|

市场调查报告书

商品编码

1445952

冷媒 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029 年)Refrigerants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

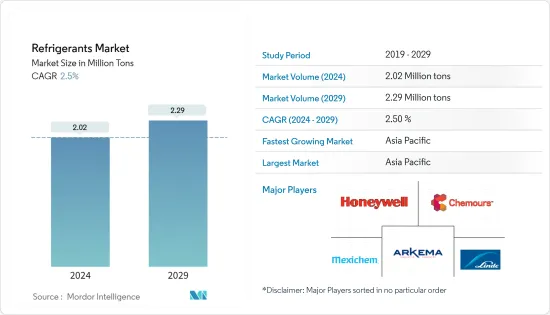

2024年冷媒市场规模预估为202万吨,预估至2029年将达229万吨,在预测期间(2024-2029年)CAGR为2.5%。

COVID-19 对市场产生了不利影响。由于大流行,所有主要製造活动都暂时停止,这最大限度地减少了对用于製冷、空调和其他应用的冷媒的需求。然而,由于所有行业生产流程的恢復,市场在 2022 年保持了成长轨迹。

主要亮点

- 推动市场的主要因素是全球冷链市场的扩张和暖通空调应用需求的增加。

- 然而,针对氟碳冷媒的严格环保法规以及《蒙特娄议定书》的不断修订可能会抑制市场。

- 绿色和低全球升温潜能值冷媒的认知和发展可能会成为未来市场成长的机会。

- 由于印度、中国和东协国家等国家的需求迅速增长,亚太地区在全球市场中占据主导地位。

冷媒市场趋势

空调应用需求不断增加

- 冷媒是一种从周围环境吸收热量的化学物质,由于这种特性而被用于冷却产品。冷媒是现代冷却系统的基本组成部分,例如空调、冰箱、冰柜、冷水机和其他应用。

- 此外,建筑业的扩张推动了商用空调市场,进而对冷媒需求的成长产生了正面影响。办公大楼、机场和地铁系统等基础设施开发活动的不断增长,导致竣工后对商用空调的需求增加。例如,2023年3月,美国政府资助了11个重大地铁项目,金额达44.5亿美元。

- 据国际能源总署称,到 2050 年,全球建筑空调库存预计将从 2022 年的 16 亿台增至 56 亿台,相当于未来 30 年每秒售出 10 台新空调。

- 根据日本冷冻空调工业协会统计,2021年北美空调设备的需求量约为1,650万台。

- 根据美国劳工统计局的数据,2021年,美国房主在窗型空调上的平均家庭支出为每消费者单位4.81美元。

- 此外,对环保冷却解决方案的需求正在推动冷水机组和空调製造商进行创新。例如,2022 年2 月,总部位于华盛顿的饮料加工和工业市场冷水机製造商和供应商Pro-Refrigeration, Inc. 提出了二氧化碳冷水机的想法,这是对全球暖化影响为零的天然冷媒.

- 对永续产品日益增长的需求促使各种製造商开发可持续产品和解决方案。

- 在全球范围内,由于便利、可支配收入增加、忙碌的生活方式等多种因素,冷冻和加工食品的消费量有所增加,这些因素增加了市场对冷媒的需求。

- 资料中心产生过多的热量,这带来了经济和环境挑战。如此严重的排放、对高效冷却的需求以及资料中心的不断发展,推动了资料中心暖通空调系统对高效能冷水机组的需求,并促进了市场的成长。

- 例如,2022年4月,Facebook母公司Meta在密苏里州和德克萨斯州启动了两个新的资料中心项目,使其在美国资料中心建设和营运的总投资接近160亿美元。资料中心数量的增加预计将显着推动冷媒市场的发展。

- 因此,预计上述因素将在未来几年对冷媒产生重大影响。

亚太地区将主导市场

- 亚太地区占据了最高的市场份额,并且很可能在预测期内主导市场。

- 中国是全球成长最快的经济体之一,由于人口、生活水平和人均收入的不断增长,几乎所有最终用户行业都经历了显着增长。

- 中国消费者越来越多地购买保健食品,包括需要冷藏的有机食品,如豌豆、玉米等。包装冷冻食品也越来越受欢迎,特别是乳製品、婴儿食品和糖果产品。

- 根据中国冷链专业委员会和智研组预测,未来中国冷链产业规模预计将进一步成长至约1,301.3亿美元。

- 由于即食包装食品的使用不断增加,许多中国消费者将冷冻电器视为家庭必需品,这为电器渗透市场铺平了道路。这种情况进一步加强了中国製冷市场的成长。

- 印度在现代是一个蓬勃发展的经济体,由于生活水平和人均收入的显着提高,这正在改变个人的选择和偏好。这些导致印度经济所有主要部门的扩大,导致该国更高的成长前景。

- 2022年4月,印度冷气销售量为175万台,是去年同期的两倍。根据两家公司的报告,Voltas 销售了 120 万台家用空调,而 LG 电子则销售了超过 100 万台家用变频空调。

- 此外,该地区不断增长的建筑活动也支撑了对冷媒的需求。中国计划在 2022 年建造 200 个机场,预计于 2035 年底竣工。中国建筑活动投资的不断增长正在推动对空调的需求,进而可能在预测期内推动冷媒市场的发展。

- 因此,上述因素预计将在未来几年推动亚太地区对冷媒的需求。

冷媒产业概况

冷媒市场已部分整合,前五大厂商占据了相当大的市场份额。主要公司包括(排名不分先后)霍尼韦尔国际公司、科慕公司、Mexichem SAB de CV、阿科玛集团和林德公司等。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 司机

- 全球冷链市场的拓展

- 建筑业对暖通空调系统的需求不断增长

- 限制

- 针对氟碳冷媒的严格环保法规

- 《蒙特娄议定书》的持续修订

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第 5 章:市场区隔(市场价值规模)

- 类型

- 碳氟化合物

- 氯氟烃 (CFC)

- 氢氯氟烃 (HCFC)

- 氢氟碳化合物 (HFC)

- 无机物

- 氨

- 二氧化碳

- 其他无机物

- 碳氢化合物

- 异丁烷

- 丙烷

- 其他碳氢化合物

- 其他类型

- 碳氟化合物

- 应用

- 冷藏

- 国内的

- 商业的

- 运输

- 工业的

- 空调

- 固定式

- 冷水机

- 移动的

- 其他应用

- 冷藏

- 地理

- 亚太

- 印度

- 日本

- 韩国

- 东协国家

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区 (MEA)

- 亚太

第 6 章:竞争格局

- 併购、合资、合作与协议

- 市占率(%)**/排名分析

- 领先企业采取的策略

- 公司简介

- A-Gas

- Arkema Group (Bostik SA)

- DAIKIN INDUSTRIES Ltd

- Dongyue Group

- Harp International Ltd

- Honeywell International Inc.

- Hudson Technologies

- Mexichem SAB de CV

- Navin Fluorine International Limited

- Sinochem Group

- SRF Limited

- The Chemours Company

- LINDE PLC

第 7 章:市场机会与未来趋势

- 绿色和低GWP冷媒的意识和发展

- 其他机会

The Refrigerants Market size is estimated at 2.02 Million tons in 2024, and is expected to reach 2.29 Million tons by 2029, growing at a CAGR of 2.5% during the forecast period (2024-2029).

COVID-19 had a detrimental effect on the market. All the major manufacturing activities were on a temporary halt owing to the pandemic scenario, which minimized the demand for refrigerants used for refrigeration, air conditioners, and other applications. However, the market retained its growth trajectory in 2022 due to the resumed production processes in all industries.

Key Highlights

- The major factors driving the market are the expansion of the global cold chain market and increasing demand for HVAC applications.

- However, stringent environmental regulations against fluorocarbon refrigerants and the continuous amendments in the Montreal Protocol are likely to restrain the market.

- The awareness and development of green and low GWP refrigerants are likely to act as an opportunity for market growth in the future.

- Asia-Pacific dominated the market across the world, owing to the rapidly growing demand from the countries like India, China and ASEAN Countries.

Refrigerants Market Trends

Increasing Demand from Air-conditioning Application

- Refrigerants are chemicals that absorb heat from their surroundings and are used in cooling products because of this characteristic. Refrigerant is a fundamental part of contemporary cooling systems, such as air conditioners, refrigerators, freezers, chillers, and other applications.

- Moreover, the expansion of the construction industry accounts for the propulsion of the commercial AC market, which in turn positively impacts the growth in demand for refrigerants. The growing infrastructure development activities, such as office complexes, airports, and metro rail systems, contribute to the increasing requirement for commercial AC after their completion. For instance, in March 2023, the United States government funded 11 major metro rail projects with an amount of USD 4.45 billion.

- According to the International Energy Agency, the global stock of air conditioners in buildings is anticipated to grow up to 5.6 billion by 2050, up from 1.6 billion in 2022, which amounts to 10 new ACs sold every second for the next 30 years.

- According to the Japan Refrigeration and Air Conditioning Industry, the demand for air conditioning devices in North America amounted to approximately 16.5 million units in 2021.

- According to the U.S. Bureau of Labor Statistics, in 2021, the mean household expenditure on window air conditioners by homeowners in the United States amounted to USD 4.81 per consumer unit.

- Additionally, the demand for environmentally friendly cooling solutions is driving chiller and air conditioner manufacturers to innovate. For instance, in February 2022, a Washington-based manufacturer and supplier of chillers for beverage processing and industrial markets, Pro-Refrigeration, Inc., developed the idea of a CO2 chiller, a natural refrigerant with zero impact on global warming.

- The increasing need for sustainable products is leading various manufacturers to develop sustainable products and solutions.

- Globally, there has been an increase in the consumption of frozen and processed food due to several factors, like convenience, an increase in disposable income, busy lifestyles, and many others, that have boosted the demand for refrigerants in the market.

- The data centers produce excessive heat, which presents an economic and environmental challenge. Such heavy emissions, the need for efficient cooling, and the increasing development of data centers have driven the demand for efficient chillers in HVAC systems in data centers and contributed to the market's growth.

- For instance, in April 2022, Meta, the parent company of Facebook, started two new data center projects in Missouri and Texas, bringing its total investment in the United States data center construction and operations to almost USD 16 billion. The increasing number of data centers is expected to significantly drive the refrigerants market.

- Therefore, the aforementioned factors are expected to have a significant impact on refrigerants in the coming years.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region accounted for the highest market share and is likely to dominate the market during the forecast period.

- China is one of the fastest-growing economies worldwide, and almost all the end-user industries have been experiencing significant growth owing to the rising population, living standards, and per capita income.

- Chinese consumers are increasingly purchasing health and wellness food products, including organic foods that require cold storage, including peas, corn, etc. Packaged frozen foods are also increasingly popular, especially dairy, baby food, and confectionery products.

- According to the China Cold Chain Committee and the Intelligence Research Group, the cold chain industry sector in China is expected to increase further to about USD 130.13 billion in the future.

- Many consumers in China are considering refrigeration appliances as household necessities owing to the increasing usage of ready-to-eat packaged food, which paves the way for appliances to penetrate the market. The scenario further strengthens the growth of the Chinese refrigeration market.

- India is a booming economy in modern times, due to significantly rising living standards and per capita income, which are changing the choices and preferences of an individual. These are resulting in the broadening of all major sectors of the Indian economy, leading to higher growth prospects in the country.

- India recorded a sale of 1.75 million units of air conditioners in April 2022, double as compared to the same period in the year prior. According to the companies' reports, Voltas sold 1.2 million units of residential ACs, while LG Electronic sold over one million units of residential inverter air conditioners.

- Moreover, rising construction activities in the region are also supporting the demand for refrigerants. China concentrated on constructing 200 airports in 2022, with completion anticipated for the end of 2035.The growing investments in construction activities in the country are driving the demand for ACs, which, in turn, may drive the refrigerants market over the forecast period.

- Therefore, the aforementioned factors are expected to boost the demand for refrigerants in the Asia-Pacific region in the coming years.

Refrigerants Industry Overview

The refrigerants market is partially consolidated, with the top five players accounting for a decent share of the market. The major companies include (not in a particular order) Honeywell International Inc., The Chemours Company, Mexichem SAB de CV, Arkema Group, and Linde PLC, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Expansion of the Global Cold Chain Market

- 4.1.2 Increasing Demand from Construction Sector for HVAC Systems

- 4.2 Restraints

- 4.2.1 Stringent Environmental Regulations against Fluorocarbon Refrigerants

- 4.2.2 Continuous Amendments in the Montreal Protocol

- 4.3 Industry Value-Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Fluorocarbons

- 5.1.1.1 Chlorofluorocarbons (CFC)

- 5.1.1.2 Hydrochlorofluorocarbons (HCFC)

- 5.1.1.3 Hydrofluorocarbons (HFC)

- 5.1.2 Inorganics

- 5.1.2.1 Ammonia

- 5.1.2.2 Carbon Dioxide

- 5.1.2.3 Other Inorganics

- 5.1.3 Hydrocarbons

- 5.1.3.1 Isobutane

- 5.1.3.2 Propane

- 5.1.3.3 Other Hydrocarbons

- 5.1.4 Other Types

- 5.1.1 Fluorocarbons

- 5.2 Application

- 5.2.1 Refrigeration

- 5.2.1.1 Domestic

- 5.2.1.2 Commercial

- 5.2.1.3 Transportation

- 5.2.1.4 Industrial

- 5.2.2 Air-conditioning

- 5.2.2.1 Stationary

- 5.2.2.2 Chiller

- 5.2.2.3 Mobile

- 5.2.3 Other Applications

- 5.2.1 Refrigeration

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 India

- 5.3.1.2 Japan

- 5.3.1.3 South Korea

- 5.3.1.4 ASEAN Countries

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Rest of the Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa (MEA)

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 A-Gas

- 6.4.2 Arkema Group (Bostik SA)

- 6.4.3 DAIKIN INDUSTRIES Ltd

- 6.4.4 Dongyue Group

- 6.4.5 Harp International Ltd

- 6.4.6 Honeywell International Inc.

- 6.4.7 Hudson Technologies

- 6.4.8 Mexichem SAB de CV

- 6.4.9 Navin Fluorine International Limited

- 6.4.10 Sinochem Group

- 6.4.11 SRF Limited

- 6.4.12 The Chemours Company

- 6.4.13 LINDE PLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Awareness and Development of Green and Low GWP Refrigerants

- 7.2 Other Opportunities

2024-2032 年按产品类型(氟碳、无机、碳氢化合物等)、应用(商业、工业、家用等)和地区分類的日本冷媒市场报告

2024-2032 年按产品类型(氟碳、无机、碳氢化合物等)、应用(商业、工业、家用等)和地区分類的日本冷媒市场报告 冷媒市场:按类型、应用分类 - 2025-2030 年全球预测

冷媒市场:按类型、应用分类 - 2025-2030 年全球预测 冷媒市场规模、份额、趋势分析报告:按产品、按应用、按地区、细分市场预测,2024-2030

冷媒市场规模、份额、趋势分析报告:按产品、按应用、按地区、细分市场预测,2024-2030 气溶胶冷媒全球市场 2024-2028

气溶胶冷媒全球市场 2024-2028 气溶胶冷媒市场报告(按产品(HFC-143a、HFC-32、HFC-125、SF6 等)、容器类型(钢、铝)、最终用途产业(住宅、商业、工业)和地区)2024-2032年

气溶胶冷媒市场报告(按产品(HFC-143a、HFC-32、HFC-125、SF6 等)、容器类型(钢、铝)、最终用途产业(住宅、商业、工业)和地区)2024-2032年 离心式冷水机组冷媒市场规模 - 按冷媒、最终用途、压缩机和预测,2024 年 - 2032 年

离心式冷水机组冷媒市场规模 - 按冷媒、最终用途、压缩机和预测,2024 年 - 2032 年 冷媒 R32 全球市场规模、份额、成长分析(按类型、按应用)- 产业预测,2024-2031 年

冷媒 R32 全球市场规模、份额、成长分析(按类型、按应用)- 产业预测,2024-2031 年 R32全球市场:市场占有率及排行榜·整体销售额及需求预测 (2024-2030年)

R32全球市场:市场占有率及排行榜·整体销售额及需求预测 (2024-2030年) 2024 年冷媒全球市场报告

2024 年冷媒全球市场报告 HFO-1234YF 2024 年世界市场报告

HFO-1234YF 2024 年世界市场报告