|

市场调查报告书

商品编码

1444447

全球智慧涂料市场:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Smart Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

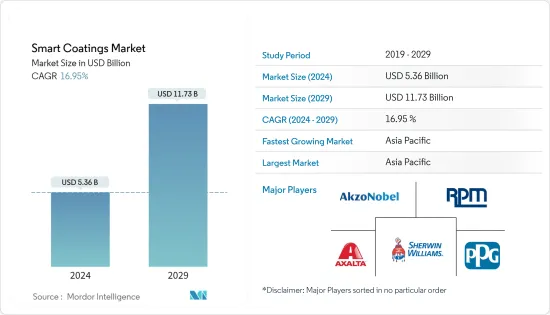

全球智慧涂料市场规模预计到2024年将达到53.6亿美元,并在2024-2029年预测期间以16.95%的复合年增长率增长,到2029年将达到117.3亿美元。我是。

COVID-19 大流行对市场产生了负面影响。然而,在疫情大流行后,由于全球建筑、汽车、航太和国防等各种最终用户产业的成长,预计市场将在预测期内稳定成长。

主要亮点

- 短期内,建筑业需求上升预计将带动市场需求。

- 另一方面,用于製造智慧涂料的昂贵且高品质的原材料可能会抑制市场并阻碍市场成长。

- 预计增加使用奈米粒子来改善功能将是未来几年市场的机会。

- 预计亚太地区将主导市场,并且在预测期内也将见证最高的复合年增长率。

智慧涂料市场趋势

建筑业的需求不断成长

- 智慧涂料,如自清洁涂料,用于玻璃幕墙,特别是高层商业和办公大楼,以方便维护。抗菌涂料广泛应用于医院、厨房、公共卫生间。防腐蚀涂料也用于基础设施和工业建筑。

- 亚太地区的建筑业是世界上最大的,并且由于人口增长、中阶收入增加和都市化稳步增长。

- 根据中国国家统计局的数据,2021年中国建筑产值为25.92兆元人民币(4.016兆美元),而2020年为23.27兆元人民币(3.374兆美元)。这导致中国建筑需求的扩大。

- 除了住宅建筑外,亚太地区近年来办公空间市场也不断发展,使其成为商业建筑领域最大的市场之一。

- 根据美国人口普查局的数据,2021 年美国年度新建工程金额为 16,264.44 亿美元,而 2020 年为 14,995.70 亿美元。此外,美国住宅的年价值估计为 美元。 2021 年为 8,029.33 亿美元,而 2020 年为 6,442.57 亿美元。

- 根据欧盟统计局数据,德国2022年第一季建筑总产量较2021年第一季成长5.4%,较同年上季成长3.6%,导致建筑中智慧涂料的消费应用程式增加。

- 因此,建设活动的强劲成长正在刺激市场需求。

中国主导亚太

- 就市场占有率而言,亚太地区在全球智慧涂料市场中占据主导地位。建设活动增加和汽车行业成长等因素为所研究的市场提供了推动力。

- 智慧涂料越来越多地应用于中国的建筑业。中国拥有全世界最大的建筑业。此外,多个大型建设计划正在进行中,中国很可能在可预见的未来保持其最大建筑业的地位。

- 中国主要受到经济成长支持下发达的住宅和商业建筑业的推动。在中国,香港住宅委员会推出多项措施,鼓励兴建廉租住宅。当局的目标是到 2030 年在 10 年内交付 301,000 套社会住宅。

- 在印度,汽车业对GDP总量的贡献为7.1%,製造业占GDP的49%,年销售额75亿卢比(1万美元),出口额35亿卢比(4,700美元)。它变成了。

- 此外,2021年生产了4,399,112辆汽车,比2020年的3,394,446辆成长了30%。印度汽车产业乐观地认为,产量将在 2022 年达到 COVID-19 大流行前的水平。儘管半导体短缺阻碍了製造业,我们还是在 2021 年奠定了坚实的基础。

- 根据联合国贸易和发展会议(UNCTAD)的数据,截至2022年初,日本商船队总量为40,263,340载重吨,较2022年初的39,312,530载重吨增长2.42%。这将增加2021年国内智慧涂料的需求。

- 所有上述因素都可能在预测期内扩大市场。

智慧涂料产业概况

全球智慧涂料市场是一个半一体化市场。市场上的主要企业包括(排名不分先后)Akzo Nobel NV、PPG Industries Inc、The Sherwin-Williams Company、RPM International Inc. 和 Axalta Coating Systems, LLC。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 优于传统涂料的性能

- 建筑业需求不断增长

- 抑制因素

- 智慧涂料高成本

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章市场区隔(收益市场规模)

- 功能

- 防污

- 抗菌的

- 防锈

- 防冻

- 自清洁

- 色移

- 其他特性

- 最终用户产业

- 建筑/施工

- 车

- 海洋

- 航太/国防

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 其他地区

- 南美洲

- 中东/非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业采取的策略

- 公司简介

- 3M

- Akzo Nobel NV

- Axalta Coating Systems, LLC

- Dupont

- Hempel AS

- Jotun

- NEI Corporation

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

第七章市场机会与未来趋势

The Smart Coatings Market size is estimated at USD 5.36 billion in 2024, and is expected to reach USD 11.73 billion by 2029, growing at a CAGR of 16.95% during the forecast period (2024-2029).

The COVID-19 pandemic had a negative impact on the market; however, post the pandemic, the market is projected to grow steadily during the forecast period owing to growth in various end-user industries like construction, automotive, aerospace, and defense across the world.

Key Highlights

- Over the short term, the rising demand from the construction industry is expected to drive the demand in the market.

- On the flip side, expensive quality raw materials used in the manufacturing of smart coatings are likely to restrain the market and hinder the market's growth.

- Increasing the use of nanoparticles to improve functionality is projected to act as an opportunity for the market in the coming years.

- The Asia-Pacific region is expected to dominate the market and will also witness the highest CAGR during the forecast period.

Smart Coating Market Trends

Increasing Demand from Building and Construction Industry

- Smart coatings like self-cleaning coatings are used on glass walls in buildings for easier maintenance, especially for high-rise commercial and office buildings. Antimicrobial coatings find extensive application in hospitals, kitchens, and public bathrooms. Anti-corrosion coatings are also used in infrastructure and industrial buildings.

- The construction sector in the Asia-Pacific region is the largest in the world and is increasing at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization.

- According to the National Bureau of Statistics of China, the output value of the construction works in the country accounted for CNY 25.92 trillion (USD 4.016 trillion) in 2021 compared to CNY 23.27 trillion (USD 3.374 trillion) in 2020, thereby enhancing the demand in the market studied.

- Apart from residential construction, the Asia-Pacific region has also been a thriving market for office spaces in recent years and is one of the largest markets for the commercial construction sector.

- According to the United States Census Bureau, the annual value for new construction in the United States accounted for USD 1,626,444 million in 2021, compared to USD 1,499,570 million in 2020. Moreover, the annual value of residential construction in the United States was estimated at USD 802,933 million in 2021, compared to USD 644,257 million in 2020.

- According to Eurostat, the total construction production in Germany increased by 5.4% in Q1 2022, compared to the Q1 2021 production, and increased by 3.6% compared to the previous quarter in the same year, thereby enhancing the consumption of smart coatings from various construction applications in the country.

- Hence, such robust growth in construction activities is fuelling the demand for the market.

China to Dominate the Asia-Pacific Region

- The Asia-Pacific region dominated the global smart coatings market in terms of market share. Factors such as increasing construction activities and a growth of the automotive industry are favoring the studied market.

- Smart coatings are being increasingly used in China's building and construction industry. China has the world's largest construction industry. Moreover, with several major construction projects in progress, China is likely to maintain its stature as the largest construction industry over the foreseeable future.

- China has been majorly driven by ample developments in the residential and commercial construction sectors supported by the growing economy. In China, the housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units in 10 years by 2030.

- In India, the contribution of the automobile sector to the overall GDP stands at 7.1%, while it stands at 49% of the manufacturing GDP, with an annual turnover of INR 7.5 lakh crore (USD 0.010 million) and an export of INR 3.5 lakh crore (USD 0.0047 million).

- In addition, 43,99,112 vehicles were produced in 2021, which increased by 30% compared to the 33,94,446 units manufactured in 2020. The Indian automotive sector is optimistic about reaching pre-COVID-19-pandemic levels of production volume in 2022 after laying a solid foundation in 2021 despite manufacturing being hampered by a semiconductor shortage.

- According to the UN Conference on Trade and Development (UNCTAD), Japan's merchant fleet accounted for 40,263.34 thousand dead-weight tons at the start of 2022, registering a growth rate of 2.42%, compared to 39,312.53 thousand dead-weight ton at the beginning of 2021, thereby, increasing the demand for smart coatings in the country.

- All the aforementioned factors are likely to augment the market over the forecast period.

Smart Coating Industry Overview

The global market for smart coatings is a semi-consolidated market. Major players in the market include Akzo Nobel NV, PPG Industries Inc, The Sherwin-Williams Company, RPM International Inc., and Axalta Coating Systems, LLC, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Superior Properties Over Traditional Coatings

- 4.1.2 Growing Demand from the Construction Sector

- 4.2 Restraints

- 4.2.1 High Cost of Smart Coatings

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Revenue)

- 5.1 Function

- 5.1.1 Anti-fouling

- 5.1.2 Anti-microbial

- 5.1.3 Anti-corrosion

- 5.1.4 Anti-icing

- 5.1.5 Self-cleaning

- 5.1.6 Color-shifting

- 5.1.7 Other Functions

- 5.2 End-User Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Marine

- 5.2.4 Aerospace and Defense

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Akzo Nobel NV

- 6.4.3 Axalta Coating Systems, LLC

- 6.4.4 Dupont

- 6.4.5 Hempel AS

- 6.4.6 Jotun

- 6.4.7 NEI Corporation

- 6.4.8 PPG Industries Inc.

- 6.4.9 RPM International Inc.

- 6.4.10 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing use of Nanoparticles to Improve Functionality

- 7.2 Increasing Opportunities for Smart Coatings to Replace Conventional Coatings in Various End-user Industries