|

市场调查报告书

商品编码

1444236

苯乙烯-市场占有率分析、产业趋势与统计、成长预测(2024-2029)Styrene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

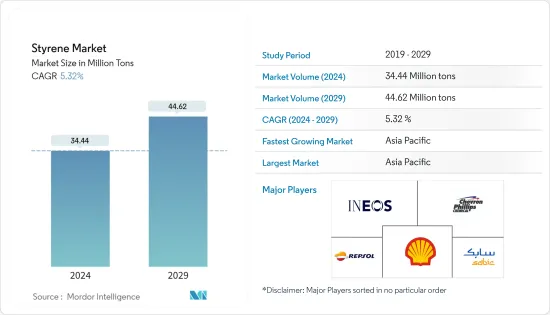

预计2024年苯乙烯市场规模为3,444万吨,预计2029年将达到4,462万吨,在预测期间(2024-2029年)复合年增长率为5.32%。

COVID-19大流行对苯乙烯市场产生了负面影响。然而,由于包装、建筑、汽车等各行业的消费增加,2021年市场显着復苏。

主要亮点

- 短期来看,消费性电器产品产业需求的成长是推动所研究市场成长的关键因素。

- 然而,包装行业中生物基塑胶的使用增加可能会限制市场成长。

- 儘管如此,正在进行的生物基聚苯乙烯研究可能很快就会为全球市场创造利润丰厚的成长机会。

- 亚太地区主导苯乙烯市场,最大消费国包括中国、日本和东南亚国协。

苯乙烯市场趋势

包装产业引领市场

- 苯乙烯由于其优越的性能而常用于包装行业。一种多功能轻质塑料,具有优异的透明度、抗衝击性和绝缘性能。这些特性使其适用于广泛的包装应用。

- 苯乙烯在包装产业最常见的用途之一是生产聚苯乙烯泡沫,通常称为发泡聚苯乙烯 (EPS) 或发泡聚苯乙烯。 EPS 泡棉广泛用于保护性包装,如缓衝材料、生鲜产品的隔热材料和轻型运输容器。

- 苯乙烯也用于製造硬质聚苯乙烯,通常用于食品包装。透明聚苯乙烯容器(例如翻盖式容器、杯子和托盘)在外食行业中很受欢迎,因为它们的透明度使顾客可以轻鬆看到里面的东西。

- 此外,聚苯乙烯也用于医疗和保健行业的各种包装应用。 IQVIA显示,全球医药市场近年来成长显着。到 2022 年,全球医药市场总额预计将达到 1.48 兆美元。这仅比 2021 年的市场规模估计为 1.42 兆美元略有增加。

- 在亚太地区,由于生活方式的改变、人们可支配收入的增加、专业人士数量的增加以及对快餐的日益偏好,对加工食品的偏好正在增加。

- 由于国内电商收入上升等因素,中国已成为全球最大的包装材料消费国。据印度塑胶工业协会称,印度包装工业位居世界第五,每年以22-25%左右的速度成长。由于高技术纯熟劳工和低廉的人事费用,食品包装和加工成本可比欧洲低40%。人口的增长和对包装的需求的增加预计将推动市场的发展。

- 同样,到2022年,欧洲食品和饮料业将僱用460万人,创造收益11,590亿美元,付加价值2,300亿欧元(2,423.7亿美元),成为欧洲最大的製造业之一。欧洲。由于该地区食品和饮料行业的成长,导致对食品包装的需求增加,扩大了所覆盖的市场。

- 根据联邦统计局统计,2022年德国包装产业收益达350.4亿欧元(377.1亿美元),较前一年成长。

- 这些因素被认为支持了所研究市场的包装领域的需求。

预计亚太地区将主导市场

- 亚太地区在市场上占据主导地位,并可能在预测期内继续保持主导地位。

- 全部区域包装应用的增加、对电气和电子产品的强劲需求以及汽车和运输行业的快速成长正在积极推动苯乙烯市场的发展。

- 据ZEVI称,2021年亚洲电子市场规模达3.11兆欧元(3.67兆美元),成长10%。预计 2022 年需求将成长 13%,2023 年将成长 7%。中国的市场是全世界最大的,比所有已开发国家的总和还要重要。 2021年,中国市场贡献了2.7兆美元(2.45兆美元),占全球市场的41.6%。此外,中国电子产业到2022年将成长14%,预计到2023年将成长8%。

- 根据中国工业协会统计,中国拥有全球最大的汽车生产基地,2022年汽车产量将达2,700万辆,比去年的2,600万辆成长3.4%。

- 中国是世界主要包装工业之一。由于客製化包装的兴起和食品业对包装消费品的需求不断增加,预计该国在预测期内将持续成长。根据Interpack预测,2023年中国食品包装产业包装总数预计将达到4,470亿件。

- 据行业出版物称,总合超过350万吨的聚苯乙烯和ABS塑料新工厂将于2021-2022年投产,其中包括中石化古雷、浙江石化和山东利华亚等公司的新设施。那然而,由于国内能源危机,可能会出现延误。

- 同样,根据印度包装工业协会(PIAI)的数据,印度包装行业在预测期内预计将以 22% 的速度成长。此外,预计到2025年,印度包装市场将达到2,048.1亿美元,2020年至2025年的复合年增长率为26.7%。因此,该地区的塑胶射出成型市场预计将成长。

- 就电子领域而言,根据电子情报技术产业协会(JEITA)预测,2022年全球电子资讯科技产业产值预估为3.44兆美元,较2017年的3.36兆美元与前一年同期比较,成长率为2021年将达1兆美元。

- 因此,上述因素显示该地区各终端用户对苯乙烯的需求不断增加。

苯乙烯产业概况

所研究的市场在主要企业中部分分散。主要企业包括(排名不分先后)壳牌公司、雪佛龙菲利普斯化学公司、SABIC、雷普索尔和英力士。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 消费性电器产品产业需求不断成长

- 包装产业需求增加

- 其他司机

- 抑制因素

- 包装行业越来越多地使用生物基塑料

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章市场区隔(市场规模)

- 产品类别

- 聚苯乙烯

- 丙烯腈 丁二烯 苯乙烯

- 苯乙烯-丁二烯橡胶

- 其他产品种类(苯乙烯-丙烯腈)

- 最终用户产业

- 包装

- 建造

- 消费品

- 汽车和交通

- 电气和电子

- 其他最终用户产业(纺织)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 南非

- 沙乌地阿拉伯

- 其他中东/非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业采取的策略

- 公司简介

- Chevron Phillips Chemical Company

- Covestro AG

- Hanwha Group

- INEOS(INEOS Styrolution)

- LG Chem

- LyondellBasell Industries Holdings BV

- Reliance Industries Ltd

- Repsol

- SABIC

- Shell PLC

- Versalis SpA(Eni SpA)

第七章市场机会与未来趋势

- 持续研究开发生物基聚苯乙烯

- 其他机会

The Styrene Market size is estimated at 34.44 Million tons in 2024, and is expected to reach 44.62 Million tons by 2029, growing at a CAGR of 5.32% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the styrene market. However, the market recovered significantly in 2021, owing to rising consumption of various industries, such as packaging, construction, automotive, and others.

Key Highlights

- Over the short term, the growing demand from the consumer electronics industry is a major factor driving the growth of the market studied.

- However, increasing usage of bio-based plastics in the packaging industry is likely to restrain the growth of the market.

- Nevertheless, ongoing research to develop bio-based polystyrene is likely to create lucrative growth opportunities for the global market soon.

- The Asia-Pacific region dominates the styrene market, with the largest consumption coming from countries such as China, Japan, ASEAN countries, etc.

Styrene Market Trends

Packaging Industry to Drive the Market

- Styrene is commonly used in the packaging industry due to its favorable properties. It is a versatile, lightweight plastic with excellent clarity, impact resistance, and thermal insulation. These characteristics make it suitable for a wide range of packaging applications.

- One of the most common uses of styrene in the packaging industry is in producing polystyrene foam, often referred to as expanded polystyrene (EPS) or Styrofoam. EPS foam is widely used for protective packaging, including cushioning materials, insulation for perishable goods, and lightweight shipping containers.

- Styrene is also used to produce rigid polystyrene, which is commonly employed in food packaging. Clear polystyrene containers, such as clamshells, cups, and trays, are popular in the food service industry due to their transparency, allowing customers to view the contents easily.

- Furthermore, polystyrene is also used in the medical and healthcare industries for various packaging applications; IQVIA shows that the global pharmaceutical market has grown significantly in recent years. The total global pharmaceutical market was valued at USD 1.48 trillion by 2022. This is only a slight increase from 2021 when the market was valued at USD 1.42 trillion.

- In Asia-Pacific, the demand for packaged food is growing, owing to lifestyle changes, the growing disposable income of people, the increasing number of working professionals, and the growing preference for fast food.

- China is the world's largest packaging consumer across the world owing to the factors such as growing per capita income, coupled with rising e-commerce giants in the country. India's packaging industry is the fifth-largest in the world, and it is growing at about 22-25% per year, as per the Plastics Industry Association of India. Packaging and processing food costs can be 40% lower than in Europe because of highly skilled labor and cheap labor costs. The growing population and increasing demand for packaging are expected to drive the market.

- Similarly, in 2022, the Europe food and beverages industry employs 4.6 million people and generates EUR 1.1 trillion (USD 1.159 trillion) in revenue and EUR 230 billion (USD 242.37 billion) in value-added, making it one of the largest manufacturing industries in Europe. Thereby, the growing food and beverages industry in the region is increasing the demand for food packaging, as well as boosting the market studied.

- According to Statistisches Bundesamt, the revenue of the packaging industry in Germany has reached EUR 35.04 billion (USD 37.71 billion) in 2022 and has registered growth when compared to previous years.

- Such factors are likely to support the demand for the studied market from the packaging segment.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific dominated the market and will likely continue its dominance during the forecast period.

- Increasing packaging applications across the region, robust demand for electrical and electronic products, and the rapid growth of automotive and transportation sectors are actively boosting the styrene market.

- According to ZEVI, the Asian electro market reached EUR 3.11 trillion (USD 3.67 trillion) in 2021, a 10% rise. The demand increased by 13% in 2022 and estimated a 7% growth rate for 2023. China's market is the largest in the world, even more significant than the combined markets of all industrialized countries. In 2021, the Chinese market contributed EUR 2.07 trillion (USD 2.45 trillion), or 41.6% of the world market; additionally, the Chinese electronic industry expanded by 14% in 2022, and the sector is expected to grow by 8% in 2023.

- According to the China Association of Automobile Manufacturers (CAAM), China has the largest automotive production base in the world, with a total vehicle production of 27 million units in 2022, registering an increase of 3.4 % compared to 26 million units produced last year.

- China is one of the key packaging industries in the world. The country is expected to witness consistent growth during the forecast period due to the rise of customized packaging and increased demand for packaged consumer goods in the food segment. According to Interpak, in China, in the foodstuff packaging category, total packaging is expected to reach 447 billion units in 2023.

- According to industry publications, in 2021-2022, new factories for polystyrene and ABS plastics were expected to launch with a combined capacity of over 3.5 million tons, including new facilities for companies like Sinopec Gulei, Zhejiang Petrochemical, and Shandong Lihuaya. However, a delay may be observed due to the energy crisis in the country.

- Similarly, according to the Packaging Industry Association of India (PIAI), the Indian packaging industry is expected to grow at a rate of 22% during the forecast period. Moreover, the Indian packaging market is expected to reach USD 204.81 billion by 2025, registering a CAGR of 26.7% between 2020 and 2025. Therefore, the plastic injection molding market is expected to grow in the region.

- Considering electronics, according to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3.44 trillion in 2022, registering a growth rate of 1% year on year, compared to USD 3.36 trillion in 2021.

- Thus, the abovementioned factors indicate the rising demand for styrene from various end users in the region.

Styrene Industry Overview

The market studied is partially fragmented among the top players. The key players (not in any particular order) include Shell PLC, Chevron Phillips Chemical Company LLC, SABIC, Repsol, and INEOS, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand from the Consumer Electronics Industry

- 4.1.2 Increasing Demand from Packaging Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Usage of Bio-based Plastics in the Packaging Industry

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Polystyrene

- 5.1.2 Acrylonitrile Butadiene Styrene

- 5.1.3 Styrene Butadiene Rubber

- 5.1.4 Other Product Types (Styrene-Acrylonitrile)

- 5.2 End-user Industry

- 5.2.1 Packaging

- 5.2.2 Construction

- 5.2.3 Consumer Goods

- 5.2.4 Automotive and Transportation

- 5.2.5 Electrical and Electronics

- 5.2.6 Other End-user Industries (Textile)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chevron Phillips Chemical Company

- 6.4.2 Covestro AG

- 6.4.3 Hanwha Group

- 6.4.4 INEOS (INEOS Styrolution)

- 6.4.5 LG Chem

- 6.4.6 LyondellBasell Industries Holdings BV

- 6.4.7 Reliance Industries Ltd

- 6.4.8 Repsol

- 6.4.9 SABIC

- 6.4.10 Shell PLC

- 6.4.11 Versalis SpA (Eni SpA)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ongoing Research to Develop Bio-based Polystyrene

- 7.2 Other Opportunities

苯乙烯、乙烯、丁烯、苯乙烯(SEBS):市场占有率分析、产业趋势/统计、成长预测(2024-2029)

苯乙烯、乙烯、丁烯、苯乙烯(SEBS):市场占有率分析、产业趋势/统计、成长预测(2024-2029) 苯乙烯市场依产品种类(聚苯乙烯、丙烯腈丁二烯苯乙烯、苯乙烯丙烯腈、丁苯橡胶等)、最终用户(包装、建筑、消费品、汽车等)及区域 2024-2032

苯乙烯市场依产品种类(聚苯乙烯、丙烯腈丁二烯苯乙烯、苯乙烯丙烯腈、丁苯橡胶等)、最终用户(包装、建筑、消费品、汽车等)及区域 2024-2032 苯乙烯 - 石化产品全球市场报告 2024

苯乙烯 - 石化产品全球市场报告 2024 全球苯乙烯市场:工厂产能、产量、工艺、技术、利用率、需求和供应、最终用途、对外贸易、销售渠道、区域需求、公司份额(2015-2030 年)

全球苯乙烯市场:工厂产能、产量、工艺、技术、利用率、需求和供应、最终用途、对外贸易、销售渠道、区域需求、公司份额(2015-2030 年) 苯乙烯异戊二烯苯乙烯(SIS)的全球市场(2016年~2032年)

苯乙烯异戊二烯苯乙烯(SIS)的全球市场(2016年~2032年) 苯乙烯的全球市场报告 2023年

苯乙烯的全球市场报告 2023年 Alpha甲基苯乙烯(AMS)的全球市场(2016年~2032年)

Alpha甲基苯乙烯(AMS)的全球市场(2016年~2032年)