|

市场调查报告书

商品编码

1444701

聚烯烃 (PO) - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029 年)Polyolefin (PO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

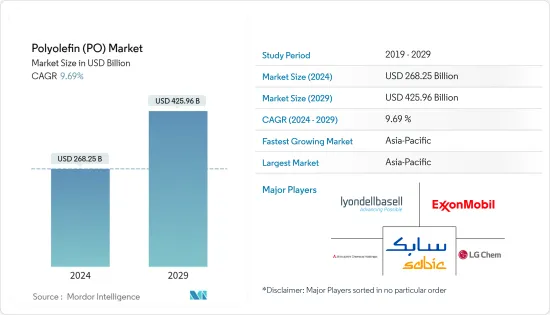

2024年聚烯烃市场规模预计为2,682.5亿美元,预计到2029年将达到4,259.6亿美元,在预测期(2024-2029年)CAGR为9.69%。

COVID-19的传播损害了市场,因为它导致许多最终用户行业关闭。在大流行期间,中国由于包装等行业的强大而成为聚烯烃的主要消费国之一,从而严重阻碍了聚烯烃市场、玩具製造、建筑和汽车。然而,随着2021年各行业恢復製造活动,研究的市场也可能復苏。

主要亮点

- 聚烯烃因其先进的性能而被用于电子、汽车和其他行业。预计这将有助于市场在短期内成长。

- 然而,各国政府对塑胶实施的日常严格的环境法规可能会限制市场。

- 对绿色聚烯烃的日益关注可能会在未来几年创造新的机会。

- 亚太地区主导全球市场,最大的消费来自印度、中国等。

聚烯烃市场趋势

薄膜和片材的需求不断增加

- 薄膜和片材可用于运输、包装、农业、建筑和建筑业等。

- 农业部门正在推动市场的扩张,对温室用聚烯烃薄膜和片材、覆盖物和青贮饲料拉伸膜的需求。青贮饲料片和窗膜以及医疗领域也有这种需求。

- 聚烯烃农业薄膜还可以保护蔬菜免受霜冻、风雨和害虫的影响,同时加速水果、蔬菜和花卉的成熟,使农民能够在一年内种植多种作物。聚烯烃薄膜也有助于减少蒸发,从而节省用水。

- 另一方面,聚烯烃片材用于建筑领域。用作蒸气缓凝剂的聚乙烯板安装在板下方。这些片材可以延迟较长时间而不会降解。因此,建筑业对聚烯烃的需求不断扩大。

- 亚太地区建筑业预计将成为全球规模最大、成长最快的行业,全球建筑支出的 45% 份额来自该地区。未来几年,这可能会让更多的人想要薄膜和板材。

- 2022财年,印度聚烯烃总产能超过1.2万吨,其中大部分聚烯烃由Reliance Industries Limited生产,约占印度聚烯烃总产能的47%。

- 由于这些因素,随着薄膜和片材需求的增加,聚烯烃市场在未来几年可能会成长。

亚太地区将主导市场

- 由于中国是全球聚烯烃的主要消费国,亚太地区是聚烯烃市场的主导地区。这一增长是由电子商务的成长推动的,因为快递业务的强劲导致对塑胶包装的需求激增。该国的製造业是其经济的主要贡献者之一。

- 中国政府宣布了未来10年的大型建设计划,其中包括将2.5亿人迁移到新特大城市的计划。这是建筑化学品在施工过程中以多种方式使用以改善建筑性能的绝佳机会。

- 智慧型手机、OLED电视、平板电脑和其他消费性电子产品等电子产品正在市场上成长最快。随着中产阶级口袋里的钱越来越多,对电子产品的需求将会增加,这将推动该国对聚烯烃的需求。

- 在中国,到 2023 年底,电子产品市场预计将达到 3,850 亿美元以上。

- 所有上述因素都可能增加预测期内对聚烯烃的需求。

聚烯烃产业概况

聚烯烃市场本质上是整合的。一些主要参与者(排名不分先后)包括 LyondellBasell Industries Holdings BV、埃克森美孚公司、SABIC、LG Chem 和三菱化学控股公司等。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 司机

- 偏好从刚性包装转向软包装

- 对低成本室内家具的需求不断增长

- 限制

- 日益严格的环境法规

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第 5 章:市场区隔(市场价值规模)

- 材料种类

- 聚乙烯(PE)

- 聚丙烯(PP)

- 聚烯烃弹性体 (POE)

- 乙烯醋酸乙烯酯 (EVA)

- 应用

- 薄膜和片材

- 射出成型

- 吹塑成型

- 挤压涂布

- 纤维和拉菲草

- 地理

- 亚太

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太

第 6 章:竞争格局

- 併购、合资、合作与协议

- 市占率/排名分析

- 领先企业采取的策略

- 公司简介

- Arkema Group

- BASF SE

- Braskem

- Chevron Phillips Chemical Company

- China National Petroleum Corporation

- China Petrochemical Corporation

- Daelim

- Dow

- ExxonMobil Corporation

- Formosa Plastics Corporation

- Japan Polypropylene Corporation

- LG Chem Ltd.

- LyondellBasell Industries Holdings BV

- Mitsubishi Chemical Holdings Corporation

- Mitsui Chemicals Incorporated

- Nova Chemicals Corporation

- PetroChina Company Limited

- Reliance Industries Limited

- SABIC (Saudi Basic Industries Corporation)

- Sasol Ltd.

- Tosoh Corporation

第 7 章:市场机会与未来趋势

- 越来越关注绿色聚烯烃

The Polyolefin Market size is estimated at USD 268.25 billion in 2024, and is expected to reach USD 425.96 billion by 2029, growing at a CAGR of 9.69% during the forecast period (2024-2029).

The spread of COVID-19 hurt the market because it caused many end-user industries to shut down.During the pandemic, China hampered the polyolefins market intensively, as it is one of the major consumers of polyolefins owing to its strong industries such as packaging, toy manufacturing, construction, and automotive. However, as the industries resumed their manufacturing activities in 2021, the studied market may also recover.

Key Highlights

- Polyolefin is used in electronics, cars, and other industries because of its advanced properties. This is expected to help the market grow in the short term.

- However, growing environmental regulations on plastic imposed by various governments may constrain the market.

- The growing focus on green polyolefin is likely to create new opportunities in the coming years.

- Asia-Pacific dominated the market worldwide, with the largest consumption coming from India, China, etc.

Polyolefins Market Trends

Increasing Demand from Films and Sheets

- Films and sheets can be used in the transportation, packaging, agriculture, building and construction, and building industries, among others.

- The agricultural sector is driving the market's expansion, with demand for polyolefin films and sheets for greenhouses, mulch, and silage stretch films. The demand is also seen in silage sheets and window films, as well as in the medical sector.

- Polyolefin-based agricultural films also protect vegetables from frost, wind, rain, and pests while speeding up the ripening of fruits, vegetables, and flowers, allowing farmers to grow several crops in a year. Polyolefin films also help reduce evaporation, thus saving water.

- On the other hand, polyolefin sheets are used in the building sector. The polyethylene sheeting, which works as a vapor retarder, is installed beneath the slab. These sheets can retard for a longer time without degrading. As a result, the demand for polyolefin from the construction industry is expanding.

- The Asia-Pacific construction industry is projected to become the world's largest and fastest-growing industry, with a 45% share of global construction spending coming from the region. In the coming years, this is likely to make more people want films and sheets.

- In fiscal year 2022, India had a total polyolefins production capacity of over 12 thousand kilotons.The most polyolefins were made by Reliance Industries Limited, which made up almost 47% of India's total polyolefins production capacity.

- Because of these things, the polyolefin market is likely to grow in the coming years as the demand for films and sheets rises.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is the dominant region in the polyolefins market, owing to China being the major consumer of polyolefins worldwide. The growth is driven by increasing e-commerce, as the strong courier business led to a spike in demand for plastic packaging. The country's manufacturing sector is one of the major contributors to its economy.

- The Chinese government announced big building plans for the next 10 years, including plans to move 250 million people to new megacities. This is a big chance for construction chemicals to be used in a variety of ways to improve building properties during construction.

- Electronic items, such as smartphones, OLED TVs, tablets, and other consumer electronics, are recording the fastest growth in the market. With more money in the pockets of the middle class, there will be more demand for electronics, which will drive the demand for polyolefins in the country.

- In China, the electronics segment is projected to reach over USD 385 billion by the end of 2023.

- All the above-mentioned factors will likely increase the demand for polyolefins over the forecast period.

Polyolefins Industry Overview

The polyolefin market is consolidated by nature. Some of the major players (not in any particular order) include LyondellBasell Industries Holdings BV, ExxonMobil Corporation, SABIC, LG Chem, and Mitsubishi Chemical Holdings Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Shift in Preferences from Rigid Packaging to Flexible Packaging

- 4.1.2 Growing Demand for Low-Cost Interior Furnishings

- 4.2 Restraints

- 4.2.1 Growing Environmental Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material Type

- 5.1.1 Polyethylene (PE)

- 5.1.2 Polypropylene (PP)

- 5.1.3 Polyolefin Elastomer (POE)

- 5.1.4 Ethylene Vinyl Acetate (EVA)

- 5.2 Application

- 5.2.1 Films and Sheets

- 5.2.2 Injection Molding

- 5.2.3 Blow Molding

- 5.2.4 Extrusion Coating

- 5.2.5 Fibers and Raffia

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema Group

- 6.4.2 BASF SE

- 6.4.3 Braskem

- 6.4.4 Chevron Phillips Chemical Company

- 6.4.5 China National Petroleum Corporation

- 6.4.6 China Petrochemical Corporation

- 6.4.7 Daelim

- 6.4.8 Dow

- 6.4.9 ExxonMobil Corporation

- 6.4.10 Formosa Plastics Corporation

- 6.4.11 Japan Polypropylene Corporation

- 6.4.12 LG Chem Ltd.

- 6.4.13 LyondellBasell Industries Holdings BV

- 6.4.14 Mitsubishi Chemical Holdings Corporation

- 6.4.15 Mitsui Chemicals Incorporated

- 6.4.16 Nova Chemicals Corporation

- 6.4.17 PetroChina Company Limited

- 6.4.18 Reliance Industries Limited

- 6.4.19 SABIC (Saudi Basic Industries Corporation)

- 6.4.20 Sasol Ltd.

- 6.4.21 Tosoh Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Focus on Green Polyolefin

聚烯市场:按产品、应用和最终用户划分 - 2025-2030 年全球预测

聚烯市场:按产品、应用和最终用户划分 - 2025-2030 年全球预测 2024-2028年全球聚烯市场

2024-2028年全球聚烯市场 全球聚烯烃塑性体(POP)市场(2016-2036)

全球聚烯烃塑性体(POP)市场(2016-2036) 烯烃嵌段共聚物(OBC)的全球市场(2016-2036)

烯烃嵌段共聚物(OBC)的全球市场(2016-2036) 北美聚烯和工程塑胶化合物市场规模、份额和趋势分析报告:按产品、应用、国家和细分市场预测,2024-2030 年

北美聚烯和工程塑胶化合物市场规模、份额和趋势分析报告:按产品、应用、国家和细分市场预测,2024-2030 年 聚烯市场,占有率,规模,趋势,产业分析报告:各原料,各用途,各地区,各市场区隔&预测,2024年~2032年

聚烯市场,占有率,规模,趋势,产业分析报告:各原料,各用途,各地区,各市场区隔&预测,2024年~2032年 全球聚烯烃市场

全球聚烯烃市场![聚烯纤维市场报告:趋势、预测、竞争分析 [2024-2030]](/sample/img/cover/42/1448499.png) 聚烯纤维市场报告:趋势、预测、竞争分析 [2024-2030]

聚烯纤维市场报告:趋势、预测、竞争分析 [2024-2030] 聚烯市场-2024年至2029年预测

聚烯市场-2024年至2029年预测 氯化聚烯市场报告:2030 年趋势、预测与竞争分析

氯化聚烯市场报告:2030 年趋势、预测与竞争分析