|

市场调查报告书

商品编码

1690745

5G 设备 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)5G Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

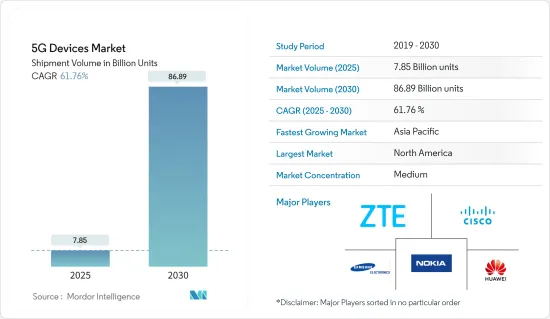

根据出货量计算,5G 设备市场规模预计将从 2025 年的 78.5 亿台扩大到 2030 年的 868.9 亿台,预测期间(2025-2030 年)的复合年增长率为 61.76%。

5G技术将提供超高速的网路覆盖,并藉助物联网实现许多新应用。新冠疫情也减缓了 5G 的推出。

关键亮点

- 根据爱立信消费者实验室去年的报告,去年 4 月至 7 月期间,他们对 37 个市场的 49,100 名客户进行了线上访谈。入选访谈的受访者代表了受访市场中的 17 亿网友和 4.3 亿 5G 用户,年龄从 15 岁到 69 岁不等。研究表明,下一波 5G 浪潮已经到来,早期采用者市场已经看到主流客户开始接受这项技术。

- 预计连接性、数位应用和可穿戴技术的日益普及将推动 5G 设备市场参与企业的成长。此外,升级现有的支援基础设施,包括数据机、塔和其他支援基础设施,对新参与企业来说是一个巨大的机会。 5G技术的采用在全球多个区域市场收到了正面的讯号,因此,5G设备市场的成长预计将带来巨大的机会。

- 各大晶片製造商也专注于开发5G设备组件,以促进这些设备在市场上的普及。这包括透过推出更多型号以供大众采用而在大众市场中竞争的晶片组供应商。去年 5 月,联发科推出了 Dimensity 1050 mmWave SoC 及相关型号,重点在于突出其设备中的 5G 连接功能。

- 此外,新的用例、经营模式和设备成本下降正在推动物联网的采用,从而导致全球连网设备和端点的数量增加。 5G 预计将提供海量机器通讯(mMTC),并支援数百亿台网路设备的无线连线。现代通讯系统已经支援多种 MTC 应用。然而,mMTC 的大量设备数量和微小有效载荷尺寸需要新的概念和方法。 5G 将实现每平方公里约 100 万台设备的密度。

- 然而,在许多地区,在全球范围内运作和安装支援基础设施仍然是一个重大障碍。例如,去年9月,国际标准组织3GPP更新了5G规范的下一个版本“Release 17”,该版本发布于前一年下半年。受疫情等因素影响,去年3月该版本发行暂停。这种延误会导致公司供应链和其他活动的后续延误。

- 新冠疫情的直接影响已波及各行各业,造成大规模裁员、失业率创历史新高,并严重抑制了消费者支出。新冠肺炎疫情的蔓延导致供应链严重中断,短期至中期阻碍了5G建设进程。因此,5G硬体将出现重大延迟,经济放缓将带来普遍影响。

5G设备市场趋势

智慧型手机市场预计将出现最高成长

- 根据爱立信2021年行动报告,全球将推出约650款新型5G智慧型手机,占所有5G机型的50%。智慧型手机提供的手持无线外形和 5G 存取的便利性几乎无与伦比。虽然全球多个地区已经开始推出 5G,但其他一些地区仍未推出 5G,它们正准备推出支援 5G 的智慧型手机,以利用即将到来的 5G 服务。

- 预计不断进步的技术以及对超高频宽、超低延迟和大规模连接的需求将为市场提供成长机会。此外,预计在预测期内,能源管理和智慧家庭产品等整合物联网 (IoT) 应用对高速资料连接的需求不断增长将推动 5G 智慧型手机的普及。

- 为了跟上竞争激烈的市场格局,一些智慧型手机製造商正在根据区域市场反应制定策略发布计划。去年 8 月,三星新一代 5G折迭式设备在不到 12 小时内的销售额就达到 60 亿印度卢比,随后三星共用在印度市场推出更多智慧型手机。该公司计划在明年印度推出 5G 之前推出该设备。

- 此外,市场参与企业正专注于为客户提供高阶 5G 智慧型手机体验。例如,高通去年 5 月发布了骁龙 8 Gen 1 SoC,其时脉速度高达 3.2GHz,可用于旗舰智慧型手机。处理器搭载第四代骁龙X65 5G Modem-RF系统,可达到高达10 Gbps的5G速度。

- 这项市场发展正在推动 5G 智慧型手机市场的发展,吸引买家升级其非 5G 智慧型手机,以获得最新、最快的全方位智慧型手机体验。

预计北美将占很大份额

- 该地区的服务供应商已经推出了商用5G服务,重点是行动宽频。支援所有三个频段的 5G 设备的推出将使该技术在该地区迅速普及。目前,5G 服务要么与 4G 服务集成,要么在客户从有 5G 服务的区域移动到没有 5G 服务的区域时进行 5G 到 4G 的切换。

- 根据爱立信2021年行动报告,2021年从4G到5G的过渡取得了显着进展,新增5G用户约6,400万。预计今年底5G用户数将达2.5亿,到2027年将达4亿,占行动用户的90%。

- 同样,北美的固定无线接入 (FWA) 用户数量增长最快,接受调查的服务供应商中近 60% 提供 FWA。此类区域性推出将有助于为5G部署提供基础设施支持,涵盖北美最大的新增用户区域。

- 最近已推出多款产品,实现了全部区域的5G 连线。诺基亚去年 9 月宣布,正在扩大其工业用户设备组合,以促进北美私人无线网路连接。其全新诺基亚 5G 工业现场路由器和加密狗、无线存取频谱功能和诺基亚连接营运仪表板为部署和管理安全可靠的私人 4G/LTE 和 5G 无线提供了更多选择。诺基亚的 5G 现场路由器和 5G 加密狗可部署在美国和加拿大的公民宽频无线电服务 (CBRS) 3.5GHz 频段。

5G设备产业概况

5G 设备市场竞争适中,由许多全球和地区参与企业组成。这些参与企业拥有相当大的市场占有率,并致力于扩大基本客群。供应商专注于研发投资,以推出新的解决方案、策略伙伴关係和其他有机和无机成长策略,从而获得竞争优势。

- 2022 年 9 月 - HMD Global 在德国柏林举行的 IFA 2022 上推出了拥有约 11 个 5G频宽的全新 5G 智慧型手机诺基亚 X30,以及其他几款诺基亚产品。

- 2022 年 8 月 - 巴帝电信 (Airtel) 宣布已与爱立信、诺基亚和三星签署 5G 网路合同,将于 2022 年 8 月开始推出 5G。与三星的合作将于 2022 年开始,与现有合作伙伴诺基亚和爱立信一起提供 5G 装置和解决方案。此次 5G伙伴关係是在印度电讯部举办的频谱竞标中,Airtel竞标并获得 900 MHz、1,800 MHz、2,100 MHz、3,300 MHz 和 26 GHz 的 19,867.8 MHZ 频谱之后建立的。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 市场定义和范围

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业相关人员分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 如何影响 5G 格局

第五章市场动态

- 市场驱动因素

- 全球设备和端点数量持续成长

- 组件和设备层面的技术创新推动采用

- 智慧型手机使用量的增加和智慧型手机技术的不断进步预计将推动市场

- 市场限制

- 缺乏监管和标准化

- 设计和营运挑战

- 市场机会

- 工业部门的需求预计将增加

- 继续努力在新兴国家引入5G

- 5G时间表和5G设备的采用

- 5G及未来

- 主要行业法规政策

第六章 技术简介

第七章 5G市场现状

- 全球通讯业者数量 - 试验和商业发布细分(2018 年第二季 - 第一季)

- 5G部署的国家覆盖范围—投资和商业化趋势

- 总行动通信基地台回程传输、宏蜂窝基地台和小型基地台基地台回程传输利用率(微波、卫星和 6 GHz 以下)

- 市场展望

第八章市场区隔

- 外形尺寸

- 模组

- CPE(室内/室外)

- 智慧型手机

- 热点

- 笔记型电脑

- 工业级 CPE/路由器/网关

- 其他外形尺寸

- 频谱支持

- 低于 6 GHz

- 毫米波

- 两个频谱带

- 地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 其他亚太地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 北美洲

第九章竞争格局

- 公司简介

- ZTE Corporation

- Cisco Systems Inc

- Nokia Corporation

- Huawei Technologies Co. Ltd

- Samsung Electronics Co. Ltd

- Xiaomi Corporation

- Motorola Mobility LLC(Lenovo Group Limited)

- BBK Electronics Corporation

- Keysight Technologies Inc.

第十章投资分析

第十一章 市场机会与未来趋势

The 5G Devices Market size in terms of shipment volume is expected to grow from 7.85 billion units in 2025 to 86.89 billion units by 2030, at a CAGR of 61.76% during the forecast period (2025-2030).

5G technology will offer ultra-high-speed network coverage and enable numerous new applications with the help of IoT. Also, the COVID-19 pandemic has delayed the widespread deployment of 5G.

Key Highlights

- According to the last year's Ericsson ConsumerLab report, Online interviews were conducted with 49,100 customers in 37 markets between April and July last year. The respondents chosen for the interview represent the surveyed markets' online population of 1.7 billion customers and 430 million 5G users, who range in age from 15 to 69. According to studies, the next wave of 5G is already in motion, with mainstream customers starting to accept the technology in early adopter markets.

- The growing adoption of connectivity, digital applications, and wearable technology is expected to drive growth for players in the 5G devices market. Moreover, upgrading existing supporting infrastructure, including modems, towers, and other supporting infrastructure, will present significant opportunities for new players. The 5G devices market's growth is expected to drive significant opportunities as the adoption of 5G technology has received positive signals in several local markets worldwide.

- Major chip makers also focus on 5G device component development to boost device penetration in the market. This includes chipset vendors competing in volume-driven markets as they introduce more models for mass deployments. In May last year, MediaTek launched Dimensity 1050 mmWave SoC, and related models, to highlight 5G connectivity in devices.

- Also, emerging applications, business models, and falling device costs have driven IoT adoption, increasing the number of connected devices and endpoints globally. 5G offers massive machine-type communication (mMTC), poised to support tens of billions of network-enabled devices to be wirelessly connected. Modern communication systems already serve several MTC applications. However, the characteristic properties of mMTC, i.e., the massive number of devices and the tiny payload sizes, require novel concepts and approaches. 5G allows a density of approximately one million devices per square kilometer.

- However, the global operation and installation of the supportive infrastructure continue to be a significant hurdle in many areas. For instance, in September last year, the international standardization body, 3GPP, updated the next release of the 5G specification, Release 17, for the second half of the previous year. The release was frozen in March last year due to the pandemic and other reasons. Such delays create subsequent delays in companies' supply chains and other operational activities.

- The COVID-19 pandemic's immediate effects have been felt in every industry, causing widespread layoffs, record unemployment, and severely curtailing consumer spending. The spread of COVID-19 resulted in a significant supply chain disruption impeding the 5G buildout process in the short & medium term. The critical 5G hardware delays and general effects of the economic slowdown thus apply.

5G Devices Market Trends

Smartphone Segment is Expected to Witness the Highest Growth

- According to the Ericsson Mobility Report 2021, around 650 new 5G smartphones have been launched globally, accounting for 50% of all the 5G from all form factors. The handheld wireless form factor and convenience of 5G access offered by smartphones are nearly unmatched. As several parts of the world have already begun rolling out 5G, some untouched regions are preparing to receive 5G-enabled smartphone launches to leverage the upcoming 5G launch.

- The increasing technological advancements and growing demand for ultra-high bandwidth, ultra-low latency, and massive connectivity are expected to offer growth opportunities to the market. Moreover, the rising demand for high-speed data connectivity for integrated IoT (Internet of Things) applications, such as energy management and smart home products, is anticipated to propel the adoption of 5G smartphones over the forecast period.

- Several smartphone manufacturers adapt and plan strategic launches according to the local market responses to compete in the highly competitive landscapes. In August last year, Samsung shared plans to launch more smartphones in the Indian market after recording sales of INR 600 crore in less than 12 hours for its new generation 5G-enabled foldable devices. The company would launch the devices ahead of the 5G roll-out in India in the previous year.

- Further, the market players focus on providing customers with a high-end 5G smartphone experience. For instance, in May last year, Qualcomm launched Snapdragon 8 Gen 1 SoC, with clock speeds up to 3.2 GHz for major smartphone implementation. The processor features the fourth-generation Snapdragon X65 5G Modem-RF System, bringing 5G speeds of up to 10 Gbps.

- Such developments attract buyers to upgrade their non-5G smartphones to get the latest and fastest, all-around experience in their smartphone, driving the 5G smartphone market.

North America Expected to Hold a Significant Share

- Service providers in the region have already launched commercial 5G services focused on mobile broadband. The introduction of 5G devices that support all three spectrum bands will enable early adoption of the technology in the region. As of now, 5G services are integrated with 4G services or with hand-off from 5G to 4G when a customer moves from an area where 5G service is available to one where it is not.

- According to the Ericson Mobility Report 2021, around 64 million 5G subscriptions were added in 2021 as migration from 4G to 5G subscriptions picked up significantly. The number of 5G subscriptions is expected to reach 250 million at the end of the current year and 400 million by 2027, accounting for 90 percent of mobile subscriptions.

- Similarly, the report also mentioned North America registering the strongest increase in the number of fixed wireless access (FWA), with about 60% of all service providers surveyed offering FWA. Such regional launches boost the infrastructural support for the 5G roll-out, reaching maximum areas in North America for new users.

- Multiple product launches have enabled 5G connectivity across the region recently. In September last year, Nokia announced extending its Industrial portfolio of user equipment to facilitate private wireless network connectivity in North America. Its new Nokia 5G Industrial fieldrouter and dongle, radio access spectrum capabilities, and Nokia Connectivity Operations Dashboard would provide more options for deploying and managing secure, reliable private 4G/LTE and 5G wireless. The Nokia 5G fieldrouter and 5G dongle could be deployed in the US and Canada Citizen Broadband Radio Service (CBRS) 3.5 GHz spectrum.

5G Devices Industry Overview

The 5G devices market is moderately competitive and consists of many global and regional players. These players account for a considerable market share and focus on expanding their customer base. The vendors focus on the research and development investment in introducing new solutions, strategic partnerships, and other organic & inorganic growth strategies to earn a competitive edge over their counterparts.

- September 2022 - HMD Global launched the new Nokia X30 5G smartphone and a few more Nokia products at IFA 2022 in Berlin, Germany, featuring around eleven 5G bands.

- August 2022 - Bharti Airtel (Airtel) announced signing 5G network agreements with Ericsson, Nokia, and Samsung to commence 5G deployment in August 2022. The partnership with Samsung to supply 5G equipment and solutions would begin in 2022, along with the older partners, Nokia and Ericsson. The 5G partnerships would follow closely on the edge of spectrum auctions conducted by the Department of Telecom in India, where Airtel bid for and acquired 19867.8 MHZ spectrum in 900 MHz, 1800 MHz, 2100 MHz, 3300 MHz, and 26 GHz frequencies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the 5G Landscape

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Sustained Increase in Number of Devices and Endpoints Worldwide

- 5.1.2 Technological Innovations at a Component and Device Level to Aid Adoption

- 5.1.3 Increasing use of Smart Phones and rising Technological advancement in the smart phones is expected to drive market.

- 5.2 Market Restraints

- 5.2.1 Regulatory and Standardization Delays

- 5.2.2 Design and Operational Challenges

- 5.3 Market Opportunities

- 5.3.1 Anticipated Rise in Demand from the Industrial Sector

- 5.3.2 Ongoing Efforts toward Introduction of 5G in Emerging Countries

- 5.4 5G Timeline and proliferation 5G enabled devices

- 5.5 5G and Beyond - The Path Ahead

- 5.6 Key Industry Regulations and Policies

6 TECHNOLOGY SNAPSHOT

7 5G ADOPTION MARKET LANDSCAPE

- 7.1 Number of Operators Worldwide - Breakdown by Trials and Commercial Launches (Q2'18 - Q1'20)

- 7.2 Country-level coverage on 5G Adoption - Investment and Commercialization Trends

- 7.3 Total Cell-site Backhaul, Macro, and Small Cell-site Backhaul Usage - In Percentage (Microwave, Satellite, Sub-6 GHz)

- 7.4 Market Outlook

8 MARKET SEGMENTATION

- 8.1 Form Factor

- 8.1.1 Modules

- 8.1.2 CPE (Indoor/Outdoor)

- 8.1.3 Smartphone

- 8.1.4 Hotspots

- 8.1.5 Laptops

- 8.1.6 Industrial Grade CPE/Router/Gateway

- 8.1.7 Other Form Factors

- 8.2 Spectrum Support

- 8.2.1 Sub-6 GHz

- 8.2.2 mmWave

- 8.2.3 Both Spectrum Bands

- 8.3 Geography

- 8.3.1 North America

- 8.3.1.1 United States

- 8.3.1.2 Canada

- 8.3.2 Europe

- 8.3.2.1 Germany

- 8.3.2.2 UK

- 8.3.2.3 France

- 8.3.2.4 Spain

- 8.3.2.5 Rest of Europe

- 8.3.3 Asia-Pacific

- 8.3.3.1 China

- 8.3.3.2 Japan

- 8.3.3.3 India

- 8.3.3.4 Australia

- 8.3.3.5 Rest of Asia-Pacific

- 8.3.4 Latin America

- 8.3.4.1 Brazil

- 8.3.4.2 Mexico

- 8.3.4.3 Argentina

- 8.3.4.4 Rest of Latin America

- 8.3.5 Middle East and Africa

- 8.3.5.1 UAE

- 8.3.5.2 Saudi Arabia

- 8.3.5.3 South Africa

- 8.3.5.4 Rest of Middle East and Africa

- 8.3.1 North America

9 COMPETITIVE LANDSCAPE

- 9.1 Company Profiles

- 9.1.1 ZTE Corporation

- 9.1.2 Cisco Systems Inc

- 9.1.3 Nokia Corporation

- 9.1.4 Huawei Technologies Co. Ltd

- 9.1.5 Samsung Electronics Co. Ltd

- 9.1.6 Xiaomi Corporation

- 9.1.7 Motorola Mobility LLC (Lenovo Group Limited)

- 9.1.8 BBK Electronics Corporation

- 9.1.9 Keysight Technologies Inc.

10 INVESTMENT ANALYSIS

11 MARKET OPPORTUNITIES AND FUTURE TRENDS

5G设备市场规模、份额和成长分析(按部署模式、垂直产业、应用和地区划分)-产业预测,2026-2033年

5G设备市场规模、份额和成长分析(按部署模式、垂直产业、应用和地区划分)-产业预测,2026-2033年 5G设备测试市场规模、份额和成长分析(按设备类型、最终用户和地区划分)-产业预测(2026-2033年)

5G设备测试市场规模、份额和成长分析(按设备类型、最终用户和地区划分)-产业预测(2026-2033年) 5G-Advanced 行动装置、穿戴式装置和配件5G 行动装置、功能与技术:厂商、趋势与预测市场数据概览(2025 年第四季)5G 行动装置、功能和技术:供应商、趋势和预测5G 行动装置厂商市场占有率5G晶片市场及厂商占有率5G-Advanced:市场发展与机会

5G-Advanced 行动装置、穿戴式装置和配件5G 行动装置、功能与技术:厂商、趋势与预测市场数据概览(2025 年第四季)5G 行动装置、功能和技术:供应商、趋势和预测5G 行动装置厂商市场占有率5G晶片市场及厂商占有率5G-Advanced:市场发展与机会 2025年5G设备测试全球市场报告

2025年5G设备测试全球市场报告 Micron:停止未来行动 NAND 快闪记忆体开发,专注于高利润领域

Micron:停止未来行动 NAND 快闪记忆体开发,专注于高利润领域