|

市场调查报告书

商品编码

1685828

企业应用整合:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Enterprise Application Integration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

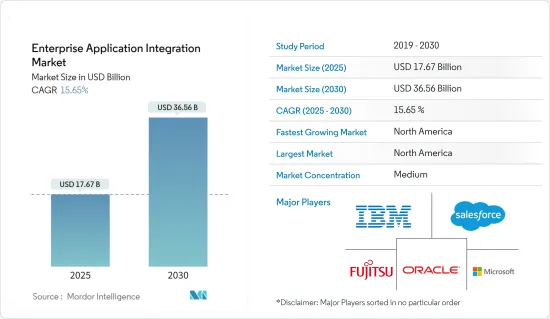

企业应用整合市场规模预计在 2025 年为 176.7 亿美元,预计到 2030 年将达到 365.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 15.65%。

数位转型正在改变企业格局

数位转型正在彻底改变每个产业。随着业务的发展,无缝整合各种应用程式的需求变得至关重要。企业应用程式整合 (EAI) 解决方案处于此转变的最前沿,使组织能够将其业务应用程式与相关资料库和工作流程整合。 EAI 的采用正值企业软体生态系统变得越来越复杂之时。根据 Okta 的《企业在工作》报告,大型企业平均部署 187 个应用程序,这表明全球应用程式使用量持续增加。这一趋势凸显了对强大的企业应用程式整合解决方案的迫切需求。

整合挑战:

主要亮点

- 不同的系统:公司通常在互不相容的框架内运营,从而阻碍 ERP、CRM 和其他关键系统之间的资料交换。

- 自动化障碍:缺乏整合导致难以实现重复任务的自动化,进而影响业务效率。

- 财务影响:根据 Cleo 的报告,24% 的供应链公司每年因软体系统整合不佳而损失超过 50 万美元。

EAI 解决方案

主要亮点

- 中间件基础设施:EAI 为不同应用程式和传统设备之间的开放资料共用引入了一个安全平台。

- 统一方法:EAI 中间件平台将资料从应用程式的限制中解放出来,帮助实现资料的集中和整合。

- 提高营运效率:整合简化了资讯共用,并提供了跨云端运算、巨量资料和物联网技术的更轻鬆的资料控制。

即时资料存取:敏捷企业的基石

随着企业追求灵活性和业务效率,对即时资料存取和管理的需求正在激增。即时洞察对于做出明智的决策、改善客户体验和推动个人化至关重要。这一趋势正在推动对云端基础的企业整合解决方案的投资,这些解决方案可以处理现代资料储存库的复杂性和数量。

市场反应

主要亮点

- 云端连线:Qlik 引入了 Qlik-cloud资料连线。它是一种 iPaaS(整合平台即服务)解决方案,可将公司的所有资料来源即时连结到云端。

- 本地优势:本地部署允许即时监控业务,同时提高资料机密性。

- 全面的解决方案Persistent 的企业整合服务使软体应用程式能够无缝协作,提供跨多个管道的一致、即时的资料视图。

对产业的影响

主要亮点

- 最佳化效能:即时资料整合可即时洞察整个软体定义企业的业务绩效。

- 更有效率的协作:EAI 工具和技术正在不断发展,以提供即时洞察并促进跨多个应用程式的合作和资讯交流。

- 管理复杂性:单一服务正在兴起,以更有效地处理各种基础设施和应用程式问题。

API主导整合:推动互联企业

行动应用程式、物联网设备和穿戴式装置的激增推动了以 API 为中心的整合的需求。即时 API 驱动的整合支援可随时监控各种参数的应用程序,促进跨多个平台的无缝资料流和同步。

大规模连结:

主要亮点

- 设备激增:思科预测,到 2030 年将有 5,000 亿台设备连接到互联网,凸显了 EAI 在管理这一庞大生态系统中发挥的关键作用。

- 资料同步:即时应用程式整合确保个人电脑、笔记型电脑和手持装置之间的资料一致性。

对企业的影响:

主要亮点

- 连结生态系统:随着数位转型的进展,企业软体整合正在从后端角色转变为连接整个生态系统的关键角色。

- 架构灵活性:EAI 解决方案正在不断发展,以支援云端和内部部署环境、敏捷交付和即插即用架构。

行业特定的采用趋势 EAI 解决方案的采用因行业而异,其中 IT 和通讯、BFSI 和製造业处于领先地位。每个行业都在使用 EAI 来应对独特的挑战并利用新的机会。

资讯科技和电讯

主要亮点

- 市场领导地位:IT 和通讯领域预计到 2027 年将达到 72.8 亿美元,复合年增长率为 17.64%。

- 电信整合:企业软体整合计划对于整合通讯产业客自订和基于市场的应用系统、平衡技术和业务需求至关重要。

BFSI 部门:

主要亮点

- 数位付款:数位付款的兴起推动了对强大资料管理系统的需求,从而刺激了 EAI 市场的成长。

- 创新平台:BlocPal International Inc. 开发的独特实体和虚拟金融服务平台是该行业致力于综合数位解决方案的一个例子。

製造业

知识工程:EAI 是整合分散式、自主製造系统和支援虚拟企业和大规模客製化等范例的关键。

主要亮点

- 竞争力:EAI对IT和基于知识的工程的有效利用提高了公司快速回应市场发展的能力。

- 展望未来:不断发展的整合格局:企业应用整合的未来特征是复杂性不断增加,并且需要更复杂、更灵活的解决方案。随着企业继续严重依赖技术,整合各种应用程式的需求只会增加。

新兴趋势:

主要亮点

- 扩大整合范围:未来的 EAI 解决方案将需要考虑组织内部和外部的大量端点。

- 快速创新:整合要求的变更率正在加快,需要更灵活、反应更快的 EAI 平台。

- 行动集成:预计 20% 的整合支出将用于行动装置的资料集成,这必须解决间歇性连线和不同吞吐量等挑战。

战略问题

主要亮点

- 平衡稳定性和创新性:IT 领导者必须保持对关键系统的控制,同时促进存取这些系统的应用程式的快速迭代。

- 预取和快取:行动应用程式越来越多地采用复杂的资料预取和快取策略来弥补连线问题。

- 不断适应:EAI 解决方案必须不断发展,以支持数位转型倡议所特有的快速创新步伐。

企业应用整合市场趋势

IT 与通讯领域:最大的终端使用者领域

IT 和电讯领域正在成为企业应用整合 (EAI) 市场的主导力量,预计到 2027 年将达到 72.8 亿美元,复合年增长率为 17.64%。这一显着的成长证实了企业软体整合解决方案在解决 IT 和通讯业复杂整合需求方面发挥的关键作用,尤其是在云端运算和数位转型领域。

云端迁移推动整合需求

- 资料和基础设施迁移:通讯业者越来越多地将资料、流程和基础设施迁移到云端,这是采用 EAI 的关键驱动因素。

- 无缝运作:这种转变需要强大的整合能力,以确保跨不同系统和应用程式的无缝运作。

- 云端基础的重点:企业越来越优先考虑资料平台即服务 (dPaaS) 而不是传统的整合平台即服务 (iPaaS) 模型来扩充性其营运。

通讯业者核心流程整合

- 整合复杂性:通讯业者正在进行大规模 EAI计划来支援核心流程,并正在建立中间件基础设施来整合客自订和市场应用系统。

- 跨境整合:电讯在其国际子公司之间协调技术解决方案面临独特的挑战,凸显了综合整合平台的重要性。

即时整合与物联网融合:

- 以 API 为中心的解决方案:行动应用程式、物联网和穿戴式装置的整合正在推动对即时、API主导的整合解决方案的需求。

- 设备爆炸式成长:预计到 2030 年将有 5,000 亿台设备实现互联,这凸显了对强大、整合的解决方案来管理这些生态系统中的资料流的需求。

协作软体解决方案推动整合需求

- 虚拟协作激增:Microsoft Teams 和 Zoom 等虚拟会议和协作工具的兴起间接推动了整合企业解决方案的需求。

- 系统互通性:公司正在寻找将协同软体与现有系统整合的解决方案,这进一步增加了对 EAI 的需求。

北美:成长最快的区域

北美是企业应用整合 (EAI) 市场成长最快的区域,预计到 2027 年将达到 142.6 亿美元,复合年增长率为 16.41%。由于该地区在数位转型方面处于领先地位,并且广泛采用云端基础的企业整合解决方案,该地区正处于快速成长轨道。

应用程式整合变得越来越普遍:

- 高采用率:超过 93% 的美国企业使用商业应用程序,这为企业软体整合供应商提供了沃土。

- 业务效率:随着企业采用越来越多的应用程序,对于提高业务效率的无缝整合解决方案的需求持续成长。

策略伙伴关係和创新解决方案:

- 推动创新的伙伴关係:HiQ与欧洲云端城市网路和Frends iPaaS平台的合作等策略合作伙伴关係正在推动混合云端整合策略的创新。

- 法规合规性:这些伙伴关係关係致力于提供解决方案,确保完全遵守对公共和商业部门企业至关重要的资料法规。

云端整合与数位转型

- 技术颠覆:物联网、云端运算和数位转型倡议的持续采用,推动了北美各产业对 EAI 解决方案的需求。

- 供应商焦点:IBM 和富士通等该地区的主要企业正透过基于 SaaS 的安全解决方案等创新引领市场,从而推动市场成长。

- 整合市场:北美 EAI 市场适度整合,全球参与者专注于最尖端科技以保持竞争力。

- 零信任架构:采用零信任架构来保障安全等创新对于在企业环境中部署 EAI 解决方案变得越来越重要。

企业应用整合产业概览

全球企业主导半整合市场

企业应用整合 (EAI) 市场具有半整合结构的特点,IBM 公司、富士通有限公司和微软等全球参与者占据着相当大的市场占有率。这些科技集团利用其广泛的资源、全球影响力和技术专长来主导市场,而规模较小、创新的企业则利用专业化的解决方案为自己开闢利基市场。

全方位服务

端到端解决方案:全球领导者提供全面的企业应用程式整合解决方案,以满足各行各业组织的不同需求。

伙伴关係生态系统:IBM 和微软等公司已经建立了广泛的合作伙伴生态系统,可以提供各种业务应用程式和资料来源的整合。

研发重点:

新兴技术:主要企业正在大力投资研发,并专注于人工智慧 (AI)、机器学习和云端运算方面的创新,以发展其 EAI 平台。

支援混合环境:此整合解决方案旨在支援混合云端整合策略,确保内部部署和云端基础的基础架构之间的平稳过渡。

创新且适应性强:

云端原生架构:对可扩展和灵活解决方案的不断增长的需求正在推动向云端原生架构的转变。

低程式码/无程式码工具:低程式码/无程式码工具的引入正在扩大整合能力的范围,并使非技术用户能够为资料整合服务做出贡献。

安全性与合规性:

资料隐私问题:随着企业努力应对日益增长的资料隐私问题,EAI 供应商和供应商正在优先考虑其解决方案的安全性、合规性和管治功能,以获得竞争优势。

API 管理:EAI 的强大 API 管理正在成为一个关键的差异化因素,使企业能够安全地整合大量应用程式和端点。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

- 技术简介

第五章 市场动态

- 市场驱动因素

- 数位转型改变商业格局

- 对即时资料存取和管理的需求日益增加

- 面向互联企业的 API主导集成

- 市场挑战

- 开放原始码软体的可用性

- 缺乏整合导致重复任务难以自动化,进而影响业务效率。

- 评估新冠肺炎对产业的影响

第六章 市场细分

- 部署类型

- 本地

- 云

- 杂交种

- 组织规模

- 大型企业

- 中小型企业

- 最终用户产业

- BFSI

- 资讯科技/通讯

- 卫生保健

- 零售

- 政府

- 製造业

- 其他最终用户产业

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- IBM Corporation

- Fujitsu Limited

- Microsoft Corporation

- MuleSoft LLC(Salesforce Inc.)

- Oracle Corporation

- SAP SE

- Software AG

- Tibco Software Inc.

- iTransition Group

第八章投资分析

第九章:市场的未来

The Enterprise Application Integration Market size is estimated at USD 17.67 billion in 2025, and is expected to reach USD 36.56 billion by 2030, at a CAGR of 15.65% during the forecast period (2025-2030).

Digital Transformation Reshaping Enterprise Landscapes

Digital transformation is revolutionizing industries across the board. As businesses evolve, the need for seamless integration of diverse applications becomes paramount. Enterprise Application Integration (EAI) solutions are at the forefront of this transformation, enabling organizations to unify databases and workflows associated with business applications. The adoption of EAI is driven by the increasing complexity of enterprise software ecosystems. According to Okta's "Businesses at Work" report, large organizations deploy an average of 187 applications, showcasing a consistent rise in application utilization globally. This trend underscores the critical need for robust enterprise application integration solutions.

Integration Challenges:

Key Highlights

- Disparate Systems: Businesses often operate with incompatible frameworks, hindering data exchange between ERP, CRM, and other critical systems.

- Automation Hurdles: The lack of integration makes automating simple tasks challenging, impacting operational efficiency.

- Financial Impact: Cleo's report reveals that 24% of supply chain companies lose over USD 500,000 annually due to inadequate software system integrations.

EAI Solutions:

Key Highlights

- Middleware Infrastructure: EAI introduces a secure platform for open data sharing between heterogeneous applications and legacy devices.

- Unified Approach: By removing data from application restrictions, EAI middleware platforms aid in centralized data management and integration.

- Operational Efficiency: Integration streamlines information sharing and provides ease in controlling data across cloud computing, Big Data, and IoT technologies.

Real-time Data Access: The Cornerstone of Agile Enterprises

The demand for real-time data access and management is surging as businesses strive for agility and operational efficiency. Real-time insights are crucial for making informed decisions, improving customer experiences, and driving personalization efforts. This trend is propelling investments in cloud-based enterprise integration solutions that can handle the complexity and volume of modern data repositories.

Market Response:

Key Highlights

- Cloud Connectivity: Qlik introduced Qlik-cloud data connectivity, an Integration Platform as a Service (iPaaS) solution, linking all enterprise data sources to the cloud in real-time.

- On-premise Advantages: On-premise implementations offer real-time monitoring of business operations with enhanced data confidentiality.

- Comprehensive Solutions: Persistent's Enterprise Integration Services enable seamless interfacing of software applications, providing a consistent, real-time view of data across multiple channels.

Industry Impact:

Key Highlights

- Performance Optimization: Real-time data integration allows for immediate insights into total business performance across software-defined enterprises.

- Collaborative Efficiency: EAI tools and technologies are evolving to deliver real-time insights, fostering successful cooperation and information exchange across multiple applications.

- Managed Complexity: Single services are emerging to handle issues across a diverse range of infrastructure and applications more effectively.

API-Driven Integration: Powering the Connected Enterprise

The proliferation of mobile applications, IoT devices, and wearables is driving the need for API-centric integration. Real-time, API-driven integration enables the creation of applications that can monitor various parameters on the go, facilitating seamless data flow and synchronization across multiple platforms.

Connectivity Scale:

Key Highlights

- Device Proliferation: Cisco projects that 500 billion devices will be connected to the Internet by 2030, emphasizing the critical role of EAI in managing this vast ecosystem.

- Data Synchronization: Real-time application integration ensures data consistency across PCs, laptops, and handheld devices

Enterprise Impact:

Key Highlights

- Ecosystem Binding: As digital transformation advances, enterprise software integration is shifting from back-end to a critical role in binding the entire ecosystem.

- Architectural Flexibility: EAI solutions are evolving to support cloud and on-premise environments, agile delivery, and plug-and-play architectures.

Industry-Specific Adoption TrendsThe adoption of EAI solutions varies across industries, with IT and telecom, BFSI, and manufacturing sectors leading the charge. Each sector leverages EAI to address unique challenges and capitalize on emerging opportunities.

IT and Telecom:

Key Highlights

- Market Leadership: The IT and telecom segment is projected to reach USD 7.28 billion by 2027, growing at a CAGR of 17.64%.

- Telecom Integration: Enterprise software integration projects are crucial for integrating custom and market application systems in telecom operations, balancing technology with business imperatives.

BFSI Sector:

Key Highlights

- Digital Payments: The rise of digital payment methods is driving the need for robust data management systems, fueling EAI market growth.

- Innovative Platforms: BlocPal International Inc.'s development of a unique physical and virtual financial services platform exemplifies the sector's push towards integrated digital solutions.

Manufacturing:

Knowledge Engineering: EAI is critical in integrating dispersed and autonomous manufacturing systems, supporting paradigms like virtual enterprise and mass customization.

Key Highlights

- Competitiveness: Efficient application of IT and knowledge-based engineering through EAI enhances firms' ability to respond swiftly to market developments.

- Future Outlook: Evolving Integration Landscape : The future of Enterprise Application Integration is characterized by increasing complexity and the need for more sophisticated, agile solutions. As organizations continue to rely heavily on technology, the demand for integrating diverse applications will only intensify

Emerging Trends:

Key Highlights

- Expanded Integration Scope: Future EAI solutions will need to consider a vastly larger collection of endpoints both inside and outside the organization.

- Rapid Innovation: The frequency of changes in integration requirements is accelerating, necessitating more flexible and responsive EAI platforms.

- Mobile Integration: It's projected that 20% of integration spending will be directed towards integrating data on mobile devices, addressing challenges like intermittent connectivity and variable throughput

Strategic Imperatives:

Key Highlights

- Balancing Stability and Innovation: IT leaders must maintain control over critical systems while fostering rapid iteration of applications accessing those systems.

- Prefetching and Caching: Mobile apps are increasingly employing sophisticated data prefetching and caching strategies to compensate for connectivity issues.

- Continuous Adaptation: EAI solutions must evolve to support the rapid pace of innovation that distinguishes digital transformation initiatives.

Enterprise Application Integration Market Trends

IT and Telecom Segment: Largest End-User Segment

The IT and Telecom segment emerges as the dominant force in the Enterprise Application Integration (EAI) market, projected to reach USD 7.28 billion by 2027 with a CAGR of 17.64%. The substantial growth underscores the critical role of enterprise software integration solutions in addressing the complex integration needs of the IT and Telecom industries, particularly in the realm of cloud computing and digital transformation.

Cloud Migration Drives Integration Demand:

- Data and Infrastructure Migration: The increasing migration of data, processes, and infrastructure to the cloud by banks and telecom operators is a significant driver for EAI adoption.

- Operational Seamlessness: This shift necessitates robust integration capabilities to ensure seamless operation across diverse systems and applications.

- Cloud-based Focus: Businesses are increasingly prioritizing data platform as a service (dPaaS) over traditional integration platform as a service (iPaaS) models to enhance operational scalability.

Telecom Operators' Core Process Integration:

- Complexity of Integration: Telecom operators are undertaking extensive EAI projects to support core processes, creating middleware infrastructures to integrate custom and market application systems.

- Cross-National Integration: Telecom companies face unique challenges in aligning technical solutions across international subsidiaries, emphasizing the importance of comprehensive integration platforms.

Real-Time Integration and IoT Convergence:

- API-Centric Solutions: The convergence of mobile applications, IoT, and wearables is driving the demand for real-time, API-driven integration solutions.

- Proliferation of Devices: By 2030, projections of 500 billion connected devices emphasize the need for robust integration solutions to manage the data flow across these ecosystems.

Collaborative Software Solutions Drive Integration Needs:

- Virtual Collaboration Surge: The rise of virtual meeting and collaboration tools, such as Microsoft Teams and Zoom, has indirectly boosted demand for integrated enterprise solutions.

- System Interoperability: Businesses are seeking solutions that integrate collaborative software with existing systems, further driving the need for EAI.

North America: Fastest-Growing Regional Segment

North America stands out as the fastest-growing regional segment in the Enterprise Application Integration (EAI) market, projected to reach USD 14.26 billion by 2027, registering a CAGR of 16.41%. The region's leadership in digital transformation and the widespread adoption of cloud-based enterprise integration solutions highlight its rapid growth trajectory.

Widespread Application Integration:

- High Adoption Rate: Over 93% of U.S. businesses utilize business applications, creating fertile ground for enterprise software integration providers.

- Operational Efficiency: As companies adopt more applications, the demand for seamless integration solutions that enhance operational efficiency continues to grow.

Strategic Alliances and Innovative Solutions:

- Partnerships Driving Innovation: Strategic collaborations, such as HiQ's alliance with the European Cloud City Network and the Frends iPaaS platform, are driving innovation in hybrid cloud integration strategies.

- Regulatory Compliance: These partnerships focus on offering solutions that ensure full compliance with data laws and regulations, critical for public and commercial sector businesses.

Cloud Integration and Digital Transformation:

- Technological Disruptions: The increasing adoption of IoT, cloud computing, and digital transformation initiatives is propelling the demand for EAI solutions across various industries in North America.

- Vendor Focus: Key players in the region, such as IBM and Fujitsu, are leading with innovations like SaaS-based security solutions, driving market growth.

- Consolidated Market: The North American EAI market is moderately consolidated, with global players focusing on cutting-edge technologies to maintain their competitive edge.

- Zero-Trust Architecture: Innovations such as the introduction of zero-trust architecture for security are becoming critical in the deployment of EAI solutions in enterprise environments.

Enterprise Application Integration Industry Overview

Global Players Dominate Semi Consolidated Market

The Enterprise Application Integration (EAI) market is characterized by a semi consolidated structure, with global players such as IBM Corporation, Fujitsu Ltd, and Microsoft holding significant market share. These technology conglomerates leverage their extensive resources, global presence, and technological expertise to dominate the market while smaller, innovative companies carve out niche roles with specialized solutions.

Comprehensive Offerings:

End-to-End Solutions: Global leaders offer comprehensive enterprise application integration solutions that cater to the diverse needs of organizations across industries.

Partnership Ecosystems: Companies like IBM and Microsoft have built extensive ecosystems of partners, enabling them to provide integration across a wide range of business applications and data sources.

Research and Development Focus:

Emerging Technologies: Key players invest heavily in R&D, focusing on innovations in artificial intelligence (AI), machine learning, and cloud computing to advance their EAI platforms.

Support for Hybrid Environments: Their integration solutions are designed to support hybrid cloud integration strategies, ensuring smooth transitions between on-premise and cloud-based infrastructures.

Innovation and Adaptability:

Cloud-Native Architectures: Market players are increasingly shifting towards cloud-native architectures to meet the growing demand for scalable, flexible solutions.

Low-Code/No-Code Tools: The introduction of low-code/no-code tools is expanding the reach of integration capabilities, allowing non-technical users to contribute to data integration services.

Security and Compliance:

Data Privacy Concerns: As enterprises grapple with growing data privacy concerns, EAI vendors and providers are emphasizing security, compliance, and governance features in their solutions to gain a competitive edge.

API Management: Robust API management for EAI is becoming a critical differentiator, allowing organizations to securely integrate a vast number of applications and endpoints.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Digital Transformation Reshaping Enterprise Landscapes

- 5.1.2 Increasing Demand for Real-time Data Access and Management

- 5.1.3 API-Driven Integration Powering the Connected Enterprise

- 5.2 Market Challenges

- 5.2.1 Availability of Open Source Software

- 5.2.2 The lack of integration makes automating simple tasks challenging, impacting operational efficiency.

- 5.3 Assessment of Impact of COVID-19 on the Industry

6 MARKET SEGMENTATION

- 6.1 Deployment Type

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.1.3 Hybrid

- 6.2 Organisation Size

- 6.2.1 Large Enterprises

- 6.2.2 Small and Medium-sized Enterprises

- 6.3 End-user Industry

- 6.3.1 BFSI

- 6.3.2 IT and Telecom

- 6.3.3 Healthcare

- 6.3.4 Retail

- 6.3.5 Government

- 6.3.6 Manufacturing

- 6.3.7 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Fujitsu Limited

- 7.1.3 Microsoft Corporation

- 7.1.4 MuleSoft LLC (Salesforce Inc.)

- 7.1.5 Oracle Corporation

- 7.1.6 SAP SE

- 7.1.7 Software AG

- 7.1.8 Tibco Software Inc.

- 7.1.9 iTransition Group

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

应用整合市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分

应用整合市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和功能划分 应用整合市场规模、份额和成长分析(按整合类型、部署模式、组件、组织规模、最终用户产业和地区划分)-2026-2033年产业预测

应用整合市场规模、份额和成长分析(按整合类型、部署模式、组件、组织规模、最终用户产业和地区划分)-2026-2033年产业预测 HubSpot咨询服务:全球市场占有率和排名、总收入和需求预测(2025-2031)

HubSpot咨询服务:全球市场占有率和排名、总收入和需求预测(2025-2031) 应用整合市场按组件、部署类型、组织规模和最终用户行业划分 - 全球预测,2025-2032 年

应用整合市场按组件、部署类型、组织规模和最终用户行业划分 - 全球预测,2025-2032 年 应用程式整合市场规模、份额和趋势分析报告:按产品、按部署、按企业规模、按整合类型、按应用程式、按行业、按地区和细分市场趋势:2024-2030

应用程式整合市场规模、份额和趋势分析报告:按产品、按部署、按企业规模、按整合类型、按应用程式、按行业、按地区和细分市场趋势:2024-2030 全球企业应用程式和整合市场,2024-2028

全球企业应用程式和整合市场,2024-2028