|

市场调查报告书

商品编码

1444420

药用塑胶瓶 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Pharmaceutical Plastic Bottles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

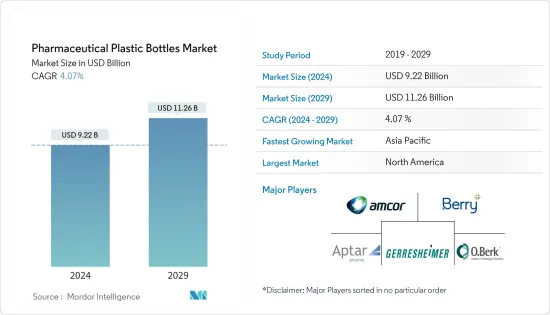

2024年药用塑胶瓶市场规模估计为92.2亿美元,预计到2029年将达到112.6亿美元,在预测期内(2024-2029年)CAGR为4.07%。

用于药品储存和运输的药品包装需求不断增长,预计将在预测期内推动市场发展。

主要亮点

- 製药业对塑胶包装的需求因其无与伦比的能力而显着增长。导致其在製药业中被更多采用的其他特性包括防潮、高尺寸稳定性、高衝击强度、抗应变、低吸水性、透明性、耐热性和阻燃性以及延长有效期。

- 由于提高回收率和最大限度地减少製药业对环境的影响,人们越来越关注永续性,因此药用塑胶瓶市场正在不断增长。技术进步以及塑胶瓶在固体甚至液体口服药物中的应用不断增加,促进了药用塑胶瓶的市场成长。然而,由于原油价格波动和各种法规导致的塑胶价格上涨将反映在塑胶价格的上涨上,这可能会影响该产品的消费并进一步阻碍所研究市场的成长。

- 塑胶瓶在业界越来越多地用于无菌填充和包装。市场供应商在各地区提供无菌瓶填充和包装服务。例如,LSNE 提供无菌滴管瓶填充服务。本公司拥有自动化填充线,可灌装标准多剂量三片瓶5毫升、10毫升瓶及无菌多剂量瓶。

- 亚太地区拥有重要的PET树脂和聚合物生产基地,这也有助于市场的成长,且不存在原料供应短缺的问题。中国是PET瓶最大的生产国和消费国之一。

- 随着对药品和其他必需品的需求不断增加,达到历史最高水平,缺乏可用的包装来包装和运输它们进一步导致供应链的严重中断。然而,对 COVID-19 患者使用的某些药物的需求增加。其中包括一些麻醉剂、抗生素、肌肉鬆弛剂和一些标籤外药物。这导致了製药公司塑胶瓶的供应。

药用塑胶瓶市场趋势

HDPE 细分市场成长率最高

- HDPE用于製造各种类型的瓶子,其中未着色的瓶子是半透明的,具有优异的挺度和阻隔性能。该材料有色素品种,可包装製药业的光敏药物。这些材料适合包装保质期较短的产品。根据美国化学理事会统计,2021年,美国树脂产量为1,239亿磅,其中热塑性塑胶约占总产量的86%。高密度聚乙烯(HDPE)是当年产量最多的树脂,产量达220亿磅。

- HDPE 还具有优异的耐化学性,这使其成为包装各种化学品和医药产品的宝贵材料。据证明,着色 HDPE 瓶比未着色 HDPE 材料具有更高的抗应力开裂性。 HDPE 的吹塑应用使其比 PP 和 LDPE 材料更耐用、用途更广泛。与其他形式的聚乙烯材料相比,它还具有优异的耐大多数溶剂性和高拉伸强度。

- HDPE 也主要用于商业领域的大型容器,因为它在普通聚合物中具有较高的强度重量比,并且比 PP 更不易碎。它在成型时保持了轻质特性,使其适合较大的容器,如塑胶罐。

- 此外,市场上多个参与者开展了各种研究和开发活动。例如,2021 年 4 月,Advil 製造商 GSK Consumer Healthcare (GSK) 宣布承诺将超过 8,000 万个 Advil 瓶中的塑胶含量减少 20%,这将导致环境中的塑胶减少近 500,000 磅。到 2022 年,Advil 预计将减少商店和网路上出售的几乎所有瓶子中的塑胶含量,但该品牌的 Easy Open 瓶子除外。新的阻隔树脂技术减少了模製和製作高密度聚乙烯 (HDPE) 瓶所需的树脂用量,同时保持阻隔保护性能。

北美占重要市场份额

- 由于塑胶容器和瓶子的消费和工业应用不断增加,美国塑胶瓶市场预计将以稳定的速度成长。据塑胶工业协会(PLASTICS)称,美国塑胶瓶的市场需求持续扩大。

- 据Pharmaceutical Commerce称,在美国,药品市场正在成长。到 2023 年,预计美国人将在药品上花费 635 至 6550 亿美元。因此,美国将成为医药支出最大的国家。

- 此外,根据Pharmaceutical Commerce称,在美国,药品市场正在成长。到 2023 年,预计美国人将在药品上花费 635 至 6550 亿美元。因此,它几乎肯定是医药支出最多的国家。

- 塑胶树脂及製品产业拥有 1,932 家工厂,拥有 93,000 名员工。塑胶产品几乎用于所有现代产品,在加拿大大多数经济领域都有需求,其中包装、建筑和汽车三大类占塑胶最终用途的 69%。

药用塑胶瓶产业概况

药用塑胶瓶市场因 Amcor Limited 等众多参与者的存在而变得分散。 Berry Plastics Group, Inc.、Aptar Pharma、Gerresheimer AG、Graham Packaging Company、Alpha Packaging 和 Alpack Plastic Packaging。参与者采取了各种有机和无机策略,如併购、合作、新产品发布和合作来主导市场。

- 2021 年 12 月 - Comar 宣布收购注塑和吹塑产品製造商 Omega Packaging。 Omega Packaging 的儿童安全 (CR) 瓶盖系列和精密模具製造能力推进了 Comar 的策略,即透过端到端客製化製造能力和扩展的产品组合为医疗保健客户提供服务。

- 2021 年 9 月 - Clearlake Capital Group 投资组合公司 Pretium Packaging 同意从 Irving Place Capital 手中收购总部位于美国的 Alpha Packaging,收购金额未公开。 Alpha Packaging 和 Pretium Packaging 将使合併后的实体能够为两家公司的现有客户群和新客户提供广泛的先进包装解决方案。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争激烈程度

- 产业价值链分析

- 评估 COVID-19 对市场的影响

第 5 章:市场动态

- 市场驱动因素

- 消费者对轻量药瓶的需求不断成长

- 增加医疗保健和製药支出以促进市场成长

- 市场限制

- 原料成本增加

- 对塑胶使用的环境担忧

第 6 章:市场细分

- 按原料分类

- 聚对苯二甲酸乙二酯(PET)

- 聚丙烯 (PP)

- 低密度聚乙烯 (LDPE)

- 高密度聚乙烯 (HDPE)

- 按类型

- 固体容器

- 滴管瓶

- 鼻喷瓶

- 液体瓶

- 口腔护理

- 其他类型

- 按地理

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 欧洲其他地区

- 亚太

- 中国

- 印度

- 日本

- 亚太其他地区

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 中东和非洲其他地区

- 北美洲

第 7 章:竞争格局

- 公司简介

- Amcor Limited

- Gerresheimer AG

- Berry Group Inc.

- Aptar Pharma

- O.Berk Company LLC

- Alpha Packaging

- Pro-Pac Packaging Ltd

- COMAR LLC

- Gil Plastic Products Ltd

- Drug Plastics Group

- Frapak Packaging

第 8 章:投资分析

第 9 章:市场机会与未来趋势

The Pharmaceutical Plastic Bottles Market size is estimated at USD 9.22 billion in 2024, and is expected to reach USD 11.26 billion by 2029, growing at a CAGR of 4.07% during the forecast period (2024-2029).

The growing demand for the packaging in pharmaceuticals for the storage and delivery of medicines is expected to drive the market during the forecast period.

Key Highlights

- The demand for plastic packaging has witnessed significant growth in the pharmaceutical industry because of its unmatched ability. Additional features that led to increased adoption in pharma are barrier against moisture, high dimensional stability, high impact strength, resistance to strain, low water absorption, transparency, resistance to heat and flame, and extension of expiry dates.

- The market for pharmaceutical plastic bottles is growing due to growing sustainability concerns by increasing the recycling rate and minimizing the environmental impact in the pharmaceutical industry. Technological advancement and the rising application of plastic bottles in solid and even liquid oral medicines have added to market growth for pharmaceutical plastic bottles. However, the rise in the price of plastics due to fluctuating prices of crude oil and various regulations would reflect on the increase in the price of plastics, which may affect the consumption of the product and further hinder the growth of the market studied.

- Plastic bottles are increasingly used for aseptic filling and packaging in the industry. Market vendors provide aseptic bottle filling and packaging services in various regions. For instance, LSNE offers aseptic dropper bottle filling services. The company has an automated filling line capable of filling standard multi-dose three-piece bottles in 5 ml and 10 ml bottles and sterile multi-dose bottles.

- Asia-Pacific has a prominent base for the production of PET resin and polymers, which is also aiding the growth of the market with no issues of a supply shortage of raw material. China is one of the largest producing and consuming countries of PET bottles.

- With the increasing demand for medicine and other essential goods at an all-time high, a lack of available packaging to package and ship them further caused a significant interruption in supply chains. However, the demand increased for some medicines used in patients with COVID-19. These included some anesthetics, antibiotics, muscle relaxants, and some off-label medicines. This led to the supply of plastic bottles in the pharmaceutical companies.

Pharmaceutical Plastic Bottles Market Trends

HDPE Segment to Report the Highest Growth Rate

- HDPE is used to manufacture various types of bottles, and among those, un-pigmented bottles are translucent, with excellent stiffness and barrier properties. The material has a pigmented variety, which can package light-sensitive drugs in the pharmaceutical industry. These materials are suited for packaging products with a short shelf life. According to American Chemical Council, in 2021, the United States produced 123.9 billion pounds of resins, in which thermoplastics accounted for roughly 86% of total production. High-density polyethylene (HDPE) was the most produced resin that year, with an output of 22 billion pounds.

- HDPE also has excellent chemical resistance, which presents it as a valuable material for packaging various chemicals and medicinal products. Pigmented HDPE bottles are witnessed to have improved stress crack resistance than un-pigmented HDPE material. The blow-molding application of HDPE makes it more durable and more versatile than PP and LDPE materials. It also has excellent resistance to most solvents and high tensile strength compared to other forms of polyethylene materials.

- HDPE is also primarily used for larger containers in the commercial sector as it has a high strength-to-weight ratio in common polymers and is less brittle than PP. It maintains a lightweight nature in molding, making it suitable for larger containers, like plastic canisters.

- Further, there have been various research and development activities by multiple players in the market. For instance, in April 2021, Advil maker GSK Consumer Healthcare (GSK) announced a commitment to reducing the plastic in more than 80 million Advil bottles by 20%, which will result in a reduction of nearly 500,000 pounds of plastic in the environment. By 2022, Advil is expected to reduce plastic in nearly all bottles available in stores and online, except the brand's Easy Open bottles. The new barrier resin technology reduces the amount of resin required to mold and craft the high-density polyethylene (HDPE) bottles while maintaining barrier protection properties.

North America Accounts for a Significant Market Share

- The US plastic bottles market is estimated to grow at a steady rate, owing to the constantly increasing consumption and industrial applications of plastic-made containers and bottles. According to the Plastics Industry Association (PLASTICS), the market demand for plastic bottles continues to expand in the United States.

- According to Pharmaceutical Commerce, in the United States, the pharmaceutical market is on the rise. By 2023, it is expected that Americans would spend USD 635 to USD 655 billion on pharmaceuticals. As a result, the United States will be the country with the greatest pharmaceutical spending.

- Moreover, according to Pharmaceutical Commerce, in the United States, the pharmaceutical market is on the rise. By 2023, it is expected that Americans will spend USD 635 to USD 655 billion on pharmaceuticals. As a result, it will almost certainly be the country with the most significant pharmaceutical spending.

- The plastic resin and products sector employs 93,000 people across 1,932 establishments. With usage in almost every modern product, plastic products are in demand in Canada in most sectors of the economy, with three categories packaging, construction, and automotive accounting for 69% of plastic end use.

Pharmaceutical Plastic Bottles Industry Overview

The pharmaceutical plastic bottle market is fragmented with the presence of many players like Amcor Limited. Berry Plastics Group, Inc., Aptar Pharma, Gerresheimer AG, Graham Packaging Company, Alpha Packaging, and Alpack Plastic Packaging. The players have adopted various organic and inorganic strategies such as mergers & acquisitions, partnerships, new product launches, and collaborations to dominate the market.

- December 2021 - Comar announced that it acquired Omega Packaging, an injection, and blow-molded product manufacturer. Omega Packaging's line of child-resistant (CR) closures and precision mold-building capabilities advance Comar's strategy to serve healthcare customers with end-to-end custom manufacturing capabilities and an expanded product portfolio.

- September 2021 - Clearlake Capital Group portfolio company Pretium Packaging agreed to acquire US-based Alpha Packaging from Irving Place Capital for an undisclosed sum. Alpha Packaging and Pretium Packaging will allow the combined entity to offer a wide range of advanced packaging solutions to both firms' existing customer bases and new customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyer

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need for Lightweight Pharma Bottles by Consumers

- 5.1.2 Increasing Spending on Healthcare and Pharmaceutical to Augment the Market Growth

- 5.2 Market Restraints

- 5.2.1 Increasing Raw Material Costs

- 5.2.2 Environmental Concerns over Usage of Plastics

6 MARKET SEGMENTATION

- 6.1 By Raw Material

- 6.1.1 Polyethylene Terephthalate (PET)

- 6.1.2 Poly Propylene (PP)

- 6.1.3 Low-density Poly Ethylene (LDPE)

- 6.1.4 High-density Poly Ethylene (HDPE)

- 6.2 By Type

- 6.2.1 Solid Containers

- 6.2.2 Dropper Bottles

- 6.2.3 Nasal Spray Bottles

- 6.2.4 Liquid Bottles

- 6.2.5 Oral Care

- 6.2.6 Other Types

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Mexico

- 6.3.4.4 Rest of Latin America

- 6.3.5 Middle East & Africa

- 6.3.5.1 Saudi Arabia

- 6.3.5.2 United Arab Emirates

- 6.3.5.3 South Africa

- 6.3.5.4 Rest of Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Amcor Limited

- 7.1.2 Gerresheimer AG

- 7.1.3 Berry Group Inc.

- 7.1.4 Aptar Pharma

- 7.1.5 O.Berk Company LLC

- 7.1.6 Alpha Packaging

- 7.1.7 Pro-Pac Packaging Ltd

- 7.1.8 COMAR LLC

- 7.1.9 Gil Plastic Products Ltd

- 7.1.10 Drug Plastics Group

- 7.1.11 Frapak Packaging

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

吹塑成型塑胶瓶市场:按类型、塑胶类型、技术、最终用户划分 - 全球预测 2025-2030

吹塑成型塑胶瓶市场:按类型、塑胶类型、技术、最终用户划分 - 全球预测 2025-2030 塑胶瓶和容器市场:按原料、类型和行业划分 - 全球预测 2025-2030

塑胶瓶和容器市场:按原料、类型和行业划分 - 全球预测 2025-2030 塑胶瓶和容器:市场占有率分析、行业趋势和统计、成长预测(2024-2029)

塑胶瓶和容器:市场占有率分析、行业趋势和统计、成长预测(2024-2029) 全球药用塑胶瓶市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球药用塑胶瓶市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 全球塑胶瓶市场规模、份额、成长分析,按材料(聚对聚对苯二甲酸乙二酯、聚丙烯)、产能、最终用途、容器类型 - 产业预测 2024-2031

全球塑胶瓶市场规模、份额、成长分析,按材料(聚对聚对苯二甲酸乙二酯、聚丙烯)、产能、最终用途、容器类型 - 产业预测 2024-2031 吹塑成型塑胶瓶全球市场2024-2028

吹塑成型塑胶瓶全球市场2024-2028 塑胶瓶:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

塑胶瓶:市场占有率分析、产业趋势与统计、成长预测(2024-2029) 宝特瓶和容器的全球市场

宝特瓶和容器的全球市场 塑胶瓶的全球市场:分析、成果、预测 (2023年~2029年)

塑胶瓶的全球市场:分析、成果、预测 (2023年~2029年)