|

市场调查报告书

商品编码

1445868

燃气引擎:市场占有率分析、行业趋势和统计、成长预测(2024-2029)Gas Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

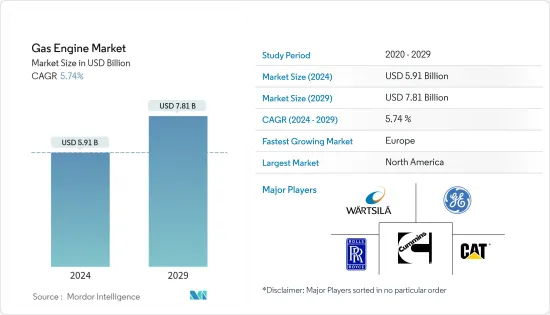

燃气引擎市场规模预计2024年为59.1亿美元,预计到2029年将达到78.1亿美元,在预测期内(2024-2029年)复合年增长率为5.74%增长。

主要亮点

- 从中期来看,燃气引擎市场主要受到全球天然气的大量供应以及发电和汽车行业对无排放气体燃料系统的需求的推动。

- 另一方面,再生能源来源的成长趋势正在阻碍燃气引擎的未来繁荣。

- 儘管如此,生产更好版本燃气引擎的技术进步正在为市场发展创造充足的机会。近日,德国曼恩能源解决方案发动机公司在纽伦堡沼气会议及贸易博览会上首次展示了其新型曼恩E3872燃气引擎系列。该发动机设计为四衝程火花点火式燃气引擎,排气量为29.6升,缸径为138毫米,衝程为165毫米。光是 12 个汽缸,效率就提高了 44%。

燃气引擎市场趋势

电力公共事业预计将显着成长

- 电力公共事业更喜欢燃气引擎来提供基本电力负载。此外,使用燃气引擎发电机被认为对于应对尖峰负载需求非常有用。世界各地的一些电力公共事业正面临尖峰负载需求的突然激增,特别是在早上和晚上。

- 在全球发电结构中,天然气发电仅次于煤炭。 2022年发电量为6,631.39TWh,约占总发电量的23%。如此大规模引入燃气引擎的最显着原因是电力产业的脱碳。许多天然气发电工程正在被添加到全球发电组合中。

- 据全球能源监测机构称,截至2022年,全球有超过600吉瓦的天然气发电厂处于开发阶段,其中160吉瓦已建成。

- 2022 年 1 月,瓦锡兰宣布从泰米尔纳德邦石油产品有限公司 (TPL)订单两台 34SG燃气引擎,用于印度清奈的一座 15.5 兆瓦自备发电厂。

- 2023年10月,济能(舟山)燃气发电有限公司与哈尔滨电力公司合作,向GE Vernova订购了两台9HA.02复合迴圈燃气涡轮机。中国国营电力公共事业祖农(舟山)燃气发电有限公司宣布在群岛最大的岛屿舟山开始建造一座新的复合迴圈发电厂。该发电厂预计将于年终年底投入运营,预计将为舟山市提供总计总合1.7 吉瓦 (GW) 的电力。 9HA.02 DLN2.6e 燃烧系统设计为使用高达 50% 体积的氢气运行,大大超出了工厂最初的使用高达 10% 氢气的目标。

- 由于这些类型的发展,预计电力业务部门在预测期内将在燃气引擎系统的所有应用中占据重要份额。

欧洲预计将出现显着成长

- 欧洲地区在大规模部署各种应用的燃气引擎方面具有最大的潜力。旨在向绿色能源转型的政府政策成为市场成长的催化剂,因为基于氢和天然气的技术可实现无排放气体环境。

- 此外,该地区行业领先公司的存在正在推动燃气引擎行业的进一步技术发展。许多公司正在推出更好的燃气引擎系统,为新应用提供更多的多功能性。

- 2023 年 4 月,Clark Energy 收到订单,为 VPI 在伊明翰能源中心的扩建设施交付50MW 氢动力 INNIO Jenbacher燃气引擎。 Clarke Energy 安装的 50MW 燃气往復式调峰设施计划于明年初投入运行,299MW 开式循环燃气涡轮机(OCGT) 计划于 2025 年夏季投入运行,从而提高对能源成功至关重要的容量的 VPI。投资。

- 2023 年 1 月,罗尔斯·罗伊斯宣布已成功测试使用 100% 氢燃料的 MTU 系列 4000 L64 引擎的 12 缸燃气版本。该公司表示,在其动力系统业务部门进行的测试中,该引擎在效率、性能、排放气体和燃烧方面表现出优异的特性。

- 预计这些发展将使欧洲地区成为预测期内的市场王牌。

燃气引擎产业概况

燃气引擎市场是半集成的。该市场的主要企业包括(排名不分先后)通用电气公司、瓦锡兰公司、劳斯莱斯控股公司、卡特彼勒和康明斯公司。

康明斯声称与各种独立引擎製造商和发电机组组装以及为其产品製造引擎的原始设备OEM进行良性竞争。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 调查先决条件

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 2028 年之前的市场规模与需求预测(十亿美元)

- 最新趋势和发展

- 政府政策法规

- 市场动态

- 促进因素

- 各最终用户产业的天然气系统供应和消耗增加

- 全球实施更严格的废气法规

- 抑制因素

- 对可再生资源的兴趣日益浓厚

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 最终用户

- 电力公共事业

- 车

- 船

- 产业

- 其他的

- 汽油种类

- 天然气

- 氢

- 其他的

- 地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 法国

- 英国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲

- 北美洲

第六章 竞争形势

- 併购、合资、合作与协议

- 主要企业采取的策略

- 公司简介

- Caterpillar Inc.

- Cummins Inc.

- Siemens AG

- Rolls-Royce Holdings PLC

- Wartsila Oyj Abp

- Mitsubishi Heavy Industries Ltd

- Hyundai Heavy Industries Co. Ltd

- Man SE

- General Electric Company

- Kawasaki Heavy Industries Ltd

- JFE Engineering Corporation

- Liebherr Group

第七章市场机会与未来趋势

The Gas Engine Market size is estimated at USD 5.91 billion in 2024, and is expected to reach USD 7.81 billion by 2029, growing at a CAGR of 5.74% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, the gas engine market is largely driven by high natural gas supply at the global level and the demand for the emissions-free fuel system in the power generation and automotive sector.

- On the other hand, the thriving future of gas engines is thwarted by the growing inclination towards renewable sources of energy.

- Nevertheless, the technical advancements to produce the better versions of gas engines create ample opportunities for market development. Recently, the German company MAN Energy Solutions Engines introduced a new MAN E3872 gas-engine series for the first time at Biogas Convention & Trade Fair in Nuremberg. It is designed as a four-stroke spark-ignition gas engine with a displacement of 29.6 liters, a bore of 138mm, and a stroke of 165mm. It has 44% greater efficiency from just 12 cylinders.

Gas Engine Market Trends

Power Utilities Expected to Witness Significant Growth

- Electric Utilities prefer gas engines to serve base electrical loads. In addition, the use of gas engine generators is also considered highly useful for handling peak load demand. Several utilities worldwide have faced a rapid spike in the peak load demand, especially during the morning and evening time periods.

- Natural gas-based power generation stands at second place in the global electricity generation mix, after coal. The output was recorded as 6631.39 TWh in 2022, making around 23% of total power generation. The most highlighted reason for such a huge deployment of gas-based engines was the decarbonization of the power sector. Many gas-to-power projects are still on the way to be added to the global power generation portfolio.

- According to global energy monitor, over 600 gigawatts of natural gas power plants are in the development stage worldwide as of 2022, of which 160 gigawatts have already been constructed.

- In Nomeber 2022, Wartsila announced to receive order for two 34SG gas engines by the Tamilnadu Petroproducts Limited (TPL) for 15.5 MW captive power plant in Chennai, India.

- In October 2023, Jineng (Zhoushan) Gas Power Generation Co. placed an order with GE Vernova for two of its 9HA.02 combined-cycle gas turbines in collaboration with Harbin Electric Corporation. China's state-owned utility Jineng (Zhoushan) Gas Power Generation Co. announced starting construction of a new combined-cycle power plant on Zhoushan, the archipelago's largest island. Scheduled to begin operations by the end of 2025, the plant is expected to deliver a total of nearly 1.7 gigawatts (GW) of electricity for Zhoushan. The 9HA.02 DLN2.6e combustion system is designed to operate on up to 50% hydrogen by volume, well above the plant's initial goal to operate on up to 10% hydrogen.

- Owing to such kind of developments, the power utility segment is expected to have a significant share among all the applications of gas engine systems during the forecast period.

Europe Expected to Have a Significant Growth

- The European region has the maximum potential to allow high deployment of gas engines in various applications. The government policies to have a greener energy transition act as a catalyst for the growth of the market, as hydrogen and natural-gas-based technologies render an emission-free environment.

- Furthermore, the presence of industry-leading companies in the region propels a higher techno-growth of the gas engine industry. Many companies have come out with better gas engine systems with more versatility for new applications.

- In April 2023, Clarke Energy recieved order to deliver 50MW of hydrogen ready INNIO Jenbacher gas engines to VPI's expansion at Immingham energy hub. A 50MW gas reciprocating peaking facility installed by Clarke Energy, scheduled to begin operation early next year, and a 299MW open cycle gas turbine (OCGT), scheduled to begin operation by summer 2025, represent VPI's investment in capacity essential to the success of the energy transition.

- In January 2023, Rolls-Royce announced that it had conducted successful tests of a 12-cylinder gas variant of the mtu Series 4000 L64 engine running on 100% hydrogen fuel. In the tests carried out by the Power Systems business unit, the company stated that the engine showed excellent characteristics in terms of efficiency, performance, emissions, and combustion.

- Owing to such developments, the European region is expected to ace the market during the forecast period.

Gas Engine Industry Overview

The gas engine market is semi-consolidated. The key players in this market include (in not particula order) General Electric Company, Wartsila Oyj Abp, Rolls-Royce Holdings PLC, Caterpillar Inc., and Cummins Inc., among others.

Cummins Inc claims to participate in healthy competition with a variety of independent engine manufacturers and generator set assemblers as well as OEMs who manufacture engines for their own products. Some of the company's major competitors in the region include CAT, MTU (Rolls Royce Power Systems Group) and Kohler/SDMO (Kohler Group), Generac, Mitsubishi Heavy Industries (MHI), etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Supply and Consumption of Gas-based Systems in Various End-user Industry

- 4.5.1.2 Implementation of stricter emission regulations worldwide

- 4.5.2 Restraints

- 4.5.2.1 Growing Inclination towards Renewable Sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End-User

- 5.1.1 Power Utilities

- 5.1.2 Automotive

- 5.1.3 Marine

- 5.1.4 Industrial

- 5.1.5 Others

- 5.2 Fuel Type

- 5.2.1 Natural Gas

- 5.2.2 Hydrogen

- 5.2.3 Other Fuel Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Cummins Inc.

- 6.3.3 Siemens AG

- 6.3.4 Rolls-Royce Holdings PLC

- 6.3.5 Wartsila Oyj Abp

- 6.3.6 Mitsubishi Heavy Industries Ltd

- 6.3.7 Hyundai Heavy Industries Co. Ltd

- 6.3.8 Man SE

- 6.3.9 General Electric Company

- 6.3.10 Kawasaki Heavy Industries Ltd

- 6.3.11 JFE Engineering Corporation

- 6.3.12 Liebherr Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Technical Advancements to Produce the Better Versions of Gas Engines

全球燃气引擎市场(按应用、燃料类型、额定功率和发动机类型)预测(2025-2032 年)

全球燃气引擎市场(按应用、燃料类型、额定功率和发动机类型)预测(2025-2032 年) 2025年燃气引擎全球市场报告

2025年燃气引擎全球市场报告 2025 年至 2033 年燃气发动机市场报告(按燃料类型、功率输出、应用、产业垂直和地区划分)

2025 年至 2033 年燃气发动机市场报告(按燃料类型、功率输出、应用、产业垂直和地区划分) 燃气引擎市场规模、份额、增长分析,按燃料类型、按产量、按应用、按最终用途、按地区 - 按行业预测,2024-2031 年

燃气引擎市场规模、份额、增长分析,按燃料类型、按产量、按应用、按最终用途、按地区 - 按行业预测,2024-2031 年 全球燃气发动机市场规模(按功率输出、燃料类型、应用、地区、范围和预测)

全球燃气发动机市场规模(按功率输出、燃料类型、应用、地区、范围和预测) 2030 年燃气引擎市场预测:按发动机类型、燃料类型、技术、应用、最终用户和地区进行的全球分析

2030 年燃气引擎市场预测:按发动机类型、燃料类型、技术、应用、最终用户和地区进行的全球分析 2024-2028年全球燃气引擎市场

2024-2028年全球燃气引擎市场 全球燃气引擎市场:按燃料类型(天然气/特殊气体)、产量、最终用户(发电、热电汽电共生、机械驱动)、最终用户行业和地区 - 预测(截至 2029 年)

全球燃气引擎市场:按燃料类型(天然气/特殊气体)、产量、最终用户(发电、热电汽电共生、机械驱动)、最终用户行业和地区 - 预测(截至 2029 年) 全球燃气发动机市场:~2030 年

全球燃气发动机市场:~2030 年