|

市场调查报告书

商品编码

1444933

光纤电缆:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Fiber Optic Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

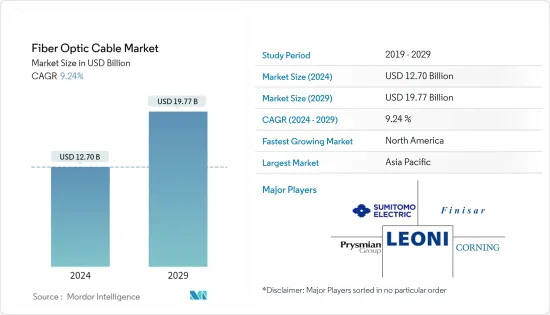

2024年光纤光缆市场规模预估为127亿美元,预估至2029年将达197.7亿美元,预测期内(2024-2029年)复合年增长率为9.24%,预计还会成长。

主要亮点

- 第五代网路和光纤基础设施的发展促进了各行业的数位转型。光纤电缆比铜缆提供更好的安全性、可靠性、频宽和安全性。光纤电缆和铜线的区别在于,光纤电缆使用光脉衝沿着光纤线路发送讯息,而不是使用电子脉衝通过铜线发送讯息。

- 随着线上交易和虚拟会议的增加,企业需要 5G 和光纤电缆来保持竞争力。这些电缆是一种经济高效、方便且简单的解决方案,适用于照明和装饰、资料传输、手术和机械测试等许多工业应用。

- 支持全球 5G 部署的政府计画正在推动市场成长。例如,欧盟委员会很早就认识到5G网路的重要性,并为5G技术的开发和研究建立了官民合作关係。因此,欧盟委员会宣布提供超过 8.61 亿美元的公共资金,透过 Horizon2020 计画支持整个欧洲的 5G 部署。

- 对5G连结不断增长的需求促使许多公司扩大产能。例如,2022年12月,爱立信宣布将与合作伙伴捷普公司在浦那扩大产能和运营,以满足印度5G网路部署的需求。

- 光纤电缆提供了许多好处,包括更高的频宽、更低的延迟以及更高的可靠性和弹性,但这些设备的安装成本可能达到数千美元,这使得许多设备成为昂贵的选择。这种高昂的安装成本可能会影响光纤市场的成长。

- COVID-19 大流行严重扰乱了全球供应链和电缆生产。由于大流行,光纤电缆工厂和製造单位已关闭,国家之间的进出口活动已暂停。对医疗基础设施的日益关注导致短期市场下跌。然而,由于数位转型、5G 采用和远距工作文化,疫情增加了对高速网路连线的需求。

光纤光缆市场趋势

电讯业预计将大幅成长

- 光纤电缆(OFC)在现代通讯结构中发挥重要作用。在过去的十年中,光纤已成为满足各种来源(包括互联网、电子商务、电脑网路和多媒体)严格频宽需求的首选频宽媒体。

- 光纤电缆具有无限频宽的优点,使其能够处理大量资讯。它们用于连接通讯网路内的各种网路节点,例如行动电话塔、资料中心和互联网服务供应商,从而允许在不同位置之间交换大量资料。光纤电缆还促进了高速互联网连接和视讯会议、线上游戏和云端运算等先进通讯技术的发展。

- 光纤电缆用于通讯业有多种原因,包括高速度和频宽、低衰减、抗电磁干扰、高可靠性、与铜缆相比维护成本低,以及由于难以窃听和窃听而具有高安全性。优点。此外,由于其安全性、扩充性和无限频宽潜力,光纤电缆也被选择来支援严重依赖即时资料收集和传输的先进技术,例如 5G、巨量资料和物联网。 5G 的推出预计将增加容量并减少网路的直接延迟。

- 互联网是全球最具创新性和发展最快的技术之一,而访问互联网的用户数量每天都在增加。截至2023年1月,美国有3.113亿网路用户,网路普及为总人口的91.8%。随着越来越多的人连接到互联网,对高速互联网的需求不断增长,这就需要更高的频宽,而这只能透过光纤电缆来实现。

- 光纤技术被《政府技术》杂誌描述为「未来性」。康卡斯特等通讯巨头已经从铜同轴电缆转向混合或全光纤电缆组件。一些专家认为,在先进电子产品的开发中,光纤有可能提供比无线更大的覆盖范围。光纤电缆预计将比下一代设备和工业要求更耐用,因为它们不会像其他基础设施那样劣化。因此,光纤的未来是充满希望的。

北美预计将成为成长最快的市场

- 近年来,随着该地区光纤部署步伐的加快,北美占据了重要地位。例如,根据光纤宽频协会 2022 年光纤供应商调查结果,美国光纤到府 (FTTH) 部署预计将在未来几年创下纪录。调查结果显示,儘管存在供应链和劳动力限制,但 2022 年 FTTH 网路仍覆盖美国790 万户家庭。

- 该协会表示,FTTH 部署的快速成长是政府大规模资助的结果,特别是 BEAD、RDOF 和 ReConnect,它们已开始产生直接影响。例如,宽频公平、存取和部署 (BEAD) 计划为所有 50 个州、华盛顿特区、波多黎各、美国属维京群岛、关岛、美属萨摩亚和英联邦的规划、基础设施部署和实施计划提供资金。北马里亚纳群岛。424.5亿美元用于扩大高速互联网接入,提供

- 此外,2022 年 7 月,美国农业部 (USDA) 宣布启动一项耗资 4 亿美元的项目,为 11 个州的 31,000 名农村居民和企业提供高速互联网接入,作为美国政府农村基础设施投资的一部分。100 万美元。每个人都可以以实惠的价格使用高速网路。

- 同样在 2022 年 11 月,加拿大光纤公司 (Canadian Fiber Optics Corp.) 宣布计划将其光纤延伸至位于亚伯达High Prairie (FTTH) 的总部基地。 CFOC 声称,该服务以 Northern Lights Fiber (NLF) 品牌提供,具有加拿大农村地区最快的住宅网路速率。

光纤光缆产业概况

光纤电缆市场竞争激烈,主要企业包括康宁公司、莱尼股份公司、藤仓有限公司和日立电缆美国公司(日立电缆)以及许多区域参与者。新业务的进入门槛较低,导致大量地区公司涌入光纤电缆产业。

2023 年 7 月,康普宣布将在未来四年内投资 6,030 万美元,扩建位于北卡罗来纳州的製造工厂。在联邦努力实现「全民网路」(包括服务不足和农村宽频市场)的推动下,这些计画将在未来四年内提高美国的供应能力,从而增强康普满足需求的能力。

2023 年 1 月,普睿司曼集团推出了 864 芯版本的 Scirocco HD 微管光纤电缆。新光缆的光纤密度为每平方毫米 9.1 条光纤,可安装在 13 毫米管道中。电缆直径为11.0mm,可容纳864芯线。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 消费者议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争公司之间的敌意强度

- 评估 COVID-19 对市场的影响

第五章市场动态

- 市场驱动因素

- 网路的普及和大量资料流量的增加

- 技术进步推动市场成长

- 资料中心设施数量增加

- 市场挑战

- 高安装成本和相关的复杂性

- 定价及价格趋势分析

- 技术蓝图

第六章市场区隔

- 按最终用户产业

- 通讯

- 电力公司

- 国防/军事

- 工业的

- 医疗保健

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 马来西亚

- 印尼

- 泰国

- 越南

- 新加坡

- 菲律宾

- 其他亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争形势

- 公司简介

- Corning Inc.

- Sumitomo Electric Industries Ltd

- Prysmian Group

- Furukawa Electric

- CommScope Holding Company Inc.

- Coherent Corporation

- Finolex Cables Limited

- Proterial Cable America Inc.(Proterial Ltd)

- Sterlite Technologies

- Yangtze Optical Fiber and Cable Joint Stock Ltd Co.

第八章 市场未来展望

The Fiber Optic Cable Market size is estimated at USD 12.70 billion in 2024, and is expected to reach USD 19.77 billion by 2029, growing at a CAGR of 9.24% during the forecast period (2024-2029).

Key Highlights

- The evolution of fifth-generation networks and fiber optic infrastructure has driven digital transformation across industries. Fiber optic cable offers better security, reliability, bandwidth, and security than copper cables. The difference between a fiber optic cable and a copper wire is that the fiber optic cable uses light pulses to transmit information down the fiber lines instead of using electronic pulses to transmit information through the copper lines.

- With growing online transactions and virtual meetings, companies need 5G and optic fiber cable to stay competitive. These cables are cost-effective, convenient, and easy solutions for many industrial applications, such as lighting and decorations, data transmission, surgeries, and mechanical inspections.

- The government programs to support 5G deployment across the globe drive market growth. For instance, the European Commission recognized the importance of the 5G network early and established a public-private partnership to develop and research 5G technology. As a result, the European Commission announced public funding of over USD 861 million to support 5G deployment across Europe through the Horizon 2020 Program.

- Due to the increasing demand for 5G connections, many players are expanding their production capabilities. For instance, in December 2022, Ericsson announced scaling up the production capacity and operations with its partner Jabil in Pune to meet the needs of 5G network deployments in India.

- Although fiber optic cable offers a host of benefits, such as higher bandwidth, low latency, and a higher degree of reliability and flexibility, they often are an expensive choice as the installation for these devices may go up to thousands of dollars. This high installation cost may impact the market growth for Fiber Optics.

- The COVID-19 pandemic severely disrupted the global supply chain and cable production. The pandemic resulted in the shutdown of factories and manufacturing units of fiber optic cables and suspended import-export activities among countries. The increased focus on medical infrastructure led to a short-term decline in the market. However, the pandemic increased the digital transformation, 5G deployment, and demand for high-speed network connectivity due to the remote work culture.

Fiber Optics Cable Market Trends

Telecommunications Sector is Expected to Witness Significant Growth

- Optical fiber cable (OFC) plays a crucial role in modern telecommunication infrastructure. Over the last decade, fiber optics has become the preferred transmission medium to cater to aggressive bandwidth demands from various sources, including the Internet, e-commerce, computer networks, and multimedia.

- Fiber optic cables offer the advantage of infinite bandwidth, which makes them capable of handling vast amounts of information. They are used to connect different network nodes in telecommunication networks, such as cell towers, data centers, and internet service providers, enabling the exchange of large amounts of data between different locations. Fiber optic cables have also enabled the development of high-speed internet connections and advanced communication technologies, such as video conferencing, online gaming, and cloud computing.

- Fiber optic cables offer several benefits in the telecommunication industry, including high speed and bandwidth, low attenuation, immunity to electromagnetic interference, high reliability, less maintenance compared to copper cables, and difficulty in tapping or intercepting, which ensures high security. Moreover, owing to their security, scalability, and unlimited bandwidth potential, fiber optic cables are also being chosen to support advanced technologies such as 5G, Big Data, and IoT that rely heavily on real-time data collection and transfer. The launch of 5G is expected to enhance capacity and lower latency straight to networks.

- The Internet is one of the most transformative and fast-growing technologies globally, with an increasing number of users accessing it every day. As of January 2023, the United States had 311.3 million Internet users, with an Internet penetration rate of 91.8% of the overall population. The demand for high-speed Internet continues to rise as more people get online, and this requires higher bandwidth, which can only be achieved through fiber optic cables.

- Fiber optic technology has been described as "future-proof" by Government Technology magazine. Telecom giants such as Comcast have already transitioned from copper coaxial cable to hybrid or fully fiber optic cable assemblies. Several specialists believe that fiber optics may carry more scope than wireless for rising sophisticated electronics. Fiber cables are expected to outlast the next generation of devices and industrial requirements as they are not expected to degrade like other infrastructure. The future of fiber optics is, therefore, promising

North America is Expected to be the Fastest Growing Market

- North America has obtained a prominent position owing to the increasing pace of fiber optic deployment in the country in recent times. For instance, according to the 2022 Fiber Provider Survey findings by the Fiber Broadband Association, US fiber-to-the-home (FTTH) deployments are expected to set a record in the coming years. The findings showed FTTH networks passed 7.9 million additional homes in the United States in 2022, despite supply chain and labor constraints.

- According to the association, the jump in FTTH deployments is a result of significant government funding efforts, such as BEAD, RDOF, and ReConnect, among others, which are beginning to have a direct effect. For instance, the Broadband Equity, Access, and Deployment (BEAD) Program provides USD 42.45 billion to expand high-speed internet access by funding planning, infrastructure deployment, and adoption programs in all 50 states, Washington DC, Puerto Rico, the US Virgin Islands, Guam, American Samoa, and the Commonwealth of the Northern Mariana Islands.

- Furthermore, in July 2022, the US Department of Agriculture (USDA) announced an investment of USD 401 million to provide access to high-speed internet for 31,000 rural residents and businesses in 11 states as part of the US government's commitment to investing in rural infrastructure and affordable high-speed internet for all.

- Also, in November 2022, Canadian Fiber Optics Corp. announced its plans to extend its fiber to High Prairie, Alberta's home (FTTH) footprint. The services, offered under the Northern Lights Fiber (NLF) brand, will feature the fastest residential internet rates offered in rural Canada, CFOC asserts.

Fiber Optics Cable Industry Overview

The Fiber Optic Cable Market is highly competitive, with key players such as Corning Inc., Leoni AG, Fujikura Ltd, and Hitachi Cable America Inc. (Hitachi Cable) alongside numerous regional firms. The barriers to entry for new players are moderate, which has led to an influx of regional companies seeking to enter the fiber optic cable industry.

In July 2023, CommScope announced to invest USD 60.3 million over the next four years to expand its manufacturing facilities based in North Carolina. These plans bolster CommScope's ability to meet U.S. supply demands driven by federal initiatives to bring 'Internet For All,' including in underserved and rural broadband markets, along with enhancing production capacity over the next four years.

In January 2023, Prysmian Group introduced its Sirocco HD micro duct cables with an 864-fiber version. The new cable boasts a fiber density of 9.1 fibers per square millimeter and can be installed in a 13-mm duct. The cable's diameter is 11.0 mm, making it possible to squeeze 864 fibers into it.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Penetration of Internet and High Data Traffic

- 5.1.2 Technological Advancements to Augment the Market Growth

- 5.1.3 Rising Number of Data Center Facilities

- 5.2 Market Challenges

- 5.2.1 High Cost of Installation and Associated Complexities

- 5.3 Analysis of Pricing and Pricing Trends

- 5.4 Technology Roadmap

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 Telecommunication

- 6.1.2 Power Utilities

- 6.1.3 Defense/Military

- 6.1.4 Industrial

- 6.1.5 Medical

- 6.1.6 Other End-User Industry

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.3.3 India

- 6.2.3.4 Malaysia

- 6.2.3.5 Indonesia

- 6.2.3.6 Thailand

- 6.2.3.7 Vietnam

- 6.2.3.8 Singapore

- 6.2.3.9 Philippines

- 6.2.3.10 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Corning Inc.

- 7.1.2 Sumitomo Electric Industries Ltd

- 7.1.3 Prysmian Group

- 7.1.4 Furukawa Electric

- 7.1.5 CommScope Holding Company Inc.

- 7.1.6 Coherent Corporation

- 7.1.7 Finolex Cables Limited

- 7.1.8 Proterial Cable America Inc. (Proterial Ltd)

- 7.1.9 Sterlite Technologies

- 7.1.10 Yangtze Optical Fiber and Cable Joint Stock Ltd Co.

8 FUTURE OUTLOOK OF THE MARKET

扩展光束电缆市场 - 全球产业规模、份额、趋势、机会和预测(按镜头尺寸、技术、连接器类型、单通道连接器与多通道连接器、地区、竞争情况细分)2018-2028 年

扩展光束电缆市场 - 全球产业规模、份额、趋势、机会和预测(按镜头尺寸、技术、连接器类型、单通道连接器与多通道连接器、地区、竞争情况细分)2018-2028 年 全球光纤光缆市场:按国家分析和预测(2023-2032)

全球光纤光缆市场:按国家分析和预测(2023-2032) 光纤电缆配件市场规模、份额、趋势分析报告:按产品类型、应用、地区和细分市场预测,2023-2030 年

光纤电缆配件市场规模、份额、趋势分析报告:按产品类型、应用、地区和细分市场预测,2023-2030 年 光纤电缆的全球市场

光纤电缆的全球市场 2023-2027年全球光纤电缆市场

2023-2027年全球光纤电缆市场 光纤电缆市场:按类型(多模、单模)、最终用途(商业、军事、太空)、用途- 俄罗斯-乌克兰衝突、高通胀的累积影响 - 2023-2030 年全球预测

光纤电缆市场:按类型(多模、单模)、最终用途(商业、军事、太空)、用途- 俄罗斯-乌克兰衝突、高通胀的累积影响 - 2023-2030 年全球预测 光纤电缆组件的全球市场的预测(~2030年)

光纤电缆组件的全球市场的预测(~2030年) 光纤电缆的全球市场:考察与预测 (到2029年)

光纤电缆的全球市场:考察与预测 (到2029年) 扩张电子束电缆的全球市场:各镜头尺寸,各技术,各用途,各连接器类型,各地区展望,竞争策略,各市场区隔预测(~2032年)

扩张电子束电缆的全球市场:各镜头尺寸,各技术,各用途,各连接器类型,各地区展望,竞争策略,各市场区隔预测(~2032年)