|

市场调查报告书

商品编码

1444142

指纹感应器:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Fingerprint Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

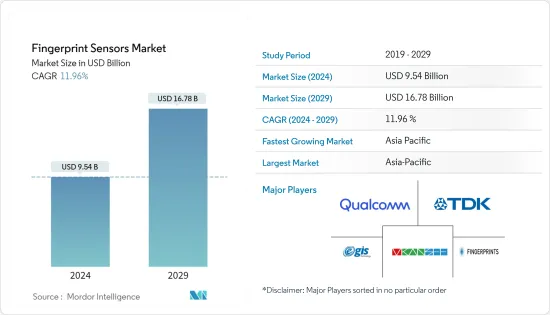

指纹感应器市场规模预计到 2024 年为 95.4 亿美元,预计到 2029 年将达到 167.8 亿美元,预测期内(2024-2029 年)复合年增长率为 11.96%。

指纹感应器市场在过去几年中迅速扩大,预计在预测期内将进一步扩大。智慧型手机普及的不断提高、安全应用数量的增加以及政府采用生物识别的倡议往往是推动全球指纹感测器需求的主要因素。

主要亮点

- 指纹是各种设备和应用领域中使用的典型生物识别之一,这就是指纹感应器的需求不断增加的原因。此外,生物辨识研究所 2021 年 6 月对全球 360 名受访者进行的调查显示,56% 的欧洲受访者同意有关生物辨识的严格法律。

- 配备指纹感应器的智慧型手机的日益普及是指纹感应器成长的显着驱动因素之一。例如,根据Counterpoint的报告,2021年第一季,三星等智慧型手机全球出货量约7,700万部,iPhone全球出货总计为5,700万部。

- 因此,平板电脑、笔记型电脑、智慧型手机和智慧型穿戴装置等智慧型装置的人均数量预计在未来几年将会增加。这些设备越来越多地包含指纹感应器。据思科称,2018年人均网路设备数量为8台,预计2022年将达到每人13.6台。

- 由于高速网路普及影响力不断扩大,智慧型手机的渗透率正在急剧上升,预计随着5G的到来,智慧型手机的普及将进一步提高。根据 GSMA 的数据,到 2025 年,北美智慧型手机用户数量预计将达到 3.28 亿。此外,到 2025 年,该地区的行动用户普及(86%) 和网路普及率 (80%) 可能会提高。此外,根据 GSMA 的数据,预计到 2025 年,欧洲将拥有最高的网路普及(82%) 和智慧型手机普及率 (88%)。

- 脸部辨识系统在各种设备中变得越来越普遍。例如,Apple、Samsung 和 OnePlus 等主要智慧型手机供应商已经内建了这种使用者验证功能。这种替代技术的日益普及可能会阻碍指纹感测器市场的成长。

- COVID-19 大流行增加了对智慧型手机、笔记型电脑、个人电脑和平板电脑等消费性电器产品的需求。例如,根据 RBC.ru 报导,2020 年 3 月疫情期间俄罗斯笔记型电脑销量有所增长,增幅达 50%。

指纹感应器市场趋势

智慧型手机应用程式预计将占据很大份额

- 在研究中考虑的所有其他设备中,智慧型手机是利用指纹感应器进行使用者身份验证的最大部分。东芝于 2011 年首次将指纹感应器应用于智慧型手机,但 Apple Touch ID 彻底改变了行动装置中的指纹感应器。

- Apple 的 Touch ID 基于电容技术,准确且易于使用,使用户身份验证快速且流畅。在苹果成功之后,三星和其他大公司也开始使用各种指纹技术进行身份验证。

- 在技术方面,电容式触控萤幕感应器正在被高阶行动电话中的超音波指纹感应器和其他设备中的光学感应器所取代。放弃电容式感测器是由于将感测器整合到显示器中的需求不断增加。

- 另一方面,平板电脑使用电容式感应器,许多小型製造商选择不在平板电脑上使用指纹感应器以保护边框。然而,三星、联想和华硕等公司在其平板电脑中使用电容式感测器。

- 智慧型手机的日益普及预计将在所研究的市场中创造更多机会。例如,《2021 年爱立信行动报告》显示,新智慧型手机用户数量超过 55 亿。

亚太地区将经历最高成长

- 中国行动交易的成长,加上政府的倡议,预计将成为该国指纹感测器市场的主要驱动力。中国的移动交易量正在迅速增加,预计这将为所研究的市场创造潜力。

- 根据中国互联网络资讯中心(CNNIC)的数据,2020年约有8.525亿用户使用行动付款交易,高于2018年的5.833亿。行动付款交易的增加增加了对各种指纹感应器的需求。

- 该公司持续的产品创新主要推动了日本指纹扫描器市场的发展。例如,2021 年 7 月,Fingerprint Cards 与东京公司 MorX 合作,在日本开发并推出生物识别付款卡。该卡具有超低功耗,配备客製化的指纹T型模组,采用标准自动化製造技术整合到支付卡中。在非接触式付款卡中添加生物识别感测器可以增加卡片支付,同时提高安全性、清洁度和卫生性。

- 日本汽车产业的公司也积极期待将指纹感应器整合到他们的下一代车型中。例如,日产推出了采用指纹生物识别的 Nissan Xmotion 概念车,以增强车辆安全性。

- 在生物识别,付款卡市场强劲,由于生物辨识付款卡需求不断增加,指纹感应器的需求大幅增加。目前,各种市场供应商正在致力于整合生物识别技术。他们将提供真正颠覆性的服务,从而显着扩大银行在国内、各种最终用户甚至其他地区的客户群。

指纹感应器产业概况

指纹感应器市场较为分散,高通、Fingerprint Card AB 和 Synaptics 等国际公司透过在各种智慧型手机中部署其解决方案占据了主要市场占有率。指纹感应器公司正在开发智慧型手机以外的新市场,甚至进入物联网领域,将指纹感应器整合到智慧卡中。我们不断整合不同的技术来改善最终用户体验。

- 2022 年 1 月 - Vivo 推出的 IQOO 9 Pro 是首款配备高通 3D Sonic Max超音波指纹辨识器的智慧型手机,并搭载最新的 Snapdragon 8 Gen 1 处理器。 IQOO 9 Pro 上的 Qualcomm 3D Sonic Max 只需轻轻一按即可实现超快速的指纹註册流程。用户指纹註册后,只需 0.2 秒即可解锁。

- 2021 年 9 月 - IDEMIA 推出 IDEMIA STORM ABIS,这是一个基于 SaaS 的自动生物识别系统 (ABIS),可实现直觉、可存取且经济实惠的指纹分析、比较和记录。 IDEMIA STORM ABIS 透过比较、分析和案例管理工具支援本地和国家搜寻,使指纹检查员能够在任何地方有效且有效率地完成测试。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

- 调查系统

- 二次调查

- 初步调查

- 对资料进行三角测量并产生见解

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 买方议价能力

- 供应商的议价能力

- 新进入者的威胁

- 竞争程度

- 替代产品的威胁

- 产业价值链分析

- 评估 COVID-19 的影响

第五章市场动态

- 市场驱动因素

- 智慧型穿戴装置和智慧型手机越来越多地使用指纹感应器

- 对安全保障和业务应用程式的需求

- 政府努力在各个领域引入生物辨识技术

- 市场限制因素

- 更多采用脸部和虹膜扫描等替代技术

第六章市场区隔

- 按类型

- 光学

- 电容

- 热

- 超音波

- 按用途

- 智慧型手机/平板电脑

- 笔记型电脑

- 智慧卡

- 物联网/其他应用

- 按最终用户产业

- 军事/国防

- 消费性电子产品

- BFSI

- 政府

- 其他的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章 竞争形势

- 公司简介

- Qualcomm Technologies, Inc.

- TDK Corporation

- Vkansee Technology Inc.

- Egis Technology Inc.

- Fingerprint Cards AB

- Shenzhen Goodix Technology Co. Ltd

- Idex Biometrics ASA

- NEC Corporation

- Next Biometrics Group ASA

- Synaptics Inc.

- Thales Group(Gemalto NV)

- Idemia France SAS

- Crucialtec Co Ltd.

- Sonavation Inc.

第八章投资分析

第9章市场的未来

The Fingerprint Sensors Market size is estimated at USD 9.54 billion in 2024, and is expected to reach USD 16.78 billion by 2029, growing at a CAGR of 11.96% during the forecast period (2024-2029).

The fingerprint sensors market has expanded rapidly over the past few years and is projected to increase even further during the forecast period. Increased adoption of smartphones, increasing security applications, and government initiatives to adopt biometrics tend to be the key factors driving the demand for fingerprint sensors globally.

Key Highlights

- The fingerprint is among the prominent type of biometrics used in various devices and application fields, owing to which the demand for fingerprint sensors is on the rise. Moreover, according to the survey carried out by Biometrics Institute for 360 respondents across the globe in June 2021, 56% of the respondents from Europe agree with strict legislation concerning biometrics.

- The growing penetration of smartphones, which are equipped with fingerprint sensors, is among the prominent driver of the growth of fingerprint sensors. For instance, as reported by counterpoint, In Q1 of 2021, the shipment of smartphones like Samsung accounted for approximately 77 million globally, and loads of iPhones globally accounted for 57 million.

- In line with that, the number of intelligent devices, such as tablets, laptops, smartphones, and smart wearables per person, is expected to increase over the coming years; these devices are increasingly being incorporated with fingerprint sensors. According to Cisco, in 2018, the number of networked devices per person stood at eight and is expected to reach 13.6 per person by 2022.

- The penetration of smartphones is increasing exponentially, owing to the increasing influence of fast internet access, and with the advent of 5G, smartphone penetration is expected to increase even further. According to GSMA, the number of smartphone subscribers in North America is expected to reach 328 million by 2025. Moreover, by 2025, the region may witness an increase in the penetration rates of mobile subscribers (86%) and the internet (80%). Additionally, according to GSMA, by 2025, Europe is estimated to register the highest internet penetration rate (82%) and smartphones (88%).

- Facial recognition systems are increasingly becoming common in various devices. For instance, major smartphone vendors, such as Apple, Samsung, and OnePlus, have already incorporated this user authentication. This increase in the adoption of substitute technology can hamper the growth of the fingerprint sensors market.

- The COVID-19 pandemic has increased the demand for consumer electronics such as smartphones, laptops, PCs, and tablets. For instance, the sale of notebooks grew in Russia amid the pandemic in March 2020 and accounted for a growth of 50%, according to RBC.ru.

Fingerprint Sensors Market Trends

Applications in Smartphones is expected to Hold a Major Share

- The smartphone is the largest segment to utilize fingerprint sensors for user authentication among all the other devices considered in the study. The earliest application of fingerprint sensors in smartphones was in 2011 by Toshiba, but Apple touch ID revolutionized fingerprint sensors in mobile devices.

- Apple's Touch ID, based on capacitive technology, was accurate and easy to use, because of which the authentication of the user became fast and smooth. After Apple's success, Samsung and other major players also started using different fingerprint technologies for authentication.

- Regarding technology, the capacitive touchscreen sensors are being replaced by ultrasonic fingerprint sensors in premium phones and optical sensors in the rest of the devices. The shift from capacitive sensors has been due to the growing demand to integrate sensors in the display.

- On the other hand, Tablets have been using capacitive sensors, and many times to keep the bezels, many small manufacturers have opted not to use fingerprint sensors on their tablets. However, companies like Samsung, Lenovo, and Asus, have been using capacitive sensors in their tablets.

- The increasing penetration of smartphones is expected to create more opportunities in the studied market. For instance, Ericsson Mobility Report 2021 shows more than 5.5 billion new smartphone subscriptions.

Asia Pacific to Witness Highest Growth

- Increasing mobile transactions in China, coupled with the government's initiatives, are expected to be the major drivers for the fingerprint sensors market in the country. China is witnessing a high mobile transactional volume, expected to create the potential for the market studied.

- According to the China Internet Network Information Center (CNNIC), in 2020, around 852.5 million users used mobile payment transactions, which increased from 583.3 million users in 2018. such an increase in mobile payment transactions provides an increasing need for various fingerprint sensors.

- The company's continuous product innovations primarily drive the market for fingerprint scanners in Japan. For instance, in July 2021, Fingerprint Cards collaborated with Tokyo-based company MoriX Co. Ltd to develop and launch biometric payment cards in Japan. Fingerprints' T-Shape module, which boasts ultra-low power consumption and is customized to be integrated into payment cards using standard automated manufacturing techniques, will be featured on the cards. Adding biometric sensors to contactless payment cards improves security, cleanliness, and sanitation while increasing card payment.

- The Japanese companies in the automotive sector are also actively looking forward to integrating fingerprint sensors in their upcoming models. For instance, Nissan introduced its concept car Nissan Xmotion featured fingerprint biometric authentication for enhanced security of the vehicles.

- Fingerprint sensors are witnessing a significant demand in South Korea due to the increasing demand for biometric payment cards, and there is a robust market for payment cards. Various market vendors are currently working to integrate biometric technology. They will have a genuinely disruptive offering that will significantly expand the banking customer base in the country, various end-users, and beyond.

Fingerprint Sensors Industry Overview

The fingerprint sensor market is fragmented, with individual international companies such as Qualcomm, Fingerprint Card AB, and Synaptics occupying a significant market share by deploying their solutions in various smartphones. Fingerprint sensor firms are unlocking new markets beyond smartphones, exploring even the IoT field, and integrating fingerprint sensors into smart cards. They are constantly incorporating different technologies to enhance the end-user experiences.

- January 2022 - The Vivo launched IQOO 9 Pro is the first smartphone to include Qualcomm's 3D Sonic Max ultrasonic fingerprint reader and is powered by the brand-new Snapdragon 8 Gen 1 processor. The IQOO 9 Pro's Qualcomm 3D Sonic Max enables a lightning-fast fingerprint enrollment process with just one tap. Once the user fingerprint is registered, it unlocks the phone in just 0.2 seconds.

- September 2021- IDEMIA launched the SaaS-based Automated Biometric Identification System (ABIS), IDEMIA STORM ABIS, for intuitive, accessible, affordable fingerprint analysis, comparison, and documentation. IDEMIA STORM ABIS supports local and national searches through tools for comparison, analysis, and case management that permits fingerprint examiners to effectively and efficiently complete examinations from anywhere.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Degree of Competition

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment Of COVID-19 Impact

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Usage of Fingerprint Sensors for Smart Wearable Devices and Smartphones

- 5.1.2 Need for Secured Security and Business Applications

- 5.1.3 Government Initiatives to Adopt Biometrics in Various Fields

- 5.2 Market Restraints

- 5.2.1 Increase in Adoption of Substitute Technologies, such as Face and Iris Scanning

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Optical

- 6.1.2 Capacitive

- 6.1.3 Thermal

- 6.1.4 Ultrasonic

- 6.2 By Application

- 6.2.1 Smartphones/Tablets

- 6.2.2 Laptops

- 6.2.3 Smartcards

- 6.2.4 IoT and Other Applications

- 6.3 By End-User Industries

- 6.3.1 Military and Defense

- 6.3.2 Consumer Electronics

- 6.3.3 BFSI

- 6.3.4 Government

- 6.3.5 Other End-User Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 South Korea

- 6.4.3.5 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle-East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Qualcomm Technologies, Inc.

- 7.1.2 TDK Corporation

- 7.1.3 Vkansee Technology Inc.

- 7.1.4 Egis Technology Inc.

- 7.1.5 Fingerprint Cards AB

- 7.1.6 Shenzhen Goodix Technology Co. Ltd

- 7.1.7 Idex Biometrics ASA

- 7.1.8 NEC Corporation

- 7.1.9 Next Biometrics Group ASA

- 7.1.10 Synaptics Inc.

- 7.1.11 Thales Group (Gemalto NV)

- 7.1.12 Idemia France SAS

- 7.1.13 Crucialtec Co Ltd.

- 7.1.14 Sonavation Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

指纹感应器市场规模、份额、成长分析,按类型、按技术、按应用、按最终用户、按地区 - 行业预测,2024-2031 年

指纹感应器市场规模、份额、成长分析,按类型、按技术、按应用、按最终用户、按地区 - 行业预测,2024-2031 年 全球指纹感应器市场:按技术、类型、应用和最终用户划分 - 预测 2025-2030 年

全球指纹感应器市场:按技术、类型、应用和最终用户划分 - 预测 2025-2030 年 到 2030 年指纹感应器市场预测:按产品、材料、功能、技术、应用和地区进行的全球分析

到 2030 年指纹感应器市场预测:按产品、材料、功能、技术、应用和地区进行的全球分析 硅基指纹感应器市场:按类型、应用和最终用途划分 - 2025-2030 年全球预测

硅基指纹感应器市场:按类型、应用和最终用途划分 - 2025-2030 年全球预测 指纹感应器市场 - 2024 年至 2029 年预测

指纹感应器市场 - 2024 年至 2029 年预测 指纹感应器市场 - 全球产业规模、份额、趋势、机会和预测,按类型、技术、应用、地区和竞争细分,2019-2029F

指纹感应器市场 - 全球产业规模、份额、趋势、机会和预测,按类型、技术、应用、地区和竞争细分,2019-2029F 指纹感测器市场,规模,占有率,趋势,产业分析报告:各类型,各技术,各用途,各地区 - 市场预测,2024年~2032年

指纹感测器市场,规模,占有率,趋势,产业分析报告:各类型,各技术,各用途,各地区 - 市场预测,2024年~2032年 指纹感应器市场:按类型、按技术、按行业、按地区

指纹感应器市场:按类型、按技术、按行业、按地区 全球指纹感应器市场:市场规模、份额、行业成长分析:按感测器技术、类型、技术、最终用途、地区 - 预测到 2029 年

全球指纹感应器市场:市场规模、份额、行业成长分析:按感测器技术、类型、技术、最终用途、地区 - 预测到 2029 年 2024-2032 年按类型、技术、应用和地区分類的指纹感测器市场报告

2024-2032 年按类型、技术、应用和地区分類的指纹感测器市场报告