|

市场调查报告书

商品编码

1445584

气体分离膜:市场占有率分析、产业趋势与统计、成长预测 (2024:2029)Gas Separation Membrane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

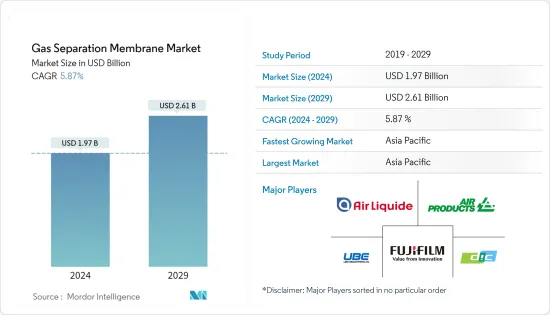

气体分离膜市场规模预计到2024年为19.7亿美元,预计到2029年将达到26.1亿美元,在预测期内(2024-2029年)增长5.87%,复合年增长率增长。

由于多个地区的严格封锁,COVID-19对石油天然气行业、製药行业和生物医疗医疗设备行业的整个供应链产生了重大影响,对气体分离膜市场产生了负面影响。然而,随着限制的取消,市场预计将随着时间的推移而加快步伐,并在预测期内继续成长。

主要亮点

- 推动市场研究的主要因素包括二氧化碳分离操作中对薄膜的需求不断增加以及政府对温室气体排放的严格监管。

- 相反,聚合物膜在高温应用中的塑化以及尺寸的增加和新膜的采用严重阻碍了市场的成长。

- 儘管如此,混合基质膜(MMM)和聚合物膜的发展及其应用的扩展预计将为相关市场带来新的可能性。

- 亚太地区是最大的市场,由于中国、印度和日本的需求不断增长,预计亚太地区将成为预测期内成长最快的市场。

气体分离膜市场趋势

制氮和富氧应用主导市场

- 氮气生产和富氧製程是化学工业的一个组成部分,用于分离所需产品和回收反应物。气体分离膜模组为商业和工业应用创建客自订化的富氮或富氧空气发生系统。

- 使用的主要薄膜类型之一是聚合物薄膜,它在环境温度或温暖温度下运作并产生富氧空气(25-50% 氧气)。也使用可以提供高纯度氧气(>90%)的陶瓷膜。然而,它需要800至900摄氏度左右的高温才能运作。

- 薄膜气体分离用于提供富氮气体取代空气来填充喷射客机的燃料箱,减少意外烧烫伤或爆炸的机会。氮气广泛用于哈伯法生产氨。然后氨用于各种化学合成以生产肥料。除此之外,氮气也用于包装和冷冻。

- 此外,当今世界,工业部门对氧气和氮气的需求很高,钢铁生产需要大量的氧气和氮气。目前,现有的碱性氧气炼钢每吨钢消耗近2吨氧气。因此,为了满足氧气需求,大多数钢厂都采用对工厂运作至关重要的气体分离模组。

- 根据世界钢铁协会的数据,2022年12月全球粗钢产量为1.407亿吨。 2022年全球粗钢总产量约18.78亿吨,较上年产量下降4%。然而,由于行业需求增加,预计 2023 年将出现正成长率,从而推动当前研究的市场。

- 近年来,医疗产业对氧气浓缩机的需求激增,尤其是在疫情期间。由于需求增加,一些製造商计划在世界各地扩建或开设更多工厂。例如,INOX Air Products Ltd 宣布于 2022 年 3 月建造印度最大的待开发区工厂。该厂将生产2,150吨/日工业气体,其中2,000吨/日气态氧、150吨/日液氧和1,200吨/日液态氧。氮气和氩气,流速为 100 TPD。

- 因此,制氮和富氧需求的增加将导致气体分离膜的需求激增,对市场产生正面影响。

亚太地区主导市场

- 由于该地区工业化程度的不断提高推动市场成长,预计亚太地区将成为气体分离膜最大且成长最快的市场。市场扩张主要是由于水库二氧化碳去除需求的增加、卫生和淡水需求的增加、都市化的加快和生活水准的提高而推动的。快速扩张和创新,加上产业整合,可能会推动区域市场的显着成长。

- 儘管如此,我国石油天然气产业是气体分离膜最重要的应用产业之一。过去二十年来,中国投资提高精製能力,以支持其不断扩张的经济。

- 此外,长期以来,中国各类原油的精製能力一直在稳步提高。根据能源调查(IEA),预计到年终,中国将拥有2000万桶精製能力,将增加未来几年对气体分离膜的需求。

- 此外,预计2022年中国原油产量约2.046亿吨,年增3%。根据中国国家统计局数据,2022年12月月度原油产量约1,700万吨,较去年同期成长2.5%。气体分离膜广泛应用于石油和天然气行业,从井口到石油回收和炼油厂,因此产品需求预计在不久的将来将激增。

- 印度拥有庞大的电力工业,由于人口成长、电气化程度提高和人均用电量增加,预计未来几年该电力工业将进一步扩张。根据印度品牌股权基金会(IBEF)统计,截至2022年10月31日,印度可再生能源装置容量(含水电)为165.94GW,占电力总装置容量的40.6%。

- 此外,增加使用气体分离膜来控制工业污水中的二氧化碳排放预计将产生正面的效果。政府加强控制气体排放的法规预计将增加未来对该产品的需求。

- 此外,该地区天然气产量的大幅增加可能会增加该地区市场对酸性气体分离中气体分离膜的需求。

气体分离膜产业概况

气体分离膜市场本质上是部分整合的,少数大型企业控制很大一部分市场。主要企业包括 Air Products and Chemicals, Inc.、UBE Corporation、Air Liquide Advanced Seperations、DIC Corporation 和 Fujifilm Corporation。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 二氧化碳分离过程对薄膜的需求不断增加

- 严格的政府温室气体排放标准

- 抑制因素

- 高温应用中聚合物膜的塑化

- 扩大规模并采用新膜

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章市场区隔

- 材料类型

- 聚酰亚胺和聚酰胺

- 聚砜

- 醋酸纤维素

- 其他材质类型

- 目的

- 制氮和富氧

- 氢气回收

- 二氧化碳移除

- 去除硫化氢

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争形势

- 併购、合资、合作与协议

- 市场排名分析

- 主要企业采取的策略

- 公司简介

- Air Liquide Advanced Separations

- Air Products and Chemicals Inc.

- DIC Corporation

- Evonik Industries AG

- Fujifilm Corporation

- Generon

- Honeywell International Inc.

- Linde PLC

- Membrane Technology and Research Inc.

- Parker Hannifin Corp.

- SLB(schlumberger)

- Toray Industries Inc.

- UBE Corporation

第七章市场机会与未来趋势

- 混合基质膜(MMM)的开发

- 高分子膜的开发及应用领域的拓展

The Gas Separation Membrane Market size is estimated at USD 1.97 billion in 2024, and is expected to reach USD 2.61 billion by 2029, growing at a CAGR of 5.87% during the forecast period (2024-2029).

COVID-19 had a significant impact on the entire supply chain of the oil and gas industry, pharmaceutical industry, and biomedical devices industry, owing to strict lockdowns in several regions and thus negatively impacting the market for gas separation membranes. However, with the lifting of restrictions, the market is expected to gain pace with time and continue to grow during the forecast period.

Key Highlights

- The primary factors driving the market study include the rising demand for membranes in carbon dioxide separation operations and stringent government regulations governing GHG emissions.

- On the contrary, the plasticization of polymeric membranes in high-temperature applications and the upscaling and adoption of new membranes have significantly hampered market growth.

- Nevertheless, the development of mixed matrix membranes (MMM) and polymeric membranes, as well as expanding applications, are projected to open new potential in the market under consideration.

- The Asia-Pacific region is the largest market and is predicted to be the fastest-growing market throughout the projection period, owing to rising demand in China, India, and Japan.

Gas Separation Membrane Market Trends

Nitrogen Generation and Oxygen Enrichment Application to Dominate the Market

- The processes of nitrogen generation and oxygen enrichment are integral parts of the chemical industry for the isolation of required products and the recovery of the reactants. The gas separation membrane modules build custom-made nitrogen or oxygen-enriched air generator systems for commercial and industrial applications.

- One major type of membrane used is polymeric, which operates at ambient or warm temperatures and may produce oxygen-enriched air (25-50% oxygen). Ceramic membranes are the other types used that may provide high-purity oxygen (90% or more). However, they require higher temperatures-around 800-900 degrees Celsius-to operate.

- Membrane gas separation is used to provide nitrogen-rich gases instead of air to fill jetliners' fuel tanks, reducing the likelihood of inadvertent burns and explosions. Nitrogen is widely utilized in the Haber process to produce ammonia. Ammonia is then employed in various chemical syntheses to produce fertilizers. Nitrogen is also used in packing and refrigeration, among other things.

- Furthermore, in today's world, oxygen and nitrogen are in high demand from the industrial sector, and large volumes are necessary for steel production. Nowadays, current basic oxygen steelmaking consumes almost 2 tons of oxygen for each ton of steel. As a result, to meet the requirement for oxygen, most steel factories employ gas separation modules, which are an essential aspect of plant operations.

- According to the World Steel Association, global crude steel production was 140.7 million tons (Mt) in December 2022. The total world crude steel production in 2022 was approximately 1,878 million tons, a 4% decrease compared to the production in the prior year. However, in 2023, it is expected to register a positive growth rate due to the increased demand in the industry, thereby driving the current studied market.

- The medical business has seen a surge in demand for oxygen concentrators in recent years, particularly during the pandemic era. With rising demand, several manufacturers intend to expand or open additional plants around the world. INOX Air Products Ltd, for example, announced in March 2022 the construction of India's largest greenfield plant, which will produce 2,150 tons per day (TPD) of industrial gases, including 2000 TPD of gaseous oxygen, 150 TPD of liquid oxygen, 1200 TPD of gaseous nitrogen, and 100 TPD of argon.

- Thus, the increased demand for nitrogen generation and oxygen enrichment will lead to an upsurge in the demand for the gas separation membrane and therefore positively affect the market.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to be the largest and fastest-growing market for gas separation membranes, owing to the region's increasing industrialization, which drives the market's growth. The market's expansion is primarily driven by rising demand for carbon dioxide removal from reservoirs, a rising need for sanitation and freshwater, increased urbanization, and higher living standards. Fast expansion and innovation, combined with industry consolidations, will likely drive significant growth in the region's market.

- Nonetheless, the oil and gas industry in China is one of the most important application industries for gas separation membranes. Over the last two decades, China has invested in increasing its refining capacity to support its expanding economy.

- Furthermore, for a long time, China has steadily increased its refining capacity for all types of crude. According to the Institute for Energy Research (IEA), China is expected to have 20 million barrels of refining capacity by the end of 2025, resulting in an increased need for gas separation membranes in the coming years.

- Furthermore, China's crude oil output in 2022 was estimated to be about 204.6 million tons, a 3% increase over the same period last year. According to the National Bureau of Statistics (NBS) of China, the monthly output of crude oil in December 2022 was approximately 17 million tons, a 2.5% rise over the same period last year. Because gas separation membranes are widely employed in the oil and gas industry, from the oil wellhead to oil recovery to the refinery, product demand will skyrocket in the near future.

- Even though India has a large power industry, the growing population, coupled with rising electrification and increasing per capita usage, will propel the industry's size in the upcoming years. According to the Indian Brand Equity Foundation (IBEF), as of October 31, 2022, India's installed renewable energy capacity (including hydro) stood at 165.94 GW, representing 40.6% of the overall installed power capacity.

- Additionally, the increasing use of gas separation membranes to control CO2 emissions from industrial effluents is expected to have a positive impact. Strengthening government regulations to curb gaseous emissions is expected to fuel the demand for the product in the future.

- Furthermore, the significant growth of natural gas production in the region may propel the demand for gas separation membranes in acid gas separation in the regional market.

Gas Separation Membrane Industry Overview

The gas separation membrane market is partially consolidated in nature, with a few major players dominating a significant portion of the market. Some of the major companies are Air Products and Chemicals, Inc., UBE Corporation, Air Liquide Advanced Seperations, DIC Corporation, Fujifilm Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Membranes in Carbon Dioxide Separation Processes

- 4.1.2 Strict Government Norms Toward GHG Emissions

- 4.2 Restraints

- 4.2.1 Plasticization of Polymeric Membranes in High-Temperature Applications

- 4.2.2 Upscaling and Adoption of New Membranes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material Type

- 5.1.1 Polyimide and Polyamide

- 5.1.2 Polysulfone

- 5.1.3 Cellulose Acetate

- 5.1.4 Other Material Types

- 5.2 Application

- 5.2.1 Nitrogen Generation and Oxygen Enrichment

- 5.2.2 Hydrogen Recovery

- 5.2.3 Carbon Dioxide Removal

- 5.2.4 Removal of Hydrogen Sulphide

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide Advanced Separations

- 6.4.2 Air Products and Chemicals Inc.

- 6.4.3 DIC Corporation

- 6.4.4 Evonik Industries AG

- 6.4.5 Fujifilm Corporation

- 6.4.6 Generon

- 6.4.7 Honeywell International Inc.

- 6.4.8 Linde PLC

- 6.4.9 Membrane Technology and Research Inc.

- 6.4.10 Parker Hannifin Corp.

- 6.4.11 SLB (schlumberger)

- 6.4.12 Toray Industries Inc.

- 6.4.13 UBE Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Mixed Matrix Membranes (MMM)

- 7.2 Development in Polymeric Membranes and Expanding Applications

气体分离膜市场:按材料、模组类型、应用和最终用途行业划分 - 2025-2030 年全球预测

气体分离膜市场:按材料、模组类型、应用和最终用途行业划分 - 2025-2030 年全球预测 气体分离膜市场机会、成长动力、产业趋势分析与预测 2024 - 2032

气体分离膜市场机会、成长动力、产业趋势分析与预测 2024 - 2032 全球气体分离膜市场:到 2033 年的机会与策略

全球气体分离膜市场:到 2033 年的机会与策略 2022-2032 年全球气体分离膜市场规模研究(按应用、材料类型、模组和区域预测)

2022-2032 年全球气体分离膜市场规模研究(按应用、材料类型、模组和区域预测) 气体分离膜市场:全球产业分析,规模,占有率,成长,趋势,预测,2024年~2033年

气体分离膜市场:全球产业分析,规模,占有率,成长,趋势,预测,2024年~2033年 气体分离膜市场规模、份额、趋势分析报告:按产品、最终用途、应用、地区和细分市场预测,2024-2030

气体分离膜市场规模、份额、趋势分析报告:按产品、最终用途、应用、地区和细分市场预测,2024-2030 气体分离膜市场 - 全球和区域分析:专注于应用、材料类型和模组 - 分析和预测,2024-2034 年

气体分离膜市场 - 全球和区域分析:专注于应用、材料类型和模组 - 分析和预测,2024-2034 年 气体分离膜市场、占有率、规模、趋势、产业分析报告:依材料、模组、应用、地区、细分市场预测,2024-2032

气体分离膜市场、占有率、规模、趋势、产业分析报告:依材料、模组、应用、地区、细分市场预测,2024-2032 全球气体分离膜市场:按模组、材料类型、应用、地区 - 预测至 2030 年

全球气体分离膜市场:按模组、材料类型、应用、地区 - 预测至 2030 年 2024年气体分离膜全球市场报告

2024年气体分离膜全球市场报告