|

市场调查报告书

商品编码

1910806

叶蜡石:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Pyrophyllite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

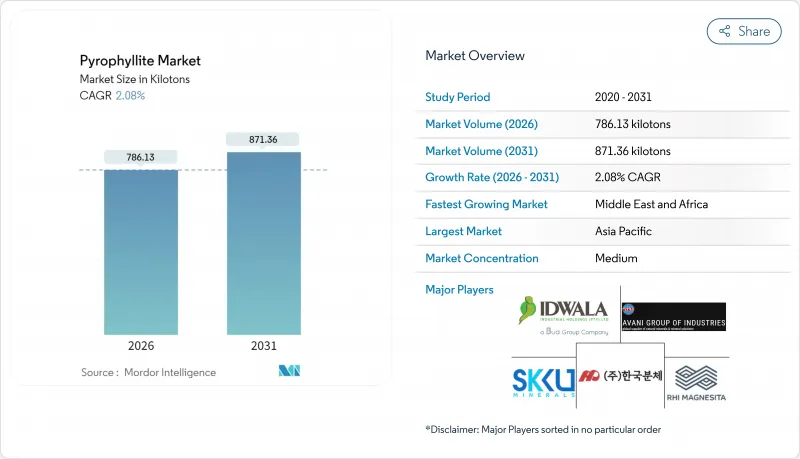

2025 年叶蜡石市场价值为 770.11 千吨,预计从 2026 年的 786.13 千吨增长到 2031 年的 871.36 千吨,在预测期(2026-2031 年)内复合年增长率为 2.08%。

这种稳定成长得益于该矿物可靠的物理特性,例如热稳定性、化学惰性和低收缩率,这些特性有助于工业用户维持产品品质的稳定性。亚太地区的需求成长是主要驱动力,该地区不断扩大的陶瓷产能和电弧炼钢製程维持了高产量水准。固态电池陶瓷和厚保护涂层是新的需求驱动因素,抵消了传统填料应用成长放缓的影响。对可吸入结晶质二氧化硅的监管力度加大推高了采矿成本,但也提高了品管标准,有利于资金雄厚且拥有先进抑尘技术的供应商。竞争整合,例如RHI Magnesita在2024年收购Resco Products,正在增强大型耐火材料买家的供应安全,并凸显叶蜡石市场作为战略材料平台的地位。

全球叶蜡石市场趋势与洞察

扩大亚太地区的陶瓷生产能力

中国和印度瓷砖及卫浴设备线的强劲扩张,透过大量吸收三轴瓷粉,推动了叶蜡石市场的发展。生产商指出,与高岭土基配方相比,叶蜡石强度提升高达24%,因此能够生产更轻的产品,并降低物流成本。更短的烧製週期进一步降低了能耗,减少了碳排放,符合区域脱碳政策的要求。随着政府奖励策略推动经济适用住宅需求的成长,瓷砖製造商正在签订远期合同,以可预测的条款购买叶蜡石,从而降低高岭土价格波动的风险。此外,叶蜡石能够可靠地热转化为莫来石,最大限度地减少釉药缺陷,从而支持生产高利润的高端瓷砖产品。这些结构优势使叶蜡石市场成为亚太陶瓷产业竞争力的重要组成部分。

电弧炼钢中耐火材料需求不断成长。

随着电炉炼钢粗钢比例的增加,钢包和中间包需要能够承受快速热循环的耐火材料。日本钢铁厂数十年来一直使用叶蜡石(日本国内俗称「硅藻土」),并已证实其在1600℃运作下具有形成莫来石的特性。印度和东南亚新建的电炉也采用了类似的材料规格,这促进了区域采购协议的达成。跨国耐火材料製造商正透过垂直整合来规避供应风险,例如2024年收购RHI Magnesia的美国资产。随着钢铁厂提高废钢熔炼量以减少范围1排放,叶蜡石市场从中受益,进一步巩固了其在耐火材料领域的领先地位。

职业粉尘危害法规

2024年,美国矿山安全与健康管理局(MSHA)将可吸入结晶质二氧化硅的允许浓度降低至50 μg/m³,并要求在浓度达到25 μg/m³时实施相应的应对措施。这带来了新的技术措施和健康监测要求。欧盟指令也随之调整,使得合规成为全球性挑战。升级通风系统、安装袋式除尘器以及实施符合ISO标准的监测都需要资本支出,这将影响利润率,尤其对于中型矿业公司而言。然而,大型矿业公司可以利用这些法规,透过第三方认证的「低粉尘」供应项目来脱颖而出,从而有可能扩大其在叶蜡石市场的份额。

细分市场分析

到2025年,天然级叶蜡石将占叶蜡石市场的86.64%,因为简单的破碎和分选流程使得交付成本经济实惠。位于拉贾斯坦邦和北卡罗来纳州的矿场是全球贸易的支柱,它们直接向耐火材料和陶瓷厂供应叶蜡石,分选工序极少。这些供应支撑着与宏观产业产量相符的基准成长。

加工后的「其他」等级矿石虽然总量较小,但预计到2031年,其复合年增长率将达到2.68%,超过天然等级矿石。生产商采用磁选、浮选和去离子水洗涤等工艺,将铁含量降低至0.4%以下(重量比),从而开拓了诸如半透明火星塞绝缘体和固体电解质框架等高端应用领域。微波焙烧结合湿式高强度磁选,可达到96%的除铁率,因此被电子製造商广泛采用。矿业公司正采用双产品策略,既要实现叶蜡石市场大宗商品部分的获利,又要获取特种矿石的利润,最终优化其收入结构。

叶蜡石市场报告按类型(天然叶蜡石、其他类型)、应用(陶瓷、耐火材料、填充材、玻璃纤维、橡胶和屋顶材料、肥料、装饰石材、其他应用)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行细分。市场预测以吨为单位。

区域分析

到2025年,亚太地区将占全球消费量的75.50%,这主要得益于中国、印度和日本完善的从矿山到窑炉的一体化供应链。光是印度一国就将生产约15万吨陶瓷,占全球总产量的24%至25%,为该地区的陶瓷产业丛集提供稳定的原料供应。中国瓷砖製造商占全球瓷砖出货量的一半,他们提前签订年度采购协议以确保运费优势。同时,日本正利用高纯度红木在连续铸造製程的特定耐火材料,凸显了该地区陶瓷应用的广泛性。

中东和非洲将成为成长最快的地区,到2031年年均复合成长率将达到2.74% 。波湾合作理事会的基础设施建设正在推动瓷砖需求,而北非的小型钢厂则指定使用当地耐火材料以减少对进口的依赖。南非和摩洛哥的矿产开发商正在勘探铝质片岩带,寻找新的矿床,旨在开发国内原料资源,从而重塑贸易流向,使其转向叶蜡石市场。

在北美,严格的联邦二氧化硅法规推高了合规成本,但也促使企业采用最佳可行控制技术,从而维持了适度成长。阿巴拉契亚地区的矿商受益接近性中西部钢铁客户的地理优势,而西海岸港口则为向亚洲出口高品质粉末提供了便利。欧洲专注于高价值工业陶瓷和特殊涂料,当地矿床纯度不足时,则从印度进口更高价值等级的产品。南美洲的潜力得益于巴西4,515.3万吨的滑石-叶蜡石蕴藏量,随着下游需求的成长,这可为未来建立国内矿物加工中心奠定基础。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚洲陶瓷产能扩张

- 电弧炼钢中耐火材料需求不断成长。

- 用于厚壁工业涂料的轻质矿物填料

- 石棉诉讼后,化妆品中滑石粉向叶蜡石的过渡

- 固态电池用陶瓷需要高纯度的铝和硅原料。

- 市场限制

- 职业粉尘危害法规

- 富含替代矿物(滑石、高岭土、长石)

- 低铁高铝矿体短缺

- 价值链分析

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型

- 天然叶蜡石

- 其他类型

- 透过使用

- 陶瓷

- 耐火材料

- 填充材(纸张、油漆、杀虫剂)

- 玻璃纤维

- 橡胶和屋顶材料

- 肥料(土壤改良剂)

- 装饰石材

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 埃及

- 奈及利亚

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Anand Talc

- Avani Group

- Hankook Mineral Powder Co. Ltd.

- Hebei Yayang Spodumene Co., Ltd.

- Idwala Industrial Holdings

- Jinhae Pyrophyllite

- Liaoyuan Pharmaceutical Co., Ltd.

- NINGBO INNO PHARMCHEM CO., LTD.

- PT Gunung Bale

- RT Vanderbilt Holding Company, Inc.

- RHI Magnesita

- SAMIROCK Company

- SEPRA

- SKKU Minerals

- Wonderstone

第七章 市场机会与未来展望

The Pyrophyllite Market was valued at 770.11 kilotons in 2025 and estimated to grow from 786.13 kilotons in 2026 to reach 871.36 kilotons by 2031, at a CAGR of 2.08% during the forecast period (2026-2031).

This steady expansion reflects the mineral's dependable physical attributes-thermal stability, chemical inertness, and low-shrinkage behavior-that help industrial users maintain reproducible product quality. Demand growth is anchored in Asia-Pacific, where ceramics capacity build-outs and electric-arc steelmaking together keep throughput volumes high. Solid-state battery ceramics and high-build protective coatings create incremental demand points that offset slower growth in legacy filler uses. Intensifying regulatory oversight of respirable crystalline silica raises mining costs, yet also elevates quality-control standards that favor well-capitalized suppliers with robust dust-mitigation technology. Competitive consolidation-illustrated by RHI Magnesita's 2024 purchase of Resco Products-reinforces supply security for large refractory buyers, underlining the pyrophyllite market's role as a strategic materials platform.

Global Pyrophyllite Market Trends and Insights

Ceramics Capacity Build-out in Asia-Pacific

Robust expansions in tile and sanitary-ware lines throughout China and India underpin the pyrophyllite market by absorbing large volumes into triaxial porcelain mixes. Producers cite up to 24% strength gains over kaolin-based recipes, enabling lighter-weight products that cut logistics costs. Shorter firing cycles further lower energy consumption and trim carbon footprints in line with regional decarbonization policies. As government stimulus pushes affordable housing, tile makers secure forward contracts that lock in pyrophyllite at predictable terms, shielding them from kaolin price swings. The mineral's predictable thermal conversion to mullite also minimizes glaze defects, supporting premium tile SKUs that command higher margins. These structural gains make the pyrophyllite market integral to Asia-Pacific's ceramic competitiveness.

Rising Refractory Demand in Electric-Arc Steelmaking

Electric-arc furnaces now account for a growing share of crude steel output, and each unit requires ladle and tundish refractories that resist rapid thermal cycling. Japanese steelmakers have relied on pyrophyllite (locally called roseki) for decades, validating its mullite-forming behavior under 1,600 °C service loads. New EAF rollouts across India and Southeast Asia replicate those material specifications, driving regional procurement contracts. Multinational refractory houses hedge supply risk through vertical integration, as seen in RHI Magnesita's 2024 U.S. asset acquisition. As steel mills intensify scrap melting to curtail Scope 1 emissions, the pyrophyllite market enjoys tailwinds that reinforce its refractory franchise.

Occupational Dust-Hazard Regulations

The U.S. Mine Safety and Health Administration in 2024 cut allowable respirable crystalline silica levels to 50 μg/m3 and mandated action at 25 μg/m3, triggering new engineering controls and medical surveillance obligations. European directives align closely, making compliance a global imperative. Upgrading ventilation, installing baghouse filters, and conducting ISO-compliant monitoring impose capital outlays that weigh on margins, especially for mid-tier miners. However, larger operators leverage these mandates to differentiate via third-party certified "low-dust" supply programs, potentially consolidating share within the pyrophyllite market.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight Mineral Fillers for High-Build Industrial Coatings

- Shift from Talc to Pyrophyllite in Cosmetics After Asbestos Litigation

- Abundant Substitute Minerals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural grades constituted 86.64% of the pyrophyllite market in 2025 on the strength of straightforward crushing-and-screening flowsheets that keep delivered-cost economics favorable. Rajasthan and North Carolina mines anchor global trade, supplying refractory and ceramic plants directly with minimal upgrading. These volumes underpin baseline growth that aligns with macro industrial output.

Processed "other" grades occupy a smaller base yet outpace natural grades at a 2.68% CAGR to 2031. Producers deploy magnetic separation, flotation, and de-ionized water washing to slash iron to below 0.4 wt%, unlocking advanced uses such as translucent spark-plug insulators and solid-state electrolyte frameworks. Microwave roasting coupled with wet-high-intensity magnetic separation achieves 96% iron removal, widening acceptance among electronics manufacturers. Dual-product strategies let miners monetize the pyrophyllite market's commodity tier while capturing specialty margins, ultimately strengthening their revenue mix.

The Pyrophyllite Market Report is Segmented by Type (Natural Pyrophyllite, Other Types), Application (Ceramics, Refractory, Filler Materials, Fiberglass, Rubber and Roofing, Fertilizers, Ornamental Stones, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific commanded 75.50% of 2025 consumption, underpinned by integrated mine-to-kiln supply chains in China, India, and Japan. India alone produced roughly 150,000 tons, equal to 24-25% of global output, conferring raw-material security to regional ceramics clusters. Chinese tile producers, accounting for half of world ceramic-tile shipments, front-load annual purchase contracts to lock in freight advantage. Concurrently, Japan leverages high-purity roseki for niche refractories in continuous-casting operations, underscoring the region's sophisticated application spectrum.

The Middle East and Africa is the fastest-growing geography at 2.74% CAGR through 2031. Gulf Cooperation Council infrastructure visions push tile demand, while North African steel mini-mills specify local refractory supply to cut import reliance. Mineral developers in South Africa and Morocco survey aluminous schist belts for new deposits, aiming to foster indigenous feedstock streams that could recalibrate trade flows into the pyrophyllite market.

North America sustains modest growth amid stringent federal silica rules that lift compliance costs but incentivize best-available-control-technology adoption. Appalachian operators bank on proximity to midwestern steel customers, whereas West-Coast ports facilitate Asian exports of upgraded powders. Europe focuses on high-margin technical ceramics and specialty coatings, importing value-added grades from India when local deposits lack required purity. South America's latent potential rests on Brazil's 45.153 million-ton talc-and-pyrophyllite reserve base, which underpins future domestic beneficiation hubs once downstream demand scales.

- Anand Talc

- Avani Group

- Hankook Mineral Powder Co. Ltd.

- Hebei Yayang Spodumene Co., Ltd.

- Idwala Industrial Holdings

- Jinhae Pyrophyllite

- Liaoyuan Pharmaceutical Co., Ltd.

- NINGBO INNO PHARMCHEM CO., LTD.

- PT Gunung Bale

- R.T. Vanderbilt Holding Company, Inc.

- RHI Magnesita

- SAMIROCK Company

- SEPRA

- SKKU Minerals

- Wonderstone

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ceramics capacity build-out in Asia

- 4.2.2 Rising refractory demand in electric-arc steelmaking

- 4.2.3 Lightweight mineral fillers for high-build industrial coatings

- 4.2.4 Shift from talc to pyrophyllite in cosmetics after asbestos litigation

- 4.2.5 Solid-state battery ceramics requiring high-purity Al-Si feedstocks

- 4.3 Market Restraints

- 4.3.1 Occupational dust-hazard regulations

- 4.3.2 Abundant substitute minerals (talc, kaolin, feldspar)

- 4.3.3 Scarcity of low-iron, high-Al2O3 ore bodies

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Natural Pyrophyllite

- 5.1.2 Other Types

- 5.2 By Application

- 5.2.1 Ceramics

- 5.2.2 Refractory

- 5.2.3 Filler Materials (Paper, Paints, Insecticides)

- 5.2.4 Fiberglass

- 5.2.5 Rubber and Roofing

- 5.2.6 Fertilizers (Soil Conditioners)

- 5.2.7 Ornamental Stones

- 5.2.8 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Anand Talc

- 6.4.2 Avani Group

- 6.4.3 Hankook Mineral Powder Co. Ltd.

- 6.4.4 Hebei Yayang Spodumene Co., Ltd.

- 6.4.5 Idwala Industrial Holdings

- 6.4.6 Jinhae Pyrophyllite

- 6.4.7 Liaoyuan Pharmaceutical Co., Ltd.

- 6.4.8 NINGBO INNO PHARMCHEM CO., LTD.

- 6.4.9 PT Gunung Bale

- 6.4.10 R.T. Vanderbilt Holding Company, Inc.

- 6.4.11 RHI Magnesita

- 6.4.12 SAMIROCK Company

- 6.4.13 SEPRA

- 6.4.14 SKKU Minerals

- 6.4.15 Wonderstone

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

滑石粉:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

滑石粉:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 日本滑石市场规模、份额、趋势和预测:按矿床类型、形态、最终用途行业和地区划分,2026-2034年

日本滑石市场规模、份额、趋势和预测:按矿床类型、形态、最终用途行业和地区划分,2026-2034年 2026年全球滑石市场报告

2026年全球滑石市场报告 超细滑石粉市场按等级、终端用途行业、应用和通路- 全球预测 2026-2032

超细滑石粉市场按等级、终端用途行业、应用和通路- 全球预测 2026-2032 叶蜡石市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2026-2033 年)

叶蜡石市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2026-2033 年) 滑石粉市场规模、份额和成长分析(按应用、等级、形态、通路、纯度和地区划分)-2026-2033年产业预测

滑石粉市场规模、份额和成长分析(按应用、等级、形态、通路、纯度和地区划分)-2026-2033年产业预测 超细滑石粉:全球市占率及排名、总收入及需求预测(2025-2031年)美国滑石粉市场规模、份额和趋势分析报告:按产品、应用和细分市场预测(2025-2033 年)滑石粉市场按应用、等级、形态、通路和纯度划分-2025-2032年全球预测

超细滑石粉:全球市占率及排名、总收入及需求预测(2025-2031年)美国滑石粉市场规模、份额和趋势分析报告:按产品、应用和细分市场预测(2025-2033 年)滑石粉市场按应用、等级、形态、通路和纯度划分-2025-2032年全球预测 滑石市场-全球产业规模、份额、趋势、机会和预测(按沉积类型、应用、地区和竞争细分,2020-2030 年)

滑石市场-全球产业规模、份额、趋势、机会和预测(按沉积类型、应用、地区和竞争细分,2020-2030 年)