|

市场调查报告书

商品编码

1445936

粉尘控制系统和抑制化学品 - 市场份额分析、行业趋势与统计、成长预测(2024 - 2029 年)Dust Control Systems And Suppression Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

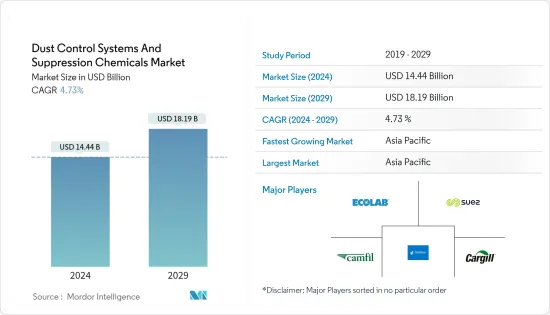

粉尘控制系统和抑尘化学品市场规模预计到 2024 年为 144.4 亿美元,预计到 2029 年将达到 181.9 亿美元,在预测期(2024-2029 年)CAGR为 4.73%。

COVID-19 大流行对市场产生了负面影响。然而,市场已达到疫情前的水平,预计在预测期内将稳定成长。

主要亮点

- 短期内,推动市场成长的主要因素是亚太地区建筑和基础设施的成长以及监管合规性的提高。

- 食品和製药行业的除尘问题预计将阻碍市场的成长。

- 亚太地区主导了全球市场,最大的消费来自中国和印度。

粉尘控制系统和抑制化学品市场趋势

建筑业主导市场

- 粉尘控制措施适用于任何可能因粉尘穿过景观或空气而造成空气和水污染的建筑工地。

- 根据HSE统计(英国政府健康与安全执行局统计),全球每年有超过500名建筑工人因接触硅尘而死亡。因此,监管有害粉尘排放变得非常重要,在过去几年中对粉尘控制系统和抑制化学物质产生了巨大的需求。

- 与传统工艺相比,抑尘解决方案为建筑应用提供了明显的优势和丰厚的效益,包括在极端气候条件下的简单应用和长效保护。

- 目前,最先进的粉尘控制解决方案可以解决建筑工地和所有类型道路的一系列粉尘控制问题,从主要公路和高速公路到运输、工业和农村道路、停机坪、硬地区域和防水路面。

- 氯化钙是建筑业使用的主要抑尘化学品。此外,建筑业使用聚合物乳液来稳定运输和通路。

- 美国拥有庞大的建筑业,僱用了超过 760 万名员工。根据美国人口普查局的数据,2022 年建筑业价值为 17,929 亿美元,比 2021 年的 16,264 亿美元增长 10.2%。

- 此外,根据美国人口普查局的进一步统计,2022年美国新建建筑年价值为16,575.90亿美元,而2021年为14,998.22亿美元。此外,美国每年的住宅建设量为2022 年,该国非住宅建筑年价值为8,491.64 亿美元,而2021 年为7,406.45 亿美元。2022 年,该国非住宅建筑年价值为8,084.27 亿美元,而2021 年为7,591.77 亿美元,从而减少了短期内研究市场消费情况。

- 此外,越来越多的外国公司在亚太地区存在,创造了对新办公室、建筑物、生产厂房等的需求,从而推动了该地区的建筑业。

- 这些因素可能有助于建筑业主导市场。

中国将主导亚太市场

- 中国建筑业正经历恆大债务危机,预计未来一段时间将会下滑。

- 过去几年,中国一直致力于减少煤炭消耗,主要是出于环境问题和气候目标。

- 政府采取这项措施是为了应对由于国内产量减少而导致该国煤炭进口增加的情况。

- 国家新批煤矿分布在新疆、内蒙古、山西、陕西等地区,是国家煤炭基地建设策略的支撑。

- 这些新矿井计划用于扩建现有煤矿。预计该国对开发和营运此类新矿山的粉尘控制系统和抑制化学品的需求将会很高。

- 该国的人口结构预计将有利于住房和商业建筑活动。不断增长的人口引发了公共和私营部门对经济适用住宅区的投资。中国政府已主动向40个重点城市赠送650万套政府补贴租赁住房,预计可容纳约1,300万人。

- 此外,中国政府还推出了大规模的建设计划,其中包括为未来十年内2.5亿农村人口向新的特大城市转移作出规定,为未来建筑材料在建筑施工中的各种应用创造了广阔的空间增强建筑性能的活动。香港房屋当局推出多项措施推动廉租房建设。官员的目标是在 2030 年之前的 10 年内提供 301,000 套公共住宅。这些因素预计将促进该国的建筑业发展,从而可能支持未来所研究的市场需求。

- 因此,各种最终用户行业的成长正在推动各种应用的粉尘控制系统和抑制化学品的需求。

粉尘控制系统和抑制化学品行业概述

抑尘化学品市场由极少数参与者部分整合。其他一些抑尘系统市场的知名企业包括嘉吉公司、SUEZ、Ecolab、Camfil 和 Donaldson Company Inc.(排名不分先后)。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 司机

- 亚太地区建筑和基础设施的成长

- 提高监理合规性

- 其他司机

- 限制

- 食品医药产业的除尘问题

- 其他限制

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争激烈程度

第 5 章:市场区隔(市场价值规模)

- 化学类型

- 木质素磺酸盐

- 氯化钙

- 氯化镁

- 沥青乳液

- 油乳液

- 聚合物乳液

- 其他化学品类型

- 系统类型

- 干采

- 湿式抑制

- 最终用户产业

- 矿业

- 建造

- 食品与饮品

- 石油天然气和石化

- 製药

- 其他最终用户产业

- 地理

- 亚太

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太

第 6 章:竞争格局

- 併购、合资、合作与协议

- 市占率(%)**/排名分析

- 领先企业采取的策略

- 公司简介

- Chemical Providers

- ADM

- Benetech Inc.

- Borregaard

- Cargill Incorporated

- Chemtex Speciality Limited

- Evonik Industries AG

- GelTech Solutions

- Hexion

- Quaker Houghton (Quaker Chemical Corporation)

- Shaw Almex Industries Ltd

- SUEZ

- Ecolab

- System Providers

- BossTek

- Camfil

- CW Machine Worx

- Donaldson Company Inc.

- DSH Systems Ltd

- Duztech AB

- Nederman Holding AB

- SLY Inc.

- The ACT Group

- Chemical Providers

第 7 章:市场机会与未来趋势

- 增加对化工产业的投资

- 绿色粉尘治理产品的出现

The Dust Control Systems And Suppression Chemicals Market size is estimated at USD 14.44 billion in 2024, and is expected to reach USD 18.19 billion by 2029, growing at a CAGR of 4.73% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the market. However, the market is reaching pre-pandemic levels and is expected to grow steadily during the forecast period.

Key Highlights

- Over the short term, the major factors driving the growth of the market are the growth in construction and infrastructure in Asia-Pacific and the increasing regulatory compliances.

- Dust collection problems in the food and pharmaceutical industry are expected to hinder the market's growth.

- Asia-Pacific dominated the market worldwide, with the largest consumption coming from China and India.

Dust Control Systems & Suppression Chemicals Market Trends

Construction Industry to Dominate the Market

- Dust control measures are applicable to any construction site with potential air and water pollution from dust traveling across the landscape or through the air.

- According to HSE statistics (the U.K. government's Health and Safety Executive statistics), every year, more than 500 construction workers die from exposure to silica dust worldwide. Hence, it became important to regulate hazardous dust emissions, creating a significant demand for dust control systems and suppression chemicals over the last few years.

- Compared to conventional processes, dust suppression solutions offer distinct advantages and lucrative benefits for construction applications, including easy application and long-life protection during extreme climatic conditions.

- Currently, there are state-of-the-art dust control solutions that can solve a range of dust control problems at construction sites and on all types of roads, from major highways and freeways to haulage, industrial, and rural roads, tarmacs, hardstand areas, and water-repellent pavements.

- Calcium chloride is the major dust control suppression chemical used in the construction industry. In addition, the construction industry uses polymer emulsions for stabilizing haul and access roads.

- The United States boasts a colossal construction sector that employs over 7.6 million employees. According to U.S. Census Bureau, in 2022, the value of construction was USD 1,792.9 billion, a 10.2% increase over the USD 1,626.4 billion spent in 2021.

- Further, as per further statistics generated by the U.S. Census Bureau, the annual value for new construction in the United States accounted for USD 1,657,590 million in 2022, compared to USD 1,499,822 million in 2021. Moreover, the annual residential construction in the United States was valued at USD 849,164 million in 2022, compared to USD 740,645 million in 2021. The annual value of non-residential construction put in place in the country was valued at USD 808,427 million in 2022, compared to USD 759,177 million in 2021, thereby decreasing the consumption of the market studied in the short term.

- Moreover, the increasing presence of foreign companies in the Asia-Pacific region has created a demand for new offices, buildings, production houses, etc., thereby driving the construction sector in the region.

- Such factors are likely to help the construction industry dominate the market.

China to Dominate the Asia-Pacific Market

- China's construction industry has been going through the Evergrande debt crisis, and it is expected to decline for a short while in the future.

- The country has been focusing on reducing coal consumption for the past few years, mainly due to environmental concerns and climate goals.

- The government took this step in accordance with the growing coal imports of the country due to the reduction in domestic production.

- The new coal mines approved in the country are located in the regions of Xinjiang, Inner Mongolia, Shanxi, and Shaanxi, supported by the national strategy toward consolidating the output at dedicated coal production bases.

- These new mines are planned for the expansion of the existing collieries. The country is expected to witness high demand for dust control systems and suppression chemicals for developing and operating such new mines.

- The country's demographics are expected to favor housing and commercial construction activities. The growing population has triggered investments in affordable residential colonies by the public and private sectors. China's government has taken the initiative to gift 40 key cities with 6.5 million government-subsidized rental homes that are supposed to accommodate around 13 million people.

- Additionally, the Chinese government has rolled out massive construction plans, which include making provisions for the movement of 250 million rural people to its new megacities over the next ten years, creating a major scope for construction materials used in the future in various applications during construction activities to enhance the building properties. The housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units in 10 years till 2030. These factors are expected to raise the construction industry in the country and thereby are likely to support the demand for the market studied in the future.

- Thus, growth in various end-user industries is boosting the demand for dust control systems and suppression chemicals for various applications.

Dust Control Systems & Suppression Chemicals Industry Overview

The dust suppression chemicals market is partially consolidated among very few players. Some of the other prominent players in the dust suppression systems market include Cargill Incorporated, SUEZ, Ecolab, Camfil, and Donaldson Company Inc. (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growth in Construction and Infrastructure in Asia-Pacific

- 4.1.2 Increase in Regulatory Compliances

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Dust Collection Problems in Food and Pharmaceutical Industry

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Chemical Type

- 5.1.1 Lignin Sulfonate

- 5.1.2 Calcium Chloride

- 5.1.3 Magnesium Chloride

- 5.1.4 Asphalt Emulsions

- 5.1.5 Oil Emulsions

- 5.1.6 Polymeric Emulsions

- 5.1.7 Other Chemical Types

- 5.2 System Type

- 5.2.1 Dry Collection

- 5.2.2 Wet Suppression

- 5.3 End-user Industry

- 5.3.1 Mining

- 5.3.2 Construction

- 5.3.3 Food and Beverage

- 5.3.4 Oil and Gas and Petrochemical

- 5.3.5 Pharmaceutical

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chemical Providers

- 6.4.1.1 ADM

- 6.4.1.2 Benetech Inc.

- 6.4.1.3 Borregaard

- 6.4.1.4 Cargill Incorporated

- 6.4.1.5 Chemtex Speciality Limited

- 6.4.1.6 Evonik Industries AG

- 6.4.1.7 GelTech Solutions

- 6.4.1.8 Hexion

- 6.4.1.9 Quaker Houghton (Quaker Chemical Corporation)

- 6.4.1.10 Shaw Almex Industries Ltd

- 6.4.1.11 SUEZ

- 6.4.1.12 Ecolab

- 6.4.2 System Providers

- 6.4.2.1 BossTek

- 6.4.2.2 Camfil

- 6.4.2.3 CW Machine Worx

- 6.4.2.4 Donaldson Company Inc.

- 6.4.2.5 DSH Systems Ltd

- 6.4.2.6 Duztech AB

- 6.4.2.7 Nederman Holding AB

- 6.4.2.8 SLY Inc.

- 6.4.2.9 The ACT Group

- 6.4.1 Chemical Providers

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Investments in the Chemical Sector

- 7.2 Emergence of Green Products for Dust Control

矿山粉尘抑制市场规模、份额和趋势分析报告:按产品、服务类型、最终用途、地区和细分市场预测,2025-2033年

矿山粉尘抑制市场规模、份额和趋势分析报告:按产品、服务类型、最终用途、地区和细分市场预测,2025-2033年 除尘系统和抑尘化学品市场:按产品类型、配方、最终用途产业、应用和分销管道划分-2025-2032年全球预测除尘系统市场按产品类型、动力来源、类型、分销管道和最终用户划分 - 全球预测 2025-2032

除尘系统和抑尘化学品市场:按产品类型、配方、最终用途产业、应用和分销管道划分-2025-2032年全球预测除尘系统市场按产品类型、动力来源、类型、分销管道和最终用户划分 - 全球预测 2025-2032 2025年全球除尘系统市场报告

2025年全球除尘系统市场报告 2025 年至 2033 年粉尘控制系统和抑制化学品市场报告(按化学品类型、系统类型、最终用户和地区)

2025 年至 2033 年粉尘控制系统和抑制化学品市场报告(按化学品类型、系统类型、最终用户和地区) 除尘系统市场规模、份额、成长分析、按类型、按移动性、按最终用户、按地区 - 行业预测,2025 年至 2032 年

除尘系统市场规模、份额、成长分析、按类型、按移动性、按最终用户、按地区 - 行业预测,2025 年至 2032 年 除尘系统市场:2025-2030 年预测除尘系统市场规模、份额、趋势分析报告:按产品类型、应用、地区和细分市场预测,2025 年至 2030 年

除尘系统市场:2025-2030 年预测除尘系统市场规模、份额、趋势分析报告:按产品类型、应用、地区和细分市场预测,2025 年至 2030 年 2030 年除尘系统市场预测:按产品、类型、系统、技术、应用、最终用户和地区进行的全球分析

2030 年除尘系统市场预测:按产品、类型、系统、技术、应用、最终用户和地区进行的全球分析 防尘的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2034年)

防尘的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2034年)