|

市场调查报告书

商品编码

1444786

地聚合物 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Geopolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

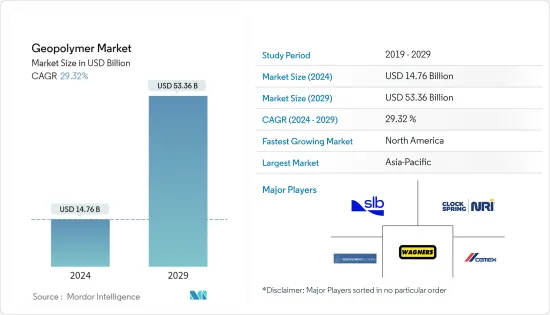

2024年,地聚合物市场规模预计为147.6亿美元,预计到2029年将达到533.6亿美元,在预测期内(2024-2029年)CAGR为29.32%。

COVID-19的引入对地质聚合物业务产生了负面影响。建筑业是受灾最严重的行业之一,由于工人短缺以及政府为在 2020 年之前防止疾病传播而实施的严格标准,正在进行的项目被叫停,所有新项目都被推迟。然而,市场预计由于2021 年建筑活动增加,预计将稳定成长。

主要亮点

- 短期内,水泥产业的环境法规和排放压力以及修復和修復市场的更高需求是推动所研究市场成长的主要因素。

- 但缺乏统一的规则和标准是预计在预测期内减缓目标产业成长的主要原因之一。

- 儘管如此,消费者越来越意识到地质聚合物产品的好处,这可能会在不久的将来为全球市场带来成长机会。

- 随着该地区建筑活动的增加,亚太地区主导了全球市场。

地聚合物市场趋势

打造细分市场以主导市场

- 地质聚合物在建筑施工中的使用具有至关重要的作用。由于世界范围内建筑活动的迅速增长和人口的过度增长,大量的温室气体被排放到大气中,造成了巨大的环境影响。随着水泥製造过程中或以其他方式排放的温室气体对环境的影响越来越大,建筑材料的整体建设为地聚合物在建筑施工中的开发和使用创造了空间。

- 值得注意的是,建筑业在过去几年经历了快速成长。根据世界银行的数据,2020年全球建筑业价值达到22.36兆美元,较2021年的27.18兆美元成长。

- 建筑业绿色技术的发展可以追溯到多年前。近年来,世界各地环保意识的增强,除了建筑材料的技术性能外,还导致人们对建筑材料的环境影响进行了积极的评估。

- 多种类型的地聚合物材料,例如地聚合物混凝土、地聚合物水泥、黏合剂、地聚合物砖、面板等,由于其在减少温室气体排放和节能方面的多功能特性而被用于建筑施工。

- 地质聚合物最近在该建筑中的应用之一被认为是2021 年1 月在伦敦建造的第一根桩,使用领先的地质聚合物製造商之一瓦格纳的地球友好混凝土(EFC),与两家领先的英国公司Keltbray 合作集团和资本混凝土。

- 此外,在澳大利亚,由 Hassell 与 Bligh Tanner 和 Wagners 共同设计的昆士兰大学全球变迁研究所 (GCI) 是世界上第一座使用地质聚合物混凝土进行结构的建筑。

- 此外,随着地聚合物在建筑施工中的使用不断增加,公众和政府对使用地聚合物混凝土优势的认识不断增强,这与图文巴威尔坎普机场(Toowoomba Wellcamp Airport)主要使用地聚合物混凝土有关;大约使用了 23,000 立方米。

- 总体而言,地质聚合物在建筑施工中的使用一直在增长。这是因为地质聚合物有很多好处。

中国将主导亚太市场

- 在亚太地区,中国凭藉着不断增长的建筑活动和不断增长的建筑材料需求,主导了全球市场份额。

- 为加速经济成长,挽回疫情期间的损失,中国财政部和国家发展部计划于 2022 年第三季投资 5,000 亿元人民币(718.6 亿美元)设立国家基础设施基金,旨在促进基础设施支出。

- 此外,中国正在扩建 30 个机场,以改善与中国第四大国际枢纽成都天府国际机场的连结性。

- 据民航局称,中国「十三五」规划中包括到2020年扩大低收入地区航空运输服务扶贫力度。未来五年至2025年,中国将投资1.43兆美元,用于重大建设项目,其中包括超大型航空运输服务。- 高压能源专案、巨量资料中心、高铁、城际轨道站、5G基地台、电动车充电站等。

- 据国家发改委透露,上海计划未来三年投资387亿美元,而广州已签约新基建项目16个,投资金额80.9亿美元。

- 此外,该国的目标是在未来五年到2025年建造500万个5G基地台,比目前的5G基地台数量增加25倍。中国这些大型基础设施开发案正在推动中国对地聚合物的需求。

- 国家也正在抓紧2020年启动的公路项目,包括投资16.1亿美元建设广南纳萨至夏侯星街等城市之间的高速公路,投资18.6亿美元建设澄江至华宁,以及投资18.6亿美元建设奎北至华宁等城市的高速公路。云南省燕山项目,投资15.4亿美元,预计2023年完工。

- 此外,投资86.8亿美元的贵州省连接纳雍至青龙和柳州至安龙的两个新高速公路项目的建设预计将对中国地聚合物市场产生积极影响。

- 从而,增加该国的住宅建设,进而对该国的地聚合物市场产生正面影响。

地聚合物产业概况

地质聚合物市场本质上高度分散。地质聚合物市场的主要参与者包括 Wagners、Geopolymer Solutons LLC、SLB、ClockSpring|NRI 和 CEMEX SAB de CV 等(排名不分先后)。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 司机

- 水泥产业的环境法规与排放压力

- 维修和復健市场的更高需求

- 限制

- 缺乏统一的标准和法规

- COVID-19 疫情造成的不利条件

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第 5 章:市场区隔(市场价值规模)

- 产品类别

- 水泥、混凝土和预製板

- 灌浆和黏合剂

- 其他产品类型

- 应用

- 大楼

- 道路和人行道

- 跑道

- 管道和混凝土修復

- 桥

- 隧道衬砌

- 铁路卧舖

- 涂层应用

- 防火

- 核废料和其他有毒废料固定化

- 特定模具产品

- 地理

- 亚太

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 世界其他地区

- 南美洲

- 中东和非洲

- 亚太

第 6 章:竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 领先企业采取的策略

- 公司简介

- Banah UK Ltd

- CEMEX SAB de CV

- Ceskych Lupkovych Zavodech AS

- ClockSpring|NRI

- Geopolymer Solutions LLC

- IPR

- Murray & Roberts

- PCI Augsburg GMBH

- Rocla Pty Limited

- Schlumberger Limited

- Wagners

- Zeobond Pty Ltd

第 7 章:市场机会与未来趋势

- 消费者对地质聚合物产品优点的认识不断增强

The Geopolymer Market size is estimated at USD 14.76 billion in 2024, and is expected to reach USD 53.36 billion by 2029, growing at a CAGR of 29.32% during the forecast period (2024-2029).

The introduction of COVID-19 had a negative influence on the geopolymer business. The construction industry was one of the hardest hit, with ongoing projects halted and all new projects postponed due to a shortage of workers and government-imposed rigorous standards aimed at preventing the spread of the disease by the year 2020. However, the market is projected to grow steadily, owing to increased building and construction activities in 2021.

Key Highlights

- Over the short term, environmental regulations and emission strain on the cement industry and higher demand from the repair and rehabilitation market are major factors driving the growth of the market studied.

- But the lack of uniform rules and standards is one of the main things that is expected to slow the growth of the target industry during the forecast period.

- Still, consumers are becoming more aware of the benefits of geopolymer products, which is likely to lead to growth opportunities for the global market in the near future.

- With rising construction activity in the region, Asia-Pacific dominated the global market.

Geopolymer Market Trends

Building Segment to Dominate the Market

- The use of geopolymers in building construction has a vital role. Due to the rapidly growing construction activities and the overgrowing population across the world, large amounts of greenhouse gases are being emitted into the atmosphere, causing a huge environmental impact. With the increasing impact of greenhouse gases on the environment emitted either during cement manufacturing or in other alternate ways, the overall construction of building materials has created scope for the development and use of geopolymers in building construction.

- It has been noted that the building and construction sector has experienced rapid growth in the past few years. According to the World Bank, the value of the global construction industry reached USD 22.36 trillion in 2020 and registered growth compared to USD 27.18 trillion in 2021.

- The development of green technology in the construction industry dates back years. The increase in environmental awareness in recent years around the world has led to a positive assessment of the environmental impact of building materials in addition to their technical properties.

- Several types of geopolymer materials, such as geopolymer concrete, geopolymer cement, binders, geopolymer bricks, panels, and many others, are being used during building construction, owing to their versatile properties in reducing greenhouse emissions as well as energy savings.

- One of the recent applications of geopolymers in the building is cited as the first ever pile constructed in London, dated January 2021, using one of the leading geopolymer manufacturers, Wagner's Earth Friendly Concrete (EFC), by working with two leading UK firms, Keltbray Group and Capital Concrete.

- Additionally, in Australia, the University of Queensland's Global Change Institute (GCI), designed by Hassell in conjunction with Bligh Tanner and Wagners, is the world's first building to use geopolymer concrete for structural purposes.

- Moreover, with such growing usage of geopolymers in building construction, awareness has been growing among the public and governments over the advantages of using geopolymer concrete, and this can be related to Toowoomba Wellcamp Airport, in which mostly geopolymer concrete was used; approximately 23.000 m3 were used.

- Overall, the use of geopolymers in building construction has been growing. This is because geopolymers have a lot of benefits.

China to Dominate the Asia-Pacific Market

- In the Asia-Pacific region, China dominated the global market share with growing construction activities and increasing demand for construction materials.

- To fasten up its economic growth to recover the losses during the pandemic period, China's Ministry of Finance and National Development has planned to invest CNY 500 billion (USD 71.86 billion) in building up a state infrastructure fund in the third quarter of 2022, aimed at promoting infrastructure spending.

- Additionally, the country is working on the expansion of 30 airports to improve the connectivity to the country's fourth largest international hub Chengdu Tianfu International Airport.

- According to CAAC, China's 13th five-year plan include the expansion of air transportation services in low-income areas for poverty alleviation in 2020. The country is investing USD 1.43 trillion in the next five year till 2025, in major construction projects which includes ultra-high voltage energy projects, big data centers, high-speed railway, and intercity tracks & stations, 5G base stations, electric vehicle charging station, and various others.

- According to National Development and Reform Commission (NDRC), Shanghai plan includes the investment of USD 38.7 billion in the next three years, whereas Guangzhou has signed 16 new infrastructure projects with and investment of USD 8.09 billion.

- Additionally, the country is targeting to build five million 5G base stations in the next five years till 2025, a growth of 25 times from the current number of 5G base stations. These massive infrastructure development projects in the country are propelling the demand for geopolymers in China.

- The country is also working on road projects initiated in 2020 which include the construction of an expressway between the cities such as Guangnan Nasa and Xiahou Xingjie with an investment of USD 1.61 billion, Chengjiang and Huaning with an investment of USD 1.86 billion, and Quibei and Yanshan in Yunan province with an investment of USD 1.54 billion which are estimated to get completed in 2023.

- Additionally, the construction of two new highway projects connecting Nayong with Qinglong, andLiuzzii with Anlong in Guizhou Province with and investment of USD 8.68 billion is expected to positively impact the geopolymers market in China.

- Thereby, increasing the residential construction in the country which in turn will have a positive effect on the geopolymers market in the country.

Geopolymer Industry Overview

The geopolymer market is highly fragmented in nature. The major players in the geopolymers market are Wagners, Geopolymer Solutons LLC, SLB, ClockSpring|NRI, and CEMEX S.A.B. de C.V., among others (not in particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Environmental Regulations and Emission Strain on the Cement Industry

- 4.1.2 Higher Demand from the Repair and Rehabilitation Market

- 4.2 Restraints

- 4.2.1 Lack of Uniform Standards and Regulations

- 4.2.2 Unfavorable Conditions Arising Due to the COVID-19 Outbreak

- 4.3 Industry Value-chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Cement, Concrete, and Precast Panel

- 5.1.2 Grout and Binder

- 5.1.3 Other Product Types

- 5.2 Application

- 5.2.1 Building

- 5.2.2 Road and Pavement

- 5.2.3 Runway

- 5.2.4 Pipe and Concrete Repair

- 5.2.5 Bridge

- 5.2.6 Tunnel Lining

- 5.2.7 Railroad Sleeper

- 5.2.8 Coating Application

- 5.2.9 Fireproofing

- 5.2.10 Nuclear and Other Toxic Waste Immobilization

- 5.2.11 Specific Mold Products

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Banah UK Ltd

- 6.4.2 CEMEX SAB de CV

- 6.4.3 Ceskych Lupkovych Zavodech AS

- 6.4.4 ClockSpring|NRI

- 6.4.5 Geopolymer Solutions LLC

- 6.4.6 IPR

- 6.4.7 Murray & Roberts

- 6.4.8 PCI Augsburg GMBH

- 6.4.9 Rocla Pty Limited

- 6.4.10 Schlumberger Limited

- 6.4.11 Wagners

- 6.4.12 Zeobond Pty Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Consumer Awareness Regarding Benefits of Geopolymer Products

按应用(水泥和混凝土、熔炉和反应器绝缘体、复合材料、装饰工艺品)、最终用途行业(建筑、基础设施、工业、艺术和装饰等)和地区分類的地聚合物市场报告 2025-2033

按应用(水泥和混凝土、熔炉和反应器绝缘体、复合材料、装饰工艺品)、最终用途行业(建筑、基础设施、工业、艺术和装饰等)和地区分類的地聚合物市场报告 2025-2033 偏高岭土基地无机聚合物市场报告:2030 年趋势、预测与竞争分析

偏高岭土基地无机聚合物市场报告:2030 年趋势、预测与竞争分析 无机聚合物黏合剂系统市场报告:2030 年趋势、预测与竞争分析

无机聚合物黏合剂系统市场报告:2030 年趋势、预测与竞争分析 飞灰无机聚合物市场报告:2030 年趋势、预测与竞争分析

飞灰无机聚合物市场报告:2030 年趋势、预测与竞争分析 无机聚合物材料市场:按产品类型、原料、加工、应用和最终用户划分 - 全球预测 2025-2030

无机聚合物材料市场:按产品类型、原料、加工、应用和最终用户划分 - 全球预测 2025-2030 全球地聚合物市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球地聚合物市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 2024 年无机聚合物全球市场报告

2024 年无机聚合物全球市场报告 2024-2032 年按应用(水泥和混凝土、熔炉和反应器绝缘体、复合材料、装饰製品)、最终用途行业(建筑、基础设施、工业、艺术和装饰等)和地区分類的地聚合物市场报告

2024-2032 年按应用(水泥和混凝土、熔炉和反应器绝缘体、复合材料、装饰製品)、最终用途行业(建筑、基础设施、工业、艺术和装饰等)和地区分類的地聚合物市场报告 全球地质聚合物市场,2024-2028

全球地质聚合物市场,2024-2028 全球地质聚合物市场 - 2023-2030

全球地质聚合物市场 - 2023-2030