|

市场调查报告书

商品编码

1445581

金属镁 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Metal Magnesium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

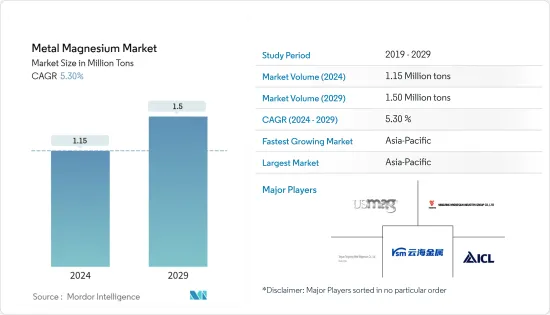

2024年金属镁市场规模预计为115万吨,预计到2029年将达到150万吨,在预测期(2024-2029年)CAGR为5.30%。

COVID-19 大流行对 2020 年的市场产生了负面影响。然而,由于汽车和电子等各种不断增长的最终用户行业的消费增加,2021 年的需求有所增加。此外,在电子领域,镁也用于散热系统、电视和电脑外壳等。这导致了大流行后时代市场的稳定成长,并预计在预测期内将继续以同样的速度成长。

主要亮点

- 短期内,与其他金属合金化的需求不断增长,以及航空航太和汽车行业对轻质材料的需求不断增长,是刺激市场需求的一些驱动因素。

- 另一方面,金属价格的波动预计将阻碍市场成长。

- 未来几年,随着越来越多的人购买电动车,市场可能会有更多机会。

- 亚太地区预计将主导市场,并且在预测期内也可能出现最高的CAGR。

金属镁市场趋势

增加铝合金生产中的用量

- 镁为金属(尤其是铝合金)提供中等和高强度的特性,而不影响延展性。添加镁的铝合金属于 5000 系列,并以板材和片材形式在市场上销售。

- 铝合金的主要应用包括航空航太零件製造、汽车零件製造、工业零件、工具和机械等。

- 随着越来越多的人想要电动车,汽车的製造方式正在改变。根据国际汽车製造商组织(OICA)的数据,2022年OICA成员国新车销售和註册总数接近6,900万辆因此,销售或製造的车辆数量的增加将导致市场对铝合金的需求增加。

- 此外,2022年前三季度,全球乘用车产量约5000万辆,较2021年同季度增长近9%,但仍比2019年疫情前水平少500万辆左右根据欧洲汽车製造商协会(ACEA ) 的报告。

- 然而,电动车领域的需求可能会增加对铝合金的需求。多种应用对轻质组件不断增长的需求预计将推动市场发展。

- 根据世界经济论坛 (WEF) 的数据,2022 年上半年全球销售了近 430 万辆新型电池驱动电动车 (BEV) 和插电式混合动力电动车 (PHEV)。此外,BEV 销量成长了约 75%与PHEV 相比,年增了37%。此外,2022年前8个月全球电动车销量突破570万辆大关,插电式电动车市占率已增至近15%。

- 铝合金也用于飞机,因为它们坚固且重量轻。减轻飞机的重量是节省能源和减少燃料使用的好方法,因为较轻的飞机需要较小的升力和推力来飞行。

- 由于航空旅客和贸易业务航空运输的增加,对商用飞机的需求不断增长,刺激了製造业。它涵盖了能够承载重载且性能高效的高强度、轻量化飞机。

- 根据波音公司对2022-2041年的商业展望,预计在预测期结束时(2041年)北美地区将覆盖全球机队的约22%。预计未来二十年机队交付量将达到 9,310 架,其中单通道交付量几乎占该地区总交付量的 70%。

- 由于所有这些因素,金属镁市场在预测期内可能会在全球范围内增长。

亚太地区将主导市场

- 亚太地区是全球市场上最大的金属镁消费国。中国、印度和日本等国大量使用镁金属。

- 金属镁主要用于铝合金、压铸、钢铁、金属还原等。此外,铝合金和压铸件越来越多地应用于汽车零件、航空航太零件和设备以及其他最终用户产业的製造。亚太地区在全球汽车、航空航太和电子市场中占有重要份额。

- 中国是汽车行业最大的製造商,预计该国的镁市场将呈指数级增长。根据中国汽车工业协会(CAAM)的数据,2022年中国汽车产量比上年成长约3.4%。 2022年汽车产量约2,700万辆,而2021年为2,608万辆。

- 此外,印度品牌资产基金会(IBEF)预测,到2026年,印度汽车产业规模将达到3,000亿美元。报告还称,2,222财年印度汽车年产量约2,300万辆。

- 在预测期内,中国对电动车的需求也可能强劲成长。这是因为,由于更多的政府措施、更多的电动车製造公司和更多的充电站,这个国家正在迅速改变。

- 中国已成为最大的电动车生产国和购买国,约占全球市场的一半。根据中国汽车工业协会的数据,预计2022年中国新能源汽车总产量约为700万辆单位。与 2021 年汽车产量(354 万辆)相比,增幅接近 97%。

- 日本也计划在2035年过渡到100%电动车销售,日本电动车市场正在成长。美国企业可能会在与电动车相关的各个领域找到商机。因此,该国电动车市场的扩大预计将有利于市场成长。

因此,上述所有因素很可能会对未来亚太地区金属镁的需求产生重大影响。

金属镁产业概况

金属镁市场本质上是部分整合的。研究市场的一些主要参与者包括南京云海特殊金属、太原桐乡金属镁、死海镁业(ICL集团)、闻喜银光镁业(集团)和美国镁业有限责任公司等(排名不分先后) 。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 司机

- 与其他金属合金化的需求不断增长

- 航太和汽车产业对轻质材料的需求不断增长

- 限制

- 金属价格波动

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第 5 章:市场区隔(市场规模按数量计算)

- 最终用户产业

- 铝合金

- 压铸

- 铁和钢

- 金属还原

- 其他最终用户产业

- 地理

- 亚太

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太

第 6 章:竞争格局

- 併购、合资、合作与协议

- 市占率(%)分析

- 领先企业采取的策略

- 公司简介

- American Magnesium

- Dead Sea Magnesium (ICL Group)

- Fu Gu Yi De Magnesium Alloy Co. Ltd.

- Nanjing Yunhai Special Metals Co. Ltd.

- Regal Metal

- Rima Industrial

- Shanxi Bada Magnesium Co. Ltd.

- Solikamsk Magnesium Works

- Southern Magnesium & Chemicals Limited (SMCL)

- Taiyuan Tongxiang Metal Magnesium Co. Ltd.

- US Magnesium LLC

- Wenxi Yinguang Magnesium Industry (group) Co. Ltd.

- Western Magnesium Corporation

第 7 章:市场机会与未来趋势

- 电动车的普及率不断提高

The Metal Magnesium Market size is estimated at 1.15 Million tons in 2024, and is expected to reach 1.5 Million tons by 2029, growing at a CAGR of 5.30% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the market in 2020. However, the demand increased in 2021 due to the rise in consumption from various growing end-user sectors, such as automotive and electronics. Moreover, in electronics, magnesium is used in heat dissipation systems, television and computer casings, and others. This resulted in the steady growth of the market in the post-pandemic era and is expected to continue at the same pace during the forecast period.

Key Highlights

- Over the short term, the growing demand for alloying with other metals and the increasing demand for lightweight materials in the aerospace and automotive industries are some driving factors stimulating market demand.

- On the flip side, fluctuations in the prices of metals are expected to hinder market growth.

- In the coming years, the market is likely to have more opportunities as more people buy electric cars.

- The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Metal Magnesium Market Trends

Increasing Usage in the Production of Aluminum Alloys

- Magnesium offers moderate and high strength characteristics to metals, especially aluminum alloys, without impacting the ductility. Aluminum alloys with magnesium added are placed in the 5000 series and are commercially available in plates and sheets.

- Major applications of aluminum alloys include aerospace parts manufacturing, automotive component manufacturing, industrial components, tools and machinery, and others.

- As more people want electric cars, the way cars are made is changing.According to the Organization Internationale des Constructeurs d'Automobiles (OICA), the total number of new automobile sales and registrations in OICA member countries was close to 69 million units in 2022. So, a rise in the number of vehicles sold or made would lead to a rise in the market demand for aluminum alloys.

- Moreover, in the first three quarters of 2022, around 50 million passenger cars were manufactured worldwide, an increase of nearly 9% compared to the same quarters in 2021. However, this was still around 5 million units less than pre-pandemic levels in 2019, as per the report of the European Automobile Manufacturers' Association (ACEA).

- However, the demand for the electric vehicle segment may likely increase the demand for aluminum alloys. The growing demand for lightweight components across several applications is anticipated to drive the market.

- As per the World Economic Forum (WEF), nearly 4.3 million new battery-powered EVs (BEVs) and plug-in hybrid electric vehicles (PHEVs) were sold globally in the first half of 2022. Additionally, BEV sales grew by around 75% on the year and PHEVs by 37%. Moreover, global electric car sales crossed the 5.7 million unit mark in the first eight months of 2022, and the market share of plug-in electric cars has increased to nearly 15%.

- Aluminum alloys are also used in airplanes because they are strong and don't weigh much.Reducing the weight of an airplane is a good way to save energy and cut down on fuel use, since a lighter plane needs less lift force and thrust to fly.

- The growing demand for commercial aircraft due to an increase in air passengers and air transport for trade operations has triggered manufacturing. It covers high-strength and lightweight aircraft that can carry heavy loads with efficient performance.

- According to Boeing's commercial outlook for 2022-2041, the North American region is predicted to cover around 22% of the global fleet at the end of the forecast period (2041). It is also anticipated that a total of 9,310 fleet deliveries will be made over the next two decades, with single-aisle accounting for almost 70% of the total deliveries in the region.

- Owing to all these factors, the market for metal magnesium is likely to grow globally during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is the biggest consumer of magnesium metal on the global market. Countries like China, India, and Japan use a lot of magnesium metal.

- Metal magnesium is mainly used in aluminum alloys, die-casting, iron and steel, metal reduction, and others. Moreover, aluminum alloys and die-casting have been increasingly used in the manufacturing of automotive parts, aerospace parts and equipment, and other end-user industries. The Asia-Pacific region has a significant global automotive, aerospace, and electronics market share.

- China being the largest manufacturer in the automotive industry, the market for magnesium in the country is predicted to rise at an exponential rate. According to the Chinese Association of Automotive Manufacturers (CAAM), China's automotive production increased by roughly 3.4% in 2022 compared to the previous year. In 2022, approximately 27 million automobiles will be produced, compared to 26.08 million units in 2021.

- The India Brand Equity Foundation (IBEF), in addition, forecasts that the Indian automotive industry will reach USD 300 billion by 2026.The report also stated that India's annual production of automobiles in FY22 was approximately 23 million units.

- During the forecast period, there is also likely to be strong growth in the demand for electric vehicles in China. This is because the country is changing quickly due to more government initiatives, more companies making electric cars, and more charging stations.

- China has been the biggest maker and buyer of electric cars, accounting for about half of the market around the world.According to the China Association of Automobile Manufacturers, the total production of new energy vehicles in China in 2022 was estimated to be about 7 million units. This saw a whooping increase of close to 97% when compared with the production of vehicles in 2021 (3.54 million units).

- Japan is also planning to transition to 100% electric car sales by 2035, and the Japanese electric vehicle market is growing. The United States companies may find business opportunities in various areas related to electric vehicles. Expansion of the electric vehicle market in the country is therefore projected to benefit market growth.

So, it's likely that all of the above factors will have a big effect on the demand for magnesium metal in the Asia-Pacific region in the future.

Metal Magnesium Industry Overview

The metal magnesium market is partially consolidated in nature. Some of the key players in the studied market include Nanjing Yunhai Special Metals Co. Ltd., Taiyuan Tongxiang Metal Magnesium Co. Ltd., Dead Sea Magnesium (ICL Group), Wenxi YinGuang Magnesium Industry (Group) Co. Ltd., and US Magnesium LLC, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Alloying with Other Metals

- 4.1.2 Increasing Demand for Lightweight Materials in the Aerospace and Automotive Industry

- 4.2 Restraints

- 4.2.1 Fluctuation in Prices of Metal

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 End-user Industry

- 5.1.1 Aluminum Alloys

- 5.1.2 Die-casting

- 5.1.3 Iron and Steel

- 5.1.4 Metal Reduction

- 5.1.5 Other End-user Industries

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 American Magnesium

- 6.4.2 Dead Sea Magnesium (ICL Group)

- 6.4.3 Fu Gu Yi De Magnesium Alloy Co. Ltd.

- 6.4.4 Nanjing Yunhai Special Metals Co. Ltd.

- 6.4.5 Regal Metal

- 6.4.6 Rima Industrial

- 6.4.7 Shanxi Bada Magnesium Co. Ltd.

- 6.4.8 Solikamsk Magnesium Works

- 6.4.9 Southern Magnesium & Chemicals Limited (SMCL)

- 6.4.10 Taiyuan Tongxiang Metal Magnesium Co. Ltd.

- 6.4.11 US Magnesium LLC

- 6.4.12 Wenxi Yinguang Magnesium Industry (group) Co. Ltd.

- 6.4.13 Western Magnesium Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Adoption of Electric Vehicles