|

市场调查报告书

商品编码

1640541

油漆和涂料添加剂:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Paints and Coatings Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

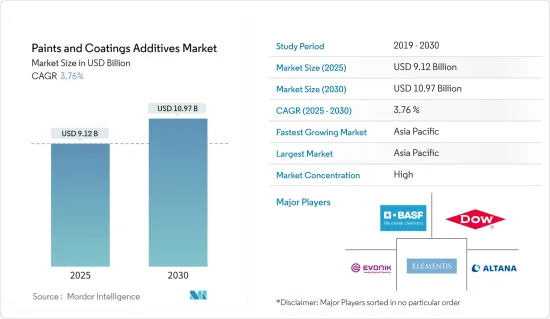

油漆和涂料添加剂市场规模预计在 2025 年为 91.2 亿美元,预计到 2030 年将达到 109.7 亿美元,预测期(2025-2030 年)的复合年增长率为 3.76%。

COVID-19 对 2020 年的油漆和涂料添加剂市场产生了负面影响。但随着主要终端用户产业復工,预计未来几年市场将稳定成长。

主要亮点

- 建筑涂料需求的增加是市场研究的主要驱动因素。

- 相反,预计日益严格的环境法规将阻碍市场成长。

- 各行业对流变改质剂的需求不断增加可能会提供机会。

- 亚太地区占全球市场主导地位,其中中国和印度的消费量最大。

油漆和涂料添加剂市场趋势

建筑业占据市场主导地位

- 建筑部门包括商业涂料中使用的添加剂,例如办公大楼、仓库、便利商店、购物中心和住宅。

- 建筑涂料中使用的主要助剂包括流变改质剂、消泡剂、分散剂和润湿剂。

- 一般来说,建筑涂料中使用的助剂有助于改善表面性能,稳定颜料,提高润湿性、分散性、消泡性等。

- 根据美国人口普查局的数据,2022 年 12 月美国新建设产值为 17,929 亿美元。 2023年3月,非住宅部门支出为9,971.4亿美元,年增18.8%。

- 此外,根据美国人口普查局的数据,2022 年 6 月私人和公共建筑住宅支出为 4,926.8 亿美元,较 2021 年 6 月的 4,842.6 亿美元增长 1.74%。因此,预计该国私人和公共非住宅建筑支出的增加将推动油漆和涂料添加剂市场的需求上升。

- 除此之外,美国也规划了各种商业建筑计划。红牛北美公司在北卡罗来纳州康科德拥有 200 万平方英尺的加工和配送设施,价值 7.4 亿美元;酪农合作社DareGold 在华盛顿州帕斯科港拥有40 万平方英尺的加工厂,价值5 亿美元。

- 沙乌地阿拉伯住宅投资的增加预计将推动油漆和涂料添加剂市场的需求。例如,在沙乌地阿拉伯,房地产开发项目数量的增加、住宅需求的不断增长以及政府发展社会经济基础设施的倡议正在推动该国的油漆和涂料添加剂市场的发展。根据沙乌地阿拉伯住宅部长马吉德·霍盖尔介绍,沙乌地阿拉伯王国计划在未来五年内建造 30 万套住宅。住宅是沙乌地阿拉伯「2030愿景」下的重点倡议之一。未来几年,该国的建筑业可能会对油漆和涂料添加剂市场产生需求。

- 政府的这些措施可望迅速振兴建设产业。这也进一步促进了建筑业的涂料和涂料添加剂的消费。

- 因此,此类住宅建设投资和计划,以及住宅建设中使用的油漆和被覆剂的消费,正在推动这些国家的建设活动。

亚太地区占市场主导地位

- 亚太地区正在寻求发展油漆和涂料行业。凭藉其对关键原材料、基本分子生产和区域市场的便捷获取,该公司预计将成为全球油漆和被覆剂供应链的核心。

- 亚太地区正在不懈地追求建造最高、最大、最宏伟的建筑。预计未来几年该国的油漆和涂料行业将实现稳步成长。预计未来几年建设产业将出现强劲成长,推动对涂料添加剂的需求。

- 在油漆和涂料添加剂市场,中国占亚太地区最大的份额。由于该国投资和建设活动的增加,预计整个预测期内对油漆和涂料添加剂市场的需求将会增加。中国近年来是全球基础设施主要投资者之一,并做出了重要贡献。例如,根据中国国家统计局的数据,2022年中国建筑业产值预计将达到人民币31.2兆元(4,758.4亿美元),比2021年成长6.5%。

- 此外,根据中国住宅及城乡建设部的数据,到2025年建设业占GDP的比重将维持在6%。在该国,预製建筑的趋势正在增长,预计预製建筑将占新建筑的 30% 以上。

- 据国家发展和改革委员会称,中国政府已核准26 个基础设施计划,预计投资约 1,420 亿美元,预计将于 2023 年完工。预计住宅需求的增加将刺激公共和私营部门的住宅建设。因此,预计住宅投资的增加将推动该国建设产业对油漆和涂料添加剂市场的需求。

- 预计印度仍将是亚太地区二十国集团中成长最快的经济体。印度政府宣布,2023-2025年三年期间的基础设施投资目标为3,765亿美元。其中包括投资1,205亿美元发展27个产业丛集,投资753亿美元用于公路、铁路和港口连通计划。因此,该国的建设产业可能会为油漆和涂料添加剂带来福音。

- 此外,据 IBEF 称,在 2022-2023 年联邦预算中,政府已拨款 10 兆印度卢比(1,305.7 亿美元)用于加强基础设施部门。此外,印度计划未来五年透过其国家基础设施管道投资 1.4 兆美元用于基础建设。

- 民航部长进一步宣布,印度政府计画在2032年建造100座机场。

- 由于上述因素,预计亚太地区将在预测期内占据全球主导地位。

油漆和涂料添加剂行业概况

油漆和涂料添加剂市场因其性质而部分整合。该市场的主要企业(不分先后顺序)包括陶氏化学、BASF欧洲公司、阿尔塔纳集团 (BYK)、赢创工业股份公司和 Elementis PLC。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 建筑涂料需求不断成长

- 各行业对流变改质剂的需求不断增加

- 其他驱动因素

- 限制因素

- 日益严格的环境法规

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第 5 章 市场区隔(以金额为准的市场规模)

- 按类型

- 除生物剂

- 分散剂和润湿剂

- 消泡剂和消泡剂

- 流变改性剂

- 表面改质剂

- 稳定剂

- 流动和流平添加剂

- 其他类型

- 按应用

- 建筑油漆和涂料

- 木器漆

- 交通运输涂料

- 防护漆

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- AGC Inc.

- ALTANA AG

- Arkema

- Ashland

- BASF SE

- Cabot Corporation

- DAIKIN INDUSTRIES, Ltd.

- Dow

- Dynea AS

- Eastman Chemical Company

- ELEMENTIS PLC

- Evonik Industries AG

- K-TECH(INDIA)LIMITED

- Momentive

- Nouryon

- Solvay

- The Lubrizol Corporation

第七章 市场机会与未来趋势

- 趋势转向水性涂料

- 其他机会

The Paints and Coatings Additives Market size is estimated at USD 9.12 billion in 2025, and is expected to reach USD 10.97 billion by 2030, at a CAGR of 3.76% during the forecast period (2025-2030).

COVID-19 negatively impacted the market for paints and coatings additives in 2020. However, with the resumption of work in major end-user industries, the market is estimated to grow steadily in the coming years.

Key Highlights

- The increased demand for architectural coatings is the major factor driving the market studied.

- Conversely, rising environmental regulations are expected to hinder market growth.

- Increasing demand for rheology modifiers in various industries will likely be an opportunity.

- Asia-Pacific dominated the global market, with the largest consumption in China and India.

Paints and Coatings Additives Market Trends

Architectural Segment to Dominate the Market

- The architectural segment includes additives used in coatings for commercial purposes, such as office buildings, warehouses, retail convenience stores, shopping malls, and residential buildings.

- Some majorly used additives for architectural coatings include rheological modifiers, defoamers, dispersants, and wetting agents.

- Generally, the additives used for architectural coatings help to enhance surface properties, stabilizing pigment, enhancing wetting, dispersing, and defoaming properties, etc.

- According to the US Census Bureau, the value of new construction output in the United States amounted to USD 1,792.9 billion in December 2022. The non-residential sector accounted for USD 997.14 billion in March 2023, registering a growth of 18.8% compared to the same period of the previous year.

- Moreover, according to the US Census Bureau, the private and public construction non-residential spending in June 2022 was 492.68 billion, which showed an increase of 1.74% compared to June 2021, which amounted to USD 484.26 billion. Therefore, increasing spending on private and public non-residential constructions in the country is expected to create an upside demand for the paints and coatings additives market.

- Apart from that, there are various construction commercial projects scheduled in the United States Red Bull North America's USD 740 million worth 2 million sq ft processing and distribution facility in Concord, North Carolina, Dairy cooperative DairgoldUSD 500 million worth 400,000 sq ft processing facility in Port of Pasco, Washington (completion scheduled for 2023), Biotics Research Corporation USD 9 million worth 88,000 sq ft warehouse, laboratory, and office facility in Rosenberg, Texas (completion scheduled for 2023).

- Increasing investment in residential constructions in Saudi Arabia is expected to boost the demand for the paints and coatings additives market. For instance, in Saudi Arabia, the growing number of real estate developments, increasing demand for residential property, and governmental initiatives to develop socio-economic infrastructure drive the country's paints and coatings additives market. According to Majid Al-Hogail, the Saudi Housing Minister, the Kingdom of Saudi Arabia plans to construct 300,000 extra housing units over the next five years. One of Saudi Arabia's significant initiatives under Vision 2030 is housing. It will likely create demand for the paints and coatings additives market from the country's construction sector in the upcoming years.

- Such initiatives by the government are expected to rapidly boost the construction industry. It is also further boosting the consumption of coating and, in turn, coating additives in the construction sector.

- Hence, all such residential construction investments and projects are driving construction activities in these countries, along with the consumption of paints and coatings for application in residential construction.

Asia-Pacific to Dominate the Market

- Asia-Pacific is aiming for the development of its paints and coatings sector. It is on the way to becoming the center of the global paints and coatings supply chain, leveraging its easy access to key feedstock, production of basic molecules, and access to the regional market.

- Asia-Pacific includes a persistent expedition in making some of the tallest, largest, and biggest structures. The paints and coatings industry in the country is expected to register steady growth in the coming years. The construction industry is poised to witness sturdy growth in the forthcoming years, augmenting the demand for coating additives.

- China holds the largest Asia-Pacific market share for the paints and coatings additives market. The demand for the paints and coatings additives market is expected to rise throughout the forecast period due to rising investments and construction activity in the country. China is a huge contributor, as it is one of the leading investors in infrastructure worldwide over the past few years. For instance, according to the National Bureau of Statistics (NBS) of China, in 2022, the output value of construction works in China amounted to CNY 31.2 trillion (USD 475.84 billion), an increase of 6.5% compared with 2021.

- Moreover, in China, according to the country's Ministry of Housing and Urban-Rural Development, the construction industry will maintain a 6% share of the country's GDP by 2025. There is a growing trend in the country for prefabricated buildings, which is expected to account for more than 30% of the country's new construction.

- According to the National Development and Reform Commission, the Chinese government approved 26 infrastructure projects at an estimated investment of about USD 142 billion, estimated to be completed by 2023. The growing demand for housing is expected to drive residential construction in the public and private sectors. Therefore, increasing investments in residential construction is expected to create an upside demand for the paints and coatings additives market from the country's construction industry.

- India is anticipated to remain the fastest-growing G20 economy in the Asia-Pacific region. The Indian government announced a target of USD 376.5 billion in infrastructure investment over three years (2023-2025). It includes USD 120.5 billion for developing 27 industrial clusters and USD 75.3 billion for road, railway, and port connectivity projects. Therefore, this will likely create an upside for paints and coatings additives from the country's construction industry.

- Moreover, according to IBEF, in Union Budget 2022-2023, the government allocated INR 10 trillion (USD 130.57 billion) to enhance the infrastructure sector. Moreover, India plans to spend USD 1.4 trillion on infrastructure through the 'National Infrastructure Pipeline' in the next five years.

- Furthermore, the civil aviation minister announced that the Indian government is also planning to construct 100 airports by 2032, owing to increasing demand for air commutes.

- The factors above are expected to make the Asia-Pacific the dominant globally during the forecast period.

Paints and Coatings Additives Industry Overview

The Paints and Coatings Additives Market is partially consolidated in nature. The major players in this market (not in a particular order) include Dow, BASF SE, Altana Group (BYK), Evonik Industries AG, and Elementis PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increased Demand for Architectural Coatings

- 4.1.2 Increasing Demand for Rheology Modifiers in Various Industries

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Rising Environmental Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Biocides

- 5.1.2 Dispersants and Wetting Agents

- 5.1.3 Defoamers and Deaerators

- 5.1.4 Rheology Modifiers

- 5.1.5 Surface Modifiers

- 5.1.6 Stabilizers

- 5.1.7 Flow and Leveling Additives

- 5.1.8 Other Types

- 5.2 Application

- 5.2.1 Architectural Paints and Coatings

- 5.2.2 Wood Paints and Coatings

- 5.2.3 Transportation Paints and Coatings

- 5.2.4 Protective Paints and Coatings

- 5.2.5 Others Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGC Inc.

- 6.4.2 ALTANA AG

- 6.4.3 Arkema

- 6.4.4 Ashland

- 6.4.5 BASF SE

- 6.4.6 Cabot Corporation

- 6.4.7 DAIKIN INDUSTRIES, Ltd.

- 6.4.8 Dow

- 6.4.9 Dynea AS

- 6.4.10 Eastman Chemical Company

- 6.4.11 ELEMENTIS PLC

- 6.4.12 Evonik Industries AG

- 6.4.13 K-TECH (INDIA) LIMITED

- 6.4.14 Momentive

- 6.4.15 Nouryon

- 6.4.16 Solvay

- 6.4.17 The Lubrizol Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Trends Towards Water Coatings

- 7.2 Other Opportunities

环保涂料添加剂市场分析与预测(至2035年):类型、产品、应用、技术、最终用户、成分、形态、材料类型、工艺

环保涂料添加剂市场分析与预测(至2035年):类型、产品、应用、技术、最终用户、成分、形态、材料类型、工艺 全球磺酸盐酸市场依等级、应用、终端用户产业及通路划分,预测至2026-2032年

全球磺酸盐酸市场依等级、应用、终端用户产业及通路划分,预测至2026-2032年 挥发性有机化合物 (VOC) 市场规模、份额和成长分析(按化合物类型、应用、最终用途和地区划分)—2026-2033 年行业预测

挥发性有机化合物 (VOC) 市场规模、份额和成长分析(按化合物类型、应用、最终用途和地区划分)—2026-2033 年行业预测 消泡剂涂料添加剂市场规模、份额和成长分析(按消泡剂类型、应用和地区划分)-2026-2033年产业预测2025-2032年全球消泡涂料添加剂市场(按原始材料类型、形式和最终用途)预测包装涂料添加剂市场按形态、涂层技术、应用和最终用途划分-全球预测,2025-2032年涂料添加剂市场(按树脂类型、形态、添加剂类型、应用和最终用途产业划分)-2025-2032年全球预测

消泡剂涂料添加剂市场规模、份额和成长分析(按消泡剂类型、应用和地区划分)-2026-2033年产业预测2025-2032年全球消泡涂料添加剂市场(按原始材料类型、形式和最终用途)预测包装涂料添加剂市场按形态、涂层技术、应用和最终用途划分-全球预测,2025-2032年涂料添加剂市场(按树脂类型、形态、添加剂类型、应用和最终用途产业划分)-2025-2032年全球预测 涂料助剂市场报告:趋势、预测与竞争分析(至2031年)黏合剂涂层市场,按技术、按产品、按应用、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

涂料助剂市场报告:趋势、预测与竞争分析(至2031年)黏合剂涂层市场,按技术、按产品、按应用、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测 黏剂涂料的全球市场规模:各技术,各产品,各用途,各地区,范围及预测

黏剂涂料的全球市场规模:各技术,各产品,各用途,各地区,范围及预测