|

市场调查报告书

商品编码

1521328

混凝土:市场占有率分析、产业趋势、成长预测( 喷混凝土 )Sprayed Concrete (Shotcrete) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

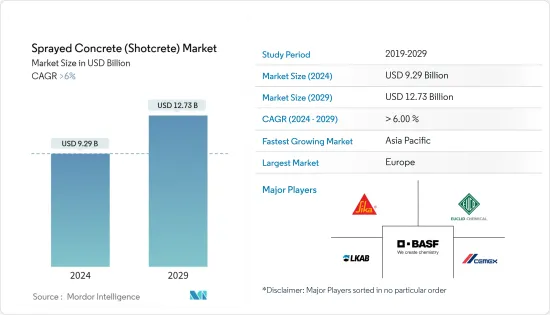

混凝土市场规模预计2024年为92.9亿美元,预计2029年将达到127.3亿美元,预测期内(2024-2029年)复合年增长率将超过6%,增长率将发生变化。

COVID-19 对混凝土市场的影响因地区、计划类型和经济状况而异。儘管最初遇到了干扰和挑战,但市场在某些地区显示出復苏甚至成长的迹象。随着疫情影响持续缓解,混凝土市场在其固有优势以及技术和应用不断进步的推动下,长期前景依然乐观。

主要亮点

- 混凝土市场由于其多功能性、强度、速度、效率、环境效益以及与全球基础设施趋势的结合,正经历建筑业不断增长的需求。

- 然而,干混凝土製程中排放的粉尘造成的环境问题对所调查的市场成长构成了挑战。

- 活性化的研发活动可能会在未来五年为喷混凝土混凝土提供机会。

- 欧洲预计将主导全球市场,亚太地区预计将成为预测期内成长最快的地区。

混凝土市场趋势

建筑业的需求增加

- 混凝土应用于各种基础设施计划。例如,它被用来沿着海岸线建造坚固的防波堤和屏障,以防止侵蚀和风暴潮。在交通领域,我们也参与跑道、航站等机场功能的建造与修復。此外,也用于建设和改善地铁、停车场等地下设施。

- 根据美国地质调查局(USGS)预测,2022年美国水泥公司将生产9,500万吨水泥,与前一年同期比较2021年的9,300万吨增加2.2%。

- 此外,美国人口普查局强调,美国建筑业产值激增,达到17,920亿美元,与前一年同期比较超过1,660亿美元。水泥产量的增加显示了混凝土市场的广阔前景,并暗示着潜在成长和机会的扩大。

- 根据中国国家统计局数据,2022年中国水泥产量近21.3亿吨,2021年为23.3亿吨,下降9%。政府宣布减产,以解决水泥产业产能过剩问题。儘管发生这种转变,持续的建筑需求以及对建筑效率和永续性的重视可能仍会推动混凝土市场的成长。

- 日本财务省公布的2022财年日本建设产业销售额约为149.8兆日圆(1.15兆美元),较上年度增长9.6%。随着建设活动的扩大,对混凝土等多功能、高效材料的需求不断增长,特别是基础设施、隧道和桥樑。

- 据印度财政部称,2023 财年建设业的实际附加价值毛额(GVA) 飙升超过 9%。另一方面,2021 财年成长-8.6%,2022 财年成长 10.7%。疫情对2021年的建设业产生了影响。然而,復苏的迹像很明显,预计将在预测期内推动混凝土市场。

- 混凝土的地下应用包括补充或更换传统支撑,例如滞后和钢架、密封岩石表面、引导水以及安装临时支撑或永久衬砌。交通运输、用水和污水领域扩张计画的大幅增加预计将推动地下建设活动。

- 所有上述因素预计将在预测期内推动混凝土(喷混凝土)市场。

亚太地区主导市场

- 根据美国地质调查局预测,2022年中国水泥产量将达21亿吨,位居世界第一,印度紧追在后,为3.7亿吨,越南则为1.2亿吨。三个主要生产国均位于亚太地区,凸显了水泥产业在全球的主导地位。

- 采矿和采石业通常需要基础设施开发,例如隧道、竖井和地下结构的建设。混凝土因其强度、耐用性和对恶劣环境的适应性而对于这些应用至关重要。

- 根据越南统计总局的数据,2022年,采矿业为GDP贡献了约268.1兆越南盾(11.65兆美元),占全国GDP总量的2.82%。这比 2021 年的 206.2 兆越南盾(8.96 兆美元)大幅成长,占 GDP 的 2.42%,成长了 30%。随着采矿和采石业的扩张,地面支撑、隧道衬砌和矿井等应用对混凝土的需求不断增加。

- 印度工业和内贸促进部报告称,到 2022 年,印度采矿业将成长约 12%。

- 此外,工业和贸易促进部表示,印度水泥产量2022财年年增长率为20.8%,2021财年为10.8%,2020财年为0.9%,反映了从疫情影响中的復苏。为正值。这种復苏趋势预计将对混凝土市场产生正面影响。

- 根据中国国家统计局预测,2022年中国建筑业产值将超过31兆元(4.61兆美元),与前一年同期比较增长10%,达到29.31兆元人民币(4.36兆美元)。与前一年同期比较稳定成长,比10年前成长了近100%。不断增长的建筑业正在将混凝土的应用范围从住宅和商业结构扩展到专业基础设施,从而推动了需求和市场范围。

- 据国土交通省称,2022财年日本民间建筑投资将达到约37.1兆日圆(2,600亿),将对混凝土市场产生重大影响。此外,预计 2023 年私人建筑投资将保持在这一水平,这表明对混凝土的需求持续增长。

- 因此,所有这些市场趋势预计将在预测期内推动亚太地区混凝土(喷混凝土)市场的需求。

混凝土产业概述

全球混凝土市场因其性质而部分整合。主要参与者(排名不分先后)包括 Sika、 BASF SE、Euclid Chemical Company、Cemex 和 LKAB Berg & Betong。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 建筑业的需求增加

- 采矿和隧道开挖的增加

- 其他司机

- 抑制因素

- 混凝土的成本高于传统混凝土或预製混凝土

- 干燥过程中产生的粉尘所造成的环境问题

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

第五章市场区隔(以金额为准的市场规模)

- 流程

- 湿喷

- 干喷

- 最终用户产业

- 基础设施

- 采矿和隧道挖掘

- 维修和维修

- 其他最终用户(航太/国防、住宅/商业建筑、环境应用)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- BASF SE

- Cemex

- Custom Crete

- Ductal

- HeidelbergCement

- JE Tomes & Associates Inc.

- LKAB Berg & Betong

- Sika

- Target Products Ltd

- The Euclid Chemical Company

- The QUIKRETE Companies

第七章 市场机会及未来趋势

- 活性化研发活动

- 其他机会

The Sprayed Concrete Market size is estimated at USD 9.29 billion in 2024, and is expected to reach USD 12.73 billion by 2029, growing at a CAGR of greater than 6% during the forecast period (2024-2029).

The COVID-19 impact on the sprayed concrete market varied depending on the region, project type, and economic conditions. While initial disruptions and challenges were significant, the market showed signs of resilience and even experienced some growth in specific areas. As the pandemic's effects continue to moderate, the long-term outlook for the sprayed concrete market remains positive, driven by its inherent advantages and continued advancements in technology and applications.

Key Highlights

- The sprayed concrete market is driven by increasing demand from the construction sector by the combination of its versatility, strength, speed, efficiency, environmental benefits, and alignment with global infrastructure development trends.

- However, the environmental issues arising from the dust released in the dry-sprayed concrete process pose challenges to the studied market growth.

- Increasing research and development activities are likely to provide opportunities for the sprayed concrete (shotcrete) market over the next five years.

- Europe dominated the market across the globe and Asia-Pacific is expected to be the fastest-growing region over the forecast period.

Sprayed Concrete Market Trends

Increasing Demand From Construction Sector

- Sprayed concrete finds applications in a range of infrastructure projects. For instance, it's used to create strong seawalls and barriers along coastlines to protect against erosion and storm surges. Additionally, in the realm of transportation, it plays a role in constructing and fixing airport features like runways and terminals. Moreover, it's employed in the construction and improvement of underground facilities such as metro systems and parking garages.

- US cement companies produced 95Mt of cement in 2022, up by 2.2% year-on-year from 93Mt in 2021, according to the United States Geological Survey (USGS).

- Additionally, the US Census Bureau highlighted a surge in U.S. construction output, reaching USD 1,792 billion, up by over USD 166 billion from the previous year. This uptick in cement production signals promising prospects for the sprayed concrete market, suggesting potential growth and expanded opportunities.

- As per the National Bureau of Statistics of China, in 2022, the production volume of cement in China amounted to almost 2.13 billion metric tons and 2.33 billion metric tons in 2021 a 9% decline. The government announced to reduce the output, in order to address the production overcapacity in the cement sector. Despite this shift might still stimulate growth in the sprayed concrete market due to ongoing construction demands and an emphasis on construction efficiency and sustainability.

- In fiscal year 2022, Japan's construction industry, as per the Ministry of Finance, saw sales of about JPY 149.8 trillion (USD 1.15 trillion), a 9.6% rise from the previous year. With growing construction activities, there's heightened demand for versatile and efficient materials like sprayed concrete, especially for infrastructure, tunnels, and bridges.

- According to the Ministry of Finance (India), the real gross value added (GVA) in the construction industry in FY2023 surged by over 9%. In contrast, there were contractions of -8.6% in FY2021 and a growth of 10.7% in FY2022. The pandemic impacted the construction sector in 2021. However, signs of recovery are evident and expected to drive the sprayed concrete market during the forecast period.

- Underground applications of shotcrete include supplementing or replacing conventional support materials, such as lagging and steel sets, sealing rock surfaces, channeling water flows, and installing temporary support and permanent linings. Significantly growing expansion programs within the transportation and water/wastewater sectors are expected to provide a boost to the underground construction activities.

- All the aforementioned factors are expected to drive the sprayed concrete (shotcrete) market during the forecast period.

Asia-Pacific Region to Dominate the Market

- In 2022, According to the US Geological Survey, global cement production showed China as the leading producer with 2,100 million metric tons, followed by India at 370 million metric tons, and Vietnam at 120 million metric tons. All three leading producers are from the Asia-Pacific region, highlighting its dominance in the cement industry on a global scale.

- The mining and quarrying sector often requires infrastructure development for operations such as building tunnels, shafts, and underground structures. Sprayed concrete is essential in these applications due to its strength, durability, and adaptability to challenging environments.

- According to the General Statistics Office of Vietnam, in 2022, the mining and quarrying sector contributed approximately VND 268.1 trillion (USD 11.65 trillion) to the GDP, making up 2.82% of the nation's total GDP. This marks a significant rise from VND 206.2 trillion (USD 8.96 trillion), or 2.42% of the GDP, in 2021, indicating a 30% increase. With the expansion of the mining and quarrying sector, there is an increased demand for sprayed concrete in applications such as ground support, tunnel linings, and mine shafts.

- India's mining industry witnessed a growth of approximately 12% in FY2022, as reported by the Department for Promotion of Industry and Internal Trade (India).

- Additionally, as indicated by the Department for Promotion of Industry and Internal Trade (India), the annual growth rate for cement production in India saw positive shifts: 20.8% in FY2022, -10.8% in FY2021, and -0.9% in FY2020, reflecting a rebound from the pandemic's effects. This recovery trajectory is expected to have a positive impact on the Sprayed Concrete Market.

- As per the National Bureau of Statistics of China, the construction industry in China generated an output of over CNY 31 trillion (USD 4.61 trillion) in 2022, representing an increase of 10% of CNY 29.31 trillion (USD 4.36 trillion) compared to the previous year and there is an increase of almost 100% from a decade ago with a steady growth y-o-y. The growing construction sector broadens sprayed concrete's applications, from residential and commercial structures to specialized infrastructure, boosting its market demand and reach.

- According to MLIT (Japan), private sector building construction investment in Japan reached approximately JPY 37.1 trillion (USD 0.26 trillion) in fiscal year 2022, significantly influencing the sprayed concrete market. Additionally, projections suggest that private investment in building construction will maintain this level into fiscal 2023, indicating a sustained demand for sprayed concrete.

- Hence, all such market trends are expected to drive the demand for the sprayed Concrete (shotcrete) market in the Asia-Pacfic region during the forecast period.

Sprayed Concrete Industry Overview

The global sprayed concrete market is partially consolidated in nature. The major players (not in any particular order) include Sika, BASF SE, The Euclid Chemical Company, Cemex, and LKAB Berg & Betong among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Construction Sector

- 4.1.2 Growing Mining and Tunnel Activities

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Sprayed Concrete is Costlier than Traditional and Precast Concrete Types.

- 4.2.2 Environmental Issues Arising from the Dust Released in Dry Process

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Process

- 5.1.1 Wet Spraying

- 5.1.2 Dry Spraying

- 5.2 End-User Industry

- 5.2.1 Infrastructure

- 5.2.2 Mining and Tunneling

- 5.2.3 Repair and Rehabilitation

- 5.2.4 Other End Users (Aerospace And Defense, Residential and Commercial Construction, and Environmental Applications)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Cemex

- 6.4.3 Custom Crete

- 6.4.4 Ductal

- 6.4.5 HeidelbergCement

- 6.4.6 JE Tomes & Associates Inc.

- 6.4.7 LKAB Berg & Betong

- 6.4.8 Sika

- 6.4.9 Target Products Ltd

- 6.4.10 The Euclid Chemical Company

- 6.4.11 The QUIKRETE Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing R&D activities

- 7.2 Other Opportunities