|

市场调查报告书

商品编码

1444455

全球工业润滑油市场:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Industrial Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

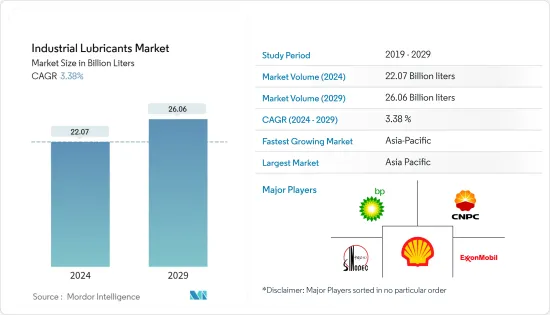

据预测,2024年全球工业润滑油市场规模将达到220.7亿公升,2024-2029年预测期间复合年增长率为3.38%,到2029年将达到260.6亿公升。

2020 年的市场受到了 COVID-19 的负面影响。然而,疫情对工业活动中的自动化流程产生了大规模的正面影响。由于大流行而导致的劳动力供应有限、工作场所保持安全距离的需要以及各种个人防护设备的使用正在加速各行业自动化的采用。此外,生产率的提高也增加了机器的运作时间和设备速度,增加了承载能力设备适当润滑的重要性,增加了所研究市场的需求。

主要亮点

- 短期内,风力发电产业需求的增加预计将推动市场成长。

- 然而,润滑油对环境的负面影响可能会阻碍所研究市场的成长。

- 然而,生物润滑剂的日益突出和低黏度润滑剂的开发可能成为研究市场的成长机会。

- 亚太地区主导全球市场,大部分消费来自中国、印度和印尼等国家。

工业润滑油市场趋势

发电业主导市场

- 发电是全球经济最重要的部门之一,没有发电,几乎所有製造业务都可能停止。製造技术的进步使各种新工厂运作,增加了各个最终用户行业的电力需求。

- 涡轮机在发电能源领域发挥重要作用。涡轮机广泛用于发电,无论电力源为何,例如风能、太阳能、水力发电或火力发电。在发电过程中,涡轮机释放大量的热。一般来说,除了涡轮机外,发电领域使用的主要零件还包括泵浦、轴承、风扇、压缩机、齿轮和液压系统。风力发电机受到许多因素的影响,例如湿度、高压、高负载、振动和温度。齿轮油和透平油广泛用于该领域的润滑目的。

- 许多公司已经意识到,降低机器生命週期内的总拥有成本 (TCO) 是从投资中获得最大价值的关键。然而,润滑对 TCO 的影响常常被低估。

- 通常,润滑油成本占发电公司总营运费用的比例不到 5%。根据一项行业调查,大约 58% 的公司认识到他们选择的润滑剂可以节省 5% 或更多的成本,但他们认识到润滑剂的影响可能高达 6 倍。不到十分之一的公司( 8%) 有

- 在水力发电中,润滑油用于空气压缩机、齿轮、涡轮机、循环油系统、液压设备、轴承等。消耗的润滑油包括润滑脂、一般润滑油、传动油、透平油、液压油等。在核能发电厂中,润滑油(透平油)主要用于蒸气涡轮以提高效率。

- 燃煤发电厂的空气压缩机、油压设备、涡轮机、移动设备、轴承、齿轮等都使用润滑油。煤炭挖土机系统还消耗各种类型的润滑油,如齿轮油、润滑脂、变速箱油、液压油等。燃煤发电厂消耗高温、耐用的润滑油。

- 因此,所有这些因素和趋势预计将在全球经济从疫情中復苏后推动润滑油的需求。

亚太地区主导市场

- 由于中国、印度和印尼等国家消费量的增加,亚太地区已成为锂消费的主要市场。

- 目前,中国已成为最大的润滑油和润滑脂消费国。涉及各行业的大规模製造活动以及工业和汽车行业的快速成长使该国成为形势领先的润滑油消费国和生产国之一。

- 2021年,中国经济高层批准了90个固定资产投资计划,为促进发展做出了贡献。 2021年,发改委核准投资计划1,220亿美元,主要投向交通、能源、节水、资讯科技等领域。根据最新统计,2021年中国固定资产投资超过54.45兆元(约7.68兆美元),与前一年同期比较增4.9%,较2019年同期成长8%。随着2021年及以后财政和金融支持的增加,该国有潜力和奖励扩大有效投资。

- 此外,中国正在重点发展新型基础设施,在不久的将来,新基础设施的建设将占固定资产的大部分。由于支出增加和政府对基础设施发展的关注,预计未来建设活动将继续增长。

- 中国工业协会公布的数据显示,2021年汽车累计产量2,608.2万辆,与前一年同期比较增加3.4%。中国汽车工业协会预测,2022年及以后汽车市场可能会持续保持稳定成长。

- 印度是该地区第二大润滑油消费国,也是仅次于美国和中国的世界第三大润滑油消费国。该国约占全球润滑油市场需求的 7%。虽然工业润滑油市场本质上是分散的,但印度润滑脂市场本质上是高度一体化的,排名前五的公司占据了75%以上的市场占有率。

- 有利的政府政策,例如将 FAME-II 计划延长至 2024 年、加强对两轮车的奖励以及针对汽车和汽车零部件行业推出生产连结奖励计画(PLI) 计划(价值 2600 亿卢比)(约 PLI)卢比的先进化学电池。

- 印尼(世界第四人口大国)由于人口众多、都市化程度高、中产阶级迅速崛起,近年来成为潜在的润滑油市场之一。近年来,采矿、纺织和基础设施等产业的工业润滑油消耗量不断增加。

- 根据印尼食品和饮料企业家协会 (GAPMMI) 预测,到 2021 年,食品和饮料产业预计将成长 7%。据印尼统计局Badan Pusat Statistik称,大中型製造业产出为负值。 2021年增长率为8.01%。

- 印尼政府计划在2024年投资约4,120亿美元用于建设计划,包括兴建25个机场和住宅。此类投资是政府加强国家成长目标的一部分。然而,供应链中断预计将在短期内扰乱该行业最初预期的成长途径。

- 因此,所有上述因素都可能对未来所研究的市场产生重大影响。

工业润滑油产业概况

全球工业润滑油市场本质上是分散的。市场主要企业包括荷兰皇家壳牌公司、埃克森美孚公司、中国石油化学股份有限公司、中国石油天然气集团公司、英国石油公司(嘉实多)等。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 风力发电产业的需求不断增加

- 其他司机

- 抑制因素

- 润滑油对环境的负面影响

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章市场区隔

- 产品类别

- 机油

- 变速箱/液压油

- 金属加工液

- 一般工业油

- 齿轮油

- 润滑脂

- 加工油

- 其他产品类型

- 最终用户产业

- 发电

- 重型机械

- 食品与饮品

- 冶金/金属加工

- 化学製造

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 菲律宾

- 印尼

- 马来西亚

- 泰国

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 俄罗斯

- 土耳其

- 西班牙

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 智利

- 南美洲其他地区

- 中东

- 沙乌地阿拉伯

- 伊朗

- 伊拉克

- 阿拉伯聯合大公国

- 科威特

- 其他中东地区

- 非洲

- 埃及

- 南非

- 奈及利亚

- 阿尔及利亚

- 摩洛哥

- 其他非洲

- 亚太地区

第六章 竞争形势

- 合併、收购、合资、合作和协议

- 市场占有率(%)分析

- 主要企业采取的策略

- 公司简介

- Amsoil Inc.

- Bharat Petroleum Corporation Limited

- Blaser Swisslube AG

- BP PLC(Castrol)

- Carl Bechem GmbH

- Chevron Corporation

- China National Petroleum Corporation(PetroChina)

- China Petroleum &Chemical Corporation(SINOPEC Group)

- Eni SpA

- Exxon Mobil Corporation

- FUCHS

- Gazprom Neft PJSC

- Gulf Oil International

- HPCL

- Idemitsu Kosan Co. Ltd

- Indian Oil Corporation Ltd

- ITW(ROCOL)

- ENEOS

- Kluber Lubrication

- Lukoil Lubricants Company

- PT Pertamina

- Petrobras

- Petronas Lubricants International

- Phillips 66 Lubricants

- Repsol

- Royal Dutch Shell PLC

- Tide Water Oil Co.(India)Ltd

- TotalEnergies

- Valvoline Inc.

第七章市场机会与未来趋势

- 生物润滑剂日益受到关注

- 低黏度润滑油的开发

The Industrial Lubricants Market size is estimated at 22.07 Billion liters in 2024, and is expected to reach 26.06 Billion liters by 2029, growing at a CAGR of 3.38% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. However, the pandemic has affected the automation process in industrial activities on a large scale in a positive way. The limited availability of manpower due to the pandemic, the need to keep a safe distance in working places, and the use of various personal protective equipment have accelerated the adoption of automation throughout industries. Moreover, the increase in productivity has also increased the run time of the machinery and the speed of the equipment, which has increased the importance of adequate lubrication on the load-bearing surfaces of the equipment, thus enhancing the demand for the studied market.

Key Highlights

- Over the short term, increasing demand from the wind energy sector is expected to drive the market's growth.

- However, the detrimental effects of lubricants on the environment are likely to hinder the growth of the market studied.

- Nevertheless, the growing prominence of bio-lubricants and the development of low-viscosity lubricants are likely to act as opportunities for the growth of the market studied.

- Asia-Pacific dominates the market across the world, with the most substantial consumption from countries like China, India, and Indonesia.

Industrial Lubricants Market Trends

Power Generation Segment Dominated the Market

- Power generation is one of the most important sectors of the global economy, without which almost all manufacturing operations may cease. Advancements in manufacturing technologies are resulting in the commencement of various new plants, increasing the demand for electricity in various end-user industries.

- Turbines play a key role in the energy sector for generating electricity. Irrespective of the source of electricity, i.e., wind, solar, hydro, thermal, and others, turbines are widely used for power generation. A large amount of heat is emitted from a turbine during the production of electricity. In general, other than turbines, the major components used in the power generation sector include pumps, bearings, fans, compressors, gears, and hydraulic systems. Wind turbines are subjected to many factors, such as humidity, high pressure, high loads, vibrations, and temperature. Gear and turbine oils are widely used in this sector for lubrication purposes.

- Many companies are already aware of the fact that reducing the total cost of ownership (TCO) over the lifetime of machinery is key to extracting the best possible value from the investment. However, the impact of lubrication on the TCO is underestimated too often.

- In general, the cost of lubricants accounts for less than 5% of a power generation company's total operational expenditure. According to an industry survey, about 58% of the companies recognized that lubricant selection could help reduce costs by 5% or more, but fewer than 1 in 10 (8%) companies realized that the impact of lubrication could be up to six times more.

- In hydroelectric power generation, lubricants are used for air compressors, gears, turbines, circulating oil systems, hydraulics, and bearings, among other purposes. The lubricants consumed include greases, general lubricating oils, transmission oils, turbine oils, and hydraulic oils, among others. In nuclear power plants, lubricants (turbine oils) are used mainly for steam turbines for better efficiency.

- In coal-fired power plants, lubricants are used for air compressors, hydraulics, turbines, mobile equipment, bearings, and gears. Coal excavator systems also consume different types of lubricants, including gear oils, greases, transmission oils, and hydraulic oils. Coal-fired power plants consume high-temperature and heavy-duty lubricants.

- Hence, all such factors and trends are expected to drive the demand for lubricants, post the global economic recovery from the pandemic.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific was found to be the major market for the consumption of lithium, owing to increasing consumption from countries such as China, India, and Indonesia.

- China is the largest consumer of lubricants and greases in the current scenario. The vast manufacturing activities pertaining to different sectors and the rapid growth in the industrial and automotive sectors have pushed the country to stand among the major lubricant consumers and producers in the global landscape.

- In 2021, China's top economic planner sanctioned 90 fixed-asset investment projects, helping increase development. In 2021, the National Development and Reform Commission approved USD 122 billion in investment projects, mostly in the transportation, energy, water conservation, and information technology sectors. According to the current statistics, China's fixed-asset investment increased by 4.9% Y-o-Y to over CNY 54.45 trillion (~USD 7.68 trillion) in 2021, up 8% from the same period in 2019. With enhanced fiscal and monetary support beyond 2021, the country has the potential and incentive to expand effective investments.

- In addition, China has been focusing on new infrastructure, with construction being the majority type of fixed assets, in the near future. Such growth in construction activity is expected to be witnessed in the future, owing to increased expenditure and the government's focus on infrastructure growth.

- The China Association of Automobile Manufacturers (CAAM) reported cumulative motor vehicle production levels for 2021, which were 26.082 million units, up by 3.4% Y-o-Y. CAAM predicts the motor vehicle market may continue to record steady growth in 2022 and beyond.

- India is the second-largest lubricant consumer in the region and the third-largest in the world, after the United States and China. The country accounts for about 7% of the demand in the global lubricants market. While the industrial lubricants market is fragmented in nature, the Indian grease market is highly consolidated in nature, with the top five players accounting for more than 75% of the market share.

- Favorable government policies, such as the extension of the FAME-II scheme until 2024, the enhancement of incentives for two-wheelers, the launch of the production-linked incentive (PLI) scheme for the auto and auto component sector (worth INR 26,000 crore (~USD 3.20 billion)), and the PLI for advanced chemistry cell worth INR 18,000 crore (~USD 2.22 trillion), are likely to provide significant support to the sector as it adopts advanced technologies.

- Indonesia (the world's fourth-largest populated country) has been among the potential lubricants markets in recent years on account of its huge population, high urbanization, and rapidly rising middle class. Sectors such as mining, textile, and infrastructure have been driving the consumption of industrial lubricants in the recent past.

- According to the Indonesian Food and Beverage Entrepreneurs Association (GAPMMI), the food and beverage industry is estimated to rise by 7% by 2021. As per Badan Pusat Statistik (Statistics Indonesia), the production output from large and medium manufacturing industries exhibited a negative growth of 8.01% in 2021.

- The Government of Indonesia has been planning to invest about USD 412 billion in building projects, including constructing 25 airports, residential complexes, etc., by 2024. Such investments are part of the government's target to seek to strengthen growth in the country. However, the disruption in the supply chain is expected to hinder the initially expected growth path of the sector in the short term.

- Therefore, all the aforementioned factors are likely to significantly impact the market studied in the future.

Industrial Lubricants Industry Overview

The global industrial lubricants market is fragmented in nature. Some of the key players in the market include Royal Dutch Shell PLC, Exxon Mobil Corporation, China Petroleum & Chemical Corporation, China National Petroleum Corporation, and BP PLC (Castrol), among other companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Wind Energy Sector

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Detrimental Effects of Lubricants on the Environment

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Engine Oil

- 5.1.2 Transmission and Hydraulic Fluid

- 5.1.3 Metalworking Fluid

- 5.1.4 General Industrial Oil

- 5.1.5 Gear Oil

- 5.1.6 Grease

- 5.1.7 Process Oil

- 5.1.8 Other Product Types

- 5.2 End-user Industry

- 5.2.1 Power Generation

- 5.2.2 Heavy Equipment

- 5.2.3 Food and Beverage

- 5.2.4 Metallurgy and Metalworking

- 5.2.5 Chemical Manufacturing

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Phillipines

- 5.3.1.6 Indonesia

- 5.3.1.7 Malaysia

- 5.3.1.8 Thailand

- 5.3.1.9 Vietnam

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Turkey

- 5.3.3.7 Spain

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Chile

- 5.3.4.5 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Iran

- 5.3.5.3 Iraq

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Kuwait

- 5.3.5.6 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 Egypt

- 5.3.6.2 South Africa

- 5.3.6.3 Nigeria

- 5.3.6.4 Algeria

- 5.3.6.5 Morocco

- 5.3.6.6 Rest of Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Amsoil Inc.

- 6.4.2 Bharat Petroleum Corporation Limited

- 6.4.3 Blaser Swisslube AG

- 6.4.4 BP PLC (Castrol)

- 6.4.5 Carl Bechem GmbH

- 6.4.6 Chevron Corporation

- 6.4.7 China National Petroleum Corporation (PetroChina)

- 6.4.8 China Petroleum & Chemical Corporation (SINOPEC Group)

- 6.4.9 Eni SpA

- 6.4.10 Exxon Mobil Corporation

- 6.4.11 FUCHS

- 6.4.12 Gazprom Neft PJSC

- 6.4.13 Gulf Oil International

- 6.4.14 HPCL

- 6.4.15 Idemitsu Kosan Co. Ltd

- 6.4.16 Indian Oil Corporation Ltd

- 6.4.17 ITW (ROCOL)

- 6.4.18 ENEOS

- 6.4.19 Kluber Lubrication

- 6.4.20 Lukoil Lubricants Company

- 6.4.21 PT Pertamina

- 6.4.22 Petrobras

- 6.4.23 Petronas Lubricants International

- 6.4.24 Phillips 66 Lubricants

- 6.4.25 Repsol

- 6.4.26 Royal Dutch Shell PLC

- 6.4.27 Tide Water Oil Co. (India) Ltd

- 6.4.28 TotalEnergies

- 6.4.29 Valvoline Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Prominence for Bio-Lubricants

- 7.2 Development of Low Viscosity Lubricants

2025-2029年全球工业润滑油市场

2025-2029年全球工业润滑油市场 工业润滑脂市场按基础油类型、增稠剂类型、最终用途行业和地区划分

工业润滑脂市场按基础油类型、增稠剂类型、最终用途行业和地区划分 全球工业润滑油市场:产业分析、规模、占有率、成长、趋势与预测,2025 年至 2032 年

全球工业润滑油市场:产业分析、规模、占有率、成长、趋势与预测,2025 年至 2032 年 2025-2033 年按产品类型、基础油、最终用途产业和地区分類的工业润滑油市场报告工业润滑油市场:按类型、基础油、按产品类型、按最终用户 - 2025-2030 年全球预测

2025-2033 年按产品类型、基础油、最终用途产业和地区分類的工业润滑油市场报告工业润滑油市场:按类型、基础油、按产品类型、按最终用户 - 2025-2030 年全球预测 全球工业润滑油市场规模研究(按产品、应用和区域预测 2022-2032)

全球工业润滑油市场规模研究(按产品、应用和区域预测 2022-2032) 全球工业润滑油市场 2024-2031

全球工业润滑油市场 2024-2031 工业润滑油的全球市场:基础油(矿物油、合成油、生物基油)、产品类型(液压油、金属加工油、润滑脂)、最终用途产业(建筑、发电、食品加工)和地区.预测(~-2029)

工业润滑油的全球市场:基础油(矿物油、合成油、生物基油)、产品类型(液压油、金属加工油、润滑脂)、最终用途产业(建筑、发电、食品加工)和地区.预测(~-2029) 全球工业润滑油市场

全球工业润滑油市场 重型设备润滑油市场 – 2023 年至 2028 年预测

重型设备润滑油市场 – 2023 年至 2028 年预测