|

市场调查报告书

商品编码

1444646

耐火材料:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Refractories - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

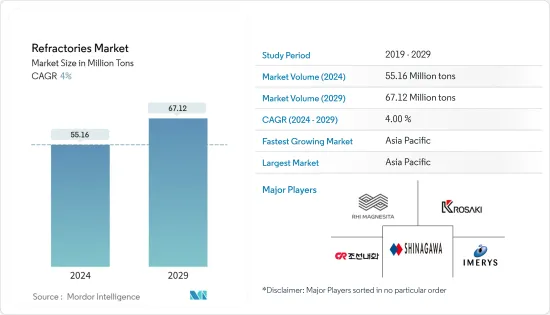

2024年耐火材料市场规模预估为5,516万吨,预估至2029年将达到6,712万吨,预测期间(2024-2029年)复合年增长率为4%。

由于COVID-19的影响,许多国家进入封锁状态,极大地影响了全球经济,经济和工业活动暂时停止。耐火材料市场也对钢铁、水泥、能源化工、陶瓷等终端用户产业的生产和需求产生影响。即使在大流行之后,最终用户产业仍在成长。这反映了经济开放后产品需求的增加。

主要亮点

- 从中期来看,推动所研究市场的关键因素是新兴国家钢铁产量的强劲成长以及有色金属材料产量的增加。耐火材料用于黑色金属和有色金属产品的内衬应用。

- 此外,玻璃产业的高需求是推动成长的主要因素。

- 同时,日益增强的环保意识促使世界各地的政府和环境机构制定了耐火材料的使用和处置指南。它可能会阻碍市场成长。

- 印度钢铁业的成长潜力预计将为研究市场提供新的机会。

- 亚太地区可能会主导市场并维持最高的复合年增长率。中国、俄罗斯、墨西哥、南非等新兴国家正大力投资大型基础建设计划,预计将显着促进钢铁业的成长。

耐火材料市场趋势

钢铁业需求增加

- 钢铁业是耐火材料的主要终端用户,约占市场的70%。这些材料可以承受 260 度C(500 °F) 至 1850 度C(3400 °F) 的高温,而物理特性不会发生显着变化。

- 耐火材料在钢铁工业的主要应用包括用于生产钢的炉衬、用于在进一步加工前加热钢的炉子以及用于容纳和运输金属和炉渣的容器,包括用于热气体通过的烟道和烟囱。 。实施和其他应用程式。

- 根据世界钢铁协会的数据,2023 年 2 月 63 个国家的粗钢产量为 1.424 亿吨。这显示了全球普遍的需求前景,有助于推动钢铁生产活动。

- 2023年2月排名前10位的钢铁生产国包括中国(8010万吨)、印度(10万吨)、日本(690万吨)、美国(600万吨)、俄罗斯(560万吨)。 。

- 2022年9月,Essar宣布计画在2025年投资40亿美元,在沙乌地阿拉伯建造和试运行一座年产400万吨的钢铁设施。

- 在欧盟,低碳钢需求持续復苏,经济信心和投资条件也在改善。然而,与难民危机和英国相关的政治形势是我们财务状况面临的不确定性风险。预计该地区的钢铁需求在预测期内将缓慢增长。

- 所有上述因素预计将在预测期内推动全球市场。

亚太地区主导市场

- 在亚太地区,中国是最大的经济体,也是全球最大的製造业和生产之一。由于原料供应充足,中国在耐火材料市场的消费和生产方面占据主导地位。

- 中国是世界上最大的钢铁生产国。根据世界钢铁协会报告,2023年2月中国产量约8,010万吨,较2022年2月成长5.6%。国内巨大的钢材需求预示着耐火材料市场的机会。

- 印度国内粗钢产量预计到2030-31年将达2.55亿吨。在2022-23年联盟预算中,印度政府向钢铁部拨款620万美元。

- 此外,根据「十四五」计画(2021-2025年),中国设定了约1100吉瓦的燃煤发电装置目标。因此,网路营运商国家电网和中国电力委员会正在製定在该国开发数百座新燃煤发电厂的计画。

- 日本钢铁联合会的资料显示,2022年国内粗钢产量达8,920万吨,而2021年为9,630万吨。

- 总体而言,预计亚太地区耐火材料需求在预测期内将大幅增加。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 耐火材料在钢铁工业的继续使用

- 非铁金属产量增加

- 抑制因素

- 中国耐火材料产量下降

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章市场区隔(市场规模(数量))

- 产品类别

- 非黏土耐火材料

- 菱镁砖(重烧镁砂、电熔镁砂、轻烧氧化镁)

- 氧化Brick

- Brick

- 铬铁矿砖

- 其他产品类型(碳化物、硅酸盐)

- 黏土耐火材料

- 高铝

- 耐火粘土

- 绝缘

- 非黏土耐火材料

- 最终用户产业

- 钢

- 能源和化学品

- 非铁金属

- 水泥

- 陶瓷製品

- 玻璃

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、合作与协议

- 市场占有率分析

- 主要企业采取的策略

- 公司简介

- Chosun Refractories

- Harbisonwalker International

- IFGL Refractories Ltd

- Imerys

- Intocast AG

- Krosaki Harima Corporation

- Magnezit Group

- Minerals Technologies Inc.

- Morgan Advanced Materials

- Puyang Refractories Group Co., Ltd

- Refratechnik

- RHI Magnesita GmbH

- Saint-Gobain

- Shinagawa Refractories Co. Ltd

- Vesuvius

第七章市场机会与未来趋势

- 扩大耐火材料回收的投资与研究

The Refractories Market size is estimated at 55.16 Million tons in 2024, and is expected to reach 67.12 Million tons by 2029, growing at a CAGR of 4% during the forecast period (2024-2029).

Due to COVID-19, numerous countries were in lockdown, significantly affecting the global economy, and economic and industrial activities were temporarily halted. The refractories market also witnessed a repercussion in production and demand from the end-user industries, such as iron and steel, cement, energy and chemicals, ceramics, etc. Although in the post-pandemic period, the end-user industries are growing because of the growing demand for products after economies open up.

Key Highlights

- Over the medium term, the significant factors driving the market studied are the strong growth of iron and steel production in emerging countries and the increased output of non-ferrous materials. The refractories are used for internal lining applications in iron steel and non-ferrous productions.

- Moreover, high demand from the glass industry is the primary factor driving the growth.

- On the flip side, due to increasing environmental awareness, government agencies and environmental agencies worldwide are laying down guidelines regarding the usage and disposal of refractories. It is likely to hinder market growth.

- The growth potential of the Indian steel industry is expected to provide new opportunities for the market studied.

- The Asia-Pacific region will likely dominate the market and register the highest CAGR. Emerging countries like China, Russia, Mexico, and South Africa are investing heavily in large-scale infrastructure projects, which are expected to boost the iron and steel industry's growth significantly.

Refractories Market Trends

Increasing Demand from the Iron and Steel Industry

- The iron and steel industry is the primary end user of refractories, which accounts for around 70% of the market. These materials can withstand high temperatures, ranging from 260°C (500°F) to 1850°C (3400°F), without any significant change in their physical properties.

- The major refractory applications in the iron and steel industry include using internal furnace linings to make iron and steel, in furnaces for heating steel before further processing, in vessels for holding and transporting metal and slag, in the flues or stacks through which hot gases are conducted, and other applications.

- According to the World Steel Association, the production of crude steel for 63 countries in the month of February 2023 was 142.4 million metric tons (Mt). It indicates the demand prospect prevailing worldwide, which is instrumental in driving steel production activities.

- The top 10 steel-producing countries in the month of February 2023 included China (80.1 Mt), India (10 Mt), Japan (6.9 Mt), the United States (6 Mt), Russia (5.6 Mt), and various others.

- In September 2022, Essar announced its plans to invest USD 4 billion in building and commissioning a four-mtpa steel complex in Saudi Arabia by 2025.

- In the European Union, a mild steel demand recovery continues while improving economic sentiment and investment conditions. However, uncertainties in the political landscape related to the refugee crisis and Brexit are some of the risks to the financial situation. The demand for steel in the region is anticipated to grow slowly over the forecast period.

- All the factors above are expected to drive the global market during the forecast period.

Asia-Pacific region to Dominate the Market

- In the Asia-Pacific region, China is the largest economy and one of the world's largest manufacturing and production industries. China dominates the refractories market in terms of consumption and production owing to the abundant supply of raw materials.

- China is the largest producer of steel in the world. As per the World Steel Association report, China produced around 80.1 Mt (million tons) in February 2023, which is up by 5.6% compared to February 2022. This massive demand for steel in the country projects market opportunities for refractories.

- In India, by FY 2030-31, crude steel actual production in the country is forecasted to reach 255 MT. In Union Budget 2022-23, the Indian government allocated USD 6.2 million to the Ministry of Steel.

- Furthermore, China, under its 14th Five-Year Plan (2021-2025), has set coal-power capacity targets to about 1,100 GW. Thus, the network operator State Grid and the China Electricity Council have targeted plans to develop hundreds of new coal-fired power stations in the country.

- As per the data of the Japan Iron and Steel Federation, the crude steel production in the country reached 89.2 million tons in 2022, compared to 96.3 million tons in 2021.

- Overall, refractory demand in the Asia-Pacific region is expected to grow significantly during the forecast period.

Refractories Industry Overview

The refractories market stands to be fragmented in nature. The major players (not in any particular order) include RHI Magnesita GmbH, Chosun Refractories ENG Co., Ltd., Krosaki Harima Corporation, Shinagawa Refractories Co., Ltd., and Imerys.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Continuous Usage of Refractories in the Iron and Steel Industry

- 4.1.2 Increase in the Production of Non-ferrous Metals

- 4.2 Restraints

- 4.2.1 Decreasing Production of Refractories in China

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Non-clay Refractory

- 5.1.1.1 Magnesite Brick (Dead Burned Magnesia, Fused Magnesia, and Caustic Calcined Magnesia)

- 5.1.1.2 Zirconia Brick

- 5.1.1.3 Silica Brick

- 5.1.1.4 Chromite Brick

- 5.1.1.5 Other Product Types (Carbides, Silicates)

- 5.1.2 Clay Refractory

- 5.1.2.1 High Alumina

- 5.1.2.2 Fireclay

- 5.1.2.3 Insulating

- 5.1.1 Non-clay Refractory

- 5.2 End-user Industry

- 5.2.1 Iron and Steel

- 5.2.2 Energy and Chemicals

- 5.2.3 Non-ferrous Metals

- 5.2.4 Cement

- 5.2.5 Ceramic

- 5.2.6 Glass

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chosun Refractories

- 6.4.2 Harbisonwalker International

- 6.4.3 IFGL Refractories Ltd

- 6.4.4 Imerys

- 6.4.5 Intocast AG

- 6.4.6 Krosaki Harima Corporation

- 6.4.7 Magnezit Group

- 6.4.8 Minerals Technologies Inc.

- 6.4.9 Morgan Advanced Materials

- 6.4.10 Puyang Refractories Group Co., Ltd

- 6.4.11 Refratechnik

- 6.4.12 RHI Magnesita GmbH

- 6.4.13 Saint-Gobain

- 6.4.14 Shinagawa Refractories Co. Ltd

- 6.4.15 Vesuvius

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Investments and Research on the Recycling of Refractories

耐火材料市场:依碱度、物理形态、製造流程、产品、应用划分 - 2025-2030 年全球预测

耐火材料市场:依碱度、物理形态、製造流程、产品、应用划分 - 2025-2030 年全球预测 2030 年耐火材料市场预测:按形状、化学成分、最终用户和地区进行的全球分析

2030 年耐火材料市场预测:按形状、化学成分、最终用户和地区进行的全球分析 2024-2028年全球耐火材料市场

2024-2028年全球耐火材料市场 全球耐火材料市场 2024-2031

全球耐火材料市场 2024-2031 全球耐火材料市场:按形状、碱度、最终用途产业、製造流程、产品、地区 - 预测至 2029 年

全球耐火材料市场:按形状、碱度、最终用途产业、製造流程、产品、地区 - 预测至 2029 年 耐火材料市场:依形状、依产品、按碱度、依最终用途产业、按地区

耐火材料市场:依形状、依产品、按碱度、依最终用途产业、按地区 全球耐火材料市场:市场规模和占有率分析 - 趋势、驱动因素、竞争格局和预测(2024-2030)

全球耐火材料市场:市场规模和占有率分析 - 趋势、驱动因素、竞争格局和预测(2024-2030) 中国的耐火材料市场

中国的耐火材料市场 2024-2032 年按形式、碱度、製造工艺、成分、耐火矿物、应用和地区分類的耐火材料市场报告

2024-2032 年按形式、碱度、製造工艺、成分、耐火矿物、应用和地区分類的耐火材料市场报告 2024 年耐火材料世界市场报告

2024 年耐火材料世界市场报告