|

市场调查报告书

商品编码

1687302

热塑性聚酯弹性体(TPE-E)-市场占有率分析、产业趋势与统计、成长预测(2025-2030)Thermoplastic Polyester Elastomer (TPE-E) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

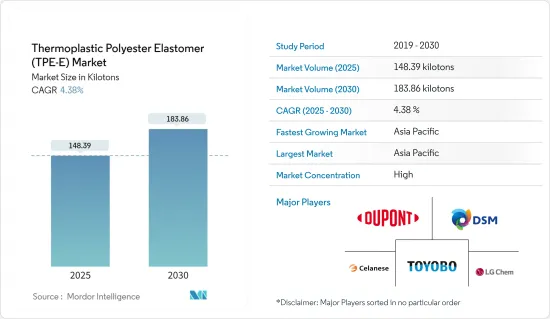

热塑性聚酯弹性体的市场规模预计在 2025 年为 148.39 千吨,预计到 2030 年将达到 183.86 千吨,预测期(2025-2030 年)的复合年增长率为 4.38%。

2020年市场受到了新冠疫情的负面影响。疫情对汽车产业造成了严重衝击,包括全球范围内的生产中断和供应链中断,对市场产生了负面影响。然而,由于汽车行业的成长,市场在 2021 年復苏良好。

关键亮点

- 短期内,汽车产业需求的增加以及医疗保健和医疗设施支出的增加是推动市场成长的关键因素。

- 然而,热塑性聚酯弹性体的高成本是预测期内限制该产业成长的主要因素。

- 生物基热塑性聚酯弹性体市场的兴起预计很快就会为全球市场提供丰厚的成长机会。

- 由于中国、日本和其他东南亚国家对热塑性聚酯弹性体 (TPE-E) 的需求很高,加上汽车生产和医疗行业对 TPEE 的使用量持续增加,预计亚太地区在评估期内的研究市场将出现健康成长。

热塑性聚酯弹性体(TPE-E)市场趋势

在汽车产业的应用日益广泛

- 热塑性聚酯弹性体 (TPE-E) 是一种高性能材料,在汽车产业的应用正在迅速扩大。 TPE-E 在汽车领域的应用范围从外部和内部零件到引擎零件。 TPE-E凭藉其高耐用性、轻盈性、成本绩效,获得了汽车材料厂商的大力支持。

- TPE-E 在汽车行业有多种应用,包括生产高品质汽车仪錶面板、CVJ 防尘罩、车轮罩、进气管、安全气囊展开门、仪表板组件、立柱饰板、门衬里和把手、座椅靠背和安全带组件。

- TPE-E 具有出色的耐磨性和抗震性,并且可以染成任何颜色,从而具有很高的设计自由度。 TPE-E 即使在恶劣的天气条件下也非常耐用,因此成为汽车锁等内部机构的热门选择。这些特性也支持了电动车製造对长期耐热材料的需求。

- 汽车产业致力于将轻量材料应用于各种车辆。因此,全球汽车产业的成长预计将推动对 TPE-E 的需求。

- 根据 OICA 的数据,2021 年全球汽车总销量为 80,154,988 辆,而 2020 年为 12,452,453 辆,成长了 3%。

- 印度和中国已经实施了汽车报废政策,以淘汰过时的汽车并最大限度地减少污染。该计划的目标是淘汰 51,000 辆车超过 20 年的轻型汽车和 34,000 辆车龄超过 15 年的轻型汽车。该计划旨在透过逐步淘汰没有有效适用证书的老旧和无法运行的车辆来减少污染。预计这种方法将增加市场对新车的需求。

- 2021年全年全球电动车销量达6.75亿辆,较2020年成长108%。这个数字包括乘用车、轻型卡车和轻型商用车。 2021 年,纯电动车占电动车销量的 71%,而插电式混合动力车占 29%。

- 国际能源总署预测,在新政策情境下,预计2030年全球电动车销售将达到1.25亿辆(不包括两轮车和三轮车)。根据EV30@30情景,预计到2030年中国约70%的汽车销售将是电动车。销售额数据,估计欧洲占电动车销售的50%,日本占37%,加拿大和美国占30%,印度占29%。

- 因此,由于上述因素,预计预测期内对 TPE-E 的需求将受到正面影响。

亚太地区占市场主导地位

- 预计亚太地区将主导市场。以国内生产毛额计算,中国是该地区最大的经济体。中国是成长最快的经济体之一,目前是世界上最大的製造业基地之一。该国的製造业是该国经济的主要贡献者之一。

- 中国是世界上最大的汽车製造国。由于人们日益关注环境问题,该国的汽车产业正在不断发展,重点是製造确保燃油效率同时最大限度减少排放气体的产品。据 OICA 称,预计该国 2021 年汽车产量将达到 2,608 万辆,比 2020 年的 2,523 万辆增长 3%,到 2025 年将增长到 3,500 万辆。汽车产量的成长预计将推动该国电动车和内燃机汽车製造领域对热塑性聚酯弹性体的需求。

- 中国拥有完善的一般工业部门。中国国家统计局发布的资料显示,2021年全国工业增加与前一年同期比较增9.6%。该国2021年12月工业生产年增4.3%(季增0.42%),增加了该国对热塑性聚酯弹性体的需求。

- 中国拥有世界上最大的电子产品製造基地之一,对韩国、新加坡和台湾等现有的上游製造商构成了激烈的竞争。智慧型手机、OLED 电视和平板电脑等电子产品在市场消费性电子领域的需求成长最快。中国经济发展和人民生活水准的提高,带动了电子产品的需求。

- 收入的持续提高将导致人口人均可支配收入的增加,预计将有利于中国对电子产品的需求。中产阶级和高所得群体的扩大预计将推动电子产品的需求。根据中国国家统计局的数据,2021年家用电子电器及电器产品领域的销售额达到9.3464亿元人民币(约1.3127亿美元)。预计销售额将以每年2.04%的速度成长,到2025年市场规模预计将达到1,756.7亿美元。

- 此外,根据 OICA 的数据,2021 年印度汽车产量约为 4,399,112 辆,比 2020 年的 3,381,819 辆成长 30%。

- 此外,预计到 2022 年,该国的医疗保健产业规模将达到 3,720 亿美元,主要原因是健康意识增强、保险覆盖率广、收入增加以及疾病增加。印度的医疗保健产业受惠于每年1.6%的人口成长率。

- 近年来,印度工业部门快速成长。印度工业生产指数(IIP)从 2020-21 年的 111.7 上升至 2021-22 年的 128.7。这一增长也得到了政府各项倡议的支持,例如国家製造业计划(旨在到 2025 年将製造业在 GDP 中的份额提高到 25%)和针对製造商的 PLI 计划(于 2022 年启动),从而增加了该国对热塑性聚酯弹性体的需求。

- 据印度品牌资产基金会(IBEF)称,到2025年,印度电子製造业的规模预计将达到5,200亿美元。由于政府推出的「印度製造」、「国家电子产品计画」、「电子设备零净进口」和「零缺陷效应」等倡议,印度的电气和电子设备製造业预计将快速成长。这些措施致力于发展国内製造业,减少进口依赖,促进出口和製造业,并使国家自力更生,正如「印度製造」计画所体现的那样。

- 由于所有这些因素,预计该地区的热塑性聚酯弹性体市场在预测期内将稳定成长。

热塑性聚酯弹性体(TPE-E)产业概况

全球热塑性聚酯弹性体(TPE-E)市场呈现整合态势,顶级上市公司占据全球市场的大部分份额。全球公司正大力进行研发、收购和合作,以开发新技术并提高其市场占有率和实力。研究的市场中的关键製造商包括杜邦、塞拉尼斯公司、荷兰皇家帝斯曼集团、LG化学、东洋纺等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 汽车产业需求增加

- 增加医疗保健和医疗设施支出

- 限制因素

- 热塑性聚酯弹性体高成本

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔

- 类型

- 射出成型级

- 挤压等级

- 其他的

- 最终用户产业

- 车

- 医疗保健

- 工业的

- 电气和电子

- 消费品

- 其他的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业策略

- 公司简介

- Celanese Corporation

- Chang Chun Group

- DSM

- Kolon Plastic Inc.

- LG Chem

- Mitsubishi Chemical Corporation

- Radici Partecipazioni SpA

- Sichuan Sunshine Plastics Co. Ltd

- SK Chemicals

- Toyobo Co. Ltd

第七章 市场机会与未来趋势

- 生物基热塑性聚酯弹性体的新兴市场

The Thermoplastic Polyester Elastomer Market size is estimated at 148.39 kilotons in 2025, and is expected to reach 183.86 kilotons by 2030, at a CAGR of 4.38% during the forecast period (2025-2030).

The market was negatively impacted by COVID-19 in 2020. The pandemic had a severe impact on the automotive industry, including manufacturing interruptions and disruption in the supply chain across the globe, thereby negatively affecting the market. However, the market recovered steadily, owing to the increased growth of the automotive industry in 2021.

Key Highlights

- Over the short term, growing demand from the automotive industry, coupled with growing expenditure on healthcare and medical facilities, are major factors driving the growth of the market studied.

- However, the high cost of thermoplastic polyester elastomer is a key factor anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the emerging market for bio-based thermoplastic polyester elastomer is likely to create lucrative growth opportunities for the global market soon.

- Asia-Pacific is estimated to witness healthy growth over the assessment period in the studied market due to the high demand for thermoplastic polyester elastomer (TPE-E) in China, Japan, and other Southeast Asian countries owing to continuous and rising usage of TPEE in automotive production, coupled with the growing medical industry.

Thermoplastic Polyester Elastomer (TPE-E) Market Trends

Increasing Usage in the Automotive Industry

- Thermoplastic polyester elastomers (TPE-E) are high-performance materials whose application in the automotive industry has rapidly increased. TPE-E utilization in the automotive sector extends from the exterior and interior parts to engine components. The high durability, light weight, and cost-effectiveness of TPE-Es make them extremely coveted by automotive materials manufacturers.

- TPE-Es serve the automotive industry in several applications, some of which include the manufacturing of high-quality automotive instrument panels, CVJ boots, wheel covers, air intake ducting, airbag deployment doors, dashboard components, pillar trim, door liners and handles, seat backs, and seat belt components, among others.

- TPE-Es offer high design flexibility by being resistant to abrasion and vibration and dyeable in any desired color. They are highly durable in harsh weather conditions; hence they are preferred for internal mechanisms such as car locks. These properties also support the demand for long-term heat-resistant materials in electric vehicle fabrication.

- The automotive industry is working on utilizing lightweight materials for various vehicle applications. Hence, the growing automotive industry globally is expected to boost the demand for TPE-Es.

- According to OICA, the global sales of all vehicles in 2021 acoounted for 80,154,988 units, registering a growth of 3% as compared to 12,452,453 units sold in 2020.

- Vehicle scrappage policies are being implemented in India and China to scrap outdated vehicles and minimize pollution. It plans to cover 51 lakh light motor vehicles older than 20 years and 34 lakh light motor vehicles older than 15 years. This program aims to reduce pollution by phasing out obsolete or inoperable vehicles that do not have a valid fitness certificate. This approach will raise market demand for new cars.

- The global EV sales reached 675 million units in the entire year of 2021, 108% more as compared to the EV sales in 2020. This volume includes passenger vehicles, light trucks, and light commercial vehicles. The BEVs stood for 71% of total EV sales, while the PHEVs stood at 29% in 2021.

- According to the IEA, in 2030, global electric vehicle sales are expected to reach 125 million, per the New Policies Scenario (excluding two/three-wheelers). In the EV30@30 Scenario, in 2030, around 70% of vehicle sales in China are expected to be EVs. Also, as per the approximate sales value till now, EV sales in Europe was estimated at 50%, while it was 37% in Japan, 30% in Canada and the United States, and 29% in India.

- Therefore, owing to the above factors, the demand for TPE-E is expected to be impacted positively during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the market. In the region, China is the largest economy in terms of GDP. China is one of the fastest emerging economies and has become one of the biggest production houses in the world today. The country's manufacturing sector is one of the primary contributors to the country's economy.

- China is the largest manufacturer of automobiles in the world. The country's automotive sector has been shaping up for product evolution, focusing on manufacturing products to ensure fuel economy while minimizing emissions, owing to the growing environmental concerns. In 2021, according to the OICA, the automotive production in the country reached 26.08 million, which increased by 3%, compared to 25.23 million vehicles produced in 2020, and is expected to grow up to 35 million vehicles by 2025. The increase in automotive production is estimated to drive the demand for thermoplastic polyester elastomers in the country from both EVs and IC engine vehicle manufacturing sectors.

- China has a well-established general industrial sector. According to the data published by China's National Bureau of Statistics, the country's value-added industrial output went up 9.6% Year-on-Year in 2021. The country's industrial output grew 4.3% Y-o-Y in December 2021 (a 0.42 % increase from November), thereby increasing the demand for thermoplastic polyester elastomers in the country.

- China has one of the world's largest electronics production bases and offers tough competition to the existing upstream producers, such as South Korea, Singapore, and Taiwan. Electronic products, such as smartphones, OLED TVs, and tablets, have the highest growth rates in the consumer electronics segment of the market in terms of demand. Economic development in China and improving living standards among the population drive the demand for electronic goods.

- The continuous growth of income resulted in the rise in the population's per capita disposable income, which is expected to benefit the demand for electronic goods in China. The expansion of the middle class and high-income population group is expected to propel the demand for electronics. According to the National Bureau of Statistics of China, the revenue in the consumer electronics and household appliances segment reached CNY 934.64 million (approx. USD 131.27 million) in 2021. The revenue is expected to show an annual growth rate of 2.04%, resulting in a projected market volume of USD 175,670 million by 2025.

- Further, in India, as per OICA, around 4,399,112 vehicles were produced in 2021, which increased by 30%, comparison to 3,381,819 units manufactured in 2020.

- Also, the healthcare sector in the country is expected to reach USD 372 billion by 2022, mainly driven by increasing health awareness, access to insurance, rising income, and diseases. The medical sector in India is benefiting from the growing population at a rate of 1.6 % per year.

- India has witnessed rapid growth in the industrial sector in recent years. The index of industrial production (IIP) in India increased from 111.7 in 2020-21 to 128.7 in the 2021-22 period. This growth is also supported by various government initiatives like the National Manufacturing Policy (which aims to increase the share of manufacturing in GDP to 25% by 2025) and the PLI scheme for manufacturing (which was launched in 2022), thereby increasing the demand for thermoplastic polyester elastomers in the country.

- According to the India Brand Equity Foundation (IBEF), the Indian electronics manufacturing industry is expected to reach USD 520 billion by 2025. Electrical and electronics production in India is expected to increase rapidly due to government initiatives with policies, such as Make in India, the National Policy of Electronics, Net Zero Imports in Electronics, and the Zero Defect Zero Effect. Such policies offer a commitment to growth in domestic manufacturing, lowering import dependence and energizing exports and manufacturing, like the 'Make in India' program, to make the country self-reliant.

- Due to all such factors, the market for thermoplastic polyester elastomer in the region is expected to have a steady growth during the forecast period.

Thermoplastic Polyester Elastomer (TPE-E) Industry Overview

The global thermoplastic polyester elastomer (TPE-E) market is consolidated in nature, as the top listing companies hold a significant share of the global market. Global companies are significantly focusing on R&D, acquisitions, and collaborations to develop new technologies and to increase their market presence and foothold. The major manufacturers in the market studied include Dupont, Celanese Corporation, Koninklijke DSM N.V., LG Chem, and Toyobo Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand From the Automotive Industry

- 4.1.2 Growing Expenditure on Healthcare And Medical Facilities

- 4.2 Restraints

- 4.2.1 High Cost of Thermoplastic Polyester Elastomer

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Injection Molding Grade

- 5.1.2 Extrusion Grade

- 5.1.3 Other Types

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Healthcare

- 5.2.3 Industrial

- 5.2.4 Electrical and Electronics

- 5.2.5 Consumer Goods

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Celanese Corporation

- 6.4.2 Chang Chun Group

- 6.4.3 DSM

- 6.4.4 Kolon Plastic Inc.

- 6.4.5 LG Chem

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 Radici Partecipazioni SpA

- 6.4.8 Sichuan Sunshine Plastics Co. Ltd

- 6.4.9 SK Chemicals

- 6.4.10 Toyobo Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Market for Bio-based Thermoplastic Polyester Elastomer

弹性体市场分析及预测(至2035年):类型、产品、应用、技术、最终用户、形态、材料类型、组件、製程、安装类型

弹性体市场分析及预测(至2035年):类型、产品、应用、技术、最终用户、形态、材料类型、组件、製程、安装类型 2026-2034年全球阀门软座弹性体市场规模、份额、趋势和成长分析报告全球丁基弹性体市场规模、份额、趋势和成长分析报告(2026-2034年)全球耐热弹性体市场规模、份额、趋势和成长分析报告(2026-2034年)超弹性材料全球市场规模、份额、趋势和成长分析报告(2026-2034)

2026-2034年全球阀门软座弹性体市场规模、份额、趋势和成长分析报告全球丁基弹性体市场规模、份额、趋势和成长分析报告(2026-2034年)全球耐热弹性体市场规模、份额、趋势和成长分析报告(2026-2034年)超弹性材料全球市场规模、份额、趋势和成长分析报告(2026-2034) 弹性体市场 - 全球产业规模、份额、趋势、机会及预测(按类型、热塑性塑胶、应用、地区和竞争格局划分,2021-2031年)

弹性体市场 - 全球产业规模、份额、趋势、机会及预测(按类型、热塑性塑胶、应用、地区和竞争格局划分,2021-2031年) 工业热塑性聚氨酯弹性体市场按产品类型、硬度、加工製程、形状、应用和最终用途产业划分-2026-2032年全球预测

工业热塑性聚氨酯弹性体市场按产品类型、硬度、加工製程、形状、应用和最终用途产业划分-2026-2032年全球预测 高性能弹性体市场预测至2032年:按类型、加工方法、应用、最终用户和地区分類的全球分析

高性能弹性体市场预测至2032年:按类型、加工方法、应用、最终用户和地区分類的全球分析 弹性体:应用及全球市场

弹性体:应用及全球市场 再生弹性体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

再生弹性体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)