|

市场调查报告书

商品编码

1444638

主动资料仓储 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Active Data Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

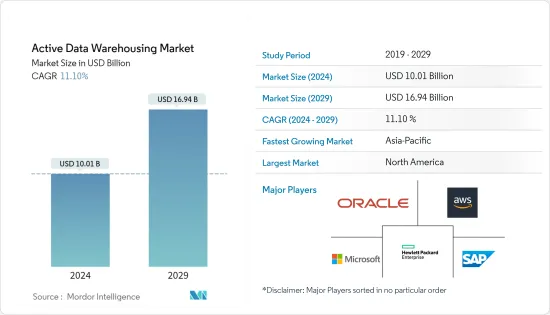

主动资料仓储市场规模预计到 2024 年为 100.1 亿美元,预计到 2029 年将达到 169.4 亿美元,在预测期内(2024-2029 年)CAGR为 11.10%。

此外,预计发展中国家的需求成长将在整个预测期内为活跃资料仓储市场带来新的机会。

主要亮点

- 由于对下一代商业智慧的持续需求以及组织产生的资料量不断增加等因素,活跃的资料仓储市场即将发生重大转变。 ADW 允许使用者即时存取大量复杂资讯。这些资料被有效且相关地组织,预计将有助于预测期内的市场成长。对低延迟和高速分析的需求不断增长,加上商业智慧在企业管理中日益重要的作用,预计将显着推动市场需求。

- 此外,据 Oracle 称,在巴西,近 90% 的人口居住在城市地区,SKY Brasil 拥有约 29% 的直接入户卫星服务市场份额。该公司选择在 Oracle 云端基础架构上执行的 Oracle 自治资料仓储整合到 Oracle Siebel CRM 中,以执行即时、复杂的行销分析。与先前的本地解决方案相比,部署者的部署和开始生产时间减少了 90%,同时基础设施成本节省了 60%。此外,ADW 显着降低了计算成本,再加上将资料合併在一个位置,预计这将对市场成长产生积极影响。

- 此外,ADW 大大降低了计算成本,再加上将资料合併在一个位置,预计这也将对市场成长产生积极影响。除这些因素外,在全球范围内,组织中大数据趋势的显着上升导致对分析的需求不断增加,预计这也将有助于市场成长。此外,为了扩展运算能力以满足需求并在使用高峰时轻鬆缩减运算能力,市场上的供应商一直遵循基于资源使用情况的云端资料仓储定价模型。它解决了供应商可能寻求的规模经济问题以及客户要求的灵活性问题。然而,固定容量的资料仓储迫使组织购买超出所需的运算容量。

- 由于人们对资料管理和复杂性不断增加的担忧日益增加,资料仓储引起了人们对实际应用程式的极大兴趣,特别是在金融、商业、医疗保健和其他行业。数位化企业流程导致 IT 产业采用具有资料分析功能的新技术先进营运。因此,现代资料仓储系统促进了数位业务营运所需的即时、企业级分析和资讯洞察的开发。

- 然而,主动资料仓储市场受到多种因素的限制,包括高昂的安装成本和日益增加的网路威胁。

- COVID-19 对市场产生了复杂的影响。例如,Burtch Works 和国际分析研究所 (IIA) 对美国 300 名分析专业人士进行的一项调查显示,超过 43% 的受访者表示,分析是他们采取行动做出重要选择的关键因素,以应对COVID-19 问题。受疫情影响,企业缩减营运、削减开支、关闭办公室。在家工作范式的广泛采用给企业带来了另一个困难。基于云端的资料仓储的安装预计将因此类发展而加速。此次疫情为采用资料仓储提供了许多优势,包括成本效益、获得大型技能库以及增强的可扩展性。

主动资料仓储市场趋势

智慧型手机渗透率的上升可能会推动市场成长

- 行动电话,尤其是智慧型手机,在人们中变得越来越普遍。透过现代资讯和通讯技术(ICT),使用者可以快速获取重要资讯。根据 GSMA 统计,截至去年,全球活跃 iOS 和 Android 智慧型手机数量超过 62 亿部,预计到 2025 年将达到 74 亿部。此外,行动技术在一系列电脑系统中的使用正在增加,包括资料仓储(DW )、商业智慧(BI) 系统和资料分析系统。

- 手机充当资料库,储存了大量的用户资料。储存的资料可以根据用户批准的条款和条件进行分析。资料可以透过各种活动资料仓储检索和分析,以收集使用者的多种特征。智慧型手机用户需要庞大的云端资料库来进行资料访问,因此需要资料仓储解决方案,从而推动市场成长。

- 此外,由于中国、巴西和印度等新兴国家智慧型手机使用量的增加以及社群媒体流量的增加,不断增加的资料流需要更多的功能,包括即时资料储存。

- 此外,预计各国智慧型手机使用量的不断增长将推动市场成长。例如,根据资讯和广播部的数据,2022年11月,印度拥有超过12亿手机用户,其中6亿智慧型手机用户。此外,有人提到,除了相对便宜的资料速率外,智慧型手机的广泛使用还导致个人在行动装置上消费大量资讯和娱乐。

预计北美将占据重要的市场份额

- 与欧洲或亚洲组织相比,美国组织是多个垂直领域分析的重要采用者。由于庞大的需求和供应商的存在,美国被认为是市场上的重要国家。此外,根据 GSMA 的数据,去年北美有 3.29 亿行动服务用户,占总人口的 84%。由于该地区的大多数新的独特客户来自美国,该地区营运商的整体潜在市场已接近饱和。到 2025 年,该地区预计将增加 1,200 万用户,其中 75% 由美国提供。

- 此外,该国的消费者也看重能够为他们的问题提供即时帮助的供应商;因此,许多零售组织正在采用主动资料仓储概念来增强忠诚度管理应用程序,这些应用程式在留住消费者方面发挥着至关重要的作用。

- 行动宽频的成长导致该国大数据分析和云端运算的增加。到 2022 年,美国将拥有相当多的分析采用者,鼓励多家企业从本地部署转向基于云端的部署,预计这将是资料仓储安装的潜在市场。此外,随着该国贸易活动的增加和企业数量的增加,物流活动预计也会增加。然而,该国不断增加的公共债务预计将推高通货膨胀率,从而限制小商贩的活动。

- 根据微软的说法,人工智慧驱动的虚拟代理为新兴管道做出了巨大贡献。自然语言处理和机器学习等功能能够全天候 (24/7) 提供智慧、对话式且快速的解决方案。它显示了公司为提高客户满意度而投入的重要性和支出。因此,对此类复杂平台和分析的需求将继续帮助活跃资料仓储保持稳定的成长率。

- 市场的另一个关键驱动因素是对具有 BI 功能的解决方案的需求不断增长。政府措施和医生用于改善初级保健(例如疾病的检测和预防)的资料分析的增加正在推动市场发展。因此,许多医疗保健组织已开始在主动资料仓储上投入更多资金,以节省成本。在预测期内,保险公司和其他 BFSI 公司对即时分析和 BI 的需求不断增长,预计将提振美国对 ADW 的需求。

主动资料仓储产业概述

主动资料仓储市场高度分散,国内外多家厂商竞争激烈,包括微软公司、甲骨文公司、SAP SE等。技术进步也为企业带来了相当大的竞争优势,市场正在不断扩大。也见证了多个合作伙伴关係。

2022 年 5 月,戴尔技术公司和 Snowflake Inc. 宣布就一个新专案建立合作伙伴关係,将其本地储存产品组合中的资料与 Snowflake 资料云端连结起来。名为 Snowflake Data Cloud 的云端原生平台旨在消除对单独资料湖和仓库的需求,同时实现整个企业的安全资料共享。它允许用户聚合来自各种软体即服务和云端平台的资料集,并将其提供给任何用户。此外,2022 年 5 月,Oracle 和着名企业云端资料管理供应商 Informatica 宣布建立策略合作关係,使 Informatica 的资料整合和治理解决方案能够与 Oracle 云端基础架构结合使用。此外,Oracle 还指定 Informatica 作为企业云端资料治理以及 OCI 上资料仓储和 Lakehouse 解决方案整合的推荐合作伙伴。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代产品的威胁

- 竞争激烈程度

- 评估 COVID-19 对市场的影响

第 5 章:市场动态

- 市场驱动因素

- 各行业越来越多地采用商业智慧和大数据分析解决方案

- 智慧型手机渗透率的上升可能会推动市场成长

- 市场挑战

- 资源消耗大、实施时间长

- 日益增长的网路威胁可能会限制市场成长

第 6 章:市场细分

- 依部署类型

- 本地部署

- 云

- 杂交种

- 按企业规模

- 中小企业

- 大型企业

- 按行业分类

- BFSI

- 製造业

- 卫生保健

- 零售

- 其他垂直行业

- 地理

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 欧洲其他地区

- 亚太

- 中国

- 日本

- 亚太其他地区

- 世界其他地区

- 北美洲

第 7 章:竞争格局

- 公司简介

- Treasure Data Inc.

- Cloudera Inc.

- Snowflake Computing Inc.

- Oracle Corporation

- Hewlett Packard Enterprise Company

- Microsoft Corporation

- SAP SE

- Amazon Web Services, Inc.

- VMware Inc. (Pivotal Software Inc.)

- Huawei Technologies Co. Ltd

- Teradata Corporation

- Kognitio Ltd

- IBM Corporation

第 8 章:投资分析

第 9 章:市场的未来

The Active Data Warehousing Market size is estimated at USD 10.01 billion in 2024, and is expected to reach USD 16.94 billion by 2029, growing at a CAGR of 11.10% during the forecast period (2024-2029).

Additionally, the growth in demand from developing nations is anticipated to open up new opportunities for the active data warehousing market throughout the projection period.

Key Highlights

- The active data warehousing market is poised for a significant shift, owing to factors like the ongoing demand for next-gen business intelligence coupled with the growing amount of data organizations generate. ADW allows users to access an enormous range of complex information in real-time. The data is organized efficiently and relevantly, which is anticipated to aid market growth over the forecast period. The rising demand for low latency and high-speed analytics, combined with the growing role of business intelligence in enterprise management, is expected to drive the market demand significantly.

- Further, according to Oracle, in Brazil, with nearly 90% of the population living in urban areas, SKY Brasil has approximately 29% market share for direct-to-home satellite services. The company opted for Oracle's Autonomous Data Warehouse running on Oracle Cloud Infrastructure, integrated into Oracle's Siebel CRM, to perform real-time, sophisticated marketing analytics. The deployer achieved 90% less time in deployment and commencing production than its previous on-premise solution while realizing 60% of infrastructure cost savings. Furthermore, ADW significantly diminishes the cost of computing, coupled with combining data in a single location, which is further projected to impact market growth positively.

- Additionally, ADW substantially decreases the cost of computing, coupled with combining data in a single location, which is also expected to impact the market growth positively. Along with these factors, globally, the significant rise in the Big Data trend in organizations is leading to the increasing demand for analytics, which is also projected to aid market growth. Also, to scale the computing capacity to match the demand and effortlessly scale back down when the usage peaks, vendors in the market have been following resource usage-based models for the pricing of cloud data warehousing. It addresses the issues of economies of scale that vendors may look for and the flexibility that clients demand. However, fixed-capacity data warehouses force organizations to buy more computing capacity than needed.

- Data warehousing has generated a lot of interest in real-world applications, notably in finance, business, healthcare, and other industries, as a result of growing concerns about data management and rising complexity. Digitalizing corporate processes led to the adoption of new technologically advanced operations with data analytics capabilities in the IT industry. As a result, modern data warehouse systems facilitate the development of the real-time, enterprise-scale analytics and information insights required for digital business operations.

- However, the market for active data warehousing is being restrained by various factors, including high installation costs and increased cyber threats.

- COVID-19 created a mixed impact on the market. For instance, in a survey of 300 analytics professionals in the US, Burtch Works and the International Institute for Analytics (IIA) revealed that over 43% of respondents said that analytics was a crucial factor in their actions to make essential choices in response to the COVID-19 problem. Companies scaled back operations due to the pandemic epidemic, reduced expenses, and closed offices. The widespread adoption of the work-from-home paradigm presents another difficulty for firms. Cloud-based data warehouse installations are anticipated to be accelerated by such developments. The pandemic provided numerous advantages for adopting data warehousing, including cost-effectiveness, access to a large skill pool, and enhanced scalability.

Active Data Warehousing Market Trends

Rising Penetration of Smartphones may Drive the Market Growth

- Mobile phones, especially smartphones, are becoming increasingly widespread among various people. Users may get essential information rapidly owing to modern information and communication technology (ICT). According to the GSMA, there are more than 6.2 billion active iOS and Android smartphones worldwide as of last year, and it is expected to reach 7.4 billion by 2025. Additionally, the usage of mobile technology is increasing across a range of computer systems, including Data Warehouse (DW), Business Intelligence (BI) systems, and Data Analytic systems.

- Mobile phones act as a database, where a considerable amount of user data is stored. The stored data can be subjected to analysis as per the T&C approval by the user. The data can be retrieved and analyzed by various active data warehouses to collect multiple traits of the user. Smartphone users need a vast cloud database for data access, thereby needing data warehousing solutions, driving market growth.

- Further, an increasing data stream necessitates more capabilities, including real-time data storage, as a result of the rising smartphone usage in emerging nations like China, Brazil, and India, as well as the increased social media traffic.

- Moreover, the growing smartphone usage across various countries is anticipated to drive market growth. For instance, according to the Ministry of Information and Broadcasting, in November 2022, India had more than 1.2 billion mobile phone subscribers, including 600 million smartphone users. Furthermore, it was mentioned that in addition to having relatively cheap data rates, the widespread usage of smartphones has led to individuals consuming a lot of information and entertainment on their mobile devices.

North America is Expected to Hold a Significant Market Share

- The United States organizations are significant adopters of analytics across several verticals, compared with European or Asian organizations. The United States is considered an essential country in the market because of the considerable demand and presence of vendors. Also, according to GSMA, there were 329 million mobile service subscribers in North America last year, or 84% of the total population. With most of the region's new unique customers coming from the United States, the total addressable market for the operators in the area is approaching close to saturation. The United States would provide 75% of the 12 million more users anticipated in the region by 2025.

- Also, consumers in the country value vendors that provide real-time assistance with their issues; hence, many retail organizations are adopting active data warehousing concepts to enhance loyalty management applications that play a crucial role in retaining consumers.

- The growth of mobile broadband led to increased Big Data analytics and cloud computing in the country. The United States, with a considerable number of analytics adopters in 2022, encouraged multiple enterprises to switch from on-premise to cloud-based deployment, which is estimated to be an addressable market for data warehouse installations. Furthermore, logistics activities are expected to increase with the rise in trade activities and the growing number of businesses in the country. However, the ever-increasing public debt of the country is expected to drive the inflation rate up, thus curtailing small vendors' activities.

- As per Microsoft, AI-driven virtual agents have contributed significantly toward emerging channels. Features like natural language processing and machine learning possess capabilities to deliver smart, conversational, and fast solutions 24/7. It indicates the importance and spending that companies direct toward improving customer satisfaction. Therefore, the demand for such sophisticated platforms and analytics will continue to help register a steady growth rate of active data warehousing.

- Another key driver in the market is the increasing need for solutions with BI capabilities. Government initiatives and increased data analytics physicians use for improved primary care, such as the detection and prevention of diseases, are driving the market. Thus, many healthcare organizations have started spending more on active data warehousing to increase cost savings. Over the forecast period, the increasing demand for real-time analytics and BI from insurance and other BFSI companies is expected to bolster the demand for ADW in the United States.

Active Data Warehousing Industry Overview

The Active Data Warehousing Market is highly fragmented, with several domestic and international players in a fairly-contested market space, including Microsoft Corporation, Oracle Corporation, SAP SE, etc. Technological advancements are also bringing considerable competitive advantage to companies, and the market is also witnessing multiple partnerships.

In May 2022, Dell Technologies Inc. and Snowflake Inc. announced a partnership on a new project to link data from its on-premises storage portfolio with the Snowflake Data Cloud. A cloud-native platform called Snowflake Data Cloud is intended to do away with the need for separate data lakes and warehouses while enabling safe data sharing throughout enterprises. It allows users to aggregate datasets from various software-as-a-service and cloud platforms and make them available to any user. Also, in May 2022, Oracle and Informatica, a prominent provider of enterprise cloud data management, announced a strategic relationship that will enable Informatica's data integration and governance solutions to be used with Oracle Cloud Infrastructure. Additionally, Oracle has designated Informatica as a recommended partner for enterprise cloud data governance and integration for data warehouse and lakehouse solutions on OCI.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in the Adoption of Business Intelligence and Big Data Analytics Solutions in Various Industries

- 5.1.2 Rising Penetration of Smartphones may Drive the Market Growth

- 5.2 Market Challenges

- 5.2.1 High Consumption of Resources and Time Required for Implementation

- 5.2.2 Growing Cyber Threats may Restrain the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Type of Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.1.3 Hybrid

- 6.2 By Size of Enterprise

- 6.2.1 Small and Medium-sized Enterprises

- 6.2.2 Large Enterprises

- 6.3 By Industry Vertical

- 6.3.1 BFSI

- 6.3.2 Manufacturing

- 6.3.3 Healthcare

- 6.3.4 Retail

- 6.3.5 Other Industry Verticals

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 Rest of Asia-Pacific

- 6.4.4 Rest of the World

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Treasure Data Inc.

- 7.1.2 Cloudera Inc.

- 7.1.3 Snowflake Computing Inc.

- 7.1.4 Oracle Corporation

- 7.1.5 Hewlett Packard Enterprise Company

- 7.1.6 Microsoft Corporation

- 7.1.7 SAP SE

- 7.1.8 Amazon Web Services, Inc.

- 7.1.9 VMware Inc. (Pivotal Software Inc.)

- 7.1.10 Huawei Technologies Co. Ltd

- 7.1.11 Teradata Corporation

- 7.1.12 Kognitio Ltd

- 7.1.13 IBM Corporation