|

市场调查报告书

商品编码

1444840

粮食储存筒仓 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Grain Storage Silos - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

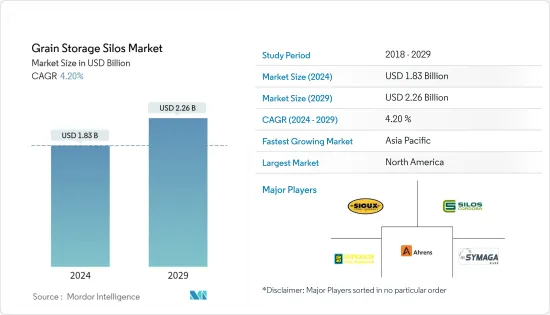

粮食仓储筒仓市场规模预计到 2024 年为 18.3 亿美元,预计到 2029 年将达到 22.6 亿美元,在预测期内(2024-2029 年)CAGR为 4.20%。

主要亮点

- 由于人口的增加,世界各地的农业生产力正在提高。儘管生产力不断扩大,但由于粮食损失,自给自足仍是关键问题之一。粮食损失的发生是由于缺乏适当的储存设施,导致价格下跌和农民利润减少。对适当的收穫后储存设施的需求有助于全球粮仓市场的发展。因此,该市场的关键驱动因素包括粮食价格波动和大容量储存需求上升。

- 同时,母公司不断增加的投资和技术发展也在推动市场。例如,在印度,2021 年,印度最大的私人农业收穫后管理公司国家商品管理服务有限公司 (NCML) 在哈里亚纳邦推出了四个公共仓储筒仓设施。由于粮食库存逐年增加,需要更大的储存能力,这推动了全球市场的发展。

- 此外,粮食储存对于发展中国家和已开发国家都非常重要,因为它们储存大量粮食以供将来使用和出口。因此,害虫、囓齿动物和鸟类对谷物的腐败造成了农作物的重大损失。例如,北美的粮仓市场庞大。该地区的农民很少在销售年度结束时持有大量库存。小麦、大麦、玉米、大豆和其他谷物的库存几乎全部来自非农场。此外,该地区的公司还在扩大筒仓的储存容量,以储存大量谷物。因此,这些因素有助于预测期内的市场成长。

粮食储存筒仓市场趋势

大容量储存需求不断成长

美国、俄罗斯、印度、巴西等世界主要粮食生产国对粮食仓储的需求不断增长,推动了研究期间粮食仓储筒仓产业的发展。此外,投入成本的上升和粮食储存所需的大量投资导致所有地区对筒仓的需求增加。根据国际谷物理事会(IGC)的数据,全球小麦库存从2020年的2.76亿吨增加到2021年的2.78亿吨。谷物产量的增加导致预测期内市场的成长。

此外,埃及的谷物尤其是小麦依赖进口。乌克兰和俄罗斯之间的衝突给小麦供应带来挑战。即使采取额外措施使其小麦供应多样化,全球价格上涨仍将阻碍埃及从国际来源购买大量小麦的能力。因此,埃及继续建造新的筒仓并扩大储存能力,这可能使埃及能够限制进口以抵御价格飙升。

除此之外,由于粮食运输的自动化,筒仓是一种具有成本效益的粮食储存方式,从长远来看营运成本较低。由于监控和资料采集 (SCADA) 系统实现自动化操作,因此筒仓的装卸成本也低于谷物仓库。筒仓的成本效益和大容量的优势正在推动全球粮食储存筒仓市场的发展。

北美主导市场

2020 年,北美地区使用筒仓储存粮食的比例最大。根据美国农业部 (USDA) 的数据,过去 10 年,农场内储存量增加了 16 亿蒲式耳,非农场储存量增加了 2.2 蒲式耳。亿蒲式耳,分别成长14% 和24%。该国的生产商大多喜欢平底或漏斗底筒仓,因为它们可以用于长期储存。它增加了美国平底筒仓或漏斗底筒仓的市场。

此外,美国的粮食储存能力在过去20年中大幅提高。根据美国农业部统计,2020年全国粮食储存量约253亿蒲式耳。玉米、大豆、小麦和其他作物的储存在绝对数量、收穫时间和生产地点方面有所不同。在全国范围内,玉米在粮食库存中占主导地位。收穫后玉米占美国谷物库存的四分之三以上,其中大部分玉米库存都在农场。 2021 年,在玉米总库存中,农场库存为 72.3 亿蒲式耳,比 2020 年增加 3%。主要粮食作物库存的增加导致预测期内市场成长。

同时,根据美国农业部的数据,美国和中国最近对初级商品征收关税导緻美国农民累积了粮食剩余,导致可用库存总量的 20% 被大豆、玉米、和小麦。由于现有筒仓已满负荷,预计在预测期内,全国对更多大型筒仓的需求将进一步增加。

粮食仓储产业概况

粮食仓储市场较为分散,主要参与者占市场份额较少。 Ahrens Agri、布勒集团、苏科思钢铁公司、Symaga 和 Silos Cordoba 是所研究市场的主要参与者。新产品发布、合作和收购是全球市场领先公司采取的主要策略。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 市场概况

- 市场驱动因素

- 市场限制

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代产品的威胁

- 竞争激烈程度

第 5 章:市场细分

- 类型

- 钢筒仓

- 金属筒仓

- 其他类型

- 产品

- 平底筒仓

- 料斗底部筒仓

- 饲料漏斗

- 农场筒仓

- 地理

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 俄罗斯

- 欧洲其他地区

- 亚太

- 中国

- 日本

- 印度

- 澳洲

- 亚太其他地区

- 南美洲

- 巴西

- 南美洲其他地区

- 中东和非洲

- 南非

- 中东和非洲其他地区

- 北美洲

第 6 章:竞争格局

- 最常用的策略

- 市占率分析

- 公司简介

- Rostfrei Steels

- Superior Grain Equipment

- Henan Sron Silo Engineering Co.

- Silos Cordoba

- Sioux Steel Company

- Skess Corporation

- Nelson

- Symaga

- Arsenal Steel Silos

- Ahrens Agri

第 7 章:市场机会与未来趋势

The Grain Storage Silos Market size is estimated at USD 1.83 billion in 2024, and is expected to reach USD 2.26 billion by 2029, growing at a CAGR of 4.20% during the forecast period (2024-2029).

Key Highlights

- Agricultural productivity is increasing worldwide due to the increasing population. Despite the expanding productivity, self-sufficiency is one of the critical problems due to grain losses. This grain loss happens due to proper storage facilities' unavailability, which leads to a price drop and a decrease in the profits for the farmers. The need for appropriate post-harvest storage facilities aids the market for grain silos across the globe. Therefore, the critical drivers for this market include fluctuating grain prices and rising demand for large-capacity storage.

- Along with this, the primary company's increasing investments and technological developments are also driving the market. For instance, in India, in 2021, National Commodities Management Services Limited (NCML), India's largest private-sector agriculture post-harvest management company, launched four public storage silo facilities in Haryana. Due to the increase in grain stocks every year, there is a need to have larger storage capacities, which is driving the market globally.

- Furthermore, the storage of grains is of great importance in developing and developed countries as they store large grain capacities for future use and export. Thus, the spoilage of grains by pests, rodents, and birds causes significant losses to the crops. For instance, The market for grain silos is huge in North America. Farmers in the region rarely hold substantial inventories at the end of a marketing year. Inventories of wheat and barley, corn, soybeans, and other grains are almost entirely held off-farm. Additionally, companies in the region are also expanding the silo's storage capacity to store a large volume of grains. Hence, these factors aid the market growth in the forecast period.

Grain Storage Silos Market Trends

Rising Demand for Large Capacity Storage

The growing demand for grain storage from the leading grain-producing countries in the world, namely, the United States, Russia, India, Brazil, and others, have driven the grain storage silos industry during the study period. Further, rising input costs and heavy investments required in grain storage led to a rise in demand for silos across all regions. According to the International Grains Council (IGC), the global wheat stock increased from 276 million metric tons in 2020, and the stock accounted for 278.0 million tons in 2021. This increase in the production of grains led to the market's growth in the forecast period.

Further, Egypt relies on imports for grains, especially wheat. The conflict between Ukraine and Russia caused wheat supply challenges. Even with additional measures to diversify its wheat supply, rising global prices would impede Egypt's ability to purchase large volumes of wheat from international sources. Therefore, Egypt continued to build new silos and expand its storage capacity, which may allow Egypt to limit imports to withstand price spikes.

Along with this, silos are cost-effective modes of grain storage due to the automation of grain transport, resulting in low operational costs in the long run. The loading and unloading costs of silos are also low than grain warehouses, as automation is operated by the Supervisory Control and Data Acquisition (SCADA) system. The benefits of cost-effectiveness and the large holding capacity of silos are driving the grain storage silos market globally.

North America Dominates the Market

North America held the largest share in using silos for grain storage in 2020. As per the United States Department of Agriculture (USDA), in the last ten years, the on-farm storage increased by 1.6 billion bushels and off-farm storage by 2.2 billion bushels, registering a growth of 14% and 24%, respectively. The producers in the country mostly prefer flat-bottom or hopper-bottom silos as they can be used for long-term storage. It increased the market for flat-bottom silos or hopper-bottom silos in the United States.

Moreover, the US grain storage capacity improved substantially in the last 20 years. According to USDA, in 2020, the national grain storage capacity was approximately 25.3 billion bushels. Corn, soybeans, wheat, and other crop storage differ concerning the absolute quantity, harvest timing, and production location. Nationally, corn dominates grain inventories. Post-harvest corn makes up more than three-quarters of US grain inventories, with the majority of corn inventory held on-farm. Of the total corn stocks, 7.23 billion bushels were stored on farms in 2021, an increase of 3% from 2020. This increase in the stocks of major grain crops leads to market growth during the forecast period.

Along with this, as per USDA, the recent imposition of tariffs by both the United States and China on primary commodities led to the accumulation of grain surplus for the US farmers, resulting in 20% of the total available storage filled with soybean, corn, and wheat. It is anticipated to further boost the need for more large storage silos across the country during the forecast period, as the existing ones are reaching full capacity.

Grain Storage Silos Industry Overview

The grain storage silos market is fragmented, in which major players account for less market share. Ahrens Agri, Buhler Group, Sioux Steel Company, Symaga, and Silos Cordoba are the major players in the market studied. New product launches, partnerships, and acquisitions are the major strategies adopted by the leading companies in the market globally.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Steel Silos

- 5.1.2 Metal Silos

- 5.1.3 Other Types

- 5.2 Product

- 5.2.1 Flat Bottom Silos

- 5.2.2 Hopper Bottom Silos

- 5.2.3 Feed Hoppers

- 5.2.4 Farm Silos

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United Sates

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Netherlands

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Rostfrei Steels

- 6.3.2 Superior Grain Equipment

- 6.3.3 Henan Sron Silo Engineering Co.

- 6.3.4 Silos Cordoba

- 6.3.5 Sioux Steel Company

- 6.3.6 Skess Corporation

- 6.3.7 Nelson

- 6.3.8 Symaga

- 6.3.9 Arsenal Steel Silos

- 6.3.10 Ahrens Agri

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

铝製筒仓市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

铝製筒仓市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 谷物储存筒仓市场规模、份额和趋势分析报告:按筒仓类型、储存容量、材料、应用、操作类型、地区和细分市场预测(2025-2033 年)

谷物储存筒仓市场规模、份额和趋势分析报告:按筒仓类型、储存容量、材料、应用、操作类型、地区和细分市场预测(2025-2033 年) 筒仓袋市场:按薄膜类型、材料、封口类型和最终用途划分-2025-2032 年全球预测粮仓和储存系统市场(按产品类型、容量范围、材料、最终用户和安装位置)—2025 年至 2032 年全球预测

筒仓袋市场:按薄膜类型、材料、封口类型和最终用途划分-2025-2032 年全球预测粮仓和储存系统市场(按产品类型、容量范围、材料、最终用户和安装位置)—2025 年至 2032 年全球预测 全球数位双胞胎谷仓市场:未来预测(至 2032 年)—按组件、部署方法、技术、应用、最终用户和地区进行分析

全球数位双胞胎谷仓市场:未来预测(至 2032 年)—按组件、部署方法、技术、应用、最终用户和地区进行分析 2025年全球粮仓及仓储系统市场报告

2025年全球粮仓及仓储系统市场报告 全球筒仓袋市场

全球筒仓袋市场 全球筒仓袋市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)全球粮仓及储存系统市场2025年全球粮食储存筒仓市场报告

全球筒仓袋市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)全球粮仓及储存系统市场2025年全球粮食储存筒仓市场报告