采取策略措施以满足不断增长的需求提供了重大机会。对于非食品应用,玉米粉在造纸工业中用作填充物和施胶剂。它也应用于纺织、洗衣、铸造、气浮和黏剂行业。玉米粉在各行业的广泛应用正在推动市场的成长。

北美在工业淀粉市场中占有很大份额

由于利用所有原料的食品工业高度发达,北美在工业淀粉市场按地区占据领先地位。在全球范围内,美国是最大的玉米生产国,2021-2022年产量为3.8394亿吨,用于多种用途,包括淀粉生产。由于对无麸质成分的产品标籤有严格的规定,市场严重倾向于无麸质食品的消费。因此,美国的大多数加工食品淀粉都不含无麸质,并且源自玉米、糯玉米和马铃薯。因此,小麦淀粉的市占率较低。由于消费者对健康和清洁成分的需求不断增加,加拿大的工业淀粉市场正在快速成长。具有微妙风味的浅色应用尤其推动了对国内天然淀粉的需求。当地製造商将其用于加工食品,有助于保持其产品的吸引力。

工业淀粉产业概况

工业淀粉市场高度分散,许多国家、地区和国际参与者争夺市场占有率。该市场的主要企业包括阿彻丹尼尔斯米德兰公司、嘉吉公司、泰特莱尔公司和特雷奥斯集团。公司采取扩张、新产品发布和创新等关键策略来加强营运。与当地公司达成新协议和合作伙伴关係的策略使公司能够扩大海外足迹,根据行业需求的偏好发布新产品,并利用这些地区小公司的专业知识。我能够做到。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 市场限制因素

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 按类型

- 本国的

- 淀粉衍生物和甜味剂

- 按来源

- 玉米

- 小麦

- 木薯

- 马铃薯

- 其他来源

- 按用途

- 食物

- 餵食

- 造纸工业

- 製药业

- 其他用途

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 西班牙

- 英国

- 德国

- 俄罗斯

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲

- 北美洲

第六章 竞争形势

- 最采用的策略

- 市场占有率分析

- 公司简介

- Cargill Incorporated

- Archer Daniels Midland Company

- Ingredion Incorporated

- Tate &Lyle PLC

- Agrana Beteiligungs AG

- Kent Nutrition Group Inc.(Grain Processing Corp.)

- The Tereos Group

- Cooperatie Koninklijke Cosun UA

- Altia PLC

- Angel Starch and Food Pvt. Ltd

- Manildra Group

- Japan Corn Starch Co. Ltd

第七章市场机会与未来趋势

第八章 免责声明

The Industrial Starches Market size is estimated at USD 57.21 billion in 2024, and is expected to reach USD 74.41 billion by 2029, growing at a CAGR of 5.40% during the forecast period (2024-2029).

Starch is a carbohydrate extracted from agricultural raw materials, which finds applications in many everyday food and non-food products. Industrial starches are derived from various sources, including corn, potato, wheat, and other sources. With the global economy gradually improving and resulting in an increased intake of processed and convenience foods, the market for industrial starch, which finds substantial usage in these food applications, is finding increased demand, thereby driving the overall market.

The demand for modified starches is increasing in parallel with the rapid development of the food industry. Modified starches offer many functional benefits to various foods, such as bakeries, snacks, beverages, and nutritional foods. Currently, a wide range of starches are available in the market, studied in the form of native starches, modified starches, malt dextrin, starch-based sugars, and others. These starches have expanding applications, primarily in the beverage and confectionery industries and the pharmaceutical and fermentation industries, among others, driving the market.

Industrial Starch Market Trends

Corn as one of the Prominent Source of Industrial Starch

Starch derived from corn is in high demand because of its textural properties, especially as a thickening agent in industries such as dairy and beverages. The ingredient also gains an edge in the development of gluten-free products, which is a challenge for starch sourced from wheat, considering the potential remains of traces during extraction. The trend of clean-label ingredients and products is drastically impacting the global food and beverage industry. Moreover, the rapid expansion of the food processing industry offers a significant opportunity for ingredient manufacturers to adopt strategic measures to cater to the growing demand. When it comes to non-food applications, the paper industry utilizes corn starch as a filler and sizing material. It also finds applications in the textile, laundry, foundry, air flotation, and adhesive industries. The wide applications of corn starch in various industries drive market growth.

North America Holds a Major Share in the Industrial Starches Market

With a highly developed food industry utilizing all ingredients, North America occupies the pole position in the Industrial Starches Market by region. Globally, the United States is the largest producer of corn, with a production of 383.94 million metric tons in 2021-2022, which is utilized in various application areas, including starch production. The market is significantly inclined toward the consumption of gluten-free food, supported by the country's government with its stringent regulations regarding product labeling of gluten-free ingredients. Thus, most modified food starches in the United States are gluten-free and derived from corn, waxy maize, and potatoes. Consequently, the wheat-sourced starches amount to a lower share of the market. The Canadian industrial starches market is growing rapidly, owing to rising consumer demand for healthy and cleaner ingredients. Light-colored applications with subtle flavors especially drive the demand for native starches in the country. Local manufacturers are using it in processed food products, aiding in maintaining the product's appeal.

Industrial Starch Industry Overview

The industrial starch market is highly fragmented, with many local, regional, and international players competing for market share. Some of the major players in the market are Archer Daniels Midland Company, Cargill Incorporated, Tate & Lyle PLC, and The Tereos Group. Companies adopt major strategies for expansion, new product launches, and innovations to strengthen their business. The strategy of forming new agreements and partnerships with local players helped the companies increase their footprint in foreign countries and release new products according to the industrial requirements preferences and leverage the expertise of these small regional companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Native

- 5.1.2 Starch Derivatives & Sweeteners

- 5.2 By Source

- 5.2.1 Corn

- 5.2.2 Wheat

- 5.2.3 Cassava

- 5.2.4 Potato

- 5.2.5 Other Sources

- 5.3 By Application

- 5.3.1 Food

- 5.3.2 Feed

- 5.3.3 Paper Industry

- 5.3.4 Pharmaceutical Industry

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Spain

- 5.4.2.2 United Kingdom

- 5.4.2.3 Germany

- 5.4.2.4 Russia

- 5.4.2.5 France

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Cargill Incorporated

- 6.3.2 Archer Daniels Midland Company

- 6.3.3 Ingredion Incorporated

- 6.3.4 Tate & Lyle PLC

- 6.3.5 Agrana Beteiligungs AG

- 6.3.6 Kent Nutrition Group Inc. (Grain Processing Corp.)

- 6.3.7 The Tereos Group

- 6.3.8 Cooperatie Koninklijke Cosun UA

- 6.3.9 Altia PLC

- 6.3.10 Angel Starch and Food Pvt. Ltd

- 6.3.11 Manildra Group

- 6.3.12 Japan Corn Starch Co. Ltd