|

市场调查报告书

商品编码

1444147

腈纶:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Acrylic Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

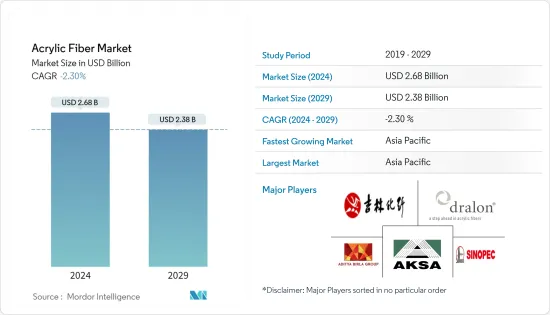

2024年腈纶市场规模预计为26.8亿美元,预计2029年将下降至23.8亿美元。

2021 年,市场受到 COVID-19 的负面影响,因为疫情导致企业、产品和製造设施放缓,导致经济活动减少。然而,市场在预测期内不会復苏。

主要亮点

- 从中期来看,推动所研究市场成长的主要因素包括对服装使用的高需求。

- 另一方面,聚酯等替代品的出现以及全球对丙烯酸纤维生产的严格监管预计将阻碍市场成长。

- 从形状来看,长丝细分市场占据最大的市场占有率,预计在预测期内将成长。

- 由于东南亚国协和印度的高需求,亚太地区主导了腈纶纤维市场。

腈纶纤维市场趋势

羊毛细分市场占据主导地位

- 羊毛在服装类中的使用可以追溯到古代。羊毛具有抗皱、吸湿、保暖等优良能。羊毛的一个主要特征是它能够随着时间的推移从变形中恢復。因此,由这些纤维製成的服装类很有吸引力。

- 由 100% 羊毛纤维机织或针织的布料可用于服装,如毛衣、连帽衫、靴子、靴子内衬、帽子、手套、运动服、地毯、毯子、滚刷、室内装饰、块毯和防护衣。成为製造标准。

- 大多数丙烯酸纤维用于製造非常流行的羊毛和丙烯酸混纺织品。 55% 羊毛和 45% 丙烯酸纤维的混合物用于製造圆形针织产品。这种混合物特别用于运动服的生产,具有易于护理、耐用、外观保持、色彩造型和偏好等特点。

- 根据您的要求,有多种混合物在世界各地广泛使用。 50/50 和 70/30 腈纶羊毛混纺很受欢迎,因为它们便宜、美观且易于加工。根据 TextileExchange.org 统计,2021 年羊毛纤维产量为 103 万吨。

- 因此,羊毛产业对丙烯酸纤维的需求不断增加可能会主导市场。

中国将主导亚太地区

- 中国是全球最大的腈纶生产国,占全球腈纶产量的30%以上。中国纺织业多年来规模不断扩大,主要得益于东南亚国协、欧洲、美国、日本等国内外市场的需求。

- 伊朗、印度、越南、巴基斯坦和阿联酋是中国腈纶纤维出口的最大市场。该国也从日本、德国、泰国、韩国和土耳其等国家进口丙烯酸纤维。

- 2021年,我国腈纶进口总合7.5万吨,较2020年的6.8万吨增加10.3%。 2021年的增加主要是由于3月至5月的增加,期间增加了约7,800吨。服装和家居应用的需求不断增长可能会推动丙烯酸纤维市场的发展。

- 中国是全球最大的纺织品生产国和出口国,以金额为准计算约占世界纺织品出口总额的43%。因此,中国服饰的成长可望提振腈纶市场。

- 因此,所有这些市场趋势预计将在预测期内提振中国腈纶市场的需求。

腈纶纤维产业概况

腈纶纤维市场本质上是整合的。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 服装应用需求高

- 线上购买推动了对最终用途产品的需求

- 抑制因素

- 聚酯等替代品的可用性

- 世界各地对丙烯酸纤维生产的严格规定

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章市场区隔(市场规模、数量)

- 型态

- 订书钉

- 灯丝

- 混合

- 羊毛

- 棉布

- 其他(纤维素)

- 目的

- 服饰

- 家居家具

- 产业

- 其他(室内装潢)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 土耳其

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、合作与协议

- 市场占有率(%)分析

- 主要企业采取的策略

- 公司简介

- Aditya Birla Management Corporation Pvt. Ltd

- Aksa Akrilik Kimya Sanayii AS

- China Petrochemical Corporation

- Dralon

- FORMOSA PLASTIICS CORPORATIION

- Goonvean Fibres

- Indian Acrylics Limited

- Japan Exlan Co. Ltd

- Jiangsu Zhongxin Resources Group

- Jilin Chemical Fiber Group Co. Ltd

- Kaltex

- KANEKA CORPORATION

- Mitsubishi Chemical Corporation

- Pasupati Acrylon Ltd

- PetroChina Company Limited

- Polyacryl Iran Corp.

- Polymir

- SDF

- SGL Carbon

- Taekwang Industrial Co. Ltd

- TORAY INDUSTRIES INC.

- Vardhman Acrylics Ltd

- Yousuf Dewan Companies

第七章市场机会与未来趋势

The Acrylic Fiber Market size is estimated at USD 2.68 billion in 2024, and is expected to decline to USD 2.38 billion by 2029.

The market was negatively impacted by COVID-19 in 2021, as the pandemic resulted in the slowdown of businesses, products, and manufacturing facilities, resulting in less economic activity. However, the market is excepted to recover during the forecasting period.

Key Highlights

- Over the medium term, the major factor driving the growth of the market studied includes the high demand for the use of apparel.

- On the flip side, the availability of substitutes like polyester and stringent regulations worldwide on the production of acrylic fiber are expected to hinder the growth of the market.

- By form, the filament segment accounted for the largest market share, and it is expected to grow during the forecast period.

- Asia-Pacific dominated the acrylic fiber market due to high demand from the ASEAN countries and India.

Acrylic Fiber Market Trends

Wool Segment to Dominate the Market

- The use of wool for clothing ages back to ancient times. Wool has outstanding properties, such as resistance to wrinkles, moisture absorption, and warmth. A significant feature of wool is its ability to recover from deformation over time. Hence, clothing made from these fibers is attractive.

- Fabrics that are woven or knitted with 100% wool fiber have become a standard in making apparel, like sweaters, hoodies, boots, boot lining, hats, gloves, athletic wear, carpeting, blankets, roller brushes, upholstery, area rugs, protective clothing, wigs, hair extensions.

- The majority of Acrylic Fiber is used to make wool and acrylic blends which are very popular. These blends of 55% wool and 45% acrylic fiber are used to make circular knit goods. This blend is particularly used in making sportswear, which has characteristics like the ease of care, durability, appearance retention, color styling, and palatability.

- Depending on the requirements, there are different blends that are widely used across the world. The 50/50 and 70/30 acrylic wool blends are popular among those that are inexpensive, look good, and are easy to handle. The 50/50 acrylic wool blend is used to make lightweight apparel that has excellent durability and shape retention. The 70/30 acrylic wool blend is used to make slacks. According to TextileExchange.org, 1.03 million tonnes of wool fiber was produced in 2021.

- Hence, increasing demand for acrylic fiber in the wool segment is likely to dominate the market.

China to Dominate the Asia-Pacific Region

- China is the largest producer of acrylic fibers across the world, accounting for a share of more than 30% of the global acrylic fiber production. Owing to the demand from domestic and international markets, primarily from ASEAN countries, Europe, the United States, and Japan, the textile industry in China has expanded over the years.

- Iran, India, Vietnam, Pakistan, and the United Arab Emirates are some of the largest markets where China exports acrylic fibers. The country also imports acrylic fiber from countries like Japan, Germany, Thailand, South Korea, and Turkey.

- In 2021, China's acrylic fiber import volumes totaled 75,000 tons, up 10.3% from 68,000 tons in 2020. The rise in 2021 was mainly attributed to the increase in March-May, up about 7,800 tons during the period. Increased demand from apparel and household furnishing applications may drive the market for acrylic fibers.

- China is the largest textile-producing and exporting country in the world, it holds about 43% share of the world's total textile exports in terms of value. Thus, the growth in China's clothing industry is anticipated to boost the market for acrylic fibers.

- Hence, all such market trends are expected to add to the demand for the acrylic fibers market in China during the forecast period.

Acrylic Fiber Industry Overview

The acrylic fiber market is consolidated in nature. Some of the major players in the market include Aksa Akrilik Kimya Sanayii AS, Dralon, Jilin Chemical Fiber Group Co., Ltd., Aditya Birla Management Corporation Pvt. Ltd, and Sinopec, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 High Demand for Use in Apparels

- 4.1.2 Online Purchasing Drive the Demand for End Use Products

- 4.2 Restraints

- 4.2.1 Availability of Substitutes, like Polyester

- 4.2.2 Stringent Regulations Worldwide on the Production of Acrylic Fiber

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Form

- 5.1.1 Staple

- 5.1.2 Filament

- 5.2 Blending

- 5.2.1 Wool

- 5.2.2 Cotton

- 5.2.3 Other Blendings (Cellulose)

- 5.3 Application

- 5.3.1 Apparel

- 5.3.2 Household Furnishing

- 5.3.3 Industrial

- 5.3.4 Other Applications (Upholstery)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Turkey

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aditya Birla Management Corporation Pvt. Ltd

- 6.4.2 Aksa Akrilik Kimya Sanayii AS

- 6.4.3 China Petrochemical Corporation

- 6.4.4 Dralon

- 6.4.5 FORMOSA PLASTIICS CORPORATIION

- 6.4.6 Goonvean Fibres

- 6.4.7 Indian Acrylics Limited

- 6.4.8 Japan Exlan Co. Ltd

- 6.4.9 Jiangsu Zhongxin Resources Group

- 6.4.10 Jilin Chemical Fiber Group Co. Ltd

- 6.4.11 Kaltex

- 6.4.12 KANEKA CORPORATION

- 6.4.13 Mitsubishi Chemical Corporation

- 6.4.14 Pasupati Acrylon Ltd

- 6.4.15 PetroChina Company Limited

- 6.4.16 Polyacryl Iran Corp.

- 6.4.17 Polymir

- 6.4.18 SDF

- 6.4.19 SGL Carbon

- 6.4.20 Taekwang Industrial Co. Ltd

- 6.4.21 TORAY INDUSTRIES INC.

- 6.4.22 Vardhman Acrylics Ltd

- 6.4.23 Yousuf Dewan Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Future Market for Acrylic Paper

丙烯酸纤维市场:按形状类型、织物类型、应用分类 - 2025-2030 年全球预测

丙烯酸纤维市场:按形状类型、织物类型、应用分类 - 2025-2030 年全球预测 腈纶短纤维市场:按染色方法、混纺、混纺类型和最终用途分类 - 全球预测 2025-2030

腈纶短纤维市场:按染色方法、混纺、混纺类型和最终用途分类 - 全球预测 2025-2030 全球丙烯酸纤维市场评估:依技术、形状、混合、最终用途产业、地区、机会、预测(2017-2031)

全球丙烯酸纤维市场评估:依技术、形状、混合、最终用途产业、地区、机会、预测(2017-2031) 腈纶纤维市场-2024年至2029年预测

腈纶纤维市场-2024年至2029年预测 丙烯酸纤维市场 - 按纤维类型(短纤维、丝束纤维)、按应用、按最终用途和 2032 年预测

丙烯酸纤维市场 - 按纤维类型(短纤维、丝束纤维)、按应用、按最终用途和 2032 年预测 丙烯纤维市场:趋势,机会,竞争分析【2023-2028年】

丙烯纤维市场:趋势,机会,竞争分析【2023-2028年】 丙烯纤维市场:各染色方法,各纤维形态,各混纺,各终端用户,各地区-规模,占有率,展望,机会分析,2023~2030年

丙烯纤维市场:各染色方法,各纤维形态,各混纺,各终端用户,各地区-规模,占有率,展望,机会分析,2023~2030年 短纤丙烯纤维的全球市场

短纤丙烯纤维的全球市场