|

市场调查报告书

商品编码

1444020

纤维水泥 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Fiber Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

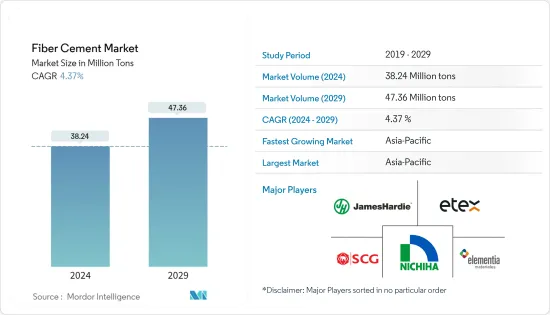

纤维水泥市场规模预计到2024年为3824万吨,预计到2029年将达到4736万吨,在预测期内(2024-2029年)CAGR为4.37%。

由于政府的禁令和限制,2020年和2021年上半年Covid-19大流行的零星爆发极大地限制了全球建筑业,从而限制了纤维水泥市场的成长。住宅房地产受到的打击最严重,因为主要城市的严格封锁措施导致房屋登记暂停和房屋贷款支付缓慢。然而,自限制解除以来,该行业一直在良好復苏。过去两年,房屋销售的增加、新项目的推出以及对新办公室和商业空间的需求不断增加一直引领着市场復苏。

主要亮点

- 从中期来看,全球不断增长的住宅建设是促进所研究市场成长的主要驱动因素。此外,纤维水泥具有众多优势,例如使用寿命长、是普通水泥的可持续替代品、强度高且与油漆相容性高,这些都促使建筑材料製造商越来越精确地使用纤维水泥他们所承担的项目中的产品。

- 另一方面,木材、金属和乙烯基等替代产品的供应是预计在预测期内抑制目标产业成长的关键因素。

- 儘管如此,纤维水泥在欧洲木框架领域的渗透率不断提高,以及印度纤维水泥日益取代低端胶合板领域等因素可能很快就会为全球市场创造利润丰厚的成长机会。

- 预计亚太地区将在预测期内主导市场。这一增长归因于该地区住宅和商业领域的充分发展,更加重视低收入人群的住房建设,从而导致外部和内部住宅应用对纤维水泥的需求旺盛。

纤维水泥市场趋势

住宅最终用户产业的需求不断成长

- 住宅产业是纤维水泥的主要最终用户产业,纤维水泥用于住宅建筑中的内部覆层,包括隔间墙、窗台、天花板和地板以及瓷砖背板。

- 纤维水泥产品因其具有混凝土耐磨、抗紫外线、防火、防虫防藻、耐腐蚀、美观等多种优点,在住宅产业中广泛使用。此外,纤维水泥产品安装简单、维护成本低、耐用且具有成本效益,并且具有低噪音渗透和低热效应,使其成为世界各地经济适用房的首选材料。

- 中产阶级住房的建筑概念随着虚拟实境、扩增实境、机器学习等新兴建筑技术的发展而不断发展。由于这些技术的进步,人们能够以最佳成本建造房屋并享受舒适感。公寓、平房和别墅等住宅物业在新兴国家越来越受欢迎,这主要是由城市化推动的。

- 北美、亚太和欧洲等地区的住宅建设近年来稳定成长。在亚太地区,印度、中国、印尼、新加坡和越南等国家的住宅建设正在增加。然而,在住宅需求旺盛的推动下,北美和欧洲的住宅建设正在成长。

- 预计中国的人口结构将有利于住房建设活动。人口的成长引发了公共和私营部门对经济适用住宅区的投资。根据中国国家统计局的数据,中国房屋开工量从 2022 年 7 月的 76,066.76 万平方公尺跃升至 8 月的 8,5,062 万平方公尺。

- 美国正在大规模进行新房屋建设和房屋翻新。根据美国人口普查局和美国住房和城市发展部发布的统计数据,2022年8月住房竣工量经季节调整后的年增长率为1,342,000套。该价值较 2021 年 8 月的 1,302,000 套增长了 3.1%。单户住宅竣工率增长了 0.4%,2022 年 8 月为 1,017,000 套,而 2022 年 7 月为 1,013,000 套。

- 德国拥有欧洲最大的建筑业。德国联邦统计局报告称,2021 年该国住宅存量达到 4,310 万套,比上一年增长 0.7%(即 28 万套住宅),比 2011 年住宅总数增长 6.0%。2021年,德国住宅建筑业获得的建筑许可数量连续第三次增长,达到12.9万套。

- 为了满足沙乌地阿拉伯的住房需求,政府于2022年9月宣布,打算根据其2030年愿景计划,投资1.1兆美元建造555,000套住宅单元。

- 考虑到上述所有事实和因素,住宅建筑应用中纤维水泥的使用和需求预计在预测期内将会成长。

亚太地区将主导市场

- 亚太地区以庞大的市场份额主导全球市场,预计在预测期内将保持其主导地位。亚太国家各类建筑活动对纤维水泥的大量消耗是推动目标产业成长的主要因素。

- 亚太地区的建筑业是世界上最大的,并且由于人口增长、中产阶级收入增加和城市化而以健康的速度增长。

- 中国的主要推动力是在经济成长的支持下,住宅和商业建筑领域的充分发展。在内地,香港房管局推出多项措施推动廉租房建设。官员的目标是到 2030 年提供 301,000 套公共住宅。

- 此外,未来七年,印度可能会在住房方面投资约1.3兆美元,其中可能会建造6,000万套新房屋。预计到 2024 年,该国经济适用房的供应率将增加 70% 左右。印度政府的「到 2022 年为所有人提供住房」也是该行业的重大游戏规则改变者。该倡议旨在到2022年底为城市贫困人口建设超过2000万套保障性住房,将大大促进住房建设。预计这将为未来几年该国纤维水泥市场的成长提供各种机会。

- 此外,智慧城市任务是印度政府承担的另一个重大项目,将在全国建造100多个智慧城市,以实现印度快速城市化。该国的工商业基础设施已成为高成长产业之一。印度政府一直在製定倡议,例如放宽建筑业吸引外国直接投资流入的规则,以加快全国的发展。

- 日本正在兴建许多豪华公寓和住宅区。例如,三菱州立大学正在建造日本最高的建筑,该建筑将包括 50 套豪华公寓,每个公寓每月可产生 43,000 美元的租金。该项目正在东京车站附近建设,预计将于 2027 年竣工。

- 泰国是最大的游客中心之一,在购物中心、豪华酒店等的扩建和建设上投入巨资。芭堤雅万豪侯爵酒店是泰国在建项目中最大的项目,预计将于 2024 年投入运营, 900多间客房。新的马奎斯万豪酒店将成为双酒店开发项目的一部分,其中还包括拥有 398 间客房的 JW 万豪酒店和芭堤雅海滩水疗度假村。到 2027 年,万豪可能会在泰国曼谷和芭堤雅新增 4 家旗下三个品牌的酒店。万豪在泰国的投资组合包括 45 家酒店和度假村,其中包括 Asset World Corporation 旗下的 9 家酒店。

- 所有上述因素都可能在预测时间内推动亚太纤维水泥市场的成长。

纤维水泥产业概况

全球纤维水泥市场本质上是部分分散的,没有参与者占据所研究市场的重要份额。一些主要公司包括 James Hardie Building Products Inc.、Etex Group、NICHIHA、SCG 和 Elementia Materiales。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 司机

- 全球住宅建设不断成长

- 纤维水泥的优点

- 限制

- 替代方案的存在

- 其他限制

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第 5 章:市场区隔(市场规模按数量计算)

- 应用

- 壁板

- 屋顶

- 包层

- 成型与修整

- 其他应用

- 最终用户产业

- 住宅

- 非住宅

- 地理

- 亚太

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太

第 6 章:竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 领先企业采取的策略

- 公司简介

- American Fiber Cement Corporation

- Cembrit Holding A/S (Swisspearl Group AG)

- CenturyPly

- CSR Limited

- Elementia Materials

- Etex Group

- Everest Industries Limited

- James Hardie Industries PLC

- NICHIHA Co. Ltd

- Saint-Gobain

- SCG

- Toray Industries Inc.

- TPI Polene Public Company Limited

第 7 章:市场机会与未来趋势

The Fiber Cement Market size is estimated at 38.24 Million tons in 2024, and is expected to reach 47.36 Million tons by 2029, growing at a CAGR of 4.37% during the forecast period (2024-2029).

The sporadic outbreak of the COVID-19 pandemic in 2020 and the first half of 2021 drastically curtailed the global construction sector due to imposed government bans and restrictions, thereby limiting the growth of the fiber cement market. Residential real estate was the worst hit as strict lockdown measures across major cities resulted in the suspension of home registrations and slow home loan disbursements. However, the sector has been recovering well since restrictions were lifted. An increase in house sales, new project launches, and increasing demand for new offices and commercial spaces have been leading the market recovery over the last two years.

Key Highlights

- Over the medium term, the rising residential construction across the world is the major driving factor augmenting the growth of the market studied. Furthermore, a plethora of advantages offered by fiber cement, such as exhibiting long service life, representing a sustainable alternative to regular cement, and demonstrating high strength and compatibility to paints, are propelling the construction materials manufacturers to increasingly become more precise in including fiber cement products in the projects they have undertaken.

- On the flip side, the availability of alternative products such as wood, metals, and vinyl is the key factor anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, factors like the increasing penetration of fiber cement in the timber frame segment in Europe and the growing replacement of the low-end plywood segment with fiber cement in India are likely to create lucrative growth opportunities for the global market soon.

- The Asia-Pacific is expected to dominate the market during the forecast period. This growth is attributed to the ample developments in the region's residential and commercial sectors with a higher focus on housing construction for the low-income population which leads to bullish demand for fiber cement in external and internal residential applications.

Fiber Cement Market Trends

Increasing Demand from the Residential End-user Industry

- The residential industry is the major end-user industry for fiber cement which is used for internal claddings, including partition walls, windowsills, ceilings and floors, and tile backer boards in residential construction.

- The widespread use of fiber cement products in the residential industry is due to the various advantages, such as wear and tear resistance to concrete, UV resistance, fire resistance, pest and algae resistance, corrosion-free, aesthetically appealing, and others. In addition, fiber cement products are simple to install, low-maintenance, durable, and cost-effective, as well as offer low noise penetration, and low heating effects which make them the preferred material in affordable housing around the world.

- Architecture ideas for middle-class housing are evolving, along with emerging technologies in construction, like virtual reality, augmented reality, machine learning, etc. Due to such technological advancements, people are able to construct houses at optimal costs and enjoy comfort. Residential properties such as apartments, bungalows, and villas are gaining popularity in emerging nations and are mainly driven by urbanization.

- Residential construction in regions, such as North America, Asia-Pacific, and Europe, has been witnessing steady growth in recent times. In Asia-Pacific, residential construction is increasing in countries, including India, China, Indonesia, Singapore, and Vietnam, among others. Whereas, North America and Europe are witnessing growth in residential construction, widely driven by a high demand for residential houses.

- China's demographics are expected to favor housing construction activities. The growing population has triggered investments in affordable residential colonies by both the public and private sectors. As per the National Bureau of Statistics of China, housing starts in China jumped to 85062 Ten Thousand Square meters in August from 76066.76 Ten Thousand Square meters in July of 2022.

- The United States is going massive in new home construction and home refurbishment. As per the statistics released by the U.S. Census Bureau and the U.S. Department of Housing and Urban Development, an increase in housing completions in August 2022 was recorded at a seasonally adjusted annual rate of 1,342,000. The value showed an increase of 3.1% from 1,302,000, the value obtained in August 2021. The single-family housing completions registered a 0.4% increase in rate which stood at 1,017,000 in August 2022 while the July 2022 rate was 1,013,000.

- Germany has the largest construction sector in Europe. The German Federal Statistical Office reports the stock of dwellings reaching 43.1 million in 2021 in the country, showing an increase of 0.7% (i.e., 280,000 dwellings) from the previous year and 6.0% in comparison to the total dwellings in 2011. The total number of building permits achieved by Germany's residential construction sector rose consecutively for the third time in 2021, reaching 129 thousand units.

- To meet the housing needs of Saudi Arabia, the government, in September 2022, announced its intention to build 555,000 residential units with an investment of USD 1.1 trillion under its Vision 2030 program.

- Considering all the above facts and factors, the usage and demand of fiber cement for residential construction applications are expected to grow in the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominated the worldwide market with a significant market share and is projected to maintain its dominance during the forecast period. The significantly large consumption of fiber cement across all types of construction activities in Asia-Pacific countries is the primary factor driving the growth of the target industry.

- The construction sector in the Asia-Pacific region is the largest in the world and is increasing at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization.

- China is majorly driven by ample developments in the residential and commercial construction sectors, supported by the growing economy. In China, the housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units by 2030.

- Furthermore, India is likely to witness an investment of around USD 1.3 trillion in housing, over the next seven years, during which, it is likely to witness the construction of 60 million new homes. The rate of availability of affordable housing is expected to rise by around 70%, in 2024 in the country. The Indian government's 'Housing for All by 2022' is also a major game-changer for the industry. This initiative aims to build more than 20 million affordable homes for the urban poor by the end of 2022. This will provide a significant boost to housing construction. This is expected to provide various opportunities for the growth of the fiber cement market in the country in the coming years.

- Furthermore, the smart cities mission is another major project undertaken by the government of India, which will construct more than 100 smart cities all over the country to achieve rapid urbanization in the country. Industrial and commercial infrastructure in the country has emerged as one of the high-growth sectors. The Indian government has been formulating initiatives like easing the rules to attract FDI inflow in the construction sector to expedite development across the nation.

- Many luxury apartments and residential complexes are under construction in Japan. For instance, Mitsubishi State is constructing Japan's tallest building, which is to comprise 50 luxury apartments, each of which will be able to generate USD 43,000 per month of rent. The project is being built near the Tokyo station and will reach completion by 2027.

- Thailand is one of the largest hubs for tourists and has been witnessing huge investments in the expansion and construction of malls, luxury hotels, etc. The Pattaya Marriott Marquis Hotel is the largest project in Thailand's pipeline, which may be in operation by 2024, with over 900 guest rooms. This new Marriott Marquis will be part of a dual-property development, which will also include the 398-room JW Marriott and the Pattaya Beach Resort & Spa. Marriott may add four new hotels under three of its brands across Bangkok and Pattaya in Thailand by 2027. Marriott's portfolio in Thailand includes 45 hotels and resorts, including nine properties with Asset World Corporation.

- All the above-mentioned factors are likely to fuel the growth of the Asia-Pacific fiber cement market over the forecast time frame.

Fiber Cement Industry Overview

The global fiber cement market is partially fragmented in nature, with no players capturing a significant share of the market studied. Some of the major companies are James Hardie Building Products Inc., Etex Group, NICHIHA Co., Ltd, SCG, and Elementia Materiales.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Residential Construction Across the World

- 4.1.2 Advantages Offered by Fiber Cement

- 4.2 Restraints

- 4.2.1 Presence of Alternatives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Siding

- 5.1.2 Roofing

- 5.1.3 Cladding

- 5.1.4 Molding and Trimming

- 5.1.5 Other Applications

- 5.2 End-user Industry

- 5.2.1 Residential

- 5.2.2 Non-residential

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 American Fiber Cement Corporation

- 6.4.2 Cembrit Holding A/S (Swisspearl Group AG)

- 6.4.3 CenturyPly

- 6.4.4 CSR Limited

- 6.4.5 Elementia Materials

- 6.4.6 Etex Group

- 6.4.7 Everest Industries Limited

- 6.4.8 James Hardie Industries PLC

- 6.4.9 NICHIHA Co. Ltd

- 6.4.10 Saint-Gobain

- 6.4.11 SCG

- 6.4.12 Toray Industries Inc.

- 6.4.13 TPI Polene Public Company Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

纤维水泥雨幕板市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2019-2029F

纤维水泥雨幕板市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2019-2029F 纤维水泥雨幕板市场:各产品类型,各建设类型,各终端用户,各地区,机会,预测,2017年~2031年

纤维水泥雨幕板市场:各产品类型,各建设类型,各终端用户,各地区,机会,预测,2017年~2031年 纤维水泥市场:依产品种类、依应用、按地区

纤维水泥市场:依产品种类、依应用、按地区 纤维水泥壁板和麵板市场,按产品类型、原材料、建筑类型、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

纤维水泥壁板和麵板市场,按产品类型、原材料、建筑类型、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 纤维水泥市场,按材料、应用、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

纤维水泥市场,按材料、应用、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 全球纤维水泥市场规模、份额和趋势分析报告 - 按最终用途、按原材料、按建筑类型、按地区、展望和预测,2024-2031

全球纤维水泥市场规模、份额和趋势分析报告 - 按最终用途、按原材料、按建筑类型、按地区、展望和预测,2024-2031 全球纤维水泥市场规模、份额、成长分析、按产品类型(板、片材)、最终用户(建筑、基础设施)、按应用(住宅、非住宅)- 2024-2031 年产业预测

全球纤维水泥市场规模、份额、成长分析、按产品类型(板、片材)、最终用户(建筑、基础设施)、按应用(住宅、非住宅)- 2024-2031 年产业预测 2024 年纤维水泥全球市场报告

2024 年纤维水泥全球市场报告 2023-2030 年全球纤维水泥市场规模研究与预测(依原料、建筑类型、最终用途及区域分析)

2023-2030 年全球纤维水泥市场规模研究与预测(依原料、建筑类型、最终用途及区域分析) 全球纤维水泥市场(2023-2033):依最终用户、应用、材料、地区/国家进行分析和预测

全球纤维水泥市场(2023-2033):依最终用户、应用、材料、地区/国家进行分析和预测