|

市场调查报告书

商品编码

1444558

公共事业拖拉机:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Utility Tractor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

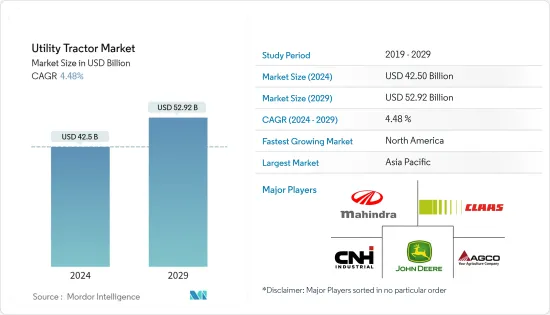

公共事业拖拉机市场规模预计到 2024 年为 425 亿美元,预计到 2029 年将达到 529.2 亿美元,在预测期内(2024-2029 年)复合年增长率为 4.48%。

主要亮点

- 公共事业拖拉机设计用于执行各种任务,例如前置装载机作业、整地和运输。这种类型的拖拉机用于农业任务,例如犁地和牵引重物。由于粮食需求的增加和农业机械化的普及,全世界农业机械的使用正在增加。公共事业拖拉机帮助农民轻鬆进行耕作过程。

- 公共事业拖拉机由 35 马力到 100 马力的部分组成,包括许多用于中小型农业作业的紧凑型公共事业拖拉机。小农越来越多地采用紧凑型公共事业拖拉机(40HP 至 70HP),因为它们比普通农用拖拉机小得多且便宜得多。儘管成本低廉,但紧凑型拖拉机可协助农民利用后铲和前端装载机等农业设备执行更多任务,从而节省人事费用。儘管坚硬的土壤条件是大型(41-50马力)拖拉机需求增加的主要原因,但它们在基础设施和建筑等非农业部门的使用不断增加,也促进了大型拖拉机需求的增加类别。因此,公共事业拖拉机行业将在未来几年内成长。

- 公共事业拖拉机可用于装载和挖掘,并配备重要的前部或后部附件,例如前端装载机和后铲。儘管如此,它也可用于景观美化、播种、种植干草和除雪,使其成为全球该领域的市场领导者。 2019年印度农业机械化水准为40.0%-45.0%。该国约 80.0% 的小农和边缘农户拥有的土地不到 5 公顷,减缓了农业机械的普及。印度农业部门对动物和人力的使用显着下降。其中许多由拖拉机和柴油发动机等石化燃料驱动的车辆提供动力。这导致了从传统农业流程向机械化农业流程的转变。

- 儘管与中国、巴西等其他新兴国家相比,印度的机械化程度较低,但绝对处于成长阶段。为了提高机械化水平,印度政府正在透过对各种设备提供补贴并支持透过前端代理商批量采购来推动“平衡农业机械化”,预计在预测期内这一数字将继续增加,公共事业市场预计将走强。

公共事业拖拉机市场趋势

人们对农业机械化的兴趣日益浓厚

- 精密农业和越来越多地采用农业技术来提高产量,正在增加世界各地少耕土地对多功能拖拉机的需求。农业培训计画的增加,促进农业机械的大规模使用,也正在提振拖拉机产业。此外,一些开发中国家的政府正在提供补贴和财政援助,以支持关键农业流程的自动化。

- 此外,各种技术进步导致预先安装 GPS 和远端资讯处理系统的现代拖拉机出现。全球农用拖拉机市场预计将受到自动拖拉机日益普及以及可用于农业目的的远端监控无线连接的广泛普及的推动。

- 现代农业,农业机械化对农民增收至关重要。然而,中国作物生产中机械的使用效率低。中国农业大学在北京进行的一项研究显示,2020年全国作物种植和收穫机械化率达71%。

- 小麦、稻米、玉米播种、收穫总合机械化率分别超过95%、85%、90%。为了加速农业机械化进程,中国政府鼓励农民使用机械,包括对购买机械、使用机械给予财政补贴,对向个体农民提供机械的合作社给予支持,我们推出了一系列政策。

- 亚太地区的农民也在寻找具有客製化功能的公共事业拖拉机,以满足他们的高效农业需求。因此,为了满足消费者的需求,国内外许多农机製造商纷纷开发出技术先进、能够适应各种农业应用的新型公共事业拖拉机,以拉动未来市场的成长。

- 2022年,约翰迪尔美国为农民推出了Gtaor公共事业拖拉机。 AutoTrac 辅助转向系统可在车辆穿过田地时保持一致、可重复的精确度和效率,进而提高操作员的工作效率。 AutoTrac 让农民能够保持警惕并专注于机器设定和控制各种田间条件。农民使用公共事业拖拉机进行采样、散布,并用精确的网格划分田地。

亚太地区主导市场

- 儘管印度拥有丰富的廉价劳动力,但对粮食的需求仍在增加,农业机械化(特别是拖拉机)的采用也增加。中国也是如此,农业机械化也有类似的趋势。印度和中国的农民对机械化越来越感兴趣,原因有几个。原因之一是人口成长和都市化导致对粮食的需求不断增加,从而需要提高农业生产力。另一个原因是人事费用上升使得机械投资更具成本效益。

- 印度北部地区,尤其是旁遮普邦、北方邦和哈里亚纳邦,多用途拖拉机在该国的普及较高。在印度,根据印度政府《农业宏观管理计画》机械化部分,为促进农业机械化提供补贴,其中包括购买35马力以下拖拉机最高3万卢比,其中包括成本的25%。 -起飞(PTO)马力。在印度,自订就业服务使小农受益,并且出现了新一代企业家,他们为小土地所有者的利益而操作多功能拖拉机。这些因素将导致预测期内该地区的市场成长。

- 中国农业机械化水准提高的趋势是农业投资的增加和政府对农业机械化的推动。农业机械化投资正在创造亚太地区对多功能拖拉机的需求。国家统计局资料显示,2019年我国拖拉机产量61.77万台。大中型拖拉机逐渐被小型拖拉机取代。

- 截至2019年终,我国农用拖拉机保有量2,224万台,其中大中型拖拉机444万台。中国也推出了「中国製造2025」计划,重点以高端机械生产农用拖拉机等90%的农业机械,到2020年将占中国细分市场三分之一的份额。支持国产拖拉机,促进国内农用拖拉机市场发展。

- 多用途拖拉机用于农业生产,马恆达 (Mahindra & Mahindra) 和约翰迪尔 (John Deere) 等国内领先公司借助其产品为该地区的农业实践做出了重大贡献。促进未来几年的市场成长。在新兴国家,由于农民可支配收入低、人事费用高,对35马力至100马力的拖拉机的需求不断增加。由于农田面积较小,农民更喜欢为农业目的量身订製的小型紧凑型/公共事业拖拉机。此外,小型拖拉机减少燃料消费量有助于增强小型和边缘农民的能力。

公共事业拖拉机产业概况

公共事业拖拉机市场高度整合,少数厂商占大部分市场占有率。 Deere & Company、CNH Industrial、AGCO Corporation、CLAAS KGaA mbH、Mahindra & Mahindra Corporation 是该市场的主要企业。新产品发布、合作伙伴关係和收购是全球领先公司采用的关键策略。除了创新和扩张之外,研发投资和新产品系列的开发可能是未来几年的关键策略。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 市场限制因素

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争公司之间敌对的强度

第五章市场区隔

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 其他亚太地区

- 世界其他地区

- 巴西

- 南非

- 其他的

- 北美洲

第六章 竞争形势

- 最采用的策略

- 市场占有率分析

- 公司简介

- Deere and Company

- CNH Global NV

- AGCO Corporation

- CLAAS KGaA mbH

- Mahindra and Mahindra Corporation

- Kubota Corporation

- Escorts Group

- Tractors and Farm Equipment Limited(TAFE)

- Kuhn Group

- Yanmar Company Limited

第七章市场机会与未来趋势

The Utility Tractor Market size is estimated at USD 42.5 billion in 2024, and is expected to reach USD 52.92 billion by 2029, growing at a CAGR of 4.48% during the forecast period (2024-2029).

Key Highlights

- Utility tractor is designed for various tasks such as front loader work, soil cultivation, and transportation. This type of tractor is used for farming operations such as plowing and pulling heavy implements. Globally the use of machinery in agriculture is increasing due to increased demand for food and higher penetration of farm mechanization. Utility tractors help the farmer carry out the agriculture process with ease.

- The utility tractors comprise a range of 35 HP to 100 HP segments, including many compact and utility-type tractors meant for small- to mid-sized farming tasks. Small-scale farmers are increasingly adopting compact utility tractors (40HP-70HP) as they are much smaller than the average agricultural tractors and priced much lower. Despite the low-cost, compact tractors can help farmers perform many tasks with the help of farm equipment, such as backhoes and front-end loaders, and save labor wage expenses. Although a key reason for the increasing demand for larger (41-50 HP) tractors is the hard soil condition, increased use in non-agricultural segments, such as infrastructure and construction fields, has also contributed to the increase in demand in this category, which will boost the utility tractors industry to grow in the coming years.

- Utility tractors can work with significant front or rear attachments, like front-end loaders and backhoes, for loading and digging. Still, they can also be used for landscaping, seeding, hay cultivation, and snow removal, which drives the market for this segment globally. The farm mechanization level in India was recorded at 40.0%-45.0% in 2019. The penetration of farm equipment is slow, as almost 80.0% of small and marginal farmers own less than five hectares of land in the country. The agriculture sector in India has witnessed a substantial decline in the use of animal and human power in the agriculture sector. Many of these are driven by fossil fuel-operated vehicles, such as tractors and diesel engines. This has shifted from the traditional agriculture process to a more mechanized one.

- Though the level of mechanization in India is lower than in other developing countries, like China and Brazil, it is certainly in a growing phase. To increase the mechanization level, the Indian government has been promoting 'Balanced Farm Mechanization' by providing subsidies on various equipment and supporting bulk buying through front-end agencies, which is expected to strengthen the utility tractors market during the forecast period.

Utility Tractor Market Trends

Growing Preference For Farm Mechanization

- Precision farming and the increasing adoption of farm technology to boost production are driving up demand for utility tractors in minimum arable landholdings across the globe. The growing number of farm training programs promoting the use of agricultural machinery on a wide scale is also driving the tractor industry. Moreover, governments in several developing nations are providing subsidies and financial aid to help automate key agricultural processes.

- Furthermore, modern tractors with pre-installed GPS and telematics systems have emerged due to different technical breakthroughs. The global agriculture tractor market is likely to be driven by the rising popularity of automated tractors and the widespread use of wireless connectivity for remote monitoring, which can be used for agriculture purposes.

- Agricultural mechanization is essential to increase farmers' income in modern agriculture. However, the use of machinery for crop production in China is inefficient. According to a study conducted by China Agricultural University (CAU), Beijing, in 2020, the national crop planting and harvesting mechanization rate reached 71%.

- The total mechanization rate of planting and harvesting exceeded 95%, 85%, and 90% for wheat, rice, and maize, respectively. To accelerate agricultural mechanization, the Chinese government issued a series of policies to encourage farmers to use machinery, including financial subsidies for machine purchases and machine operations and support for cooperatives to provide machinery for individual farmers.

- Farmers in the Asia-Pacific region also seek utility tractors with tailored features to fulfill their needs for effective farming. So, to meet consumer demand, many international and domestic agriculture machinery manufacturers are developing new technologically advanced utility tractors which can handle various farming applications to push the market to grow in the future.

- In 2022, John Deere US launched Gtaor Utility Tractor for Farmers. The AutoTrac-assisted steering system increases operator productivity by maintaining consistent, repeatable accuracy and efficiency as the vehicle moves across the field. With AutoTrac engaged, farmers can remain alert and focused on controlling machine settings and varying field conditions. Farmers use the utility tractor for precise grid sampling, spraying, and field boundary creation.

Asia-Pacific Dominates the Market

- Despite abundant and cheap labor in India, there has been a growing demand for food, which has led to an increase in the adoption of farm mechanization, particularly in the form of tractors. This is also true for China, where there has been a similar trend toward mechanization in agriculture. For several reasons, farmers in India and China are increasingly turning to mechanization. One reason is the growing demand for food due to population growth and urbanization, which has led to a need for increased productivity in agriculture. Another reason is the rising cost of labor, which has made it more cost-effective to invest in machinery.

- The penetration of utility tractors in the country is higher in North India, particularly in Punjab, Uttar Pradesh, and Haryana. In India, under the mechanization component of the Macro-Management of Agriculture Scheme, by the Indian government, there is a provision of subsidy to promote agricultural mechanization, including 25% of the cost limited to INR 30,000 for buying tractors of up to 35 Power-take-off (PTO) HP. In India, custom hiring services have benefitted smaller farmers, and a new breed of entrepreneurs who operate utility tractors for the benefit of small landholders has emerged. These factors will lead the market to grow in the region during the forecasting period.

- The trend behind the increase in farm mechanization in China has been increased agricultural investments and the government's push toward farm mechanization. The investments in farm mechanization create the demand for utility tractors in the Asia Pacific. According to data from the National Bureau of Statistics of China, China produced 617,700 tractors in 2019. Large and medium-sized tractors gradually replaced small tractors.

- By the end of 2019, China boasted of 22.24 million agricultural tractors, including 4.44 million large- and medium-sized tractors. China has also introduced the 'Made in China 2025' scheme, which focuses on producing 90% of its agricultural equipment with high-end machines, like agricultural tractors, holding a one-third share of their segments by 2020. This, in turn, boosts indigenously produced tractors and propels the country's agricultural tractor market.

- Utility Tractors are being used for the agricultural process, and major players in the country are contributing to it, such as Mahindra & Mahindra and John Deere, with the help of their products, are contributing a lot to the agricultural practices carried out in the region to increase the market growth in the coming years. In developing countries, the demand for 35HP - 100HP tractors is high due to the low disposable income of farmers and high labor costs. Farmers prefer small and customized compact/utility tractors for agricultural purposes due to small farmland sizes. Moreover, lesser fuel consumption by small tractors helps to empower small and marginal farmers.

Utility Tractor Industry Overview

The utility tractors market is highly consolidated, with few players cornering most of the market share. Deere & Company, CNH Industrial, AGCO Corporation, CLAAS KGaA mbH, and Mahindra & Mahindra Corporation are major players in this market. New product launches, partnerships, and acquisitions are the major strategies the leading global companies adopt. Along with innovations and expansions, investments in R&D and developing novel product portfolios will likely be crucial strategies in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Geography

- 5.1.1 North America

- 5.1.1.1 United States

- 5.1.1.2 Canada

- 5.1.1.3 Rest of North America

- 5.1.2 Europe

- 5.1.2.1 Germany

- 5.1.2.2 United Kingdom

- 5.1.2.3 France

- 5.1.2.4 Spain

- 5.1.2.5 Italy

- 5.1.2.6 Rest of Europe

- 5.1.3 Asia-Pacific

- 5.1.3.1 China

- 5.1.3.2 Japan

- 5.1.3.3 India

- 5.1.3.4 Rest of Asia-Pacific

- 5.1.4 Rest of the World

- 5.1.4.1 Brazil

- 5.1.4.2 South Africa

- 5.1.4.3 Other Countries

- 5.1.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Deere and Company

- 6.3.2 CNH Global NV

- 6.3.3 AGCO Corporation

- 6.3.4 CLAAS KGaA mbH

- 6.3.5 Mahindra and Mahindra Corporation

- 6.3.6 Kubota Corporation

- 6.3.7 Escorts Group

- 6.3.8 Tractors and Farm Equipment Limited (TAFE)

- 6.3.9 Kuhn Group

- 6.3.10 Yanmar Company Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球智慧拖拉机市场-2025-2030年预测

全球智慧拖拉机市场-2025-2030年预测 三点式连结:2025-2031年全球市占率及排名、总销售量及需求预测

三点式连结:2025-2031年全球市占率及排名、总销售量及需求预测 全球全轮驱动拖拉机市场(按马力范围、安装类型、应用、通路、变速箱类型、发动机类型、最终用户和技术划分)—预测(2025-2032 年)大型推土机市场按设备类型、马力范围、应用、最终用户、销售管道和动力传动系统划分-2025-2032年全球预测履带拖拉机市场按应用、马力范围、最终用户、燃料类型、变速箱类型和分销渠道划分-2025-2032年全球预测拖拉机农具市场(按农具类型、应用、销售管道和最终用户划分)—2025-2032 年全球预测电动拖拉机市场:按拖拉机类型、功率输出、应用、分销管道和充电基础设施划分-2025-2032年全球预测

全球全轮驱动拖拉机市场(按马力范围、安装类型、应用、通路、变速箱类型、发动机类型、最终用户和技术划分)—预测(2025-2032 年)大型推土机市场按设备类型、马力范围、应用、最终用户、销售管道和动力传动系统划分-2025-2032年全球预测履带拖拉机市场按应用、马力范围、最终用户、燃料类型、变速箱类型和分销渠道划分-2025-2032年全球预测拖拉机农具市场(按农具类型、应用、销售管道和最终用户划分)—2025-2032 年全球预测电动拖拉机市场:按拖拉机类型、功率输出、应用、分销管道和充电基础设施划分-2025-2032年全球预测 2025 年全球四轮驱动拖拉机市场报告

2025 年全球四轮驱动拖拉机市场报告 输电绝缘子市场,按材料类型、按绝缘子类型、按电压、按应用、按最终用户、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

输电绝缘子市场,按材料类型、按绝缘子类型、按电压、按应用、按最终用户、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 全球氢动力拖拉机市场

全球氢动力拖拉机市场