|

市场调查报告书

商品编码

1519949

金属黏剂:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Metal Bonding Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

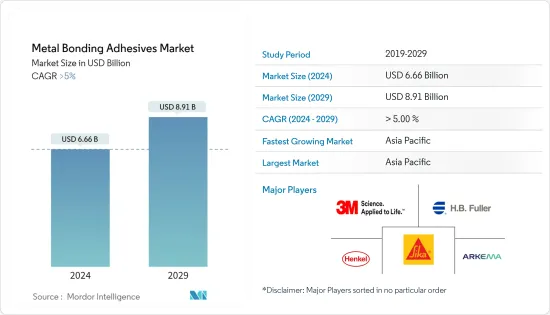

金属黏剂市场规模预计到2024年为66.6亿美元,预计到2029年将达到89.1亿美元,在预测期内(2024-2029年)复合年增长率将超过5%,预计将会如此。

COVID-19 大流行扰乱了供应链,导致生产放缓和停工以及景气衰退,对金属黏剂市场产生了重大影响。儘管 COVID-19 的最初影响是负面的,但市场预计将在预测期内復苏。

主要亮点

- 推动市场的主要因素是汽车和运输业需求的增加。

- 另一方面,由于国家之间地缘政治紧张局势加剧导致原物料价格波动正在阻碍市场成长。

- 生物基黏剂的创新发展为市场带来了新的机会。

- 亚太地区是最大的市场,由于中国、印度和日本等国家的消费量不断增加,预计亚太地区将成为预测期内成长最快的市场。

金属黏剂市场趋势

汽车和运输业的需求不断增加

- 它被汽车和运输行业的OEM广泛用于底盘结构、汽车外观、面板粘合剂、框架以及乘用车和重型车辆的加固。外饰板和麵板黏合剂是汽车领域的主要应用之一。

- 另外,在航太工业中,金属黏剂经过专门设计,具有根据使用环境设计的最大耐用性、高强度、韧性和耐温性。

- 根据OICA(国际汽车构造组织)的数据,2022年全球汽车产量约8,501万辆,较2021年的8,020.5万辆成长5.99%。 2022年,全球乘用车产量约6,000万辆,较2021年成长近7.35%。

- 亚太地区是世界上一些最有价值的汽车製造商的所在地。中国、印度、日本和韩国等新兴国家正在努力加强其製造基础并创建高效的供应链以提高盈利。

- 根据波音《2023-2042年商业展望》,到2042年,新型商用喷射机的需求预计将达到42,595架飞机,金额8兆美元。到 2042 年,全球喷射机持有几乎翻倍,达到 48,600 架,每年增长 3.5%。航空公司将用燃油效率更高的新机型替换全球约一半的机队。

- 北美地区将以 9,250 架飞机占据最大份额,其次是欧亚大陆和中国,预计到 2042 年交付9,645 架新飞机,这表明航空业的需求不断增长。

- 在中国,空中巴士公司于 2023 年 3 月宣布计划扩大其最畅销的 A320 单通道喷射机的生产并加强销售。这种扩张将显着成长金属黏剂市场,因为中国是欧洲航空公司製造商的最大市场之一,预计这些黏剂用于减轻飞机结构的重量并提高强度和抗疲劳性。

- 汽车和飞机的需求和产量的成长预计将在预测期内推动市场。

亚太地区主导市场

- 由于占据主要市场占有率的中国对技术先进的家用电器和汽车生产的需求不断增加,预计亚太地区的金属黏剂市场将出现显着而快速的成长。

- 此外,由于印度、泰国、印尼和中国拥有具有成本效益的原材料和劳动力,製造地进行了搬迁,同时跨国公司在工业和电子行业以及亚太地区的投资也不断增加。保留该地区製造地竞争日益激烈,是刺激该地区金属黏剂需求增加的核心方面。

- 中国的汽车製造业是全世界最大的。 2022年产业呈现小幅成长,产销量不断成长。 2021 年仍延续类似趋势,2022 年产量成长 3%。根据中国工业协会统计,比亚迪、上汽等企业在燃油车和电动车领域的汽车产量不断增加,汽车产量预计将持续成长。

- 根据中国工业协会的数据,中国汽车製造商预计到 2022 年将销售约 940 万辆电动和混合动力汽车汽车,高于一年前的 690 万辆。该协会也预测销售量将持续成长,到2024年将达到1,150万台。

- 例如,中国汽车巨头比亚迪2023年销售了超过300万辆电池动力汽车。其中,160万辆是纯电动车,140万辆是汽油电池混合动力汽车。合计而言,与 2022 年相比增长了 62%。此外,比亚迪报告称,去年上半年其利润增长了两倍,达到15亿美元。

- 根据《今日印度》报道,2023 年印度国内市场销量为 4,108,000 辆。这是历年销量首度突破400万台。 2022 年销量为 3,792,000 辆。在印度,马鲁蒂、现代、塔塔、本田和马恆达等主要汽车製造商因库存未售出而停止生产。预计这将在不久的将来对印度汽车生产产生重大负面影响。

- 中国拥有世界上最大的医疗保健产业之一。在「十三五」规划中,中国政府将健康和创新放在优先地位,预计预测期内对医疗设备製造业的投资将增加。此外,由于COVID-19的爆发,该国对医疗保健产业的投资逐渐增加。

- 金属黏剂在现代建筑中发挥重要作用,与焊接、铆接和螺栓连接等传统连接方法相比,具有许多优势。

- 中国的成长也得益于住宅和商业建筑业的快速扩张以及国家经济的扩张。中国正鼓励并持续推动都市化进程,预计2030年都市化率将达到70%。因此,中国等国家建筑活动的活性化预计将刺激该地区的黏剂产业。所有这些因素都会增加全部区域对黏剂的需求。

- 根据中国国家统计局的数据,到 2022 年,建筑业产值将达到 31.2 兆元(4.5 兆美元),高于 2021 年的 29.31 兆元(4.2 兆美元)。此外,根据住宅部预测,2025年后中国建筑业预计将维持GDP的6%。

- 据印度投资局称,到2025年,印度建设产业预计将达到1.4兆美元,印度建设产业跨越250子部门,并与其他行业合作,正在引进超过54项全球创新建筑技术。时代。

- 此外,在亚洲、北美和太平洋地区强劲需求的推动下,2022年韩国建筑公司的海外建筑订单连续第三年超过300亿美国。

- 因此,受上述因素影响,该地区国内金属黏剂的需求量激增。

金属黏剂产业概况

金属黏剂市场得到部分完整。主要企业(排名不分先后)包括 Henkel AG &Co.KGaA、3M、HB Fuller Company、Arkema 和 Sika AG。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究成果

- 研究场所

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 汽车和运输业的需求不断增加

- 建筑和基础设施部门的消费增加

- 其他司机

- 抑制因素

- 严格的监理政策

- 永续性问题

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章市场区隔(以金额为准的市场规模)

- 树脂型

- 丙烯酸纤维

- 环氧树脂

- 聚氨酯

- 硅胶

- 其他树脂类型(生物基树脂、混合树脂等)

- 目的

- 汽车和交通

- 航太/国防

- 电力/电子

- 工业组装

- 建筑/基础设施

- 其他用途(海洋、医疗等)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧的

- 土耳其

- 俄罗斯

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 卡达

- 埃及

- 阿拉伯聯合大公国

- 其他中东和非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Beardow Adams

- DELO Industrie Klebstoffe GmbH & Co. KGaA5

- Dow

- DuPont

- HB Fuller Company

- Henkel AG & Co. KgaA

- Huntsman International LLC

- Hexion

- ITW Performance Polymers(Illinois Tool Works Inc.)

- Parker Hannifin Corp(Lord Corporation)

- Parson Adhesives Inc.

- Sika AG

- Solvay

第七章 市场机会及未来趋势

- 生物基黏剂的创新与发展

- 转向复合黏合

The Metal Bonding Adhesives Market size is estimated at USD 6.66 billion in 2024, and is expected to reach USD 8.91 billion by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the metal bonding adhesive market by disrupting the supply chain, causing production to slow down and shut down and an economic downturn. While the initial impact of COVID-19 was negative, the market appears to be on a recovery path during the forecast period.

Key Highlights

- Major factors driving the market studied are growing demand from the automotive and transportation industry.

- On the flip side, volatility in raw material prices, due to the rising geopolitical tensions between various nations is hindering the growth of the market.

- Innovation and development of bio-based adhesives to open new opportunities for the market.

- The Asia-Pacific region represents the largest market, and it is also expected to be the fastest-growing market over the forecast period, owing to the increasing consumption from countries, such as China, India, and Japan.

Metal Bonding Adhesives Market Trends

Growing Demand from the Automotive and Transportation Industry

- Metal bonding adhesives are widely used in the automotive and transportation industry by OEMs for fabricating chassis, automotive exteriors, panel bonding, frames, and reinforcement of the passenger, as well as heavy vehicles segment. Exterior panels and panel bonding are among the top applications in the automotive segment.

- Furthermore, in the aerospace industry, metal bonding adhesives are specifically designed for maximum durability, high strength, and toughness with temperature resistance designed for their operating environment.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), in 2022, around 85.01 million vehicles were produced across the globe, witnessing a growth rate of 5.99% compared to 80.205 million vehicles in 2021, thereby indicating an increased demand for metal hoses from the automotive industry. In 2022, around 60 million passenger cars were manufactured worldwide, up nearly 7.35% compared to 2021.

- The Asia-Pacific is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, and South Korea have been working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability.

- According to the Boeing Commercial Outlook 2023-2042, the demand for new commercial jets by 2042 is expected to reach 42,595 units, valued at USD 8 trillion. The global fleet will nearly double to 48,600 jets by 2042, expanding by 3.5% annually. Airlines will replace about half of the global fleet with new, more fuel-efficient models.

- North America accounts for the largest share with 9,250 deliveries, followed byEurasia and China, with the total deliveries of new airplanes estimated to be 9,645 units by 2042, indicating rising demand from the industry.

- In China, Airbus announced plans in March 2023 to expand production of its best-selling A320 single-aisle jet and boost sales. China is one of the largest markets for European airline manufacturers, and this expansion is expected to significantly grow the metal bonding adhesives market as these adhesives are used in weight reduction and improving strength and fatigue resistance experienced by the aircraft structures.

- Over the forecast period, increasing demand and production of automotive vehicles and aircrafts are likely to drive the market.

The Asia-Pacific Region to Dominate the Market

- The Asia-Pacific metal bonding adhesives market is anticipated to witness significant and fastest growth, owing to the growing demand for technologically advanced consumer electronics and automobile production in China, which holds a significant market share.

- In addition, the relocation of manufacturing hubs due to the accessibility of cost-effective raw materials and labor in India, Thailand, Indonesia, and China, coupled with increasing investments by multinationals in the industrial and electronics sectors and growing competition among market players to hold a manufacturing base in the Asia-Pacific, is the central aspect stimulating the increasing demand for metal bonding adhesives in the region.

- The Chinese automotive manufacturing industry is the largest in the world. The industry witnessed a slight growth in 2022, wherein production and sales increased. A similar trend continued in 2021, with production witnessing a 3% incline in 2022. According to the China Association of Automobile Manufacturers (CAAM), automotive production is expected to grow in the future, with companies like BYD, SAIC Motors, and more increasing their automotive production sales in the fuel-run and electric vehicles segment.

- According to the China Association of Automobile Manufacturers, Chinese automakers are anticipated to report sales of approximately 9.4 million electric vehicles and hybrids in the previous year, up from 6.9 million in 2022. The association further projects a continued increase in sales for 2024, reaching 11.5 million units.

- For Example, China's automotive giant BYD sold over 3 million battery-powered cars in 2023, of which both batteries and gasoline power 1.6 million fully electric vehicles and another 1.4 million hybrids. Together, that is a 62 percent increase over 2022. BYD is also making money, tripling its profit to USD 1.5 billion in the first half of last year, according to BYD.

- According to India Today, 4,108,000 cars were sold in the domestic market in 2023. This was the first time during a calendar year that over 4 million units were sold in the country. In 2022, the industry witnessed sales of 3,792,000 units. In India, major automotive manufacturers, like Maruti, Hyundai, Tata, Honda, and Mahindra, have shut down their production owing to the unsold stock. This is expected to have a substantial negative impact on India's automotive production in the near future.

- China has one of the largest healthcare sectors in the world. Under the 13th Five-Year Plan, the Government of China prioritized health and innovation, which is expected to increase investments in the medical device manufacturing sector during the forecast period. Additionally, due to the COVID-19 outbreak, investment in the healthcare sector has been gradually growing in the country.

- Metal bonding adhesives play a crucial role in modern construction, offering numerous advantages over traditional joining methods like welding, riveting, or bolting.

- China's growth is also fueled by rapid expansion in the residential and commercial building sectors and the country's expanding economy. China is encouraging and enduring a continuous urbanization process, with a projected rate of 70% by 2030. As a result, increased building activity in nations like China is projected to fuel the region's adhesive industry. All such factors tend to increase the demand for adhesives across the region.

- According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.31 trillion (USD 4.2 trillion) in 2021. Moreover, as per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025.

- As per Invest India, the construction industry in India is expected to reach USD 1.4 Trillion by 2025, and the construction industry in India works across 250 sub-sectors with linkages across sectors and over 54 global innovative construction technologies identified under a Technology Sub-Mission of PMAY-U to start a new era in Indian Construction Sectors.

- Furthermore, South Korean builders' overseas building orders have surpassed 30 billion US dollars for the third consecutive year in 2022, owing to strong demand from Asia, North America, and the Pacific Ocean regions.

- Hence, owing to the factors mentioned above, the demand for metal bonding adhesives in the country has been on the rapid rise in the region.

Metal Bonding Adhesives Industry Overview

The Metal Bonding Adhesives market is partially consolidated in nature. The major players (not in any particular order) include Henkel AG & Co. KGaA, 3M, H.B. Fuller Company., Arkema and Sika AG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Automotive and Transportation Industry

- 4.1.2 Increased Consumption from Construction and Infrastructure Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Regulatory Policies

- 4.2.2 Sustainability Concerns

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resin Types (Bio-Based Resins, Hybrid, etc.)

- 5.2 Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Aerospace and Defense

- 5.2.3 Electrical and Electronics

- 5.2.4 Industrial Assembly

- 5.2.5 Construction and Infrastructure

- 5.2.6 Other Applications (Marine, Medical, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Beardow Adams

- 6.4.6 DELO Industrie Klebstoffe GmbH & Co. KGaA5

- 6.4.7 Dow

- 6.4.8 DuPont

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KgaA

- 6.4.11 Huntsman International LLC

- 6.4.12 Hexion

- 6.4.13 ITW Performance Polymers (Illinois Tool Works Inc.)

- 6.4.14 Parker Hannifin Corp (Lord Corporation)

- 6.4.15 Parson Adhesives Inc.

- 6.4.16 Sika AG

- 6.4.17 Solvay

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation and Development of Bio-based Adhesives

- 7.2 Shifting Focus Towards Adhesive Bonding for Composite Materials