|

市场调查报告书

商品编码

1687270

全球分散式阻断服务 (DDoS) 防护 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Global Distributed Denial of Service (DDoS) Protection - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

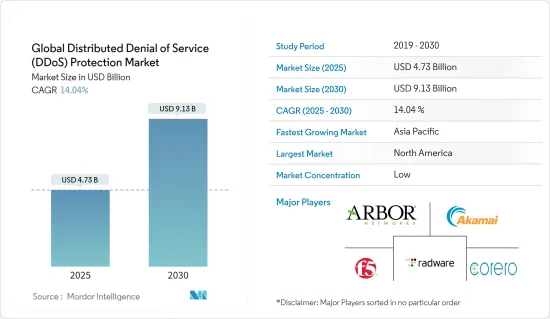

预计 2025 年全球分散式阻断服务保护市场规模为 47.3 亿美元,到 2030 年将达到 91.3 亿美元,预测期内(2025-2030 年)的复合年增长率为 14.04%。

随着新冠疫情的到来,劳动力几乎全部转移到了网路上。世界各地的人们在网路上工作、学习和购物的次数比以往任何时候都多。这也反映在最近 DDoS 攻击的目标上,最受攻击的资源是医疗保健组织、送货服务、游戏和教育平台的网站。

关键亮点

- 网路攻击的惊人成长预计将成为采用 DDoS 防护解决方案的主要驱动力。此类攻击的威胁源自于犯罪者能够轻鬆获得易于使用的工具,并且全面了解勒索的利润潜力。这些攻击直接针对商业系统和个人,可能导致巨大的经济和人身损失。

- 企业对 DDoS 保护的要求至关重要,因为无法应对攻击可能会影响收益、生产力、声誉和用户忠诚度。据Cloudflare称,DDoS攻击造成的经济负担巨大,每小时DDoS攻击将给组织带来约10万美元的损失,这进一步增加了对DDoS防护解决方案的需求。

- 此外,据 Cloudflare 称,DDoS 攻击的频率和复杂程度正在急剧上升。继第一季到第二季翻一番之后,观察到的网路层攻击总数在第三季再次翻了一番,与第一季COVID-19 之前的水平相比增加了四倍。我们也发现攻击媒介比以往任何时候都多。虽然 SYN、RST 和 UDP泛光仍然占据主导地位,但我们已经看到针对特定通讯协定的攻击爆炸式增长,包括 mDNS、Memcached 和 Jenkins DoS 攻击。

- 据思科称,到预测期中期,即2021年,流量超过1Gigabit每秒的DDoS攻击数量预计将增长到310万次,比2016年增长2.5倍。近年来,这些攻击变得更加频繁和严重。

- 此外,从国家分布来看,美国是遭受L3/4 DDoS攻击最多的国家,其次是德国和澳洲。依地区划分,前三大市场分别为北美(美国、加拿大)、欧洲(德国、俄罗斯等)、中东(阿联酋、科威特)、亚太地区、大洋洲(澳洲、泰国、日本)。

- 通讯产业是 2021 年第一季DDoS 攻击最严重的产业。据 Cloudflare 称,应用层攻击呈上升趋势,其中旨在破坏 HTTP 伺服器处理请求能力的攻击是一个主要问题。勒索软体类型的 DDoS 攻击也继续成为 2021 年第一季的一大挑战。

分散式阻断服务 (DDoS) 防护市场趋势

案例复杂的 DDoS 攻击正在推动市场

- 各行各业的 DDoS 攻击案例急剧增加,破坏了重要的组织服务并给各企业造成了数百万美元的损失,导致新兴经济体更加关注强大的保护解决方案。

- 针对暴露的网路基础架构(如串联路由器和其他网路伺服器)的网路层攻击对资料中心产生了重大影响,而相当一部分 IT 和通讯供应商则在资料中心业务。根据 Cloudflare 的数据,同步标誌 (SYN) 资料包泛光攻击仍然是最常见的攻击类型,约占 2021 年 1 月网路层攻击的 44%。已发现的其他攻击包括重置标誌 (RST) 封包、用户资料通讯协定(UDP) 和网域名称系统放大攻击。这些发展使得 DDoS 保护对于这些产业的供应商至关重要。

- 5G 的频宽增加和低延迟预计将进一步增加攻击的数量和严重性。根据 Corero 的研究,5G 更宽的频宽将允许先进的殭尸网路利用尽可能多的行动电话和物联网设备来消灭其目标。

- 此外,随着新冠疫情导致远端办公的出现,个人运算设备并不总是受到保护,这使得从不安全的在家工作环境访问公司网路时更容易受到攻击,从而导致由殭尸网路驱动的 DDoS 攻击增加。

- 随着全球各地企业的发展,新的进阶持续性威胁使关键服务面临风险。这促使组织部署更好的 DDoS 解决方案来保护其端点和网路免受潜在攻击。

预计北美将占很大份额

- 由于先进技术的采用日益增多以及网路安全解决方案的严格实施,北美预计将占据很大的市场份额。满足严格的法规和合规性要求的需求推动了该地区终端用户行业对先进安全系统的需求,从而推动了市场成长。

- 该地区还遭遇了大量的 DDoS 攻击,并且这些攻击在多个终端用户行业中可能会增加,进一步推动对 DDoS 防护解决方案的需求。此外,该地区,尤其是美国,网路攻击正在激增。该地区的数字庞大,主要是由于连网设备数量的快速增长。

- 此外,在美国,消费者正在使用公共云端将他们的个人资讯预先加载到多个行动应用程式上,使银行业务、购物和通讯更加便捷。在过去几年中,该地区的企业见证了 DDoS 攻击的增加,导致对保护解决方案的认识大大提高。此外,根据白宫经济顾问委员会的数据,美国经济每年因有害网路活动损失约 570 亿美元至 1,090 亿美元。

- 此外,Atlas VPN 估计,光是 2020 年 3 月,美国就发生了超过 175,000 次 DDoS 攻击。攻击者试图破坏美国卫生与公众服务部网站。其主要目的似乎是剥夺公民获取 COVID-19 疫情官方资料和防护措施的权利。

- 美国政府也签署立法,成立网路安全和基础设施安全局(CISA),以加强国家抵御网路攻击的能力。该机构与联邦政府合作,提供网路安全工具、事件回应服务和评估能力,以保护支援合作机构关键业务的政府网路。因此,新旧企业都可以投资于专为产业设计的正确保护套件,开闢新的途径。

- 随着各公司推出独立的 5G 网络,他们可能需要安全合作伙伴来确保他们的网络和针对攻击的安全性在威胁发生之前就已牢固建立。例如,2021年4月,DISH Network Corporation选择Allot Ltd为其美国的基于云端原生OpenRAN的5G网路提供端对端用户平面保护(UPP),以抵御DDoS和殭尸网路攻击。

分散式阻断服务 (DDoS) 防护产业概览

DDoS 防护市场由多个参与企业组成,主要是国内和国际的参与者,他们在竞争激烈的市场空间中争夺关注。该市场还具有产品渗透率高、产品差异化程度中等至高、竞争激烈等特性。市场以产品为中心,技术进步不断主导市场。创新、研发投资、合作伙伴关係和併购有望成为市场供应商之间的竞争策略的一部分。总体而言,竞争格局非常激烈,预计在预测期内仍将保持这种状态。

- 2022 年 6 月 - G-Core Labs 与英特尔合作,宣布推出一款独立解决方案 (eBPF),可缓解 DDoS 攻击,同时降低对整体延迟的影响。此基于 XDP 的解决方案无需专用 DDoS 保护伺服器角色,并可防止 SYN泛光DDoS 攻击。

- 2022 年 3 月 - 即时、高效能 DDoS 网路防护解决方案供应商 Corero Network Security 扩展了其针对殭尸网路和地毯式轰炸攻击的自动防护能力。该公司的使命是透过防止 DDoS 攻击造成的中断和停机,使网路成为更安全的商业场所。

- 2022 年 2 月-Radware 以 3,000 万美元收购 SecurityDAM,并将为Radware收购后的云端 DDoS 防护服务支付高达 1,250 万美元的成功费。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

- 研究框架

- 二次研究

- 初步研究

- 资料三角测量与洞察生成

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- 产业价值链分析

- COVID-19 市场影响评估

第五章市场动态

- 市场驱动因素

- 复杂 DDoS 攻击的兴起

- 部署经济高效的云端基础和混合的解决方案

- 跨产业的技术扩散与物联网应用

- 市场问题

- 增加网路和部署的复杂性

第六章 相关使用案例和使用案例

第七章市场区隔

- 成分

- 解决方案

- 服务

- 部署类型

- 云

- 本地

- 杂交种

- 公司规模

- 中小型企业

- 大型企业

- 最终用户产业

- 政府和国防

- 资讯科技/通讯

- 医疗保健

- 零售

- BFSI

- 媒体娱乐

- 其他的

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

第八章竞争格局

- 公司简介

- Arbor Networks Inc.(NetScout Systems Inc.)

- Akamai Technologies Inc.

- F5 Networks Inc.

- Imperva Inc.

- Radware Ltd

- Corero Network Security Inc.

- Neustar Inc.

- Cloudflare Inc.

- Nexusguard Ltd

- Dosarrest Internet Security Ltd

- Verisign Inc.

第九章投资分析

第十章:市场的未来

The Global Distributed Denial of Service Protection Market size is estimated at USD 4.73 billion in 2025, and is expected to reach USD 9.13 billion by 2030, at a CAGR of 14.04% during the forecast period (2025-2030).

With the emergence of the COVID-19 pandemic, working environments have shifted almost entirely to the web. People worldwide have increasingly started working, studying, and shopping online as compared to before. This has also been reflected in the goals of recent DDoS attacks, with the most targeted resources being the websites of medical organizations, delivery services, and gaming and educational platforms.

Key Highlights

- An alarming increase in the number of network attacks is anticipated to be a significant driver for the adoption of DDoS protection solutions. The threat of these attacks is driven by ready access to easy-to-use tools and a more comprehensive criminal understanding of its potential for profit through extortion. These attacks directly target business systems and individuals, which could lead to enormous financial and personal losses.

- The requirement for DDoS protection for enterprises has gained tremendous significance, as failure to deal with the attacks can affect revenue, productivity, reputation, and user loyalty. According to Cloudflare, the financial burden of a DDoS attack is significant, as falling victim to a DDoS attack can cost an organization around USD 100,000 for every hour the attack lasts, further fuelling the demand for DDoS protection solutions.

- Additionally, as per Cloudflare, DDoS attacks are surging in frequency and sophistication. After doubling from Q1 to Q2, the total number of network layer attacks witnessed in Q3 doubled again, resulting in a 4x increase compared to the pre-COVID-19 levels in the first quarter. The company also witnessed more attack vectors deployed than ever. While SYN, RST, and UDP floods continue to dominate the landscape, the company saw an explosion in protocol-specific attacks such as mDNS, Memcached, and Jenkins DoS attacks.

- As per Cisco, the number of DDoS attacks exceeding 1 gigabit per second of traffic is expected to rise to 3.1 million by the mid-forecast period, i.e., by 2021, which is a 2.5-fold increase from 2016. In recent years, these attacks have increased in frequency and severity.

- Moreover, the United States observed the highest number of L3/4 DDoS attacks under the country-based distribution, followed by Germany and Australia. The top countries affected by region include North America (United States, Canada), Europe (Germany, Russia, among others), the Middle East (UAE, Kuwait), Asia-Pacific, and Oceania (Australia, Thailand, Japan).

- The telecom industry was at the top when DDoS attacks most targeted it during the first quarter of 2021. According to Cloudflare, application-layer attacks are on the rise, and those that aim to disrupt the HTTP server's ability to process requests are reasons for significant concern. Also, ransom DDoS attacks continued to be a significant challenge during the first quarter of 2021.

Distributed Denial of Service (DDoS) Protection Market Trends

Increasing Instances of Sophisticated DDoS Attacks to Drive the Market

- The rapidly rising instances of DDoS attacks across multiple industries, which have disrupted crucial organizational services and the loss of millions of dollars for various companies, have increased the focus on robust protection solutions across emerging economies.

- Network layer attacks that target exposed network infrastructure such as inline routers and other network servers significantly impact data centers where a significant share of IT and telecom vendors operate. According to Cloudflare, about 44% of network layer attacks occurred in January 2021, with synchronizing flag (SYN) packet flood attacks remaining the most common. Other attacks noted included reset flag (RST) packets, user datagram protocol (UDP), and domain name system amplification attacks. Due to such developments, DDoS protection is vital for vendors operating in these industries.

- The increased bandwidth and low latency in 5G are further anticipated to increase the volume and severity of the attacks. According to Corero's study, the higher bandwidth of 5G enables advanced botnets to harness as many mobiles or IoT devices as possible to cripple their targets.

- Further, with the adoption of remote working due to the onset of Covid, corporate networks have become more vulnerable when accessed from unsecured work-from-home environments, as personal computing devices are not always protected, thus causing an increase in Botnet DDoS attacks.

- As businesses worldwide grow, new and advanced persistent threats have exposed critical services to risk. This has encouraged organizations to deploy better DDoS solutions to safeguard their endpoints and networks against potential attacks.

North America is Expected to Hold a Major Share

- The North American region is expected to hold a significant market share, primarily due to the higher adoption of advanced technologies and stricter implementation of cybersecurity solutions. Given the need to meet stringent regulatory and compliance requirements, there is a rising need for advanced security systems among the region's end-user industries that positively boost the market's growth.

- The region also accounts for a significant number of DDoS attacks, which are likely to increase with respect to multiple end-user industries, further driving the demand for DDoS protection solutions. Moreover, cyberattacks in the region, especially in the United States, are increasing rapidly. They are reaching high numbers, primarily owing to the rapidly increasing number of connected devices in the region.

- Also, in the United States, consumers have been using public clouds, and multiple mobile applications are preloaded with personal information for the convenience of banking, shopping, and communication. In the past few years, companies in the region have been witnessing increasing DDoS attacks, which has resulted in tremendous awareness related to protection solutions. Also, according to the White House Council of Economic Advisers, the US economy loses approximately USD 57 billion to USD 109 billion per year to harmful cyber activity.

- Moreover, according to Atlas VPN, it was estimated that there were more than 175,000 DDoS attacks in the United States in March 2020 alone. Attackers tried to disable the website of the US Department of Health and Human Services. The primary purpose seemed to deprive the citizens of access to official data regarding the COVID-19 pandemic and the measures being taken against it.

- The US government also signed a law to establish the Cybersecurity and Infrastructure Security Agency (CISA) to enhance the national defense against cyberattacks. The agency works with the federal government to provide cybersecurity tools, incident response services, and assessment capabilities to safeguard the governmental networks that support essential operations of the partner departments and agencies. As a result, it opens new avenues for the new and existing companies to invest in a suitable protection suite designed for the industry.

- Various firms are deploying standalone 5G networks, and they would need security partners to become ingrained in their network and security against attacks well before a threat occurs. For instance, in April 2021, DISH Network Corporation chose Allot Ltd to provide end-to-end User Plane Protection (UPP) against DDoS and botnet attacks on the United States' cloud-native, OpenRAN-based 5G network.

Distributed Denial of Service (DDoS) Protection Industry Overview

The DDoS protection market primarily comprises multiple domestic and international players fighting for attention in a somewhat contested market space. The market is also characterized by growing product penetration, moderate/high product differentiation, and high levels of competition. The market is product-centric, and technological advancements constantly govern it. Innovations, R&D investments, partnerships, and M&As are expected to be part of the competitive strategy among the vendors operating in the market. Overall, the intensity of the competitive rivalry is high, and it is expected to remain the same during the forecast period.

- June 2022 - G-Core Labs, in partnership with Intel, launched a standalone solution (eBPF) providing mitigation of DDoS attacks with a low impact on overall latency. The XDP-based solution removes the need for a dedicated DDoS protection server role and protects against SYN Flood DDoS attacks.

- March 2022 - Corero Network Security, a real-time, high-performance DDoS cyber defense solutions provider, extended its automatic protection against Botnet and Carpet Bomb attacks. The company's mission is to make the internet a safer place to do business by protecting against the disruption and downtime caused by DDoS attacks.

- February 2022 - Radware acquired SecurityDAM for USD 30 million, with contingent payments of up to USD 12.5 million for Radware's cloud DDoS protection service after the deal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Instances of Sophisticated DDoS Attacks

- 5.1.2 Introduction of Cost-effective Cloud-based and Hybrid Solutions

- 5.1.3 Proliferation of Technology and Adoption of IoT across Various Verticals

- 5.2 Market Challenges

- 5.2.1 Growing Network and Deployment Complexities

6 RELEVANT USE CASES AND CASE STUDIES

7 MARKET SEGMENTATION

- 7.1 Component

- 7.1.1 Solution

- 7.1.2 Service

- 7.2 Deployment Type

- 7.2.1 Cloud

- 7.2.2 On-premise

- 7.2.3 Hybrid

- 7.3 Size of Enterprise

- 7.3.1 Small and Medium Enterprises

- 7.3.2 Large Enterprises

- 7.4 End-user Industry

- 7.4.1 Government and Defense

- 7.4.2 IT and Telecommunication

- 7.4.3 Healthcare

- 7.4.4 Retail

- 7.4.5 BFSI

- 7.4.6 Media and Entertainment

- 7.4.7 Other End-user Industries

- 7.5 Geography

- 7.5.1 North America

- 7.5.2 Europe

- 7.5.3 Asia-Pacific

- 7.5.4 Rest of the World

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Arbor Networks Inc. (NetScout Systems Inc.)

- 8.1.2 Akamai Technologies Inc.

- 8.1.3 F5 Networks Inc.

- 8.1.4 Imperva Inc.

- 8.1.5 Radware Ltd

- 8.1.6 Corero Network Security Inc.

- 8.1.7 Neustar Inc.

- 8.1.8 Cloudflare Inc.

- 8.1.9 Nexusguard Ltd

- 8.1.10 Dosarrest Internet Security Ltd

- 8.1.11 Verisign Inc.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

全球DDoS防护与缓解安全市场:依产品、解决方案类型、应用领域、部署模式、组织规模、产业与地区划分-预测至2030年

全球DDoS防护与缓解安全市场:依产品、解决方案类型、应用领域、部署模式、组织规模、产业与地区划分-预测至2030年 分散式阻断服务 (DDoS) 防护市场按组件、安全类型、部署模式、组织规模、最终用户产业和地区划分

分散式阻断服务 (DDoS) 防护市场按组件、安全类型、部署模式、组织规模、最终用户产业和地区划分 DDoS 防护与缓解安全市场按组件、部署类型、类型、垂直行业和组织规模划分 - 全球预测 2025-2032 年DDoS 防护与缓解市场(按组件、部署类型、组织规模、安全类型和最终用户划分)—2025-2032 年全球预测

DDoS 防护与缓解安全市场按组件、部署类型、类型、垂直行业和组织规模划分 - 全球预测 2025-2032 年DDoS 防护与缓解市场(按组件、部署类型、组织规模、安全类型和最终用户划分)—2025-2032 年全球预测 2025年全球DDoS防护与缓解安全市场报告2025年全球DDoS防护与缓解市场报告

2025年全球DDoS防护与缓解安全市场报告2025年全球DDoS防护与缓解市场报告 全球分散式阻断服务 (DDoS) 攻击缓解市场

全球分散式阻断服务 (DDoS) 攻击缓解市场 分散式阻断服务攻击(DDoS)防御的全球市场,各零件,各部署类型,不同企业规模,终端用户各业界,各地区,机会,预测,2018年~2032年

分散式阻断服务攻击(DDoS)防御的全球市场,各零件,各部署类型,不同企业规模,终端用户各业界,各地区,机会,预测,2018年~2032年 分散式阻断服务保护市场规模、份额和趋势分析报告:按组件、应用、部署、企业规模、最终用途、地区和细分市场进行预测,2025 年至 2033 年

分散式阻断服务保护市场规模、份额和趋势分析报告:按组件、应用、部署、企业规模、最终用途、地区和细分市场进行预测,2025 年至 2033 年 DDoS 保护和缓解市场规模、份额、成长分析(按产品、按部署模式、按应用领域、按组织规模、按垂直行业和按地区)- 行业预测 2025-2032

DDoS 保护和缓解市场规模、份额、成长分析(按产品、按部署模式、按应用领域、按组织规模、按垂直行业和按地区)- 行业预测 2025-2032