|

市场调查报告书

商品编码

1444685

数位物流 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Digital Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

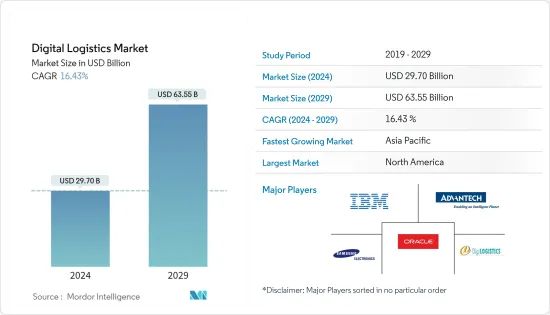

预计2024年数位物流市场规模将达297亿美元,预计2029年将达到635.5亿美元,在预测期间(2024-2029年)CAGR为16.43%。

主要亮点

- 物流业越来越多地采用先进技术,推动了成长。此外,这些数位解决方案正在帮助物流公司降低产生的成本。物流和技术的整合,以及延伸到整个供应链的基于云端的协作解决方案,仓库、运输和最终消费者资讯的紧密整合,以及整个供应链的透明度正在推动所研究市场的成长。

- 数位市场的技术进步和云端应用的不断增加预计将推动对数位物流解决方案的需求。例如去年4月,Locus与loconav宣布战略合作。 loconav 和 Locus 之间的合作将透过供应链流程自动化来促进物流领域的数位转型。

- 随着 COVID-19 的爆发,由于各国政府实施的封锁,许多产业都面临严重的供应链和物流中断。公司正在利用数位物流平台转变其供应链能力,以满足这些重要的交付需求。根据《物流新闻》报道,使用人工智慧和支援数位支付的数位供应链是应对 Covid-19 大流行等紧急情况的解决方案。

- 过去十年,由于网路购物和网路用户的发展,电子商务公司经历了巨大的成长。由于电子商务的发展,需要更快速、更有效率的运输提供者。在线上购物时,客户期望准确的订单、及时的出货和退货程序。企业正在寻找降低订单运输成本和时间的方法。电子商务是可见性、成本、易用性、交付速度和无忧退货背后的驱动力。必须透过自动化配送路线、数位化物流规划和物料移动来创建新的模型和技术来满足这一需求。因此,履行服务变得更快、更多样化,尤其是最后一英里的配送和退款。

数位物流市场趋势

仓库管理系统(WMS)部门预计将获得主要份额。

- 数位市场的技术进步和云端应用的不断增加预计将推动对数位物流解决方案的需求。例如,京东和中石化宣布计划透过其数位供应链模式建立广泛的合作伙伴关係。 2022年3月,中国石化安徽省分公司与京东签署合作协议,双方将在多项供应链服务上展开合作,推动全通路经营。该协议涵盖产品和数位供应链、共享仓库设施和智慧物流。京东将运用技术与供应链服务优势,协助安徽石化提高产能、降低成本。

- 此外,物流领域不断增长的产品创新正在显着提高市场成长率。例如,2022年6月,Semtech推出了LoRa云端定位器服务来测试LoRa Edge的超低功耗资产追踪能力。透过在基于云端的求解器中而不是在设备本身上求解资产的位置,Semtech 的 LoRa Edge 技术大大降低了功耗。因此,设备的电池寿命可达十年甚至更长。 LoRa Edge LR 系列晶片使用 GNSS 和 Wi-Fi 扫描任何室内或室外位置的设备的纬度和经度。无论资产位于何处,与 Semtech 的 LoRa 无线电传输到云端相结合,都可以获得持续覆盖。

- 感测器和物联网分析市场的进步预计将吸引物流供应商投资数位解决方案。物流中的物联网可以简化产品储存并确保高效率的仓库管理。此外,现代技术使仓库运作的检修变得更加简单。 RFID标籤和感测器可以监控库存物品的状态和位置。执行仓库自动化还可以最大限度地减少人为错误,因为流程是根据需要启用和使用的。

亚太地区预计将出现最快的成长率

- 据分析,由于中国、印度等国家采用数位技术,亚太地区在预测期内将以最高的成长率成长。物联网、人工智慧和云端等技术进步进一步促进了市场成长。

- 面对包括新冠肺炎 (COVID-19) 疫情在内的众多障碍,中国的物流业正在采用数位技术来提高效率。 2022年4月,中共中央、国务院联合印发《关于加速建构国内统一市场的意见》。声明表示,中国将优化商贸流通基础设施设计,鼓励线上线下融合发展。

- 这些措施符合中央政府鼓励第三方物流配送数位平台发展、培育一批具有全球影响力的供应链业务的承诺。例如,中国卡车叫车公司满车联盟正在加强利用数位技术来提高受疫情影响地区的物流效率。

- 此外,印度的国家物流政策预计将透过降低物流成本和增强国内商品在全球市场上的竞争力,为该国的经济发展创造一条无缝的道路。由于这些高昂的物流费用,印度国内生产的商品在国际市场上销售已处于劣势。印度製造商一直渴望的转变将透过全面的政策改革来实现,使他们能够在国际市场上为其产品设定有竞争力的价格。统一物流介面平台、数位化系统整合、物流便利化和系统改进组是这个新物流专案的四个主要部分。 「印度製造」、「数位印度」和「Atma-nirbhara」政策在全国范围内的成功执行,为国家物流政策带来了另一个组成部分。

数位物流行业概况

由于有大量满足各种类型组织(例如中小企业到大型企业)的参与者,数位物流市场呈现碎片化。该市场的一些主要参与者包括 IBM 公司、研华公司和三星电子等。市场的一些主要发展是:

- 2023 年 11 月,Suttons International 与 LogChain 开始建立数位化合作关係。此次合作源于 LogChain 最近成功推动了全球首次完全数位化的跨境运输,象征双方致力于增强物流领域的数位透明度和可扩展性。 Suttons International 正在整合其平台,作为其数位转型之旅的关键组成部分。该平台的采用凸显了 Suttons 致力于引领业界数位创新的重要一步。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 竞争激烈程度

- 替代产品的威胁

第 5 章:市场动态

- 市场驱动因素

- 数位科技的出现

- 电子商务产业的成长与多通路分销网络的出现

- 越来越多地采用基于云端的应用程式

- 市场限制

- ICT基础设施缺乏和资料安全问题

- COVID-19 对产业影响的评估

第 6 章:市场细分

- 类型

- 库存管理

- 仓库管理系统(WMS)

- 车队的管理

- 其他类型

- 最终用户垂直领域

- 汽车

- 製药/生命科学

- 零售

- 食品与饮品

- 油和气

- 其他最终用户垂直领域

- 地理

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第 7 章:竞争格局

- 公司简介

- IBM Corporation

- Advantech Corporation

- Oracle Corporation

- Samsung Electronics Co. Ltd

- DigiLogistics Technology Ltd

- Hexaware Technologies Limited

- Tech Mahindra Limited

- JDA Software Pvt Ltd

- UTI Worldwide Inc.(DSV Group)

- SAP SE

- Manhattan Associates Inc.

- HighJump Software Inc.

- Vinculum Group

第 8 章:投资分析

第 9 章:市场的未来

简介目录

Product Code: 52939

The Digital Logistics Market size is estimated at USD 29.70 billion in 2024, and is expected to reach USD 63.55 billion by 2029, growing at a CAGR of 16.43% during the forecast period (2024-2029).

Key Highlights

- Growth is driven owing to the increasing adoption of advanced technologies in the logistics sector. Moreover, these digital solutions are helping logistic companies in reducing incurred costs. Convergence of logistics and technology, along with cloud-based collaborative solutions that extend through the entire supply chain, tight integration of warehouse, transport, and end consumer information, and transparency through the supply chain are driving the growth of the market studied.

- The technological advancement in the digital market and rising cloud adoption are expected to fuel the demand for digital logistic solutions. For instance, in April last year, Locus and loconav announced a strategic cooperation. This partnership between loconav and Locus will promote digital transformation in the logistics sector by automating supply chain processes.

- With the outbreak of COVID-19, many industries have faced significant supply chain and logistic disruption owing to the lockdown imposed by various governments. Companies are transforming their supply chain capabilities with digital logistics platforms to meet those essential deliveries. According to Logistics News, digital supply chains using artificial intelligence and enabling digital payments are the solution to emergencies such as the Covid-19 pandemic.

- Over the past ten years, the e-commerce company has experienced tremendous growth due to the development of online shopping and Internet users. More rapid and efficient transportation providers are required due to the growth of e-commerce. When shopping online, customers expect accurate orders, prompt shipment, and return procedures. Businesses are looking for ways to reduce order shipping costs and timeframes. E-commerce is the driving force behind visibility, cost, ease of use, delivery speed, and hassle-free returns. New models and technologies must be created to accommodate this need by automating distribution routes, digitalizing logistics planning, and material movement. As a result, fulfillment services have become quicker and more varied, especially for last-mile delivery and refunds.

Digital Logistics Market Trends

Warehouse Management System (WMS) segment is expected to acquire major share.

- The technological advancement in the digital market and rising cloud adoption are expected to fuel the demand for digital logistic solutions. For instance, JD and Sinopec announced a plan to build a broad partnership with their digital supply chain model. In March 2022, Sinopec's Anhui province branch and JD.com signed a partnership agreement under which they will collaborate on a number of supply chain services and advance omnichannel operations. The agreement encompasses product and digital supply chains, sharing warehouse facilities, and smart logistics. JD will use its technology and supply chain services advantages to assist Sinopec Anhui in boosting productivity and cutting costs.

- Further, the growing product innovations in the logistics sector are significantly boosting the market growth rate. For instance, in June 2022, Semtech introduced the LoRa Cloud Locator Service to test the LoRa Edge's ultra-low power asset tracking capabilities. By solving the asset's position in a Cloud-based solver rather than on the device itself, Semtech'sLoRa Edge technology considerably lowers power usage. As a result, the device's battery life can last up to or even longer than ten years. The LoRa Edge LR-series chips use GNSS and Wi-Fi to scan for a device's latitude and longitude in any interior or outdoor location. Regardless of where assets are located, continuous coverage is obtained when combined with Semtech'sLoRa radio transmission to the Cloud.

- Advancements in the sensors and IoT analytics market are expected to attract logistics vendors, to invest in digital solutions. IoT in logistics can simplify storing products and ensure efficient warehouse management. Additionally, modern technology has made it much simpler to overhaul warehouse operations. RFID tags and sensors can monitor the status and location of the inventory items. Executing warehouse automation can also minimize human errors because the processes are enabled and used as needed.

Asia Pacific is Expected to Register the Fastest Growth Rate

- Asia-pacific is analyzed to grow at the highest growth rate during the forecast period owing to the adoption of digital technologies in countries such as China, India, and so on. Technological advancements such as IoT, AI, and Cloud further contribute to market growth.

- China's logistics sector is embracing digital technologies to increase efficiency in the face of numerous obstacles, including the COVID-19 pandemic. A directive on accelerating the creation of a unified domestic market was jointly published in April 2022 by the Communist Party of China Central Committee and the State Council. It stated that China would optimize the design of the infrastructure for commerce and trade circulation and encourage the fusion of online and offline development.

- The initiatives are in accordance with the central government's commitment to encourage the development of digital platforms for third-party logistics delivery and to foster a number of supply chain businesses with a global reach. For instance, Full Truck Alliance Co Ltd, a Chinese truck-hailing business, is boosting efforts to use digital technology to improve logistical effectiveness in pandemic-affected areas.

- Further, India's national logistics policy is anticipated to create a seamless course for economic development in the country by lowering logistic costs and enhancing the competitiveness of domestic goods on the global market. Due to these high logistical expenses, domestic commodities produced in India that are sold on the international market are already at a disadvantage. The shift that Indian manufacturers have been yearning for will be brought about by a comprehensive policy overhaul, allowing them to set competitive prices for their goods on the international market. Unified Logistics Interface Platform, Integration of Digital System, Ease of Logistics, and System Improvement Group are the four main parts of this new logistical project. The successful policy execution of Make in India, Digital India, and the "Atma-nirbhara drive" throughout the nation gains another component from the national logistics policy.

Digital Logistics Industry Overview

The Digital Logistics Market is fragmented due to the presence of a large number of players which cater to various types of organizations, such as SMEs to Large Enterprises. Some key players in the market are IBM Corporation, Advantech Corporation, and Samsung Electronics Co. Ltd., among others. Some key developments in the market are:

- November 2023, Suttons International and LogChain have started a digitalization partnership. This collaboration, coming from LogChain's recent success in facilitating the world's first fully digitalized cross-border shipment, symbolizes a mutual commitment to bolstering digital transparency and scalability in the logistics sector. Suttons International is integrating its platform as a pivotal component in its digital transformation journey. The platform's adoption underscores a significant step in Suttons' commitment to spearheading digital innovation within the industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Emergence Of Digital Technology

- 5.1.2 Growth In E-Commerce Industry And Emergence Of Multichannel Distribution Networks

- 5.1.3 Growing Adoption Of Cloud Based Applications

- 5.2 Market Restraints

- 5.2.1 Lack of ICT Infrastructure and Data Security Concerns

- 5.3 Assessment of Impact of COVID-19 on the Industry

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 Inventory Management

- 6.1.2 Warehouse Management System (WMS)

- 6.1.3 Fleet Management

- 6.1.4 Other Types

- 6.2 End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Pharmaceutical / Life Sciences

- 6.2.3 Retail

- 6.2.4 Food and Beverage

- 6.2.5 Oil and Gas

- 6.2.6 Other End-user Verticals

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Advantech Corporation

- 7.1.3 Oracle Corporation

- 7.1.4 Samsung Electronics Co. Ltd

- 7.1.5 DigiLogistics Technology Ltd

- 7.1.6 Hexaware Technologies Limited

- 7.1.7 Tech Mahindra Limited

- 7.1.8 JDA Software Pvt Ltd

- 7.1.9 UTI Worldwide Inc.(DSV Group)

- 7.1.10 SAP SE

- 7.1.11 Manhattan Associates Inc.

- 7.1.12 HighJump Software Inc.

- 7.1.13 Vinculum Group

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

02-2729-4219

+886-2-2729-4219

数位物流市场:按组成部分、组织规模、部署类型、产业 - 2025-2030 年全球预测

数位物流市场:按组成部分、组织规模、部署类型、产业 - 2025-2030 年全球预测 全球数位物流市场规模、份额和趋势分析报告(按部署模式、解决方案、应用、最终用户、区域展望和预测,2024-2031)

全球数位物流市场规模、份额和趋势分析报告(按部署模式、解决方案、应用、最终用户、区域展望和预测,2024-2031) 数位物流市场规模、份额、趋势分析报告:按组件、按部署、按应用、按最终用途、按地区、细分市场预测,2024-2030 年

数位物流市场规模、份额、趋势分析报告:按组件、按部署、按应用、按最终用途、按地区、细分市场预测,2024-2030 年 物流市场网路安全、机会、成长动力、产业趋势分析与预测,2024-2032

物流市场网路安全、机会、成长动力、产业趋势分析与预测,2024-2032 数位物流市场规模 - 按组成部分、按功能、按组织规模、按部署模式、按垂直行业和预测,2024 年至 2032 年

数位物流市场规模 - 按组成部分、按功能、按组织规模、按部署模式、按垂直行业和预测,2024 年至 2032 年 2023-2030 年全球数位物流市场规模研究与预测(依解决方案、应用、部署模式、最终用户和区域分析)

2023-2030 年全球数位物流市场规模研究与预测(依解决方案、应用、部署模式、最终用户和区域分析) 数位物流市场 - 全球产业规模、份额、趋势、机会和预测,按部署、系统、地区、竞争细分,2019-2029F

数位物流市场 - 全球产业规模、份额、趋势、机会和预测,按部署、系统、地区、竞争细分,2019-2029F 2024 年数位物流全球市场报告

2024 年数位物流全球市场报告 数位物流市场报告:2030 年趋势、预测与竞争分析

数位物流市场报告:2030 年趋势、预测与竞争分析 数位物流市场:按功能、服务和行业划分 - 2023-2030 年全球预测

数位物流市场:按功能、服务和行业划分 - 2023-2030 年全球预测