|

市场调查报告书

商品编码

1686524

生质塑胶市场占有率分析、产业趋势与统计、成长预测(2025-2030)Bioplastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

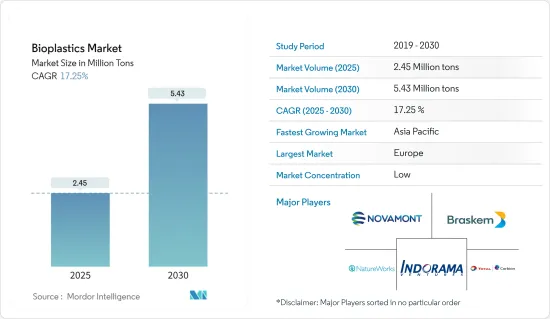

预计2025年生质塑胶市场规模为245万吨,2030年将达到543万吨,市场估计和预测期(2025-2030年)的复合年增长率为17.25%。

新冠疫情爆发导致全球范围内停工,扰乱了製造业活动和供应链,生产停顿对 2020 年的市场产生了影响。然而,情况在 2021 年开始好转,市场的成长轨迹在预测期内回升。

主要亮点

- 环境问题正在推动生质塑胶广泛使用的模式转移,这是推动市场发展的一个主要因素。此外,包装需求的成长预计也将推动市场成长。

- 然而,更廉价替代品的出现可能会阻碍市场的成长。

- 其在电子行业的日益广泛的应用可能会为市场带来新的成长机会。

- 欧洲贡献了最高的市场占有率,预计在预测期内将继续主导市场。

生质塑胶市场趋势

软包装可望主导市场

- 生质塑胶用于软包装,因为它们对自然无害且易于分解。

- 生质塑胶用于食品、药品的包装膜、饮料瓶、包装薄膜等,也用于包装非食品产品,如餐巾纸、纸巾、厕所用卫生纸、尿布、卫生棉,用于食品包装的纸板和铜版纸,以及用于製作杯子和盘子的铜版纸。此外,它还用于软包装和鬆散填充包装。

- 由玉米粉製成的生质塑胶正在软包装和鬆散填充包装中得到应用。

- 聚乳酸(PLA)主要用于食品包装,生物基聚对苯二甲酸乙二醇酯(PET)、生物基聚乙烯、生物基聚丙烯主要用作包装薄膜。

- 根据Packmedia称,全球柔性转换包装市场预计到2021年价值将达到1,020亿美元,与前一年同期比较成长8%。

- 根据Packmedia报道,美国和中亚及东亚各占28%的市占率。在欧洲,销售额成长了 6.4%,销量成长了 1.6%。 2022 年的成长预测分别为 2.9% 和 2%,同样达到欧洲水准。

- 全球包装产业正在成长。亚太地区生质塑胶产能最大,占45%。此外,中国、印度和日本等国家消费者意识的增强和政府的严格禁令正在推动该地区生质塑胶的消费。

- 因此,预计上述因素将在预测期内对市场产生正面影响。

欧洲主导市场

- 欧洲占据整个生质塑胶市场的主导地位,大部分需求来自德国、法国、义大利和英国。

- 德国食品和饮料行业的特点是中小企业部门,拥有超过 6,000 家公司。 2021年食品和饮料市场收益预计为32.22亿美元。在预测期内,市场预计将以 6.83% 的年增长率成长,这主要得益于该国软包装和硬包装行业以及生质塑胶消费的增长。

- 根据联邦统计局的数据,德国农业国内生产总值) 从 2021 年第三季的 74.1 亿欧元(约 86.1 亿美元)增至 2021 年第四季的 76.4 亿欧元(约 88.8 亿美元)。

- 法国拥有欧洲最大的农业部门。它是世界领先的农业生产国之一,生产甜菜、葡萄酒、牛奶、牛肉和小牛肉、谷物和油籽。然而,法国却遭遇了严重旱灾。据法国主要农业工人工会 FNSEA 称,由于今年春夏法国遭遇极端高温和缺雨,全国 44 万名农民中已有 1.4 万名农民提出了赔偿要求。

- 2021年,法国汽车产量约13,511,308辆,较2020年成长3%。

- 义大利包装产业是世界上最大的包装产业之一。全国有大、中、小型包装企业近7000家。超级市场零售日益增长的重要性以及消费者购买习惯的改变正在推动该国包装需求的成长。此外,出口也增加了对包装材料的需求。

- 2021年前三季度,义大利汽车总产量与2020年前第三季相比成长了20%,达到600,586辆。此外,2021 年汽车总产量将达到约 795,856 辆,较 2020 年的约 777,165 辆增加 2%。电动车的日益普及预计将在未来几年推动整个产业的成长。

- 英国是欧洲第四大塑胶消费国。该国是先进和改性塑胶开发领域最具创新力和领先的国家之一。然而,随着人们越来越意识到石油基、非生物分解的塑胶对环境的影响,国家开始转向生质塑胶。

- 英国是欧洲最大的高端消费性电子产品市场,约有18,000家电子公司在英国设立。根据英国国际贸易部的数据,英国电子业每年为当地经济创造约 160 亿英镑(约 218.6 亿美元)的价值。

- 因此,预计该地区的市场状况将在整个预测期内推动对生质塑胶的需求。

生质塑胶产业概况

生质塑胶市场比较分散。市场的主要企业(不分先后顺序)包括 Braskem、Novamont SpA、NatureWorks LLC、Indorama Ventures Public Company Limited 和 Total Corbion PLA。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 推动模式转移的环境因素

- 包装对生质塑胶的需求不断增长

- 限制因素

- 有更便宜的替代品

- 产业价值链

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 专利分析

第五章市场区隔

- 类型

- 生物基和生物分解性

- 淀粉基

- 聚乳酸(PLA)

- 聚羟基烷酯(PHA)

- 聚酯(PBS、PBAT、PCL)

- 其他生物基和生物分解性材料

- 生物基非生物分解

- 生物聚对苯二甲酸乙二醇酯(PET)

- 生物聚乙烯

- 生物聚酰胺

- 生物聚对苯二甲酸丙二醇酯

- 其他非生物分解材料

- 生物基和生物分解性

- 应用

- 软包装

- 硬质包装

- 汽车和组装

- 农业和园艺

- 建筑学

- 纤维

- 电气和电子

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率分析

- 主要企业策略

- 公司简介(概况、财务状况**、产品/服务、最新发展)

- Trinseo

- Arkema

- BASF SE

- BIOTEC

- Braskem

- Danimer Scientific

- Rodenburg Biopolymers

- Futerro

- Indorama Ventures Public Company Limited

- Minima

- Natureworks LLC

- Novamont SpA

- Total Corbion PLA

第七章 市场机会与未来趋势

- 扩大电子产业的应用

The Bioplastics Market size is estimated at 2.45 million tons in 2025, and is expected to reach 5.43 million tons by 2030, at a CAGR of 17.25% during the forecast period (2025-2030).

Due to the COVID-19 outbreak, nationwide lockdowns around the globe disrupted manufacturing activities and supply chains, and production halts impacted the market in 2020. However, the conditions started recovering in 2021, restoring the market's growth trajectory during the forecast period.

Key Highlights

- A significant factor driving the market studied is the environmental issues encouraging a paradigm shift to promote bioplastics. Additionally, the growing demand for packaging will likely favor the market's growth.

- However, the cheaper alternatives availability is likely to hamper the market's growth.

- Growing use in the electronics industry will likely provide new growth opportunities for the market.

- Europe accounts for the highest market share and is expected to dominate the market during the forecast period.

Bioplastics Market Trends

Flexible Packaging is Expected to Dominate the Market

- Bioplastics are used in flexible packaging as they are not harmful to nature and are easily degradable.

- They are used in packaging films for food items, medicines, beverage bottles, and packaging films. It is also used in packaging non-food products, such as napkins and tissues, toilet paper, nappies, sanitary towels, cardboard and coat paper for food wrapping paper, and coated cardboard to make cups and plates. Moreover, they are used in flexible and loose-fill packaging.

- Bioplastics made of cornstarch have applications in flexible and loose-fill packaging.

- Polylactic acid (PLA) is used mainly in packaging food items, while bio polyethylene terephthalate (PET), bio polyethylene, and bio polypropylene are majorly used as packaging films.

- According to Packmedia, in 2021, the world market for flexible converter packaging was estimated at USD 102 billion, up 8% from the previous year.

- According to Packmedia, the United States and Central and East Asia each share 28% of the market. At the European level, growth is around +6.4% for sales and +1.6% in volume. Growth prospects for 2022, again at the European level, are 2.9% and 2%, respectively.

- The global packaging industry is growing. Asia-Pacific includes the most significant manufacturing capacity for bioplastics, i.e., 45%. Moreover, the increasing awareness among consumers and the government's strict ban in countries like China, India, and Japan have promoted bioplastic consumption in the region.

- Thus, the abovementioned factors are expected to impact the market during the forecast period positively.

Europe to Dominate the Market

- Europe dominated the overall bioplastics market, with most of the demand coming from Germany, France, Italy, and the United Kingdom.

- Germany's food and beverage industry are characterized by its small and medium-sized enterprise sector of over 6,000 companies. The revenue in the food and beverage market was estimated at USD 3,222 million in 2021. The market is expected to grow annually by 6.83% during the forecast period, driving the country's flexible and rigid packaging industry and bioplastic consumption.

- According to the Federal Statistical Office, the Gross domestic product (GDP) from agriculture in Germany increased to EUR 7.64 billion (~USD 8.88 billion) in the fourth quarter of 2021 from EUR 7.41 billion (~USD 8.61 billion) in the third quarter of 2021.

- France is home to the largest agricultural sector in Europe. It is among the top producers in the global agriculture market and produces sugar beets, wine, milk, beef and veal, cereals, and oilseeds. However, the country experienced severe droughts. According to France's main agricultural trade union, FNSEA, 14,000 farms out of 440,000 filed compensation claims following the extreme heat and lack of rain that ravaged France during the spring and summer.

- In 2021, France produced about 13,51,308 units of vehicles, which increased by 3% in comparison to 2020.

- Italy's packaging industry is one of the largest in the world. There are nearly 7,000 significant and minor packaging companies active in the country. The growing importance of supermarket retailing and the changing consumer purchasing habits are increasing the packaging demand in the country. Besides, exports are adding to the need for packaging materials.

- The total production of automobiles in the first three quarters of 2021, Italy's automotive production increased by 20% over Q1-Q3 of 2020 and reached 600,586 vehicles. Moreover, the overall vehicle production in 2021 came to about 795,856 units, which increased by 2% compared to 2020, with a volume of about 777,165. The growing popularity of electric vehicles is expected to support the overall industry growth in the upcoming future.

- The United Kingdom is the fourth-largest consumer of plastics in Europe. The country is identified as one of the most innovative and advanced countries in terms of developing advanced and modified plastics. However, the country is focusing on bioplastics due to the increasing awareness about the environmental impact of petroleum-based non-biodegradable plastics.

- The United Kingdom is the largest European market for high-end consumer electronics products, with about 18,000 UK-based electronics companies. According to the Department for International Trade, the electronics sector in the United Kingdom is worth around GBP 16 billion (~USD 21.86 billion) yearly to the local economy.

- Hence, the market scenario in the region is expected to boost the demand for bioplastics throughout the forecast period.

Bioplastics Industry Overview

The bioplastics market is fragmented. Some of the key players in the market (not in any particular order) include Braskem, Novamont SpA, NatureWorks LLC, Indorama Ventures Public Company Limited, and Total Corbion PLA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Environmental Factors Encouraging a Paradigm Shift

- 4.1.2 Growing Demand for Bioplastics in Packaging

- 4.2 Restraints

- 4.2.1 Availability of Cheaper Alternatives

- 4.3 Industry Value Chain

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

- 4.5 Patent Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Bio-based Biodegradables

- 5.1.1.1 Starch-based

- 5.1.1.2 Polylactic Acid (PLA)

- 5.1.1.3 Polyhydroxy Alkanoates (PHA)

- 5.1.1.4 Polyesters (PBS, PBAT, and PCL)

- 5.1.1.5 Other Bio-based Biodegradables

- 5.1.2 Bio-based Non-biodegradables

- 5.1.2.1 Bio Polyethylene Terephthalate (PET)

- 5.1.2.2 Bio Polyethylene

- 5.1.2.3 Bio Polyamides

- 5.1.2.4 Bio Polytrimethylene Terephthalate

- 5.1.2.5 Other Non-biodegradables

- 5.1.1 Bio-based Biodegradables

- 5.2 Application

- 5.2.1 Flexible Packaging

- 5.2.2 Rigid Packaging

- 5.2.3 Automotive and Assembly Operations

- 5.2.4 Agriculture and Horticulture

- 5.2.5 Construction

- 5.2.6 Textiles

- 5.2.7 Electrical and Electronics

- 5.2.8 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials**, Products and Services, and Recent Developments)

- 6.4.1 Trinseo

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 BIOTEC

- 6.4.5 Braskem

- 6.4.6 Danimer Scientific

- 6.4.7 Rodenburg Biopolymers

- 6.4.8 Futerro

- 6.4.9 Indorama Ventures Public Company Limited

- 6.4.10 Minima

- 6.4.11 Natureworks LLC

- 6.4.12 Novamont SpA

- 6.4.13 Total Corbion PLA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Use in the Electronics Industry

2025-2033年生物塑胶市场报告(按产品、应用、配销通路和地区)农产品生质塑胶市场(按类型、原料、报废产品和应用)-2025-2030 年全球预测生质塑胶市场:2025-2030 年全球预测(按原料、降解性、加工方法和最终用户)

2025-2033年生物塑胶市场报告(按产品、应用、配销通路和地区)农产品生质塑胶市场(按类型、原料、报废产品和应用)-2025-2030 年全球预测生质塑胶市场:2025-2030 年全球预测(按原料、降解性、加工方法和最终用户) 电气和电子产品中的消费后再生塑胶市场规模、份额、趋势分析报告:产品、应用、地区、细分市场预测,2025-2030 年

电气和电子产品中的消费后再生塑胶市场规模、份额、趋势分析报告:产品、应用、地区、细分市场预测,2025-2030 年 全球先进化学品/原料回收市场(2025-2040)

全球先进化学品/原料回收市场(2025-2040) 生质塑胶:全球市场与技术

生质塑胶:全球市场与技术 全球纤维素生物塑胶市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年

全球纤维素生物塑胶市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年 2025 年生质塑胶和生物聚合物全球市场报告

2025 年生质塑胶和生物聚合物全球市场报告 生质塑胶市场:按产品、应用和地区划分航太生质塑胶市场规模、份额和成长分析(按类型、应用和地区)- 产业预测 2025-2032

生质塑胶市场:按产品、应用和地区划分航太生质塑胶市场规模、份额和成长分析(按类型、应用和地区)- 产业预测 2025-2032