|

市场调查报告书

商品编码

1445945

红外线摄影机 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)IR Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

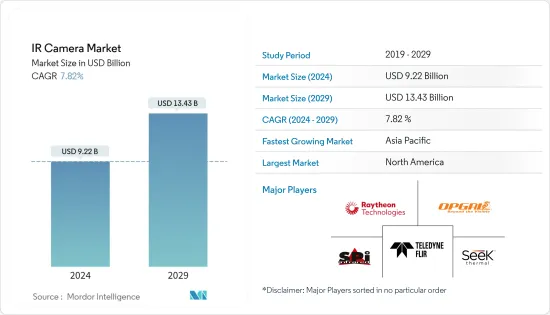

红外线摄影机市场规模预计到 2024 年为 92.2 亿美元,预计到 2029 年将达到 134.3 亿美元,在预测期内(2024-2029 年)CAGR为 7.82%。

主要亮点

- 随着未来对先进驾驶辅助系统(ADAS) 的需求不断增长以及对自动驾驶汽车的投资,红外线摄影机预计将在车辆中广泛采用。各种应用对监视的需求越来越大,包括与军事和国防、能源和商业空间相关的应用。太阳能越来越受欢迎,能源使用在全球自然资源管理策略中发挥至关重要的作用。良好的安全性至关重要,因为太阳能越来越受欢迎,而且太阳能板是一种昂贵而脆弱的商品。

- 军队对持续严格监控的需求日益增长,可能为政府使用这些解决方案提供机会。世界各国政府已大量部署无人机摄像头,覆盖约 100 公里的区域。

- 工业4.0推动了机器人等技术的发展,在工业自动化中发挥着至关重要的作用,工业中的许多核心操作都由机器人管理。 InGaAs 相机提供了新的应用,例如视觉引导机器人和自动屠宰。这些视觉引导机器人是红外线成像仪的组合,可以发现并拾取箱子中的随机零件,然后摄影机分析每个零件的方向并将它们放在传送带上。

- 短波长红外线(SWIR)在消费和汽车等终端用户领域越来越受欢迎,但它需要更多的技术进步才能使其价格合理。 ADAS 和 AV 将使用利用红外线波长的不同技术。这些技术提供了免费的资讯类型,以提供冗余并提高系统可靠性。对基于摄影机的便利功能的需求不断增长,尤其是在一些车辆中,预计将推动汽车行业对红外线摄影机的需求。

- COVID-19 对市场产生了重大影响。由于 COVID-19 被宣布为大流行病,供应链经历了相当大的中断。由于製造业活动低迷,公司倾向于取消维护,从而导致价格上涨。大流行后,大多数最终用户行业越来越多地采用红外线摄影机,对市场的成长产生了积极影响。

红外线摄影机市场趋势

冷却探测器将占据重要市场份额

- 最灵敏的红外线摄影机使用冷却探测器,场景温度变化很小。由于黑体物理学,它们提供具有高热对比度的图像,特别是在光谱的中波红外线 (MWIR) 部分。与非製冷红外线摄影机相比,增强的热差使其更容易识别目标。

- 冷却红外线热像仪能够有效地执行光谱过滤以揭示特征并进行测量,这是影响其采用的关键因素之一,而这是非冷却热像仪无法实现的。具有冷却探测器的红外线摄影机可提供更好的影像品质。与具有非冷却侦测器类型的热像仪相比,具有冷却侦测器类型的红外线热像仪具有许多优势。

- 製冷红外线探测器技术的先进发展导致了各种红外线遥感仪器的快速增长,例如高光谱遥感、空间成像和监视以及环境应用。由于低温冷却侦测器的高灵敏度,红外线系统已被开发用于对波长高达 25 μm 的各种光谱带进行成像。 2022财年,印度国防设备出口额达到1,282亿印度卢比,创同期最高水平,因而带动了军事和国防工业对红外线摄影机的需求。

- 随着技术的进步,该公司一直在开发新的创新方法来推出新型红外线摄影机。例如,2022 年 4 月,Teledyne FLIR 推出了 RS6780 远端辐射红外线摄影机,专为所有条件下的距离追踪、目标特征、户外测试和科学应用而设计。 RS6780 透过将全功能辐射红外线摄影机密封在 IP65 等级外壳内以保护其免受恶劣天气的影响,实现精确的远端测量和追踪应用。重要参与者的此类开发和创新正在推动对红外线摄影机的需求。

北美将见证显着成长

- 红外线成像对武装部队(主要是陆军、海军和空军)来说是一个福音,因为它具有昼夜工作能力和在所有天气条件下都能良好执行的能力。陆军和海军使用红外线摄影机进行边境监视和执法。它们也用于海军部门的船舶防撞和导引系统。

- 在航空业,它们大大降低了在低光源和夜间条件下飞行的风险。航空业也利用它们来识别、定位和瞄准敌军。最近,它也被纳入民航,用于飞机健康监测。

- 政府倡议,例如先进製造合作伙伴关係,旨在促使产业、各大学和联邦政府投资新兴自动化技术,将增加机器视觉系统的产量。

- 例如,2022 年 5 月,Teledyne FLIR Defense 向美国陆军交付了热成像系统。 FWS-I 系统是一种电池供电的热成像系统,可安装在不同的单兵武器系统上,以便在各种天气和照明条件下为士兵提供红外线影像。该系统还将使士兵能够透过雾、灰尘和烟雾看到东西。该公司将在马萨诸塞州比尔里卡和加州戈利塔的工厂生产 FWS-I 装置。

红外线摄影机产业概况

红外线摄影机市场本质上竞争非常激烈。高额的研发费用、合作伙伴关係和收购是该地区公司为维持激烈竞争而采取的主要成长策略。市场主要参与者包括 FLIR Systems Inc.、SPI Infrared、Opgal Optronics Industries Ltd.、Raytheon Company、Seek Thermal, Inc.、Fluke Corporation、Testo AG、HGH-Infrared、Teledyne Dalsa、DRS Technologies Inc.、InfraTec GmbH、还有很多。

2022 年 11 月,Teledyne Flir 宣布与位于华盛顿州温哥华的辅助实境穿戴解决方案开发商 RealWear 建立合作伙伴关係,成为其最新的 Thermal by Flir 合作伙伴。合作伙伴推出了首款完全免持、语音控制的热像仪模组。 Thermal by FLIR 是一项合作产品开发和行销计划,支援 OEM 製造基于 FLIR 热感摄影机模组的创新产品。

2022年9月,雷神公司与诺斯罗普格鲁曼公司合作。两家公司正在进行 DARPA 项目,以创建神经形态红外线摄影机技术。 DARPA 选择了两家公司来开展一项计划,生产新的基于事件的红外线摄影机技术,在视觉环境中传输重要资料。雷神公司和诺斯罗普·格鲁曼公司分别获得了 FENCE(基于快速事件的神经形态相机和电子设备)项目第二阶段的合同,合同金额分别为 1627 万美元和 871 万美元。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争激烈程度

- COVID-19 对红外线摄影机市场的影响

第 5 章:市场动态

- 市场驱动因素

- 各个垂直领域的监控需求不断成长

- 热像仪成本逐渐降低

- 市场挑战

- 相机功能缺乏准确性和严格的进出口法规

第 6 章:市场细分

- 透过探测器

- 冷却

- 非製冷

- 按材质

- 鎗

- 硅

- 蓝宝石

- 其他材料

- 按类型

- 短波长红外线

- 中波红外线

- 长波红外线

- 按最终用户垂直领域

- 军事与国防

- 汽车

- 工业的

- 商业及公共

- 住宅

- 其他最终用户垂直领域

- 按地理

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 亚太地区其他地区

- 世界其他地区

- 北美洲

第 7 章:竞争格局

- 公司简介

- Teledyne FLIR Systems Inc.

- SPI Infrared

- Opgal Optronics Industries Ltd.

- Raytheon Company

- Seek Thermal, Inc.

- Fluke Corporation

- Testo AG

- HGH-Infrared

- Teledyne Dalsa

- DRS Technologies Inc.

- InfraTec GmbH

第 8 章:投资分析

第 9 章:市场的未来

The IR Camera Market size is estimated at USD 9.22 billion in 2024, and is expected to reach USD 13.43 billion by 2029, growing at a CAGR of 7.82% during the forecast period (2024-2029).

Key Highlights

- With the increasing demand for advanced driver assistance systems (ADAS) in the future and investments in autonomous cars, IR cameras are expected to witness significant adoption in vehicles. There is a greater need for surveillance across various applications, including those related to the military and defense, energy, and commercial spaces. Solar energy is becoming increasingly popular, with energy use playing a critical role in the worldwide strategy to manage natural resources. Good security is essential because solar power is gaining popularity and because solar panels are an expensive and delicate commodity.

- An increasing need for continual and rigorous surveillance in the military is likely to provide an opportunity through these solutions for the use of the government. Governments worldwide have already deployed drone cameras in large numbers, covering around 100 kilometers of area.

- Industry 4.0 fueled the development of technologies like robots playing a crucial role in industrial automation, with many core operations in industries being managed by robots. InGaAs cameras offer new applications, such as vision-guided robotics and automated butchering. These vision-guided robots are a combination of IR imagers that finds and picks random parts in a bin, and then a camera analyses the orientation of each part and places them on the conveyor belt.

- Short wavelength infrared, or SWIR, is gaining popularity in end-user sectors like consumer and automotive, but it will need more technological advancement to become reasonably priced. ADAS and AV will use different technologies utilizing infrared wavelengths. These technologies offer complimentary information types to provide redundancy and boost system reliability. The increasing demand for camera-based convenience features, especially in several vehicles, is expected to fuel the demand for IR cameras in the automotive industry.

- COVID-19 impacted the market significantly. The supply chain experienced a considerable disruption owing to COVID-19 being declared a pandemic. Since manufacturing activity was low, companies were tempted to eliminate maintenance, resulting in high prices. Post-pandemic, the increasing adoption of IR cameras by most end-user industries positively impacted the markets' growth.

IR Camera Market Trends

Cooled Detectors to Hold Significant Market Share

- The most sensitive IR cameras, with only tiny variations in scene temperature, use cooled detectors. Due to blackbody physics, they provide images with high thermal contrast, especially in the spectrum's mid-wave infrared (MWIR) portion. Compared to uncooled IR cameras, the enhanced thermal difference makes it easier to identify targets.

- The ability of cooled IR cameras to effectively perform spectrum filtering to reveal features and take measurements that would otherwise be impossible with an uncooled thermal camera is one of the key factors influencing their adoption. IR cameras with cooled detectors offer better image quality. IR cameras with cooled detector types have many advantages over thermal imaging cameras with uncooled detector types.

- Advanced developments in cooled IR detector technology have led to the rapid growth of various IR remote sensing instruments like hyperspectral remote sensing, space imaging & surveillance, and environmental applications. Due to the high sensitivity of cryogenically cooled detectors, IR systems have been developed for imaging various spectral bands with wavelengths up to 25 μm. In the financial year 2022, the export value of defense equipment from India reached 128.2 billion Indian rupees, the highest during the presented period, thus driving the demand for IR cameras in the military and defense industry.

- With the advancing technologies, companies have been developing new and innovative ways to launch new IR cameras. For instance, in April 2022, Teledyne FLIR introduced the RS6780 long-range radiometric IR camera, designed for range tracking, target signature, outdoor testing, and science applications in all conditions. The RS6780 enables precision long-range measurement and tracking applications by combining a full-feature, radiometric IR camera sealed within an IP65-rated enclosure to protect it from the elements. Such developments and innovations by significant players are driving the demand for IR cameras.

North America to Witness Significant Growth

- IR imaging is a boon to the armed forces, primarily the army, navy, and air force, because of its day-night working capability and ability to perform well in all weather conditions. The army and navy use IR cameras for border surveillance and law enforcement. They are also used in ship collision avoidance and guidance systems in the naval sector.

- In the aviation industry, they have significantly mitigated the risks of flying in low light and night conditions. Aviation also uses them to identify, locate, and target enemy forces. Recently, it has also been incorporated into civil aviation for aircraft health monitoring.

- Government initiatives, such as Advanced Manufacturing Partnership, which has been undertaken to make the industry, various universities, and the federal government invest in emerging automation technologies, will increase the production of machine vision systems.

- For instance, in May 2022, Teledyne FLIR Defense delivered thermal imaging systems to US Army. The FWS-I system is a battery-operated thermal imaging system that can be mounted on different individual weapon systems to offer soldiers infrared imagery in all weather and lighting conditions. The system will also enable the soldiers to see through fog, dust, and smoke. The company will manufacture the FWS-I units at facilities in Billerica, Massachusetts, and Goleta, California.

IR Camera Industry Overview

The IR camera market is highly competitive in nature. The high expense on research and development, partnerships, and acquisitions are the prime growth strategies adopted by the companies in the region to sustain the intense competition. Key players in the market are FLIR Systems Inc., SPI Infrared, Opgal Optronics Industries Ltd., Raytheon Company, Seek Thermal, Inc., Fluke Corporation, Testo AG, HGH-Infrared, Teledyne Dalsa, DRS Technologies Inc., InfraTec GmbH, and many more.

In November 2022, Teledyne Flir announced a partnership with RealWear, Vancouver, WA, a developer of assisted reality wearable solutions, as its latest Thermal by Flir collaborator. The partners launched the first fully hands-free, voice-controlled thermal camera module. Thermal by FLIR is a cooperative product development and marketing program that supports OEMs to create innovative products based on Flir's thermal camera modules.

In September 2022, Raytheon Company collaborated with Northrop Grumman. The companies are working on a DARPA program to create neuromorphic IR camera technologies. DARPA has selected two companies to work on a program to produce new event-based IR camera technologies that transmit essential data in visual environments. Raytheon and Northrop Grumman each received contracts for Phase 2 of the FENCE (Fast Event-based Neuromorphic Camera and Electronics) program, with USD 16.27 million and USD 8.71 million awards, respectively.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the IR Camera Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Surveillance Across Various Verticals

- 5.1.2 Gradually Decreasing Costs of Thermal Cameras

- 5.2 Market Challenges

- 5.2.1 Lack of Accuracy in Camera Functionality and Stringent Import/Export Regulations

6 MARKET SEGMENTATION

- 6.1 By Detector

- 6.1.1 Cooled

- 6.1.2 Uncooled

- 6.2 By Material

- 6.2.1 Germanium

- 6.2.2 Silicon

- 6.2.3 Sapphire

- 6.2.4 Other Materials

- 6.3 By Type

- 6.3.1 Short-wavelength IR

- 6.3.2 Medium-wavelength IR

- 6.3.3 Long-wavelength IR

- 6.4 By End-user Vertical

- 6.4.1 Military and Defense

- 6.4.2 Automotive

- 6.4.3 Industrial

- 6.4.4 Commercial & Public

- 6.4.5 Residential

- 6.4.6 Other End-user Vertical

- 6.5 By Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Rest of Europe

- 6.5.3 Asia Pacific

- 6.5.3.1 China

- 6.5.3.2 India

- 6.5.3.3 Japan

- 6.5.3.4 Rest of Asia Pacific

- 6.5.4 Rest of the World

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Teledyne FLIR Systems Inc.

- 7.1.2 SPI Infrared

- 7.1.3 Opgal Optronics Industries Ltd.

- 7.1.4 Raytheon Company

- 7.1.5 Seek Thermal, Inc.

- 7.1.6 Fluke Corporation

- 7.1.7 Testo AG

- 7.1.8 HGH-Infrared

- 7.1.9 Teledyne Dalsa

- 7.1.10 DRS Technologies Inc.

- 7.1.11 InfraTec GmbH