|

市场调查报告书

商品编码

1444448

汽车ECU(电控系统):市场占有率分析、产业趋势与统计、成长预测(2024-2029)Automotive Electronic Control Unit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

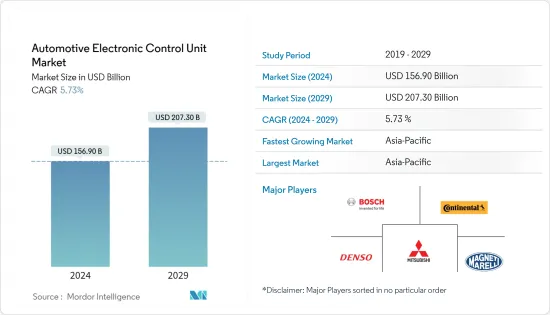

汽车ECU(电控系统)市场规模预计到2024年为1569亿美元,预计到2029年将达到2073亿美元,在预测期内(2024-2029年)增加57.3亿美元,年复合增长率为%。

由于汽车製造业的关闭和封锁,COVID-19感染疾病不可避免地对汽车ECU(电控系统)市场产生负面影响。然而,随着全球电动车的采用率与前一年同期比较快速成长,市场预计将重新获得动力。

市场主要由技术进步和製度创新所驱动。在已开发国家,消费者对驾驶便利性和安全性的偏好正在推动市场成长。导航和资讯娱乐系统是全球大多数汽车的标准配置,其采用率正在不断增加。为了将这些系统相互连接,需要电控系统汽车连接器。

政府减少燃油使用的法规以及公众提高车辆燃油效率的需求不断增加也是导致汽车领域ECU市场高速成长的主要因素。

已开发国家混合动力汽车和纯电动车等替代车辆选择的稳定成长对 ECU 市场做出了重大贡献,因为这些车辆与传统车辆相比非常复杂。驱动因素安全、保全问题、驾驶便利性、客户要求的减少维护负担也是推动 ECU 市场成长的一些因素。

将智慧型手机连接到车辆并为驾驶员提供有关车辆状况的即时资讯已成为当今的一大趋势。这些先进的 ECU 系统能够轻鬆地与智慧型手机连接,从而促进 ECU 系统的发展。

由于该地区对电动车的需求不断增长,预计亚太地区,其次是北美和欧洲,在预测期内将显着增长。此外,已开发国家和新兴国家对混合动力汽车等技术先进车辆的需求不断增长,预计将推动 ECU 市场的成长。

汽车ECU(电控系统)市场趋势

由于电动车销量的增加,对 ECU 的需求正在扩大

全球对电动车的需求正在快速增长,预计这将增加这些车辆对 ECU 的需求。此外,有利的政府补贴和措施也成为促进 ECU 市场成长的催化剂。到 2040 年,近 54% 的新车销量和 33% 的全球持有将是电动车。

欧洲各国政府已经启动了各种计划,在全部区域建造充电基础设施,以满足电动车销售目标。汽车产业的转变预计将影响汽车製造商、电子元件製造商、售后市场和产业的供应链。

随着电动车需求和销量的增加,仅与内燃机汽车相关的零件製造商正在将业务扩展到电动车领域。在汽车诊断市场中,用于引擎控制和变速箱的ECU等组件将被用于电气架构和电池管理系统的ECU所取代。

此外,预计传统的诊断系统将完全被汽车诊断系统所取代,该系统可以持续监控车辆所有电气和机械部件的状况。

预计亚太地区将主导 ECU 市场

由于小客车汽车娱乐和通讯应用的需求不断增长、可支配收入的增加以及该地区汽车产量的增加,亚太地区在汽车 ECU(电控系统)市场占据主导地位。

由于中国和日本的存在,亚太地区的电动普及很高。中国是电动车的主要市场,推进电动车技术的汽车製造商大多是日本人。电动车的发展可能与该地区 ECU 市场需求的增加有关,该地区目前在收益和销售方面占据最高的市场占有率。

由于豪华车需求的增加、节能汽车需求的增加以及政府为减少该地区碳排放而製定的严格法规,预计北美汽车电控系统市场也将成长。

由于豪华车和小客车对资讯娱乐和通讯应用的需求不断增长,欧洲汽车 ECU 市场正在不断增长。德国、义大利等欧洲国家的主要汽车製造商越来越注重提供豪华和舒适功能,这为市场成长创造了进一步的机会。

汽车ECU(电控系统)产业概况

汽车电控系统市场由李尔公司、罗伯特博世有限公司、日本电产公司、大陆集团和德尔福科技等公司主导。世界各地的公司正在采用各种创新技术并投资研发计划。此外,製造商正在透过在世界各地开设经销商和分销网络来扩大其网络,以赚取利润并加强其在行业中的影响力。例如,

2021 年 10 月,Motherson 扩大了与马瑞利汽车照明 (Marelli) 的合作,在印度设立了一个新工具室。这将是印度第一个专门用于特定照明应用的此类工具室。该工具室将是现有合资企业 Marelli Motherson Automotive Lighting India Private Limited 的延伸。这家 50/50 合资企业成立于 2008 年,旨在迎合印度户外照明市场,目前在印度拥有四家工厂。

2020年3月,罗伯特·博世有限公司与尼古拉马达公司建立合作伙伴关係,开发一款负载容量为40吨的燃料电池卡车。先进卡车系统的关键要素是博世车辆控制单元,它减少了独立单元的数量,同时为先进功能提供了更高的运算能力。 VCU 透过为复杂的电子/电子架构提供可扩展的平台来支援未来的创新,这对于支援 Nikola 卡车的高级功能至关重要。

2021年10月,采埃孚宣布其主动后轴转向系统AKC(主动运动控制)自2013年推出以来已生产100万套。 AKC 在各种驾驶情况下都能提供敏捷性、安全性和舒适性。

由于上述案例和发展,汽车电控系统市场的参与者预计将集中精力占领大部分市场占有率,并可能在预测期内扩大其地理分布。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 市场限制因素

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 透过促销

- 内燃机

- 混合

- 电池电动车

- 按用途

- ADAS 与安全系统

- 车身控制与舒适系统

- 资讯娱乐和通讯系统

- 动力传动系统系统

- 透过ECU

- 16位ECU

- 32位ECU

- 64位ECU

- 自主性别

- 常规车

- 半自动驾驶汽车

- 自动驾驶汽车

- 搭车

- 小客车

- 商用车

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 英国

- 法国

- 德国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 世界其他地区

- 南美洲

- 中东和非洲

- 北美洲

第六章 竞争形势

- 供应商市场占有率

- 公司简介

- Lear Corporation

- Robert Bosch GmbH

- Nidec Corporation

- Continental AG

- Aptiv PLC

- Leopold Kostal GmbH &Co. KG

- ZF Friedrichshafen AG

- Autoliv Inc.

- Magneti Marelli

第七章市场机会与未来趋势

The Automotive Electronic Control Unit Market size is estimated at USD 156.90 billion in 2024, and is expected to reach USD 207.30 billion by 2029, growing at a CAGR of 5.73% during the forecast period (2024-2029).

The negative impact of the COVID-19 pandemic on the automotive electronic control unit market was inevitable due to shut down of automotive manufacturing units and lockdowns. However, the market is expected to regain momentum due to the swiftly escalating year-on-year adoption rate of electric vehicles worldwide.

The market is primarily driven by technological advancements and innovation in systems. In developed nations, increasing consumer preference for driving convenience and safety is driving the market's growth. The adoption of navigation and infotainment systems is growing as they have become standard features in most cars across the world. Central electronic control unit automotive connectors are required to connect these systems to one another.

Government regulations to reduce fuel usage and increasing demand for better mileage of vehicles from the general public are other major factors leading to the high growth of the ECU market in the automotive sector.

The steady growth of alternative vehicle choices, such as hybrid and pure electric cars, in developed nations has contributed significantly to the ECU market due to the high complexities of these vehicles over conventional vehicles. Driver safety, security concerns, ease of driving, and low maintenance demanded by the customers are also some of the factors driving the growth of the ECU market.

Connecting smartphones to the vehicle and providing the driver with real-time information about the vehicle's state is a major trend in recent times. These advanced ECU systems, with the provision to connect with smartphones easily, can lead to an improvement in the growth of ECU systems.

The Asia-Pacific region, followed by North America and Europe, is anticipated to witness significant growth during the forecast period owing to the growing demand for electric vehicles in the region. Moreover, increased demand for technologically advanced vehicles like hybrid vehicles in developed and developing countries is expected to drive the growth of the ECU market.

Automotive Electronic Control Unit Market Trends

Rising Electric Vehicle Sales to Boost Demand for ECUs

The demand for electric vehicles is growing rapidly across the world, and this is expected to augment the demand for ECU in these vehicles. In addition, favorable government subsidies and initiatives act as catalysts for boosting the growth of the ECU market. By 2040, nearly 54% of new car sales and 33% of the global car fleet will be electric.

The European government has already started various projects for building charging infrastructure across the regions to meet the electric vehicle sales target. This transformation in the automotive sector is expected to impact the automakers, electronic component manufacturers, aftermarkets, and the sector's supply chain.

Manufacturers of parts and components only pertaining to IC engine vehicles are now expanding their business into the electric vehicle domain as the demand for and sale of electric vehicles increases. In the automotive diagnostics market, components, such as ECU for engine control and transmission would be replaced by ECUs for electrical architecture and battery management systems.

Moreover, the conventional diagnostic systems are anticipated to be replaced entirely by onboard diagnostic systems that would continually monitor the health of all the electric and mechanical components of the vehicle.

Asia-Pacific Anticipated to Dominate the ECU Market

Asia-Pacific dominates the automotive electronic control unit market due to a rise in the demand for in-vehicle infotainment and communication applications in passenger vehicles, increased disposable income, and a rise in automobile production in this region.

Electrification in the Asia-Pacific region has witnessed a high penetration rate due to the presence of China and Japan, as China is the leading market for electric vehicles, and most automakers advancing in electric vehicle technology are from Japan. This development in electric vehicles can be correlated to the increased demand in the market for ECU in the region, which currently holds the highest market share in terms of both revenue and volume.

North America is also expected to witness growth in the automotive electronic control unit market due to increased demand for luxury cars, growing demand for energy-efficient vehicles, and strict government regulations to reduce carbon emissions in this region.

The European automotive ECU market is growing as infotainment & communication applications are experiencing high demand for their implementation in luxury & passenger vehicles. The growing focus on providing luxury and comfort features by leading automotive manufacturers present in European countries, including Germany, Italy, etc., is further creating opportunities for the market's growth.

Automotive Electronic Control Unit Industry Overview

The automotive electronic control unit market is dominated by players such as Lear Corporation, Robert Bosch GmbH, Nidec Corporation, Continental AG, and Delphi Technologies, among others. Companies worldwide are adopting various innovative technologies and investing in R&D projects. Moreover, manufacturers are expanding their networks by developing dealership and distribution networks globally to gain profits and strengthen their industry presence. For instance,

In October 2021, Motherson extended its cooperation with Marelli Automotive Lighting (Marelli) for a new tool room in India. This will be the first of its kind tool room in India dedicated to specific lighting applications. The toolroom will be an extension of the existing joint venture company Marelli Motherson Automotive Lighting India Private Limited. The 50/50 JV was established in 2008 to address the Indian exterior lighting market, and now it has four plants in India.

In March 2020, Robert Bosch GmBH and Nikola Motor Company formed a partnership to develop a fuel cell truck with a capacity of 40 ton. The key element of the advanced truck system is the Bosch vehicle control unit, which provides higher computing power for advanced functions while reducing the number of independent units. The VCU supports future innovations by providing a scalable platform for the complex e/e architecture, which is essential to support the advanced features of Nikola's trucks.

In October 2021, ZF announced that one million units of its active rear-axle steering system AKC (Active Kinematics Control) had been produced since its launch in 2013. AKC enables agility, safety, and comfort in numerous driving situations.

Owing to the abovementioned instances and developments, players in the automotive electronic control unit market are anticipated to focus on capturing the majority of the market share and are likely to expand their geographical presence during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Propulsion

- 5.1.1 Internal Combustion Engine

- 5.1.2 Hybrid

- 5.1.3 Battery Electric Vehicle

- 5.2 By Application

- 5.2.1 ADAS and Safety System

- 5.2.2 Body Control and Comfort System

- 5.2.3 Infotainment and Communication System

- 5.2.4 Powertrain System

- 5.3 By ECU

- 5.3.1 16-bit ECU

- 5.3.2 32-bit ECU

- 5.3.3 64-bit ECU

- 5.4 By Autonomy

- 5.4.1 Conventional Vehicle

- 5.4.2 Semi-autonomous Vehicle

- 5.4.3 Autonomous Vehicle

- 5.5 By Vehicle

- 5.5.1 Passenger Car

- 5.5.2 Commercial Vehicle

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 US

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 UK

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.4.1 South America

- 5.6.4.2 Middle-East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Lear Corporation

- 6.2.2 Robert Bosch GmbH

- 6.2.3 Nidec Corporation

- 6.2.4 Continental AG

- 6.2.5 Aptiv PLC

- 6.2.6 Leopold Kostal GmbH & Co. KG

- 6.2.7 ZF Friedrichshafen AG

- 6.2.8 Autoliv Inc.

- 6.2.9 Magneti Marelli

7 MARKET OPPORTUNITIES AND FUTURE TRENDS**

汽车电控系统市场(按应用、推进类型、车辆类型、分销管道、自主水平和电子架构)—2025-2032 年全球预测电子控制管理市场按产品类型、技术、安装类型、应用和最终用户产业划分-2025-2032 年全球预测硬体在环 (HIL) 模拟市场(按类型、组件、测试类型、应用和最终用户划分)- 2025-2032 年全球预测

汽车电控系统市场(按应用、推进类型、车辆类型、分销管道、自主水平和电子架构)—2025-2032 年全球预测电子控制管理市场按产品类型、技术、安装类型、应用和最终用户产业划分-2025-2032 年全球预测硬体在环 (HIL) 模拟市场(按类型、组件、测试类型、应用和最终用户划分)- 2025-2032 年全球预测 2032 年自主群体控制软体市场预测:按类型、组件、演算法、部署模式、应用、最终用户和地区进行的全球分析球栅阵列封装市场按类型、材料类型、间距、应用、最终用户和公司规模划分 - 全球预测 2025-2030

2032 年自主群体控制软体市场预测:按类型、组件、演算法、部署模式、应用、最终用户和地区进行的全球分析球栅阵列封装市场按类型、材料类型、间距、应用、最终用户和公司规模划分 - 全球预测 2025-2030 全球摩托车电控系统市场

全球摩托车电控系统市场 全球汽车电子控制单元市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球汽车电子控制单元市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 2025年全球汽车ECU市场报告

2025年全球汽车ECU市场报告 汽车用电控系统的全球市场:车辆类别,各元件类型,容量类别,各地区,机会,预测,2018年~2032年

汽车用电控系统的全球市场:车辆类别,各元件类型,容量类别,各地区,机会,预测,2018年~2032年 汽车逻辑闸市场,按逻辑闸类型、按技术节点、按整合度、按车辆类型、按应用、按国家和地区 - 2025 年至 2032 年全球产业分析、市场规模、市场份额和预测

汽车逻辑闸市场,按逻辑闸类型、按技术节点、按整合度、按车辆类型、按应用、按国家和地区 - 2025 年至 2032 年全球产业分析、市场规模、市场份额和预测