|

市场调查报告书

商品编码

1686526

移动式製图系统:市场占有率分析、产业趋势与成长预测(2025-2030)Mobile Mapping Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

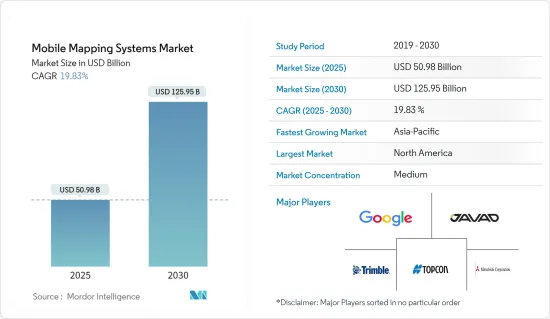

移动式製图系统市场规模预计在 2025 年为 509.8 亿美元,预计到 2030 年将达到 1259.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 19.83%。

卫星测绘技术的快速普及及其与智慧型手机和物联网 (IoT) 连接设备的无缝整合正在推动市场成长。

随着全球都市化进程加快以及政府措施的推动,智慧城市迅速扩张。智慧城市只有有了3D地图才能实现。透过对 3D 城市建模、自主导航、交通、灾害管理、道路资产数位化和减少污染的支持,智慧城市行动地图技术旨在透过优化资源和维持永续性来提高生活品质。智慧型手机和互联网的使用在管理和存取资料方面发挥关键作用。

此外,行动导航用于环境监测地理资讯系统(GIS)在环境监测的应用也越来越多。环境研究人员正在采用移动式製图GIS 工具来帮助预测和监测风暴和飓风。美国太空总署资助的生态系统监测和自然资源管理研究计划正在推动移动式製图领域的收益成长。

移动式製图系统有多种应用,包括开发用于行人导航的室内地图、用于自动驾驶汽车的高清地图、资产和基础设施管理、航空测量、管道测量、水文测量、疏浚以及海洋定位和挖掘作业。

按需部署系统的出现标誌着移动式製图市场的曲折点,它以较低的前期成本(按月/以季度为基础向用户收费)提供了高灵活性和准确性。本公司提供基于订阅的模式来应对永久用户许可的需求。

新冠疫情导致 IT 产业快速重组,企业纷纷转向远距办公。疫情期间,移动式製图市场显着成长。一些公司和机构已经使用移动式製图资料进行视觉化和地理空间分析,以限制疾病的传播。仪表板用于显示地理空间资料。其中一些仪表板和应用程式几乎即时接收资料变更。

移动式製图系统的市场趋势

影像服务区隔市场占据主导地位

- 卫星影像和 GIS 系统使安全和执法机构能够识别犯罪热点和其他趋势和模式。准确检测犯罪的空间集中度并及时绘製犯罪地点地图,使执法机构能够精确定位犯罪在空间和时间上的集中度,为减少犯罪工作提供关键资讯。

- 此类图像可以与其他资料(例如人口普查资料或商店、银行和学校的位置)迭加,有助于简化和加快此应用程式中的分析。这使安全管理人员能够了解犯罪的根本原因并制定策略。这些策略包括增加紧急情况下的警察部署和调度。

- 然而,人们对能够提供彩色和全色影像处理服务的先进遥感探测技术的需求日益增长,同时也能够透过资料融合、增强、地理配准、镶嵌以及色彩和灰阶平衡来锐化影像。

- 此外,目前的市场发展针对的是水体监测。例如,非法捕鱼和贩运的挑战使得人们需要发现海洋中的异常现象。 《自然生态与演化》的研究人员表示,在西太平洋和中太平洋等一些地区,非法捕捞可能占到渔业总量的30%。

- 联合国粮食及农业组织 (FAO) 的统计数据强调了未报告和无管制 (IUU) 捕捞的全球影响。据估计,全球每年非法、不通报和不管制渔获量的捕捞量达2,600万吨,价值100亿至230亿美元。 DigitalGlobe 和 Planet 合作开展了计划。该伙伴关係旨在侦查渔业产品的非法转运。

亚太地区发展迅速

- 预计预测期内亚太市场将大幅扩张。政府在卫星图像方面的倡议不断增加以及产品的推出,吸引了国内外公司的投资,推动了该地区市场的成长。

- 2022 年 3 月,澳洲独立无人机测绘公司 Emesent 宣布发布其最新的 Hovermap ST 自主无人机 LiDAR 测绘和测量有效载荷。 Emesent 的 LiDAR 有效载荷使用一种称为同时定位和地图绘製 (SLAM) 的技术,该技术允许无人机同时建立地图并在该地图内确定方向。

- 亚太国家GDP的快速成长带动了公共运输网路等基础设施现代化项目和创新城市计划,增加了对移动式製图技术的需求。

- 中国银川市是该地区最先进的智慧城市之一,几乎所有基础设施都连接到一个系统。例如,银川智慧城市采用的方达平台结合3D地图,在最新地图上识别节点和灯具位置,并整合多种其他应用程式。此外,该地区的市场公司正在提出创新的解决方案。

- 例如,2022 年 6 月,Grab Holdings Limited 宣布推出 GrabMaps。新的企业解决方案使该公司能够挖掘东南亚每年 10 亿美元的地图和定位服务市场潜力。 GrabMaps 最初是为内部使用而推出的,以满足对更多超当地语系化解决方案的需求,从而增强 Grab 的业务。

- 行动装置製造业的快速发展大大降低了扫描器、相机和其他组件的成本,使得小型企业和个人能够更经济地使用定位服务。

移动式製图系统产业概况

随着移动式製图产业主要参与者的不断增加,预计预测期内公司之间的竞争将会加剧。现有企业包括Google公司、Javad GNSS 公司、三菱公司、Trimble 和 Topcon 公司。大公司投入大量资源进行研发,以捍卫其市场地位并推动创新。进入障碍高、企业集中度高、市场渗透率高是影响市场竞争的重要特征。整体而言,竞争对手之间的敌意仍然较高,这主要是由于所研究市场中参与者的强大影响力所致。

2022 年 9 月,营运北美最大的公私称重站绕行网路的连网卡车服务供应商 Drivewyze 与交通分析和连网汽车服务供应商 INRIX 以及宾州收费公路委员会合作,宣布推出即时车载交通警报。宾州与俄亥俄州、新泽西州和北卡罗来纳州一道,在全州范围内提供交通延误、拥堵和事故的音频和影像警报。

2022 年 5 月,Hexagon 子公司徕卡测量系统宣布推出 Leica Pegasus TRK,这是一款现实捕捉移动式製图系统,融合了人工智慧、自主工作流程和远距移动式製图,适用于资产管理、道路建设、关键基础设施、石油和天然气以及电力行业等应用。该系统非常适合为自动驾驶汽车创建高清底图。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 产业影响评估

- 产业价值链分析

第五章市场动态

- 市场驱动因素

- 与任何车辆集成

- 市场限制

- 系统采购和部署高成本

第六章市场区隔

- 按应用

- 影像服务

- 航空移动测绘

- 紧急应变计划

- 网路使用

- 设施管理

- 卫星

- 按最终用户产业

- 政府

- 石油和天然气

- 矿业

- 军队

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章竞争格局

- 公司简介

- Google LLC(Alphabet Inc.)

- Leica Geosystems AG(Hexagon Geosystems)

- Trimble Inc.

- Topcon Corporation

- NovAtel Inc.

- Javad GNSS Inc.

- Teledyne Optech

- Mitsubishi Corporation

- Imajing SAS

- TomTom International BV

- Cyclomedia Technology BV

- INRIX Inc.

第八章投资分析

第九章:未来机会

The Mobile Mapping Systems Market size is estimated at USD 50.98 billion in 2025, and is expected to reach USD 125.95 billion by 2030, at a CAGR of 19.83% during the forecast period (2025-2030).

The rapid acceptance of satellite mapping technology and its seamless integration into smartphones and Internet of Things (IoT)-connected devices are driving the market's growth.

Smart cities rapidly expanded due to increased urbanization and supported government initiatives worldwide. A smart city can only exist with a 3D map. With the support of 3D city modeling, autonomous navigation, traffic, disaster management, digitizing roadway property, and pollution reduction, mobile mapping technology for smart cities aims to improve quality of life by optimizing resources and maintaining sustainability. Smartphone and internet usage played critical roles in data management and access.

Further, mobile navigation geographic information system (GIS) for environmental monitoring is increasingly used in monitoring the environment. Environmental researchers are employing mobile mapping GIS tools to help with storm and hurricane forecasting and monitoring. The NASA-funded research project on ecological monitoring and natural resource management drives revenue growth in the mobile mapping sector.

Mobile mapping systems are used for various applications, including developing indoor maps for pedestrian navigation, high-definition (HD) maps for autonomous vehicles, asset and infrastructure management, ariel surveys, pipeline surveys, hydrographic surveys, dredging, and offshore positioning/drilling operations.

The emergence of on-demand deployment systems is an inflection point in the mobile mapping market, as high levels of flexibility and accuracy at low initial costs are offered (users are charged on a monthly/quarterly basis). Companies offer subscription-based models to counter the need for perpetual user licenses.

The COVID-19 pandemic resulted in a rapid restructuring of the IT industry, with firms shifting to remote labor. During the pandemic, the mobile mapping market grew considerably. Several businesses and agencies used mobile mapping data for visualization and geospatial analytics to restrict the spread of the disease. Dashboards were used to display geospatial data. Some of these dashboards and applications received data changes in near-real time.

Mobile Mapping Systems Market Trends

Imaging Services Segment to Dominate the Market

- Satellite imagery and GIS systems enable security and law enforcement agencies to identify hot spots and other trends and patterns for crime mapping. Accurate detection of spatial concentrations of crime and timely mapping of crime locations help law enforcement identify the concentration of crimes in space and time, thus providing important information for crime reduction efforts.

- Such imagery helps provide efficiency and speed of analysis in this application, allowing analysts to overlay other datasets, such as census demographics and locations of stores, banks, and schools. This helps security department administrators understand the underlying causes of crime and devise strategies. These strategies include allocating police officers and dispatching them to emergencies.

- However, there is an increase in demand for advanced remote sensing techniques, which can provide color and panchromatic image processing services along with the ability to sharpen the image with data fusion, enhancements, georeferencing, mosaicing, and color and grayscale balancing.

- Furthermore, current developments in the market studied aim to monitor water bodies. For instance, the challenge of illegal fishing and trafficking led to the need to find anomalies in the oceans. According to Nature Ecology & Evolution researchers, illegal fishing may constitute up to 30% of the total fisheries in some regions, such as the western and central Pacific oceans.

- The Food and Agriculture Organization of the United Nations (FAO) statistics highlight the global impact of unreported and unregulated (IUU) fishing. Global IUU fishing is estimated to represent up to 26 million metric tons of fish caught annually (equivalent to USD 10 billion-USD 23 billion). DigitalGlobe and Planet collaborated on one such project to identify illicit activities. The partnership aims to spot illegal transshipments of fisheries.

Asia Pacific to Register Fastest Growth

- The market in Asia-Pacific is expected to expand at a significant rate during the forecast period. Increasing government initiatives for satellite imaging are attracting investment from foreign and domestic players, along with product launches, which are driving the market's growth in the region.

- In March 2022, Emesent, an Australia-based independent drone mapping business, announced the release of its latest Hovermap ST autonomous drone LiDAR mapping and surveying payload. Emesent's LiDAR payloads use a technology known as simultaneous localization and mapping (SLAM), in which a drone produces a map while simultaneously localizing itself inside that map.

- The fast GDP expansion in Asia-Pacific countries led to infrastructure modernization programs such as mass public transit networks and innovative city projects, increasing demand for mobile mapping technologies.

- Yinchuan, China, is one of the region's most advanced smart cities, with practically all infrastructure linked into a single system. For instance, the Fonda platform used in Yinchuan smart city combines a 3D map to locate the nodes and lamps in the latest map and integrates various other applications. Moreover, market players in the region are launching innovative solutions.

- For instance, in June 2022, Grab Holdings Limited announced the introduction of GrabMaps. This new enterprise solution enables the firm to capitalize annually on the USD 1.0 billion market potential for mapping and location-based services in Southeast Asia. GrabMaps was first established for internal usage to answer Grab's demand for a more hyperlocal solution to power its operations.

- Rapid mobile device manufacturing has significantly decreased the cost of scanners, cameras, and other components, making location-based services more affordable for SMEs and private individuals.

Mobile Mapping Systems Industry Overview

The growing presence of big players in the mobile mapping industry is expected to intensify competitive rivalry during the forecast period. Incumbents, such as Google Inc., Javad GNSS Inc., Mitsubishi Corporation, Trimble, and Topcon Corporation. Large companies are expending significant resources on R&D operations to protect their position and drive innovation in the market. High barriers to exit, growing levels of firm concentration, and market penetration are some of the significant characteristics influencing the competition in the market. Overall, the intensity of competitive rivalry remains moderately high, mainly driven by the strong presence of players involved in the market studied.

In September 2022, Drivewyze, the connected truck services provider and operator of North America's largest public-private weigh station bypass network, announced real-time, in-cab traffic alerts in collaboration with INRIX, a transportation analytics and connected vehicle services provider, and the Pennsylvania Turnpike Commission. Pennsylvania joins Ohio, New Jersey, and North Carolina in providing in-state alerts that offer audio and visual indicators of upcoming traffic delays, congestion, and incidents.

In May 2022, Leica Geosystems, part of Hexagon, announced the introduction of the reality capture mobile mapping system Leica Pegasus TRK, introducing artificial intelligence, autonomous workflows, and long-range mobile mapping for applications in asset management, road construction, critical infrastructure, oil, gas, and electricity industries. The system is ideal for creating high-definition base maps for autonomous vehicles.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Industry

- 4.4 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Integration with All Kinds of Vehicles

- 5.2 Market Restraints

- 5.2.1 High Cost of System Acquisition and Deployment

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Imaging Services

- 6.1.2 Aerial Mobile Mapping

- 6.1.3 Emergency Response Planning

- 6.1.4 Internet Applications

- 6.1.5 Facility Management

- 6.1.6 Satellite

- 6.2 By End-user Verticals

- 6.2.1 Government

- 6.2.2 Oil and Gas

- 6.2.3 Mining

- 6.2.4 Military

- 6.2.5 Other End-user Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Google LLC (Alphabet Inc.)

- 7.1.2 Leica Geosystems AG (Hexagon Geosystems)

- 7.1.3 Trimble Inc.

- 7.1.4 Topcon Corporation

- 7.1.5 NovAtel Inc.

- 7.1.6 Javad GNSS Inc.

- 7.1.7 Teledyne Optech

- 7.1.8 Mitsubishi Corporation

- 7.1.9 Imajing SAS

- 7.1.10 TomTom International BV

- 7.1.11 Cyclomedia Technology BV

- 7.1.12 INRIX Inc.