|

市场调查报告书

商品编码

1444523

无菌包装:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Global Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

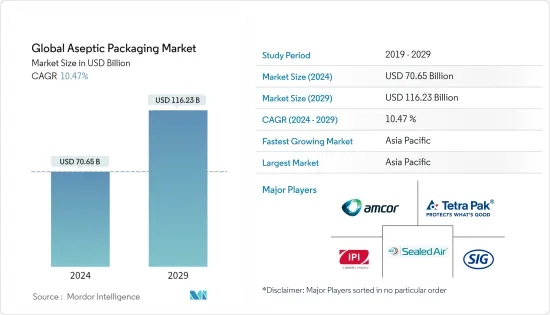

预计2024年全球无菌包装市场规模为706.5亿美元,预计2029年将达到1,162.3亿美元,在预测期间(2024-2029年)成长10.47%,复合年增长率为

无菌包装是指在超高温(UHT)下包装产品,对包装物进行单独灭菌或消毒,然后在无菌气氛下熔合密封,以避免病毒和细菌污染。此外,它保持了包装内容物的质量,并且不需要防腐剂,有利于全球无菌包装市场。

主要亮点

- 永续包装和更长的保质期对于食品和饮料行业的消费者至关重要。因此,出于成本和环境效益的考虑,大多数食品和饮料供应商都转向无菌包装。另外,无菌包装支持可回收的纸盒和环保袋、袋的包装,这些产品往往针对喜欢小容量包装且购买频繁的消费者,因此此类产品的需求将会增加,在全球范围内都非常高。

- 消费者饮食习惯的变化增加了对即食食品的偏好,对方便、优质食品的需求不断增加,为市场成长打开了进一步的大门。全球电子商务销售的适度成长和新兴市场的成长机会预计将为预测期内的无菌包装市场提供重大机会。

- 市场相关人员投资研发以维持在发展中产业的领先地位。新产品的推出也支撑了市场需求。然而,製药业对无菌包装的需求也不断增加。各国政府正在增加医疗保健领域的支出,以促进无菌包装市场的成长。

- 人们越来越认识到一次性塑胶对环境的影响和不可持续的商业行为,导致消费者要求更高标准、更低环境影响的产品。这导致许多市场相关人员转向高成本和永续包装,这可能会阻碍市场成长。

- 由于 COVID-19 的影响,市场大幅成长。疫情促使消费者转向网路零售和恐慌性备货,增加了对牛奶、婴儿食品和蔬菜等必需品的需求。 COVID-19感染疾病大流行影响了开发中国家的无菌包装材料。此外,对无菌包装食品的强劲需求正在推动对该形势的投资。业内相关人员预计医疗保健产业将对包装技术表现出强劲的需求。

无菌包装市场趋势

饮料需求的扩大推动了市场的发展

- 便携式饮料的日益普及和门市数量的增加预计将推动饮料行业的市场成长。不断变化的消费者需求为包装製造商提供了多种选择来满足饮料行业的创新包装需求。

- 消费者经常购买方便且功能性的饮料,例如即饮咖啡和茶、能量饮料以及其他可以随时随地补充营养的饮料。因此,相对健康、天然、具有功能性和实用性的非酒精饮料可以吸引忙碌的消费者。在新产品配方中利用电解质、维生素、矿物质和其他天然成分的天然能量增强特性可以帮助品牌瞄准特定的消费群体。

- 由于蔬菜和水果等多种健康成分,对营养补充饮料和产品的需求不断增加,以及全球对乳基饮料的需求不断增加,预计将在预测期内推动全球功能性增长,这被认为是饮料市场的一个重要因素。

- 健身爱好者对提供精神和身体刺激的即时能量饮料的需求不断增加,预计将在预测期内为机能饮料市场创造重大成长机会。

- 市场上的消费者对健康和保健的意识越来越强。从早晨果汁到能量饮料,我们正在增加在提神的健康趋势的产品上的支出。这一趋势使得饮料包装行业对具有成本效益的包装解决方案产生了很高的需求。牛奶和其他乳类饮料行业对无菌纸盒的需求不断增加,可能会引发市场的进一步活跃,因为纸盒具有易于产品堆迭和延长保质期等优点。

亚太地区将经历最快的成长

- 中国是亚太地区无菌包装的主要消费国之一。食品和饮料消费的成长预计将在预测期内支持市场成长。包装用餐的成长趋势、餐厅和超级市场数量的增加以及瓶装水和饮料消费量的增加是推动该国市场的关键因素。

- 在印度,该行业受到人口成长、收入增加和生活方式改变的推动。最终用户产业的成长前景正在增加对硬质塑胶包装产业的需求。此外,市场扩张产品受到越来越多使用袋包装替代包装的限制。由于包装食品需求的快速增长和可支配收入的增加,印度预计将在亚太无菌包装市场中占据主要份额。

- 在日本,使用杀菌袋的消费者数量正在增加,尤其是酱汁和咖哩。杀菌袋由塑胶和铝层压材料製成,这使得它们能够承受灭菌等热处理,并且可以用作传统罐的替代品。袋装包装比罐装便宜,特别是在进口罐装金属的国家,这是推动日本接受的一个主要因素。

- 澳洲是亚太地区成长最快的包装市场之一。肉类、生鲜食品和加工食品行业正在全国范围内增长。消费者道德关注的不断上升以及健康和福祉的趋势正在维持对本地生产的生鲜食品的需求。此外,该国长期存在的轻食趋势导致一次性和可重复使用袋等包装选项的使用增加。即饮袋装的需求也受到乳製品和新鲜果汁需求稳定成长的推动。

- 在亚太地区,韩国、印尼、越南、泰国、新加坡、孟加拉、台湾和马来西亚等国家也可能占据受访市场的很大份额。

无菌包装产业概述

无菌包装市场竞争激烈,由少数几家大公司主导市场。凭藉主导市场份额,这些领先公司专注于扩大海外客户群。这些公司利用策略合作倡议,透过收购、产品发布等方式增加市场占有率并增强产品能力。市场主要企业包括 Amcor Ltd、IPI SRL (Coesia Group)、Tetra Pak International SA、Sealed 等。 Air Corporation、SIG Combibloc Group、Schott AG。

- SIG 计划于 2023 年 2 月在全球最大的牛奶市场和主要果汁生产国之一的印度建造其第一个无菌装盒工厂。该工厂位于古吉拉突邦。这项投资将用于支援最先进的无菌纸盒包装製造能力,满足严格的印刷和精加工环境标准。

- 2022 年 11 月,Amcor PLC 宣布其目标是使所有无菌产品可回收。 Amcor 正在朝着到 2025 年使所有产品可回收、可重复使用或可堆肥的目标取得进展,公司总生产重量的 74% 已被设计为可回收,并且具有绿色功能的创造性解决方案的数量正在稳步增加。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争公司之间的敌意强度

- 评估 COVID-19 对市场的影响

- 饮料业形势

- 饮料业形势-酒精饮料

- 饮料业形势-非酒精饮料

- 饮料无菌包装 - 需求洞察

第五章市场动态

- 市场驱动因素

- 饮料需求扩大

- 提高可回收玻璃的商业价值

- 市场挑战

- 原物料价格波动

第六章市场区隔

- 副产品

- 纸箱(利乐包、组合块等)

- 袋子和小袋

- 能

- 瓶子

- 其他产品(管瓶、安瓿、注射器、杯子等)

- 按用途

- 饮料

- 即饮饮料

- 乳製品饮料

- 其他饮料

- 食物

- 加工过的食品

- 水果和蔬菜

- 乳製品

- 其他食品

- 药品

- 饮料

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲和纽西兰(太平洋)

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 其他拉丁美洲

- 中东和非洲

- 北美洲

第七章 竞争形势

- 公司简介

- Amcor Ltd.

- IPI SRL(Coesia Group)

- Tetra Pak International SA

- Sealed Air Corporation

- SIG Combibloc Group

- Schott AG

- Coveris Holdings SA

- DS Smith PLC

- Uflex Limited

- Elopak AS

- BIBP SP ZOO

- CDF Corporation

- Smurfit Kappa

- Becton, Dickinson &Co.

- Mondi PLC

第八章市场的未来

The Global Aseptic Packaging Market size is estimated at USD 70.65 billion in 2024, and is expected to reach USD 116.23 billion by 2029, growing at a CAGR of 10.47% during the forecast period (2024-2029).

Aseptic packaging is packaging a product at ultra-high temperature (UHT), sterilizing or sanitizing the packaging separately, and fusing and sealing under sterile atmospheric conditions to avoid viral and bacterial contamination. In addition, it maintains the quality of the package contents and does not require preservatives, benefiting the global aseptic packaging market.

Key Highlights

- Sustainable packaging and longer shelf life are essential to consumers in the food and beverage industry. As a result, most food and beverage vendors are inclining toward aseptic packaging due to its cost and environmental benefits. Also, as aseptic packaging supports packaging through recyclable cartons and eco-friendly pouches and bags, which often target consumers that prefer small-quantity packaging and make purchases more frequently, the demand for such products is considerably high worldwide.

- Changing consumer eating habits lead to an increased preference for ready-to-eat meals and increased demand for convenient, high-quality food products, opening more doors for market growth. A gradual increase in global e-commerce sales and growth opportunities in emerging markets is anticipated to present significant opportunities for the sterile packaging market during the forecast period.

- Market players invest in R&D to stay ahead of developing industries. New product launches also support market demand. However, the pharmaceutical industry's demand for aseptic packaging is also increasing. Governments of various countries are increasingly spending on the healthcare sector to boost the growth of the aseptic packaging market.

- The increasing awareness regarding the ecological effect of single-use plastic and unsustainable business practices has encouraged consumers to demand a higher standard of products with less environmental impact. This has made many market players shift to high-cost sustainable packaging, which can hamper the growth of the market.

- During COVID-19, the market grew significantly. Due to the pandemic, customers shifted toward online retail and panic stocking, which increased demand for essential food items such as milk, baby food, and vegetables. The COVID-19 pandemic affected aseptic packaging materials in developing and developed countries. Moreover, the strong demand for sterilized packaged foods has encouraged investment in the landscape. Industry players expect the healthcare industry to show strong demand for packaging technology.

Aseptic Packaging Market Trends

Growing Demand for Beverages to Drive the Market

- The growing popularity of on-the-go beverages and the increasing number of outlets are expected to boost the market's growth in the beverage industry. The change in consumer needs provides packaging producers with several options for meeting innovative packaging needs in the beverage industry.

- Consumers frequently grab convenient and functional drinks, such as RTD coffee and tea, energy drinks, and other beverages that can be consumed whenever and wherever they need a boost. As such, non-alcoholic beverages that offer functional and practical benefits that are relatively healthy and natural can appeal to busy consumers. Leveraging the natural, energy-boosting characteristics of electrolytes, vitamins, minerals, and other natural ingredients in new product formulations can help brands target a specific consumer base.

- The increased demand for nutraceutical beverages and products due to several healthy ingredients such as vegetables and fruits and rising global demand for milk-based drinks are expected to boost global functional growth, presumed to be an essential factor for the beverage market during the forecast period.

- The increasing demand for instant energy drinks that provide mental and physical stimulation among fitness enthusiasts is projected to create significant growth opportunities for the functional beverage market during the forecast period.

- Consumers in the market are becoming increasingly conscious of health and wellness. From juice in the morning to energy drinks, they are spending more on products that provide refreshments and are well within the wellness trend. This trend has created a high demand for cost-effective packaging solutions in the beverage packaging segment. The increasing demand for aseptic cartons from the milk and other dairy beverages sectors may trigger additional activity in the market due to cartons' ability to offer benefits like easy stacking of products and longer shelf life.

Asia-Pacific to Witness Fastest Growth

- China is one of the major consumers of aseptic packaging in the Asia-Pacific region. The growing consumption of food and beverages is anticipated to support the market's growth during the forecast period. The growing trend of packed meals, the increasing number of restaurants and supermarkets, and the increasing bottled water and beverage consumption are significant factors driving the market in the country.

- In India, the industry is driven by a growing population, increased income, and changing lifestyles. Growth prospects of end-user segments are leading to a rise in the demand for the rigid plastic packaging industry. In addition, the market's expansion products are being constrained by the increased use of alternative packaging options for a pouch packaging. Due to the rapidly growing demand for packaged food goods and increased disposable income, India is projected to hold a significant share of the Asia-Pacific aseptic packing market.

- Consumers increasingly use retort pouches in Japan, particularly for sauces and curries. Retort pouches can replace conventional cans since they are made of laminated plastic and aluminum, which can withstand the thermal processing used for sterilizing. Pouch packaging is more affordable than cans, especially in nations that import metal for canning, which is the key driver promoting acceptance in Japan.

- Australia is one of the Asia-Pacific region's fastest-growing packaging markets. The meat, fresh produce, and processed food industries are growing nationwide. Rising consumer ethical concerns and trends in health and well-being have sustained the demand for locally produced, fresh food. In addition, the use of single-serve and reusable packaging options such as pouches has increased along with the country's tendency to snack over the years. The demand for RTD pouches is also being fueled by the steadily rising demand for dairy products and fresh fruit juices.

- Under the Asia-Pacific region, other countries like South Korea, Indonesia, Vietnam, Thailand, Singapore, Bangladesh, Taiwan, Malaysia, etc., also have high potential scope for gaining a considerable share in the market studied.

Aseptic Packaging Industry Overview

The aseptic packaging market is highly competitive and consists of several major players dominating the market. With a prominent share in the market, these major players are focusing on expanding their customer bases across foreign countries. These companies are leveraging strategic collaborative initiatives to increase their market shares and strengthen their product capabilities through acquisitions, product launches, etc. Some of the major players in the market are Amcor Ltd, IPI SRL (Coesia Group), Tetra Pak International SA, Sealed Air Corporation, SIG Combibloc Group, and Schott AG.

- In February 2023, SIG will build its first aseptic carton facility in India, the world's largest milk market and one of the major juice producers. The facility will be in Ahmedabad, Gujarat. The investment will pay for cutting-edge manufacturing capabilities for aseptic carton packs that meet strict environmental criteria for printing and finishing.

- In November 2022, Amcor PLC unveiled its aim to make all its aseptic products recyclable. Amcor has made progress toward its goal of having all products recyclable, reusable, or compostable by 2025, with 74% of the company's total production weight already being designed to be a recyclable number of creative solutions with more eco-friendly features steadily increasing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

- 4.5 Beverage Industry Landscape

- 4.5.1 Beverage Industry Landscape - Alcoholic Beverages

- 4.5.2 Beverage Industry Landscape - Non-alcoholic Beverages

- 4.6 Aseptic Packaging for Beverages - Demand Insights

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Beverages

- 5.1.2 Commodity Value of Glass Increased with Recyclability

- 5.2 Market Challenges

- 5.2.1 Volatility in the Raw Material Prices

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Cartons (Tetrapak, Combibloc, Etc.)

- 6.1.2 Bags and Pouches

- 6.1.3 Cans

- 6.1.4 Bottles

- 6.1.5 Other Products (Vials, Ampoules, Syringes, Cups, Etc)

- 6.2 By Application

- 6.2.1 Beverage

- 6.2.1.1 Ready-to-drink Beverages

- 6.2.1.2 Dairy-based Beverages

- 6.2.1.3 Other Beverages

- 6.2.2 Food

- 6.2.2.1 Processed Food

- 6.2.2.2 Fruits and Vegetables

- 6.2.2.3 Dairy Food

- 6.2.2.4 Other Foods

- 6.2.3 Pharmaceuticals

- 6.2.1 Beverage

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Australia and New Zealand (Pacific)

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Latin America

- 6.3.4.1 Brazil

- 6.3.4.2 Argentina

- 6.3.4.3 Rest of Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Ltd.

- 7.1.2 IPI SRL (Coesia Group)

- 7.1.3 Tetra Pak International SA

- 7.1.4 Sealed Air Corporation

- 7.1.5 SIG Combibloc Group

- 7.1.6 Schott AG

- 7.1.7 Coveris Holdings SA

- 7.1.8 DS Smith PLC

- 7.1.9 Uflex Limited

- 7.1.10 Elopak AS

- 7.1.11 BIBP SP ZOO

- 7.1.12 CDF Corporation

- 7.1.13 Smurfit Kappa

- 7.1.14 Becton, Dickinson & Co.

- 7.1.15 Mondi PLC

8 FUTURE OF THE MARKET

无菌包装市场报告:趋势、预测和竞争分析(至 2030 年)

无菌包装市场报告:趋势、预测和竞争分析(至 2030 年) 2030 年乳製品无菌包装市场预测:按产品类型、材料、技术、应用和地区进行的全球分析

2030 年乳製品无菌包装市场预测:按产品类型、材料、技术、应用和地区进行的全球分析 无菌硬纸盒包装市场,规模,占有率,趋势,产业分析报告:包装,各材料,各用途,各地区-2025-2034年市场预测

无菌硬纸盒包装市场,规模,占有率,趋势,产业分析报告:包装,各材料,各用途,各地区-2025-2034年市场预测 无菌包装市场:按材料、类型和应用分类 - 2025-2030 年全球预测

无菌包装市场:按材料、类型和应用分类 - 2025-2030 年全球预测 无菌纸盒包装市场规模、份额、趋势分析报告:按材料、类型、应用、分销管道、地区、细分市场预测,2024-2030 年

无菌纸盒包装市场规模、份额、趋势分析报告:按材料、类型、应用、分销管道、地区、细分市场预测,2024-2030 年 2024 年全球植物来源食品包装市场报告

2024 年全球植物来源食品包装市场报告 无菌包装市场规模、份额、趋势分析:按材料、产品、应用、地区、细分市场预测,2025-2030

无菌包装市场规模、份额、趋势分析:按材料、产品、应用、地区、细分市场预测,2025-2030 无菌包装市场规模、份额、成长分析:按类型、材料、应用、地区划分 - 产业预测,2024-2031 年

无菌包装市场规模、份额、成长分析:按类型、材料、应用、地区划分 - 产业预测,2024-2031 年 无菌包装市场-2024年至2029年预测

无菌包装市场-2024年至2029年预测 2024-2032 年按类型、材料、应用和地区分類的无菌包装市场报告

2024-2032 年按类型、材料、应用和地区分類的无菌包装市场报告