|

市场调查报告书

商品编码

1444539

特种化学品 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029 年)Specialty Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

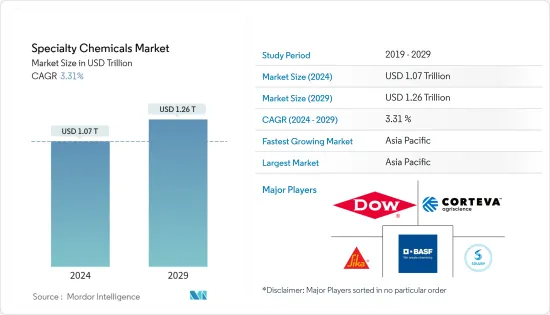

特种化学品市场规模预计到 2024 年为 1.07 兆美元,预计到 2029 年将达到 1.26 兆美元,在预测期内(2024-2029 年)CAGR为 3.31%。

2020年,市场受到COVID-19爆发的负面影响。由于疫情的影响,多个国家进入封锁状态,导致供应链中断、停工和劳动力短缺。然而,自限制解除以来,该行业正在良好復苏。房屋销售的增加和新项目的推出导致对油漆、涂料和建筑化学品的需求增加。半导体、积体电路和农业化学品需求的不断增长导致了过去两年市场的復苏。

主要亮点

- 推动市场成长的主要因素是建筑活动的强劲成长,特别是在亚太地区、中东和非洲。此外,不断增长的人口正在推动全球对粮食的需求。

- 另一方面,环境法规的加强和化石燃料储备的减少是阻碍市场成长的因素。

- 不断成长的创新产品研发可能为预测期内研究的市场提供机会。

- 亚太地区凭藉庞大的客户群主导了全球市场,导致该地区对特种化学品的高需求、工业生产的增加以及建筑业的强劲增长。

特种化学品市场趋势

农化领域将主导市场需求

- 农业化学品领域在特种化学品市场中占据主导地位。该部门的成长主要受到全球人均耕地面积减少和食品需求增加的推动。

- 全球人口正在迅速增加。不断增长的人口增加了粮食需求。为不断增长的人口提供食物正在成为一种威胁。另一方面,由于工业化和都市化,耕地面积不断减少。长期以来,人们一直使用化学肥料来提高作物生产力,因此在预测期内增加了农业化学品的需求。

- 随着人均收入的增加和人口的成长,全球粮食和经济作物的需求预计将增加。例如,根据联合国粮农组织的预测,到 2050 年,美国的粮食需求预计将增加 50-90%。

- 联合国粮食及农业组织(FAO)和国际粮食政策研究所(IFPRI)发布了2050年全球粮食需求成长的预测。FAO预测,到2050年世界粮食需求可能成长70%预计全球粮食需求的成长大部分将来自亚太地区、东欧和拉丁美洲消费者收入的成长。

- 此外,由于人们对植物养分吸收效率的日益关注以及对健康和环境监管的日益关注,微量营养素肥料、生物基肥料和特殊肥料(如液体肥料)越来越受欢迎。

- 使用微生物作为生物杂草控製剂的生物除草剂以及合成除草剂在害虫综合防治技术中也越来越受欢迎。儘管该细分市场仅占该行业的一小部分,但预计将大幅成长。

- 2021 年,所有国家的化肥出口总额约为 832 亿美元。这笔金额反映了 2020 年所有化肥出口商平均成长 50.7%5,当时化肥出口总额为 552 亿美元。

- 俄罗斯2021年出口额为124亿美元,比2020年(69.9亿美元)成长约78%,印度是俄罗斯最大的进口国之一。此外,中国的出口大幅成长近74.6%。 2021年中国化肥出口总额为114.7亿美元。

- 此外,农地承包和病虫害造成的作物损失是推动杀虫剂市场的重要因素。

- 因此,所有这些有利的趋势预计将在预测期内推动农业化学品市场的需求。预计这将推动对特种化学品的需求。

亚太地区将主导市场

- 亚太地区主导了特用化学品市场。由于建筑业的强劲增长、化妆品需求的增加、电气和电子行业产量增加的投资和生产的增加、包装行业对粘合剂和塑料的需求的增加以及增加该地区工业水处理系统的安装。

- 该地区人口的不断增长,尤其是中国和印度等国家的人口增长,对粮食的需求不断增加。预计它将推动农化市场的发展,有助于特种聚合物市场在预测期内成长。

- 亚太地区建筑业的成长主要受到服务业扩张的推动,导致办公空间需求增加、住宅建设项目增加以及跨国公司投资建立工业基地的流入在该区域。这些因素可能会增加预测期内该地区对油漆和涂料、黏合剂和密封剂、建筑化学品和特殊聚合物的需求。

- 根据中国国家统计局数据,2021年,中国建筑业企业增加价值80138亿元人民币(约11,516.1亿美元),较上年成长2.15%。

- 未来七年,印度的房屋投资也可能达到约 1.3 兆美元。该国预计将建造 6000 万套新住房。到 2025 年,印度经济适用房的供应量可能会增加 70% 左右。此外,印度政府的「到2022年为所有人提供住房」也是该行业的重大游戏规则改变者。

- 黏合剂已成为汽车应用中的主要技术组件,不断取代传统的黏合或黏合方法。该公司正在增加该地区的黏合剂和密封剂产量,从而导致对化妆品化学品的需求增加。

- 日本汽车工业协会 (JAMA) 的数据显示,2021 年日本乘用车和轻型汽车产量为 7,846,955 辆。

- 电子产业将黏合剂用于各种应用,包括保形涂层、保护端子电极以及表面安装元件的黏合等。电子业是印度成长最快的行业之一。根据电子和资讯技术部的数据,截至 2021 财年,该行业的市场规模为 4,950-50,000 亿印度卢比(约 66.95-676.2 亿美元)。

- 因此,所有这些有利趋势都可能在预测期内推动该地区特种化学品市场的成长。

特种化学品产业概况

特种化学品市场高度分散,众多参与者占据重要的市场份额。市场上一些主要的参与者(排名不分先后)包括巴斯夫股份公司、陶氏化学、科迪华、西卡股份公司和索尔维等。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 司机

- 亚太地区、中东和非洲建筑活动强劲成长

- 人口成长正在推动全球食品需求

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

- 原料分析

第 5 章:市场区隔(市场价值规模)

- 油漆和涂料

- 动力学

- 应用

- 大楼

- 汽车

- 工业的

- 木头

- 其他应用

- 催化剂

- 动力学

- 功能

- 化学合成催化剂

- 石油精炼催化剂

- 聚合催化剂

- 建筑化学品

- 动力学

- 应用

- 商业的

- 工业的

- 基础设施

- 住宅

- 公共场所

- 化妆品化学品

- 动力学

- 应用

- 头髮护理

- 皮肤护理

- 口腔护理

- 个人卫生

- 其他应用

- 染料、油墨和颜料

- 动力学

- 类型

- 油墨

- 染料

- 有机颜料

- 无机颜料

- 电子化学品

- 动力学

- 应用

- 半导体和积体电路

- 印刷电路板

- 水处理化学品

- 动力学

- 功能

- 絮凝剂

- 混凝剂

- 杀菌剂和消毒剂

- 消泡剂和消泡剂

- pH调节剂和软化剂

- 其他功能

- 食品添加物

- 动力学

- 类型

- 天然添加物

- 合成添加剂

- 农业化学品

- 动力学

- 类型

- 化肥

- 除草剂

- 杀菌剂

- 杀虫剂

- 杀线虫剂

- 杀软体动物

- 其他作物保护化学品

- 工业和公共机构清洁剂

- 动力学

- 应用

- 通用清洁剂

- 消毒剂和消毒剂

- 洗衣护理产品

- 洗车产品

- 润滑油添加剂

- 动力学

- 产品类别

- 分散剂和乳化剂

- 洗涤剂

- 氧化抑制剂

- 极压添加剂和抗磨添加剂

- 黏度指数调节剂

- 摩擦改进剂

- 缓蚀剂

- 其他产品类型

- 采矿化学品

- 动力学

- 功能

- 浮选化学品

- 萃取化学品

- 助磨剂

- 油田化学品

- 动力学

- 应用

- 杀菌剂

- 缓蚀阻垢剂

- 破乳剂

- 聚合物

- 界面活性剂

- 其他化学品类型

- 黏合剂和密封剂

- 动力学

- 科技

- 水性黏合剂

- 溶剂型黏合剂

- 热熔胶

- 反应性黏合剂

- 其他黏合剂

- 密封剂

- 塑胶添加剂

- 动力学

- 塑胶型

- 聚乙烯(PE)

- 聚苯乙烯(PS)

- 聚丙烯(PP)

- 聚酰胺 (PA)

- 聚对苯二甲酸乙二酯(PET)

- 聚氯乙烯 (PVC)

- 聚碳酸酯(PC)

- 其他塑胶类型

- 橡胶加工化学品

- 动力学

- 应用

- 胎

- 非轮胎

- 特种聚合物

- 动力学

- 纺织化学品

- 动力学

- 应用

- 涂料和施胶化学品

- 着色剂及助剂

- 整理剂

- 退浆剂

- 其他应用

- 地理

- 亚太

- 中国

- 印度

- 日本

- 韩国

- 东协国家

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太

第 6 章:竞争格局

- 併购、合资、合作与协议

- 市占率分析

- Adhesives and Sealants

- Agrochemicals

- Construction Chemicals

- Lubricants and Oil Additives

- Mining Chemicals

- Oilfield Chemicals

- Paints and Coatings

- Specialty Polymers

- Water Treatment Chemicals

- 领先企业采取的策略

- 公司简介

- 3M

- AECI

- Afton Chemical

- Akzo Nobel NV

- Albemarle Corporation

- ALTANA

- Archroma

- Arkema Group

- Ashland

- Asian Paints

- Axalta Coating Systems

- Baker Hughes Company

- BASF SE

- Berger Paints India Limited

- Buckman

- Chevron Corporation

- Clariant

- Corteva

- Covestro AG

- DIC Corporation

- Dow

- DSM

- DuPont

- Eastman Chemical Company

- Ecolab

- Evonik Industries AG

- Exxon Mobil Corporation

- Ferro Corporation

- Flint Group

- FMC Corporation

- GCP Applied Technologies Inc.

- HB Fuller Company

- Halliburton

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Huntsman International LLC

- Infineum International Limited

- Kemira

- KRONOS Worldwide Inc.

- Kurita Water Industries Ltd

- Holcim

- LANXESS

- Lonza

- MAPEI SpA

- Merck KGaA

- NIPSEA GROUP

- Nouryon

- Nutrien Ltd

- Pidilite Industries Ltd

- PPG Industries Inc.

- Procter & Gamble

- RPM International Inc.

- SABIC

- Schlumberger Limited

- Sika AG

- Solenis

- Solvay

- Syngenta

- The Chemours Company

- The Lubrizol Corporation

- The Sherwin-Williams Company

- Venator Materials PLC

- Veolia

- WR Grace & Co.

- Wacker Chemie AG

- Yara

第 7 章:市场机会与未来趋势

The Specialty Chemicals Market size is estimated at USD 1.07 trillion in 2024, and is expected to reach USD 1.26 trillion by 2029, growing at a CAGR of 3.31% during the forecast period (2024-2029).

The market was negatively impacted by the COVID-19 outbreak in 2020. Owing to the pandemic scenario, several countries went into lockdown, which led to supply chain disruptions, work stoppages, and labor shortages. However, the sector is recovering well since restrictions were lifted. An increase in house sales and new project launches have led to a rise in the demand for paints, coatings, and construction chemicals. The increasing demand for semiconductors, integrated circuits, and agrochemicals led to the market recovery over the last two years.

Key Highlights

- The major factors driving the market's growth are the robust growth of construction activities, especially in Asia-Pacific and the Middle East & Africa. Furthermore, the growing population is propelling the demand for food worldwide.

- On the flip side, increasing environmental regulations and decreasing fossil fuel reserves are the restraints hampering the market's growth.

- Growing research and development for creating novel products will likely provide an opportunity for the market studied over the forecast period.

- Asia-Pacific dominated the global market, owing to the vast customer base, leading to high demand for specialty chemicals, increasing industrial production, and robust growth of the construction sector in the region.

Speciality Chemicals Market Trends

Agrochemicals Segment to Dominate the Market Demand

- The agrochemicals segment dominated the share in the specialty chemicals market. The segment's growth is extensively driven by the decreasing per capita arable land and increasing demand for food worldwide.

- The global population is increasing rapidly. This growing population is adding to the food demand. Supplying food to this ever-increasing population is becoming a threat. On the other hand, arable land is declining due to industrialization and urbanization. Fertilizers have been used for a long time to increase crop productivity, thus, enhancing agrochemicals demand over the forecast period.

- With the increasing per capita income and growing population, food and cash crops demand is estimated to increase globally. For instance, as per the FAO, the food demand in the United States is expected to increase by 50-90% by 2050.

- The Food and Agriculture Organization of the United Nations (FAO) and the International Food Policy Research Institute (IFPRI) have published projections of an increase in global food demand by 2050. The FAO projections indicate that world food demand may increase by 70% by 2050, with much of the projected increase in global food demand expected to come from rising consumer incomes in Asia-Pacific, Eastern Europe, and Latin America.

- Furthermore, owing to the growing concerns about nutrient efficiency uptake by plants and the growing regulatory health and environmental concerns, micronutrient fertilizers, bio-based fertilizers, and specialty fertilizers (like liquid fertilizers) are gaining popularity.

- Bio-herbicides that use microbes as biological weed control agents are also gaining popularity in integrated pest management techniques, along with synthetic herbicides. Although the segment constitutes only a tiny part of the industry, it is expected to grow significantly.

- Fertilizers exported by all countries totaled around USD 83.2 billion in 2021. That dollar amount reflects an average 50.7%5 increase for all shippers of fertilizers in 2020 when overall fertilizer exports were worth USD 55.2 billion.

- Russia exported USD 12.4 billion in 2021, an increase of around 78% compared to 2020 (USD 6.99 billion), with India being one of the largest importers from the Federation. Additionally, China experienced a significant increase in exports of almost 74.6%. Fertilizer exports from China totaled 11.47 billion USD in 2021.

- Moreover, contracting agricultural land and losing crops owing to pests and diseases are the significant factors driving the insecticide market.

- Hence, all such favorable trends are expected to drive the demand for the agrochemicals market during the forecast period. It is expected to drive the need for specialty chemicals.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the specialty chemicals market. It is likely to retain its position during the forecast period due to robust growth of the construction sector, increasing cosmetic products demand, growing investment and production in the increasing electrical and electronics industry output, increasing demand for adhesives and plastics from the packaging industry, and increasing installations of water treatment systems from the industries in the region.

- The growing population in the region, especially in countries such as China and India, is increasing the demand for food. It is expected to drive the agrochemical market and consequently help the specialty polymers market grow over the forecast period.

- The growth of the Asia-Pacific construction sector is majorly driven by the service sector expansion, leading to an increase in the demand for office spaces, an increase in residential construction projects, and an inflow of investments from multinational companies to set up an industrial base in the region. Such factors will likely increase the demand for paints and coatings, adhesives and sealants, construction chemicals, and specialty polymers in the area during the forecast period.

- According to the National Bureau of Statistics of China, in 2021, the value added of construction enterprises in China was CNY 8,013.8 billion (~USD 1151.61 billion), up by 2.15% over the previous year.

- India will also likely witness an investment of around USD 1.3 trillion in housing over the next seven years. The country is expected to see the construction of 60 million new homes. The availability of affordable housing is likely to rise by around 70% by 2025 in India. Besides, the Indian government's 'Housing for All by 2022' is also a significant game-changer for the industry.

- Adhesives have become a prime technology component in automotive applications, continuously replacing traditional bonding or adhesion methods. It is increasing adhesives and sealants production in the region, leading to a rise in demand for cosmetic chemicals.

- According to Japan Automobile Manufacturers Association (JAMA), the country produced 7,846,955 units of passenger cars and light vehicles in 2021.

- The electronics industry uses adhesives for various applications, including conformal coatings, protecting terminal electrodes, and bonding of surface mount devices, among many others. The electronics industry is one of the fastest-growing industries in India. According to the Ministry of Electronics and IT, the industry's market size is INR 4,950-5,000 billion (~ USD 66.95-67.62 billion) as of fiscal 2021.

- Hence, all such favorable trends are collectively likely to drive the growth of the specialty chemicals market in the region during the forecast period.

Speciality Chemicals Industry Overview

The specialty chemicals market is highly fragmented, with numerous players holding a significant market share. Some of the major players in the market (in no particular order) include BASF SE, Dow, Corteva, Sika AG, and Solvay, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Robust Growth of Construction Activities in Asia-Pacific, and Middle East and Africa

- 4.1.2 Growing Population is Propelling the Demand for Food Worldwide

- 4.2 Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products and Services

- 4.2.5 Degree of Competition

- 4.3 Raw Material Analysis

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Paints and Coatings

- 5.1.1 Dynamics

- 5.1.2 Application

- 5.1.2.1 Architectural

- 5.1.2.2 Automotive

- 5.1.2.3 Industrial

- 5.1.2.4 Wood

- 5.1.2.5 Other Applications

- 5.2 Catalysts

- 5.2.1 Dynamics

- 5.2.2 Function

- 5.2.2.1 Chemical Synthesis Catalysts

- 5.2.2.2 Petroleum Refining Catalysts

- 5.2.2.3 Polymerization Catalysts

- 5.3 Construction Chemicals

- 5.3.1 Dynamics

- 5.3.2 Application

- 5.3.2.1 Commercial

- 5.3.2.2 Industrial

- 5.3.2.3 Infrastructure

- 5.3.2.4 Residential

- 5.3.2.5 Public Space

- 5.4 Cosmetic Chemicals

- 5.4.1 Dynamics

- 5.4.2 Application

- 5.4.2.1 Hair Care

- 5.4.2.2 Skin Care

- 5.4.2.3 Oral Care

- 5.4.2.4 Personal Hygiene

- 5.4.2.5 Other Applications

- 5.5 Dyes, Inks, and Pigments

- 5.5.1 Dynamics

- 5.5.2 Type

- 5.5.2.1 Inks

- 5.5.2.2 Dyes

- 5.5.2.3 Organic Pigments

- 5.5.2.4 Inorganic Pigments

- 5.6 Electronic Chemicals

- 5.6.1 Dynamics

- 5.6.2 Application

- 5.6.2.1 Semiconductors and Integrated Circuits

- 5.6.2.2 Printed Circuit Boards

- 5.7 Water Treatment Chemicals

- 5.7.1 Dynamics

- 5.7.2 Function

- 5.7.2.1 Flocculants

- 5.7.2.2 Coagulants

- 5.7.2.3 Biocides and Disinfectants

- 5.7.2.4 Defoamers and Defoaming Agents

- 5.7.2.5 pH Adjusters and Softeners

- 5.7.2.6 Other Functions

- 5.8 Food Additives

- 5.8.1 Dynamics

- 5.8.2 Type

- 5.8.2.1 Natural Additives

- 5.8.2.2 Synthetic Additives

- 5.9 Agrochemicals

- 5.9.1 Dynamics

- 5.9.2 Type

- 5.9.2.1 Fertilizers

- 5.9.2.2 Herbicide

- 5.9.2.3 Fungicide

- 5.9.2.4 Insecticide

- 5.9.2.5 Nematicide

- 5.9.2.6 Molluscicide

- 5.9.2.7 Other Crop Protection Chemicals

- 5.10 Industrial and Institutional Cleaners

- 5.10.1 Dynamics

- 5.10.2 Application

- 5.10.2.1 General Purpose Cleaners

- 5.10.2.2 Disinfectants and Sanitizers

- 5.10.2.3 Laundry Care Products

- 5.10.2.4 Vehicle Wash Products

- 5.11 Lubricant Additives

- 5.11.1 Dynamics

- 5.11.2 Product Type

- 5.11.2.1 Dispersants and Emulsifiers

- 5.11.2.2 Detergents

- 5.11.2.3 Oxidation Inhibitors

- 5.11.2.4 Extreme-pressure Additives and Anti-wear Additives

- 5.11.2.5 Viscosity Index Modifiers

- 5.11.2.6 Friction Modifiers

- 5.11.2.7 Corrosion Inhibitors

- 5.11.2.8 Other Product Types

- 5.12 Mining Chemicals

- 5.12.1 Dynamics

- 5.12.2 Function

- 5.12.2.1 Flotation Chemicals

- 5.12.2.2 Extraction Chemicals

- 5.12.2.3 Grinding Aids

- 5.13 Oilfield Chemicals

- 5.13.1 Dynamics

- 5.13.2 Application

- 5.13.2.1 Biocide

- 5.13.2.2 Corrosion and Scale Inhibitor

- 5.13.2.3 Demulsifier

- 5.13.2.4 Polymer

- 5.13.2.5 Surfactant

- 5.13.2.6 Other Chemical Types

- 5.14 Adhesives and Sealants

- 5.14.1 Dynamics

- 5.14.2 Technology

- 5.14.2.1 Water-borne Adhesives

- 5.14.2.2 Solvent-borne Adhesives

- 5.14.2.3 Hot-melt Adhesives

- 5.14.2.4 Reactive Adhesives

- 5.14.2.5 Other Adhesives

- 5.14.2.6 Sealants

- 5.15 Plastic Additives

- 5.15.1 Dynamics

- 5.15.2 Plastic Type

- 5.15.2.1 Polyethylene (PE)

- 5.15.2.2 Polystyrene (PS)

- 5.15.2.3 Polypropylene (PP)

- 5.15.2.4 Polyamide (PA)

- 5.15.2.5 Polyethylene Terephthalate (PET)

- 5.15.2.6 Polyvinyl Chloride (PVC)

- 5.15.2.7 Polycarbonate (PC)

- 5.15.2.8 Other Plastic Types

- 5.16 Rubber Processing Chemicals

- 5.16.1 Dynamics

- 5.16.2 Application

- 5.16.2.1 Tire

- 5.16.2.2 Non-tire

- 5.17 Specialty Polymers

- 5.17.1 Dynamics

- 5.18 Textile Chemicals

- 5.18.1 Dynamics

- 5.18.2 Application

- 5.18.2.1 Coating and Sizing Chemicals

- 5.18.2.2 Colorants and Auxiliaries

- 5.18.2.3 Finishing Agents

- 5.18.2.4 Desizing Agents

- 5.18.2.5 Other Application

- 5.19 Geography

- 5.19.1 Asia-Pacific

- 5.19.1.1 China

- 5.19.1.2 India

- 5.19.1.3 Japan

- 5.19.1.4 South Korea

- 5.19.1.5 ASEAN Countries

- 5.19.1.6 Rest of Asia-Pacific

- 5.19.2 North America

- 5.19.2.1 United States

- 5.19.2.2 Canada

- 5.19.2.3 Mexico

- 5.19.2.4 Rest of North America

- 5.19.3 Europe

- 5.19.3.1 Germany

- 5.19.3.2 United Kingdom

- 5.19.3.3 Italy

- 5.19.3.4 France

- 5.19.3.5 Spain

- 5.19.3.6 Rest of Europe

- 5.19.4 South America

- 5.19.4.1 Brazil

- 5.19.4.2 Argentina

- 5.19.4.3 Rest of South America

- 5.19.5 Middle-East and Africa

- 5.19.5.1 Saudi Arabia

- 5.19.5.2 South Africa

- 5.19.5.3 Rest of Middle-East and Africa

- 5.19.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.2.1 Adhesives and Sealants

- 6.2.2 Agrochemicals

- 6.2.3 Construction Chemicals

- 6.2.4 Lubricants and Oil Additives

- 6.2.5 Mining Chemicals

- 6.2.6 Oilfield Chemicals

- 6.2.7 Paints and Coatings

- 6.2.8 Specialty Polymers

- 6.2.9 Water Treatment Chemicals

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 AECI

- 6.4.3 Afton Chemical

- 6.4.4 Akzo Nobel NV

- 6.4.5 Albemarle Corporation

- 6.4.6 ALTANA

- 6.4.7 Archroma

- 6.4.8 Arkema Group

- 6.4.9 Ashland

- 6.4.10 Asian Paints

- 6.4.11 Axalta Coating Systems

- 6.4.12 Baker Hughes Company

- 6.4.13 BASF SE

- 6.4.14 Berger Paints India Limited

- 6.4.15 Buckman

- 6.4.16 Chevron Corporation

- 6.4.17 Clariant

- 6.4.18 Corteva

- 6.4.19 Covestro AG

- 6.4.20 DIC Corporation

- 6.4.21 Dow

- 6.4.22 DSM

- 6.4.23 DuPont

- 6.4.24 Eastman Chemical Company

- 6.4.25 Ecolab

- 6.4.26 Evonik Industries AG

- 6.4.27 Exxon Mobil Corporation

- 6.4.28 Ferro Corporation

- 6.4.29 Flint Group

- 6.4.30 FMC Corporation

- 6.4.31 GCP Applied Technologies Inc.

- 6.4.32 H.B. Fuller Company

- 6.4.33 Halliburton

- 6.4.34 Henkel AG & Co. KGaA

- 6.4.35 Hexcel Corporation

- 6.4.36 Huntsman International LLC

- 6.4.37 Infineum International Limited

- 6.4.38 Kemira

- 6.4.39 KRONOS Worldwide Inc.

- 6.4.40 Kurita Water Industries Ltd

- 6.4.41 Holcim

- 6.4.42 LANXESS

- 6.4.43 Lonza

- 6.4.44 MAPEI SpA

- 6.4.45 Merck KGaA

- 6.4.46 NIPSEA GROUP

- 6.4.47 Nouryon

- 6.4.48 Nutrien Ltd

- 6.4.49 Pidilite Industries Ltd

- 6.4.50 PPG Industries Inc.

- 6.4.51 Procter & Gamble

- 6.4.52 RPM International Inc.

- 6.4.53 SABIC

- 6.4.54 Schlumberger Limited

- 6.4.55 Sika AG

- 6.4.56 Solenis

- 6.4.57 Solvay

- 6.4.58 Syngenta

- 6.4.59 The Chemours Company

- 6.4.60 The Lubrizol Corporation

- 6.4.61 The Sherwin-Williams Company

- 6.4.62 Venator Materials PLC

- 6.4.63 Veolia

- 6.4.64 W. R. Grace & Co.

- 6.4.65 Wacker Chemie AG

- 6.4.66 Yara