|

市场调查报告书

商品编码

1445430

DPaaS(资料保护即服务):市场占有率分析、产业趋势与统计、成长预测(2024-2029)Data Protection as a Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

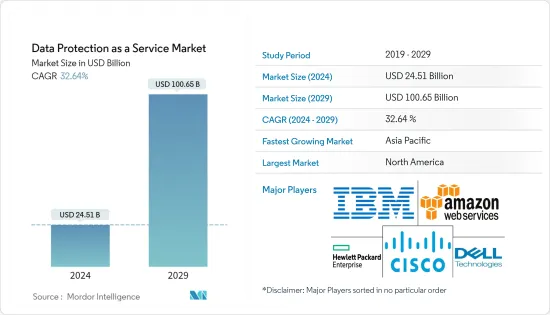

DPaaS(资料保护即服务)市场规模预计到 2024 年为 245.1 亿美元,预计到 2029 年将达到 1006.5 亿美元,在预测期内(2024-2029 年)将以 32.64% 的复合年增长率增长。

随着云端服务的成长和普及,许多公司正在寻求增强其託管服务以提供更好的优势,例如更高的可扩展性、管理和恢復选项。各种云端储存和资料安全公司正在开发资料保护即服务模型,以更好地满足客户的需求,从而推动市场向前发展。

随着时间的推移,网路攻击的频率和规模显着增加。组织需要多层、高度连接的安全系统来降低风险并防止攻击。随着威胁的不断增加和安全技能差距的扩大,内部安全团队已不足以保护您的业务。因此,此类组织不可避免地会转向资料保护即服务 (DPaaS) 解决方案。

儘管资料外洩和网路攻击的数量不断增加,但客户并不害怕与第三方公司共用他们的资料。据 SurfShark 称,2022 年第三季度,全球约有 1500 万笔资料记录因资料外洩而外洩。与上一季相比,这一数字增长了约 37%。资料外洩事件的增加使得 DPaaS(资料保护即服务)成为必要,并正在推动市场的显着成长。

此外,快速采用下一代技术以及增加资料向云端模型的迁移以获得弹性和敏捷性并优化成本节约是促进市场成长的关键因素。因此,保护和储存关键资料免受资料窃取、资料遗失和操作灾难影响企业考虑云端上的资料保护服务和解决方案,从而显着推动市场成长。

然而,对隐私和安全的日益担忧可能是在预测期内扩大市场整体成长率的因素。

一些政府以及公共和私人组织已采取措施来应对这场危机并限制 COVID-19 疾病的传播。从保持社交距离到强制在家工作(如果可能)、取消不必要的实体会议以及推广手部卫生通讯协定,人们的生活和工作方式已经改变了。这些措施的执行可能涉及私人入侵,需要公共当局和私人公司采取有效的资料保护措施,这将对 DPaaS(资料保护即服务)市场产生积极影响。

DPaaS(资料保护即服务)市场趋势

混合云端预计将占据较大份额

- 公共云端服务长期以来一直向组织承诺提供广泛的好处,但对资料保护、安全性和合规性的担忧始终阻碍了一些企业的发展。 HPE 最近委託的一份报告发现,当工作负载被认为不适合公共云端时,这三个问题是最重要的因素。随着混合云端的混合云端,形势正在发生变化,为组织提供最好的本地、私有和公共云端世界。

- 选择与供应商无关的模型来分散资料外洩和安全漏洞风险的组织数量显着增加。混合云端是这演变的核心。这种方法可能会增加资料保护的复杂性,但也使资讯安全变得更加有用。

- 据 Evaluator Group 称,58% 的组织使用混合云端资料保护解决方案进行灾害復原。同时保护资料中心内的实体资产和资料仍然是一项基本要求。虚拟资产和资料的保护也越来越受到重视。

- 采用混合云端灾难復原可以为企业带来许多好处,包括消除对辅助灾难復原站点的需求。此外,混合云端还降低了系统维护和管理的复杂性和成本。所有这些因素都解释了基于混合云端的资料保护解决方案的成长。

- IBM 表示,透过采用混合平台作为支援关键应用程式工作负载的核心策略,企业可以从工作负载效率的提高中获得业务效益。 IT 领导者报告称,到 2022 年,在混合云端中运行应用程式的最常见好处是能够优化灾害復原和业务连续性。

预计北美将占据主要份额

- 由于高认知度和高采用需求,北美市场预计将主导 DPaaS(资料保护即服务)市场。此外,提供资料保护即服务的领先公司总部位于美国,包括 IBM、思科和 Amazon Web Services 等公司。

- 随着中小企业数量的不断增加,该地区的资料中心市场正在健康成长。此外,由于资料产生量的快速增加,资料从私有伺服器迁移到云端网路的情况也已出现。这一趋势需要有弹性且可靠的备份和復原解决方案,因为服务中断会给服务供应商带来重大损失。

- 在美国,没有专门负责监督资料保护法的单一监管监督。负责联邦层级监督的监管机构会根据相关法律或法规的差异而有所不同。例如,在金融服务领域,消费者金融保护局和各个金融服务监管机构已经实施了《美国金融服务业现代化法》,该法案规范了受监管公司如何收集、使用和披露非资讯资讯。我们采用了标准基于GLB。

- 根据美国卫生与公众服务部的数据,2021 年受医疗资料外洩影响的美国居住者总数约为 4,600 万人。该地区此类案例数量的不断增加将对DPaaS(资料保护即服务)产生巨大的需求,进一步推动市场成长机会。

- 根据身分盗窃资源中心的数据,2022 年上半年美国资料外洩总数为 817总合。同时,同期,超过5,300万个人受到资料外洩、资料外洩、资料外洩等资料外洩事件的影响。

DPaaS(资料保护即服务)产业概述

资料保护即服务 (DPaaS) 市场竞争适中,由多家主要企业组成。从市场占有率来看,目前占据市场主导地位的公司寥寥可数。然而,随着资料储存和安全系统的创新,两家公司都在开发整个新兴市场,以获得新契约并扩大市场占有率。

2022 年 11 月,资料安全和管理供应商 Cohesity 将与网路安全「相关人员」合作,在 Cohesity 的资料安全和管理高峰会ReConnect 上了解有关赢得网路攻击之战的更多资讯。宣布将为客户提供一种方法资料安全联盟增加了来自业界领先的网路安全和服务公司的一流解决方案,以及 Cohesity 无与伦比的资料管理和安全专业知识。

2022 年 7 月,T-Systems 宣布其在 Amazon Web Services (AWS) 身分和存取管理安全能力中获得优秀评级。此头衔体现了T-Systems 的AWS 品质和技术要求,旨在为客户提供身分和存取管理方面的深层咨询和软体专业知识,帮助他们实现云端安全目标。这是为了证明这些要求已得到适当满足。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业相关人员分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争公司之间的敌意强度

第五章市场动态

- 市场驱动因素

- 海量资料对资料安全的需求日益增长

- 实施资料保护解决方案的严格规定

- 市场限制因素

- 云端基础的隐性成本不断增加

第六章市场区隔

- 服务

- Storage-as-a-Service

- Backup-as-Service

- Disaster Recovery-as-a-Service

- 部署

- 公共云端

- 私有云端

- 混合云端

- 最终用户产业

- BFSI

- 保健

- 政府和国防

- 资讯科技和电信

- 其他最终用户产业

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 北美洲

第七章 竞争形势

- 公司简介

- IBM Corporation

- Amazon Web Services Inc.

- Hewlett Packard Enterprise Company

- Dell Inc.

- Cisco Inc.

- Oracle Corporation

- VMware Inc.

- Commvault Systems Inc.

- Veritas Technologies LLC

- Asigra Inc.

- Quantum Corporation

- Quest Software Inc.

- NxtGen Datacenter &Cloud Technologies Pvt. Ltd.

- Hitachi Vantara Corporation

第八章投资分析

第9章市场的未来

The Data Protection as a Service Market size is estimated at USD 24.51 billion in 2024, and is expected to reach USD 100.65 billion by 2029, growing at a CAGR of 32.64% during the forecast period (2024-2029).

With the increased growth and popularity of cloud services, many businesses are looking to enhance their hosted services to give them better benefits, such as higher scalability, management, and recovery options. Various cloud storage and data security companies are developing data protection as a service model to meet better their client's needs, which propels the market forward.

Over time, the frequency and scale of cyberattacks have grown significantly. Organizations need a multi-layered, highly connected security system to mitigate risks and prevent attacks. With this growing threat and the increasing security skills gap, in-house security teams are no longer sufficient to protect businesses. Therefore, it has become inevitable for such organizations to look towards Data Protection as a Service (DPaaS) solution.

Even though the number of data breaches and cyberattacks has increased, customers are not afraid of sharing their data with third-party companies. As per SurfShark, during the third quarter of 2022, around 15 million data records were exposed worldwide through data breaches. It had increased by about 37% compared to the previous quarter. This rise in data breaches necessitates Data Protection-as-a-Service, driving the market's growth significantly.

Moreover, the surge in the adoption of next-generation technologies and rising data migration to a cloud model to gain flexibility and agility and optimize cost savings are vital factors contributing to market growth. Thus, safeguarding and storing critical data from data theft, data loss, and operational disasters influences enterprises to consider data protection services and solutions over the cloud, drastically enhancing the market's growth.

However, the rise in concerns regarding privacy and security might be a factor that could amplify the overall growth rate of the market throughout the forecast period.

Several governments and public and private organizations have introduced measures to tackle this crisis and help limit the spread of COVID-19. From social distancing to (where possible) mandatory teleworking, discontinuing nonessential physical meetings, and promoting hand hygiene protocol, the way people live, and work has changed. The enforcement of these measures can entail private-invasive actions that require efficient means of data protection by public institutions and private companies, which could positively impact the Data Protection as a Service market.

Data Protection as-a-Service (DPaaS) Market Trends

Hybrid Cloud is Expected to Hold Significant Share

- While public cloud services have long promised organizations a massive range of benefits, fears around data protection, security, and compliance have always held some firms back. A recent report commissioned by HPE found that these three issues were the most significant factors when workloads were considered unsuitable for the public cloud. With the growth of hybrid cloud, the landscape is changing, as hybrid cloud offers organizations the best of the on-premises, private, and public cloud worlds.

- There is a significant growth in the number of organizations opting for vendor-agnostic models that help them spread out the risks of data breaches and security lapses. The hybrid cloud is at the center of this evolution. While approaches like that may increase the complexity of the protection of the data, at the same time, it makes information security even more helpful.

- According to the Evaluator Group, 58% of organizations use hybrid cloud data protection solutions for disaster recovery. Protecting physical assets and data simultaneously in the data center remains an essential requirement. Protecting virtual assets and data is also gaining traction.

- Adopting hybrid cloud disaster recovery offers various advantages to businesses, such as eliminating the need for a secondary disaster recovery site. Further, the hybrid cloud also reduces the complexities and expenses of the maintenance and management of a system. All these factors account for the growth of hybrid cloud-based data protection solutions.

- As per IBM, with hybrid platforms as the central strategy for supporting key application workloads, firms are reaping the business benefits of improved efficacy of workload. In 2022, the most prevalent advantage of running applications on a hybrid cloud, as reported by IT leaders, was the ability to optimize disaster recovery and business continuity.

North America is Expected to Hold Major Share

- The North American market is expected to dominate the Data Protection as a Service Market due to high awareness and the high demand for implementation. Moreover, major players who offer Data Protection as a Service are headquartered in the United States, which includes companies such as IBM, Cisco, and Amazon Web Services.

- With the increasing number of SMEs, the data center market in the region has witnessed healthy growth. Further, a data shift has been observed from private servers to cloud networks due to exponential growth in data generation volume. This trend entails resilient and reliable backup and recovery solutions, as disruption of services results in enormous losses for the service providers.

- No single regulatory authority is dedicated to overseeing data protection law in the U.S. The regulatory authority responsible for oversight at the federal level depends on the law or regulation in question. In the financial services context, for example, the Consumer Financial Protection Bureau and various financial services regulators have adopted standards under the Gramm-Leach-Bliley Act (GLB) that dictates how firms subject to their regulation may collect, use, and disclose non-public personal information.

- According to the U.S. Department of Health and Human Services, in 2021, the total number of U.S. residents affected by healthcare data breaches was around 46 million. The rise in such cases in the region creates a massive demand for Data Protection as a Service, further enhancing the market's growth opportunities.

- As per Identity Theft Resource Center in the 1sthalf of 2022, the total number of data compromises in the U.S. came in at a total of 817 cases. Meanwhile, throughout the same time, over 53 million individuals were affected by data compromises, which included data breaches, data leakage, and data exposure.

Data Protection as-a-Service (DPaaS) Industry Overview

The Data Protection as a Service (DPaaS) market is moderately competitive and consists of several major players. In terms of market share, few players currently dominate the market. However, with innovation in data storage and security systems, the companies are increasing their market presence by securing new contracts by tapping across emerging markets.

In November 2022, Cohesity, a data security and management provider, announced at ReConnect, Cohesity's data security and management summit, that it is partnering with the 'who's who' of cybersecurity to provide customers more ways to win the war against the cyberattacks. The Data Security Alliance adds best-in-class solutions from industry-leading cybersecurity and services companies with exceptional data management and security expertise from Cohesity.

In July 2022, T-Systems declared that it had achieved an Identity and Access management distinction in the Amazon Web Services (AWS) Security Competency. This designation recognizes that T-Systems has demonstrated and successfully met the AWS's quality and technical requirements for offering customers with a deep level of consulting and software expertise in identity and access management to assist them achieve their cloud security goals.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Need for Data Security due to Huge Volume of Data

- 5.1.2 Stringent Regulations Regarding the Adoption of Data Protection Solutions

- 5.2 Market Restraints

- 5.2.1 Increasing Hidden Costs of Cloud-based Storage

6 MARKET SEGMENTATION

- 6.1 Service

- 6.1.1 Storage-as-a-Service

- 6.1.2 Backup-as-Service

- 6.1.3 Disaster Recovery-as-a-Service

- 6.2 Deployment

- 6.2.1 Public Cloud

- 6.2.2 Private Cloud

- 6.2.3 Hybrid Cloud

- 6.3 End-user Indsutry

- 6.3.1 BFSI

- 6.3.2 Heathcare

- 6.3.3 Government and Defense

- 6.3.4 IT and Telecom

- 6.3.5 Other End-user Industries

- 6.4 Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Rest of Europe

- 6.4.3 Asia Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.3.4 Rest of Asia Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Amazon Web Services Inc.

- 7.1.3 Hewlett Packard Enterprise Company

- 7.1.4 Dell Inc.

- 7.1.5 Cisco Inc.

- 7.1.6 Oracle Corporation

- 7.1.7 VMware Inc.

- 7.1.8 Commvault Systems Inc.

- 7.1.9 Veritas Technologies LLC

- 7.1.10 Asigra Inc.

- 7.1.11 Quantum Corporation

- 7.1.12 Quest Software Inc.

- 7.1.13 NxtGen Datacenter & Cloud Technologies Pvt. Ltd.

- 7.1.14 Hitachi Vantara Corporation

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

资料保护服务的全球市场规模、份额和趋势分析:按服务、按部署、按公司规模、按最终用途、按地区、前景和预测,2024-2031 年

资料保护服务的全球市场规模、份额和趋势分析:按服务、按部署、按公司规模、按最终用途、按地区、前景和预测,2024-2031 年 资料保护即服务市场:按类型、部署、组织规模、产业划分 – 2025-2030 年全球预测

资料保护即服务市场:按类型、部署、组织规模、产业划分 – 2025-2030 年全球预测 DPaaS(资料保护即服务)市场规模、份额和成长分析:按服务类型、部署、最终用途、地区 - 产业预测,2024-2031 年

DPaaS(资料保护即服务)市场规模、份额和成长分析:按服务类型、部署、最终用途、地区 - 产业预测,2024-2031 年 DPaaS(资料保护即服务)的全球市场,2024-2028

DPaaS(资料保护即服务)的全球市场,2024-2028 DPaaS(资料保护即服务)市场:依地区(北美、欧洲、亚太地区、拉丁美洲、中东非洲):全球产业分析、规模、占有率、成长、趋势、预测 2024-2032

DPaaS(资料保护即服务)市场:依地区(北美、欧洲、亚太地区、拉丁美洲、中东非洲):全球产业分析、规模、占有率、成长、趋势、预测 2024-2032 2024 年 DPaaS(资料保护即服务)全球市场报告

2024 年 DPaaS(资料保护即服务)全球市场报告 全球数据保护即服务 (DPaaS) 市场——增长、未来展望、竞争分析 (2023-2031)

全球数据保护即服务 (DPaaS) 市场——增长、未来展望、竞争分析 (2023-2031)