|

市场调查报告书

商品编码

1444405

石油和天然气 EPC:市场占有率分析、行业趋势和统计、成长预测(2024-2029 年)Oil & Gas EPC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

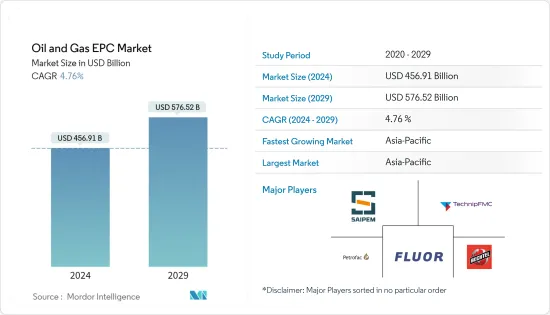

石油和天然气EPC市场规模预计2024年为4569.1亿美元,预计到2029年将达到5765.2亿美元,在预测期内(2024-2029年)增长4.76%,复合年增长率增长。

主要亮点

- 从中期来看,石油和天然气需求的成长以及天然气消费量的增加将产生天然气基础设施发展的需求,预计海上石油和天然气探勘和生产(E&P)活动也将增加。

- 另一方面,油气价格的大幅波动是油气EPC市场的主要限制因素之一。

- 儘管如此,预计在预测期内,各国新油气天然气田的发现将为上游、中游和下游所有产业的油气EPC市场创造充足的机会。

- 亚太地区主导市场,并可能在预测期内显着成长。这一增长归因于天然气需求的增加以及即将建成的液化天然气设施,从而创造了对 EPC 服务的巨大需求。

石油和天然气EPC市场趋势

上游领域预计将主导市场

- 上游油气产业的EPC包括陆上和海上探勘和生产相关服务。传统上,陆上EPC总投资高于离岸板块,主要是因为它比离岸板块投资要求更低、复杂性更小、场地更容易到达、风险更低。然而,由于陆上产业的成熟,过去十年对离岸产业的投资有所增加。

- 海上海洋工程(包括固定平台、浮体式式生产储油装运装置、浅水、深水、超深水浮体式式生产设施的设计、製造、安装、试运行和启动等设备)的EPC服务正在取得进展牵引力。

- 当涉及海上结构的 EPC 时,重要的是确定和评估海上设施的开发方案,无论是基于固定结构还是浮体结构。浅水固定平台的EPC服务包括导管架、三脚架、整体上部设施、压缩平台等的建造和部署,以确保固定平台稳定且能抵抗风和水的运动。我保证是的。深水浮体平台服务通常包括建造和部署半潜式平台的船体和甲板、FPSO 的模组和转塔、锚碇系统和浮标。

- 浮动平台通常无需铺设从生产设施到陆上码头的昂贵的远距管道。浮体式平台在小型油田中也很经济,因为固定石油平台和管道的安装成本太高。当油田耗尽时,FPSO可以移动到新位置并使用,而不是退役固定平台。

- 根据BP《2023年世界能源统计年鑑》显示,2022年全球原油产量约44亿吨。这一数字在 2018 年达到顶峰,当时全球石油产量达到约 45 亿吨。原油产量与前一年同期比较增长约4.2%。

- 在非洲,营运商签署了许多新的探勘和生产合约。例如,2022年1月,义大利石油天然气公司埃尼公司在埃及签署了5个区块的探勘合约。矿区位于东地中海、西部沙漠和苏伊士湾。该国其他公司已就东部和西部沙漠签署了七项石油和天然气生产协议。

- 这些发展预计将导致未来油气EPC市场的快速发展。

预计亚太地区将主导市场

- 亚洲国家的高都市化导致能源需求增加,导致该地区石油和天然气产量较高。中国等国家的存在是该地区EPC市场成长的主要动力。

- 中国是亚太地区最大的原油和天然气生产国。 2020年,该国天然气产量约占全国的30%。该国正在规划进一步的上游和中游计划,以实现该国天然气供需平衡。中国工业和商业领域对天然气的需求正在迅速增长。

- 许多公司都有陆地和海上探勘和生产活动的蓝图。 2021年2月,中海油宣布计画加速天然气探勘开发,包括南海深海蕴藏量和中国陆地非传统资源。该公司计划在 2021 年投资约 139.3 亿美元至 154.8 亿美元,到 2025 年将其投资组合的 30% 製成天然气,到 2035 年将 50% 製成天然气。

- 印度是亚太地区第二大原油生产国。根据英国石油公司《2023年世界能源统计年鑑》显示,2022年印度占该地区原油产量的9.5%。印度拥有石油和天然气基础设施,但印度的石油和天然气工业拥有各种设施。 、钻机、生产平台、炼油厂、管线、码头等。

- 截至 2022 年 6 月,印度拥有 77 座运作中钻机。由于油田老化和缺乏重大发现,该国的石油产量近十年来一直在下降。国营和私营公司都在製定投资计划,以提高老油田的采收率。

- 例如,2022年4月,印度石油公司(IOCL)宣布计画投资1,020亿美元用于石油、石油和润滑油(POL)储存能力,包括在东北地区建立待开发区设施。

- 由于这些发展,未来几年该地区的石油和天然气 EPC 市场可能会显着成长。

石油和天然气EPC行业概况

石油和天然气EPC市场较为分散。市场主要企业包括(排名不分先后)Saipem SpA、TechnipFmc PLC、Petrofac Limited、Fluor Corporation 和 Bechtel Corporation。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 调查先决条件

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 2028 年之前的市场规模与需求预测(美元)

- 最新趋势和发展

- 政府政策法规

- 市场动态

- 促进因素

- 天然气基础设施发展需求不断成长

- 海上石油和天然气探勘和生产 (E&P) 活动增加

- 抑制因素

- 石油和天然气价格波动较大

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 部门

- 上游

- 下游

- 中产阶级

- 地区:2028 年之前的地区市场分析、市场规模和需求预测(仅限地区)

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲

- 北美洲

第六章 竞争形势

- 併购、合资、合作与协议

- 主要企业采取的策略

- 公司简介

- National Petroleum Construction Company

- Petrofac Limited

- Tecnicas Reunidas SA

- Daewoo Engineering &Construction Co. Ltd

- Fluor Corporation

- Samsung Engineering Co. Ltd

- Korea Shipbuilding &Offshore Engineering Co. Ltd

- Hyundai Engineering &Construction Co. Ltd

- John Wood Group PLC

- TechnipFMC PLC

- Bechtel Corporation

- Saipem SpA

- McDermott International Ltd

- KBR Inc.

- Sinopec Engineering(Group)Co. Ltd

第七章市场机会与未来趋势

- 世界各地发现新油气天然气田

简介目录

Product Code: 57107

The Oil & Gas EPC Market size is estimated at USD 456.91 billion in 2024, and is expected to reach USD 576.52 billion by 2029, growing at a CAGR of 4.76% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, the growing demand for oil & gas and the rising consumption of natural gas, which is creating a need to develop the natural gas infrastructure, and an increase in offshore oil and gas exploration and production (E&P) activities are also expected to drive the growth of the market studied.

- On the other hand, the high volatility of oil and gas prices is one of the major restraints for the oil and gas EPC market.

- Nevertheless, the discovry of new oil and gas fields in various countries are exoected to create ample opportunities for the oil and gas EPC market for all the upstream, midstream, and downstream sectors during the forecast period.

- The Asia-Pacific region dominates the market and is also likely to witness significant growth during the forecast period. This growth is attributed to the increasing demand for natural gas and upcoming LNG facilities resulting in massive demand for EPC services.

Oil and Gas EPC Market Trends

Upstream Segment Expected to Dominate the Market

- The EPC in the upstream oil and gas sector includes onshore and offshore exploration and production-related services. Traditionally, the total investments in onshore EPC are more than that of the offshore segment, mainly due to lower investment requirements, lesser complexity, more accessible sites, and lower risk than the offshore segment. However, investment in the offshore segment has risen during the last decade due to maturing onshore fields.

- The EPC services for offshore, such as installations, including design, fabrication, installation, commissioning, and start-up of a fixed platform, floating production storage and offloading (FPSO) units, and floating production facilities for shallow, deep water, and ultradeep waters, are gaining traction.

- Concerning the EPC for offshore structures, identifying and assessing development options for offshore facilities, whether based on fixed or floating structures, is crucial. The EPC services for fixed platforms used for shallow waters include constructing and deploying jackets, tripods, integrated topsides, compression platforms, etc., to ensure that fixed platforms are stable and resilient to wind and water movements. The floating platform services, generally for deepwater, include constructing and deploying hulls and decks for semi-submersible platforms, modules and turrets for FPSOs, and mooring systems and buoys.

- Floating platforms generally eliminate the need for laying expensive long-distance pipelines from the production facility to an onshore terminal. Floating platforms are also economical in smaller oil fields, where the expense of installing a fixed oil platform and pipeline is too high. Once the field is depleted, FPSOs may be moved and used at a new location instead of decommissioning a fixed platform.

- According to BP Statistical Review of World Energy 2023, in 2022, global crude oil production amounted to about 4.4 billion metric tons. The figure peaked in 2018 when oil production worldwide reached nearly 4.5 billion metric tons. The crude oil production witness about 4.2% growth compared to previous year.

- In Africa, the operators have signed many new exploration and production contracts. For example, in January 2022, Eni, the Italy-based oil and gas company, clinched an exploration contract in five blocks in Egypt. The blocks are located in the Eastern Mediterranean Sea, Western Desert, and Gulf of Suez. Seven oil and gas production agreements were signed for the Eastern and Western deserts by other companies in the country.

- Such developments are likely to propel the oil and gas EPC market rapidly in the future.

Asia-Pacific Expected to Dominate the Market

- The growing energy demand due to the high urbanization rate in Asian countries has led to the region's high oil and gas production rate. The presence of countries like China is the main driver of the region's EPC market's growth.

- China is the largest crude oil and natural gas producer in Asia-Pacifi. In 2020, the country accounted for around 30% of the total natural gas production. The country has planned even more upstream and midstream projects to achieve an equilibrium in the demand-supply situation of natural gas in the country. China has witnessed an upsurge in the natural gas demand in both the industrial and commercial sectors.

- Many companies have blueprints for exploration and production activities onshore and offshore. In February 2021, CNOOC Ltd stated its plans to accelerate the exploration and development of natural gas, including deepwater reserves in the South China Sea and unconventional resources onshore in China. The company planned a capital spending of around USD 13.93-USD 15.48 billion in 2021 to make gas part of 30% of its portfolio by 2025 and 50% by 2035.

- India is the second-largest crude oil producer in the Asia-Pacific region. It accounted for 9.5% of the regional crude oil production in 2022, according to the BP Statistical Review of World Energy 2023. Although the country has a relatively less complex and new oil and gas infrastructure than China, India's oil and gas industry includes various installations, including drilling rigs, production platforms, refineries, pipelines, and terminals.

- As of June 2022, India has 77 active rigs. The country's oil production has been falling for almost a decade due to aging fields and the absence of major discoveries. Both state-owned and private players have been working on investment plans to raise recovery from older fields.

- For instance, in April 2022, Indian Oil Corporation Limited (IOCL) announced its plans to invest USD 102 billion in petroleum, oil, and lubricant (POL) storage capacities, including setting up a greenfield facility in the northeast region.

- Owing to such developments, the region is likely to witness rich growth in the oil and gas EPC market in the coming years.

Oil and Gas EPC Industry Overview

The oil and gas EPC market is fragmented. Some of the major players in the market (in no particular order) include Saipem SpA, TechnipFmc PLC, Petrofac Limited, Fluor Corporation, and Bechtel Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Demand to Develop the Natural Gas Infrastructure

- 4.5.1.2 Increase in Offshore Oil and Gas Exploration and Production (E&P) Activities

- 4.5.2 Restraints

- 4.5.2.1 High Volatility of Oil and Gas Prices

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Sector

- 5.1.1 Upstream

- 5.1.2 Downstream

- 5.1.3 Midstream

- 5.2 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 National Petroleum Construction Company

- 6.3.2 Petrofac Limited

- 6.3.3 Tecnicas Reunidas SA

- 6.3.4 Daewoo Engineering & Construction Co. Ltd

- 6.3.5 Fluor Corporation

- 6.3.6 Samsung Engineering Co. Ltd

- 6.3.7 Korea Shipbuilding & Offshore Engineering Co. Ltd

- 6.3.8 Hyundai Engineering & Construction Co. Ltd

- 6.3.9 John Wood Group PLC

- 6.3.10 TechnipFMC PLC

- 6.3.11 Bechtel Corporation

- 6.3.12 Saipem SpA

- 6.3.13 McDermott International Ltd

- 6.3.14 KBR Inc.

- 6.3.15 Sinopec Engineering (Group) Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Discovery of New Oil and Gas Fields Worldwide

02-2729-4219

+886-2-2729-4219

石油和天然气EPC 市场- 全球行业规模、份额、趋势、机会和预测,按服务类型(工程、采购)、按地点(陆上、海上)、按最终用户(上游、中游)、按地区和竞争细分, 2020-2030F

石油和天然气EPC 市场- 全球行业规模、份额、趋势、机会和预测,按服务类型(工程、采购)、按地点(陆上、海上)、按最终用户(上游、中游)、按地区和竞争细分, 2020-2030F 德国电力EPC -市场占有率分析、产业趋势与统计、成长预测(2025-2030)

德国电力EPC -市场占有率分析、产业趋势与统计、成长预测(2025-2030) 日本电力 EPC -市场占有率分析、产业趋势/统计、成长预测(2025-2030 年)

日本电力 EPC -市场占有率分析、产业趋势/统计、成长预测(2025-2030 年) 法国电力EPC市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

法国电力EPC市场:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 石油和天然气 EPC 市场规模、份额、成长分析(按合约、按最终用户、按应用、按地区)- 产业预测,2025 年至 2032 年

石油和天然气 EPC 市场规模、份额、成长分析(按合约、按最终用户、按应用、按地区)- 产业预测,2025 年至 2032 年 菲律宾电力 EPC:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

菲律宾电力 EPC:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 越南电力 EPC -市场占有率分析、产业趋势与统计、成长预测(2025-2030)

越南电力 EPC -市场占有率分析、产业趋势与统计、成长预测(2025-2030) 2024 年电力 EPC 全球市场报告

2024 年电力 EPC 全球市场报告 石油和天然气 EPC 市场,按合约类型、最终用户、应用程式和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

石油和天然气 EPC 市场,按合约类型、最终用户、应用程式和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 全球石油和天然气 EPC 市场规模研究,按产业(上游、下游、中游)和 2022-2032 年区域预测

全球石油和天然气 EPC 市场规模研究,按产业(上游、下游、中游)和 2022-2032 年区域预测

▼